Chapter 6A

Real Exchange Rate and Short Run Equilibrium

Because of shortcomings of PPP, economists try to generalise monetary approach to PPP to make a better theory.

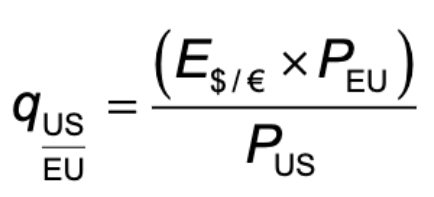

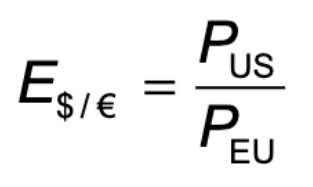

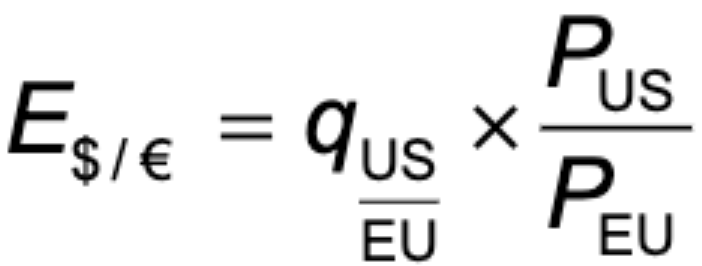

The real exchange rate is the rate of exchange (relative value/price/cost) for goods + services across countries;

e.g. the dollar price of European basket of goods + services relative to dollar price of American basket is;

If the EU basket costs €100, the US basket costs $120, and the nominal exchange rate is $1.20/€;

then real ex rate is 1 US basket per 1 EU basket.

A decrease in demand for US goods causes real depreciation in their value;

causes fall in dollar′s purchasing power of EU goods relative to dollar′s purchasing power of US goods.

implies that US goods become less expensive + less valuable relative to EU goods.

An increase in demand for US goods causes real appreciation in their value;

causes rise in dollar’s purchasing power of EU goods relative to dollar’s purchasing power of US goods.

implies that US goods become more expensive + more valuable relative to EU goods.

According to the more general real exchange rate approach, exchange rates may also be influenced by the real exchange rate:

According to the more general real exchange rate approach, exchange rates may also be influenced by the real exchange rate:

