In-Depth Notes on Accounting: Nature, Purpose, and Principles

Accounting System Overview

Organizations operate using resources including labor, materials, services, buildings, and equipment.

These resources require financing and information about their amounts and results.

Accounting is the system that provides necessary information to both internal and external parties.

Types of Organizations

For-Profit Organizations: Focus primarily on earning profit.

Nonprofit Organizations: Aim to provide services (governing, education).

Both types require accounting to understand resource management.

Information Needs

Organizations, though different, generally share similar information needs.

Example: Varsity Motors, Inc.

Operates as an automobile dealership.

Needs information on resources, financing, and results.

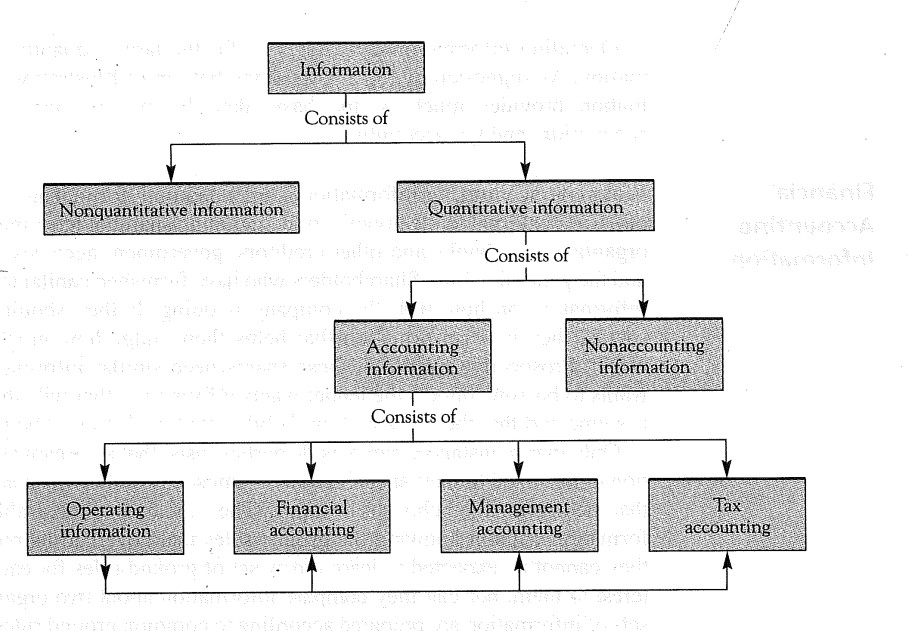

Information Classification

Accounting information can be quantitative or nonquantitative.

Quantitative: Expressed in numbers (e.g., monetary terms).

Nonquantitative: Descriptive (e.g., visual impressions).

Key categories of needed information include:

Operating Information

Financial Accounting Information

Management Accounting Information

Tax Accounting Information

Operating Information

Crucial for day-to-day activities (e.g., payroll, inventory management).

Involves details necessary for the functioning of the organization.

Financial Accounting

Aimed at both managers and external stakeholders (shareholders, creditors).

Important for assessing company performance and reliability for decisions.

Management Accounting

Used internally to aid managers in:

Planning: Deciding future actions (includes budgeting).

Implementation: Machinery to enact plans with supervision.

Control: Monitoring performance against budgets and plans.

Concept of Accounting

Defined as the process of identifying, measuring, and communicating economic information for informed judgments.

A central function is to provide data to facilitate management decision-making.

Role of Accounting Professionals

Accounting staff includes bookkeepers and CPAs (Certified Public Accountants).

CPAs subject to regulation for public companies include the SEC and PCAOB.

Accounting Principles

Based on generally accepted accounting principles (GAAP) in the U.S. managed primarily by the FASB.

Principles are established by ongoing dialogues within the profession and adapt to meet changing societal needs.

Financial Statements

Major outputs of accounting:

Balance Sheet: Snapshot of assets, liabilities, and owners' equity.

Income Statement: Reports revenues, expenses, and profit/loss.

Statement of Cash Flows: Tracks cash inflow and outflow.

Balance Sheet Components

Assets: Resources owned (e.g., cash, equipment).

Liabilities: Obligations (debts owed).

Owners' Equity: Residual interest in assets after liabilities are deducted.

Income Statement Components

Revenues: Income earned from sales.

Expenses: Costs incurred to earn revenue.

Net Income: What remains after expenses are subtracted from revenues.

Financial Statement Objectives (FASB)

Useful to investors and creditors for decisions.

Comprehensible to those with basic business knowledge.

Focus on economic resources and claims.

Reflect performance over time.

Estimate future cash receipts and obligations.

Sarbanes-Oxley Act

Requires CEOs and CFOs to certify the accuracy of financial statements to ensure accountability.

Differences in Accounting Approaches

Differences exist between GAAP and tax accounting, which can lead to discrepancies in reported income for tax versus financial reporting.