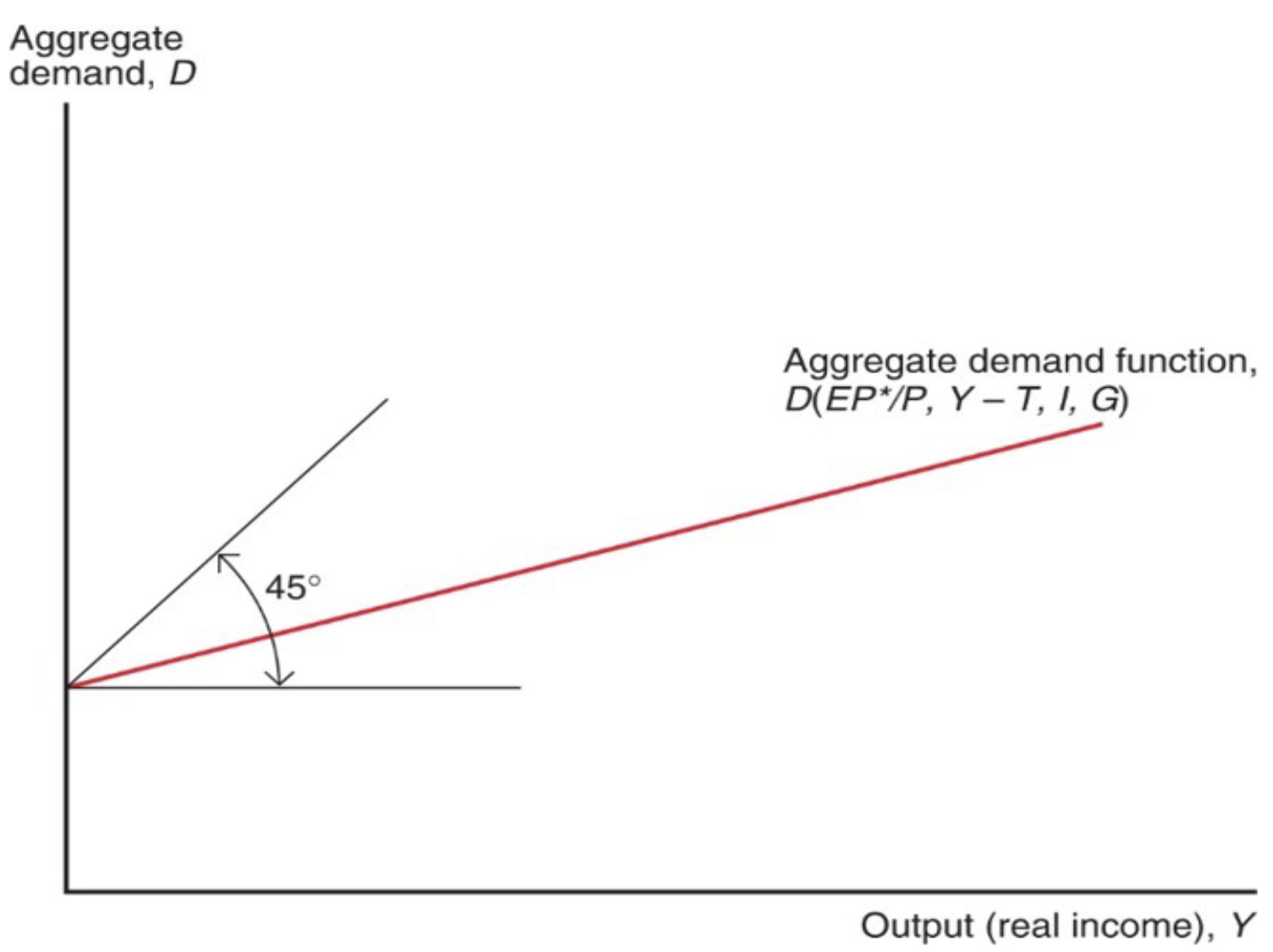

Determinants of Aggregate Demand

Aggregate demand is the aggregate goods + services individuals and institutions are willing to buy:

consumption expenditure

investment expenditure

government spending

net expenditure by foreigners (current account)

Determinants of aggregate demand include:

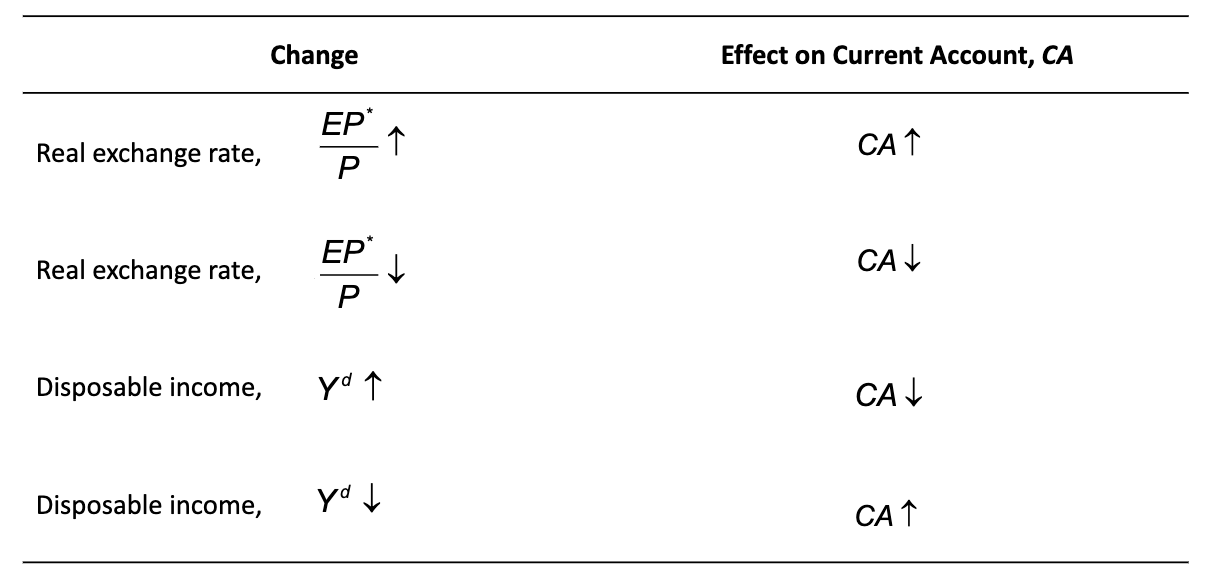

Real exchange rate: increase in real exchange rate increases current account;

therefore increases aggregate demand for domestic goods.

Disposable income: increase in disposable income increases consumption expenditure; but decreases current account.

since usually, consumption expenditure > expenditure on foreign goods; first effect dominates the second effect

as income increases for given level of taxes; aggregate consumption expenditure + aggregate demand increase by less than income.

Determinants of consumption expenditure include:

Disposable income: income from production (Y) — taxes (T).

More disposable income = more consumption expenditure

but, typically consumption increases less than disposable income increases.

Real interest rates and wealth may influence saving and spending on consumption goods;

but, we assume they are relatively unimportant here.

Determinants of investment expenditure + govt puchases include:

For simplicity, we assume;

exogenous political factors determine govt spending (G) and taxes (T)

exogenous business decisions determine investment expenditure (I)

more complicated model shows investment depends on cost of

spending or borrowing to finance investment (interest rate).

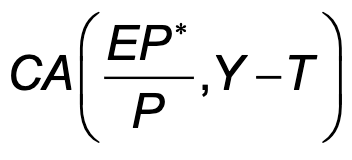

Determinants of the current account include:

Real exchange rate: prices of foreign goods relative to prices of domestic goods (both measured in the domestic currency):

As prices of foreign goods rise relative to domestic goods;

expenditure on domestic goods rises;

expenditure on foreign products falls.

Disposable income: more disposable income = more expenditure on foreign goods (imports).

Factors Determining the Current Account

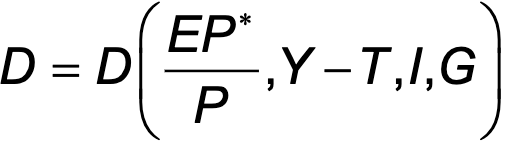

Aggregate demand is therefore expressed as:

where C (Y — T) is consumption expenditure as a function of disposable income,

where C (Y — T) is consumption expenditure as a function of disposable income,

I + G is investment expenditure + govt spending (both exogenous),

is the current account as a function of the real exchange rate + disposable income.

is the current account as a function of the real exchange rate + disposable income.

Or more simply:

How Real Exchange Rate Changes Affect the Current Account

The current account measures value of exports relative to value of imports:

When the real exchange rate rises, prices of foreign goods rise relative to prices of domestic goods.

When the real exchange rate rises, prices of foreign goods rise relative to prices of domestic goods.

volume of exports bought by foreigners rises.

volume of imports bought by domestic residents falls.

value of imports of domestic goods rises:

value/price of imports rises (since foreign products are more valuable/expensive).

When real exchange rate changes, if volumes of imports + exports do not change much, value effect may dominate volume effect.

e.g. contract obligations to buy fixed amounts of products may cause volume effect to be small.

However, evidence shows that for most countries, volume effect dominates value effect after 1 year or less.

Assume for now a real depreciation leads to increase in the current account:

volume effect dominates value effect.

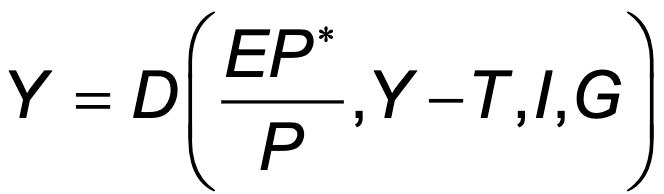

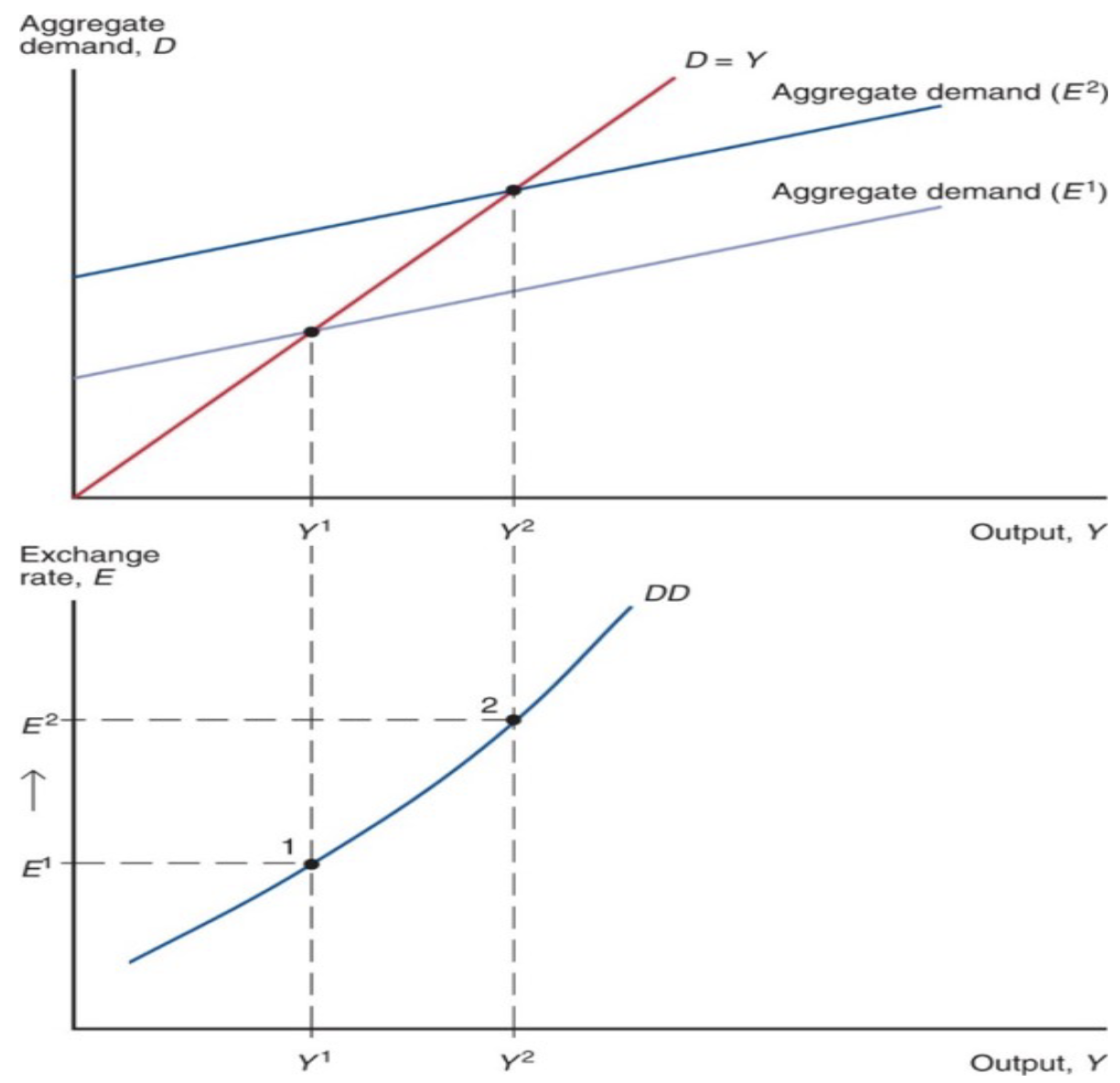

Aggregate Demand as a Function of Output

Short-Run Equilibrium for Aggregate Demand and Output

Equilibrium is achieved when the value of output + income from production Y equals the value of aggregate demand D;

where aggregate demand is a function of the real ex rate, disposable income, investment expenditure, and govt spending.

Determination of Output in the Short Run

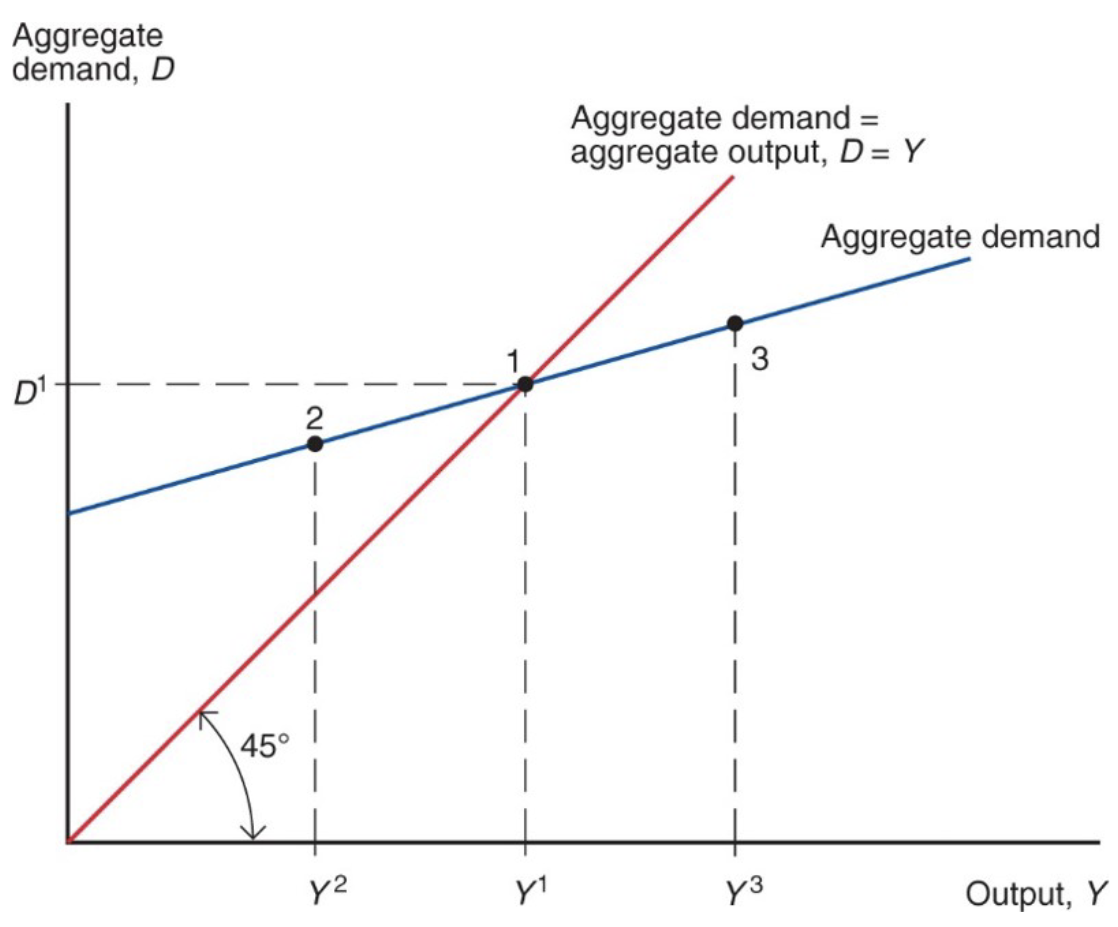

Short-Run Equilibrium and the Exchange Rate: DD Schedule

How does the ex rate affect the short-run equilibrium of AD and output?

With fixed domestic + foreign average prices, a rise in the nominal ex rate (domestic currency depreciation);

makes foreign products more expensive relative to domestic products

thus, increases AD for domestic products

in equilibrium, production will increase to match higher AD

Output Effect of a Currency Depreciation with Fixed Output Prices

Deriving the DD Schedule

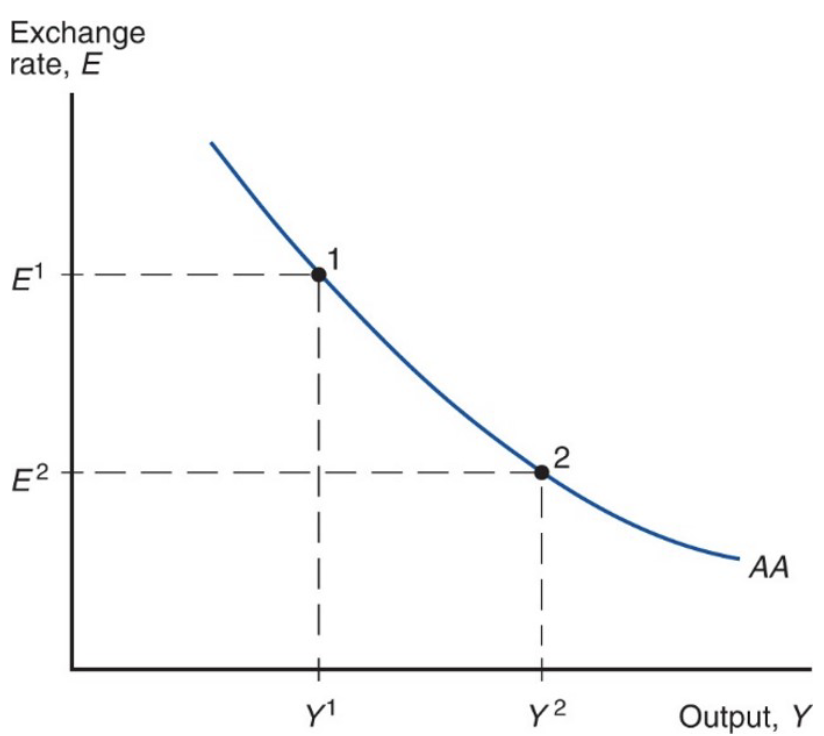

Short-Run Equilibrium and the Exchange Rate: DD Schedule

DD schedule shows combinations of output + ex rate where output market is in short-run equilibrium (AD = aggregate output);

DD curve slopes upward because rise in ex rate causes AD + aggregate output to also rise.

Shifting the DD Curve

Changes in the ex rate causes movements along the DD curve

Other changes cause it to shift:

Changes in G: more govt spending causes higher AD + output in equilibrium. Output increases for every ex rate: the DD curve shifts right.

Changes in T: lower taxes generally increases consumption, increasing AD + output in equilibrium for every exchange rate: the DD curve shifts right.

Changes in I: higher investment shifts the DD curve right.

Changes in P: higher domestic prices make domestic output more expensive compared to foreign output + reduce net export demand, shifting the DD curve left.

Changes in P * : higher foreign prices make domestic output less expensive compared to foreign output + increase net export demand, shifting the DD curve right.

Changes in C: willingness to consume more and save less shifts the DD curve right.

Changes in demand of domestic goods relative to foreign goods: willingness to consume more domestic goods compared to foreign goods shifts the DD curve right.

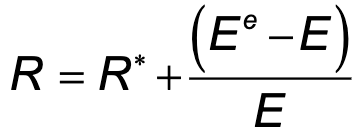

Short-Run Equilibrium in Asset Markets

Consider two sets of asset markets:

Foreign exchange markets

interest parity represents equilibrium:

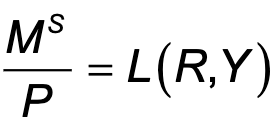

Money market

Equilibrium occurs when the QS of real monetary assets = the QD of real monetary assets:

A rise in income from production causes demand for real monetary assets to increase.

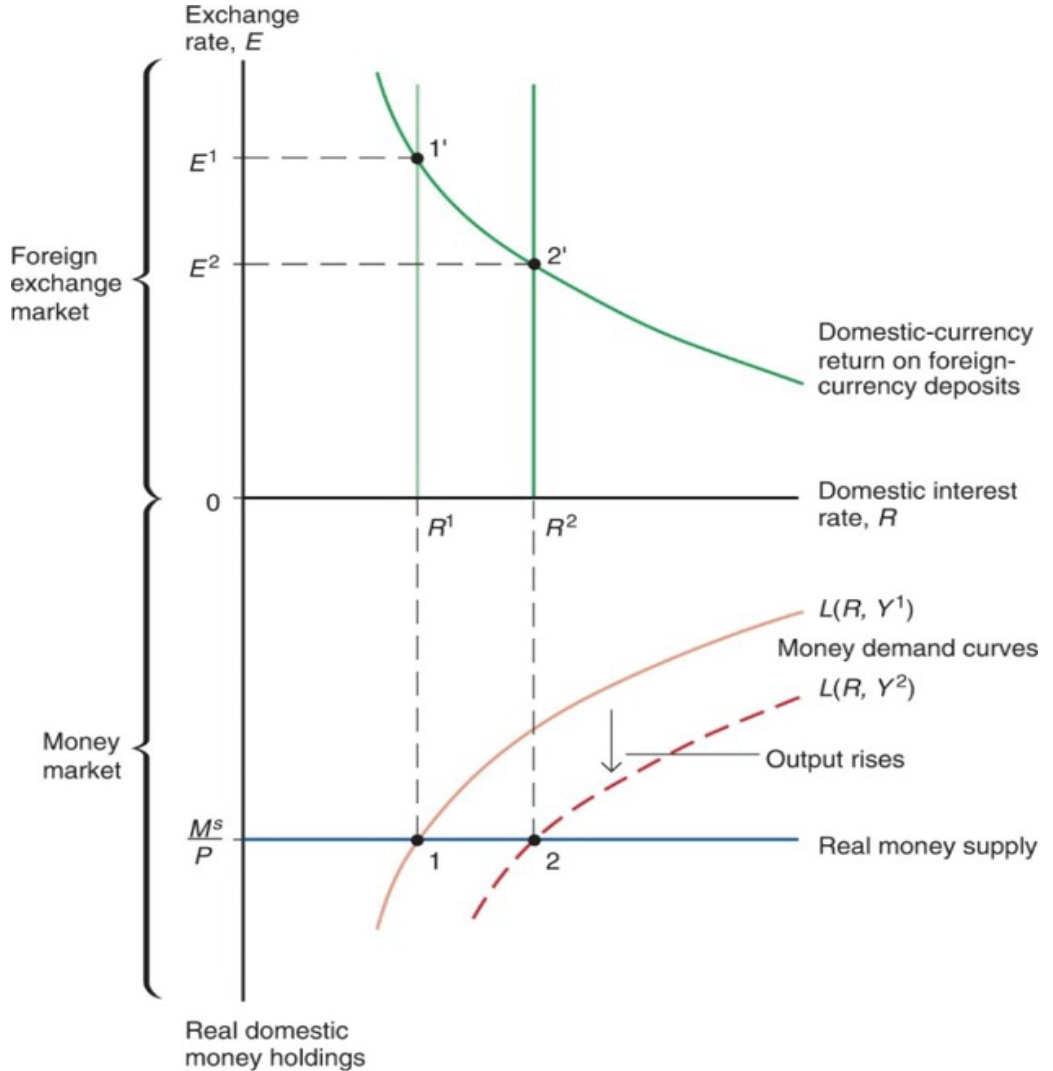

Output and the Exchange Rate in Asset Market Equilibrium

Short-Run Equilibrium in Asset Markets

When income + production increase;

demand for real monetary assets increases,

leading to increase in domestic interest rates,

leading to appreciation in domestic currency.

An appreciation in the domestic currency is shown by fall in E;

when income + production decrease, domestic currency depreciates and E rises.

Short-Run Equilibrium in Asset Markets: The AA Schedule

Shifting the AA Curve

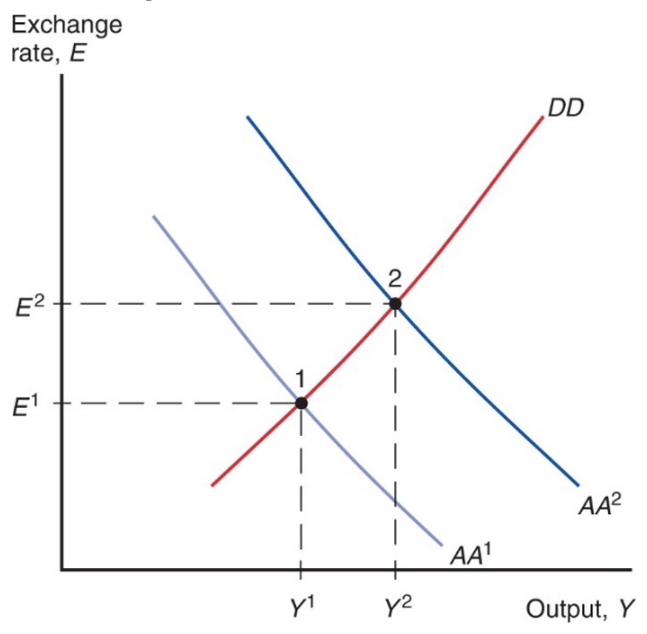

Changes in Mˢ : an increase in money supply reduces interest rates in the short run; causes domestic currency to depreciate for every output: AA curve shifts right.

Changes in P: an increase in average domestic prices decreases supply of real monetary assets; increases interest rates causing domestic currency to appreciate: AA curve shifts left.

Changes in Eᵉ : if market participants expect domestic currency to depreciate in the future; foreign currency deposits become more attractive, causing domestic currency to depreciate in short run: AA curve shifts right.

Changes in R * : an increase in the foreign interest rates makes foreign currency deposits more attractive, leading to depreciation in domestic currency: AA curve shifts right.

Changes in the demand of real monetary assets: if domestic residents are willing to hold less real money assets and more non-monetary assets; interest rates on non-monetary assets would fall, leading to depreciation in domestic currency: AA curve shifts up right.

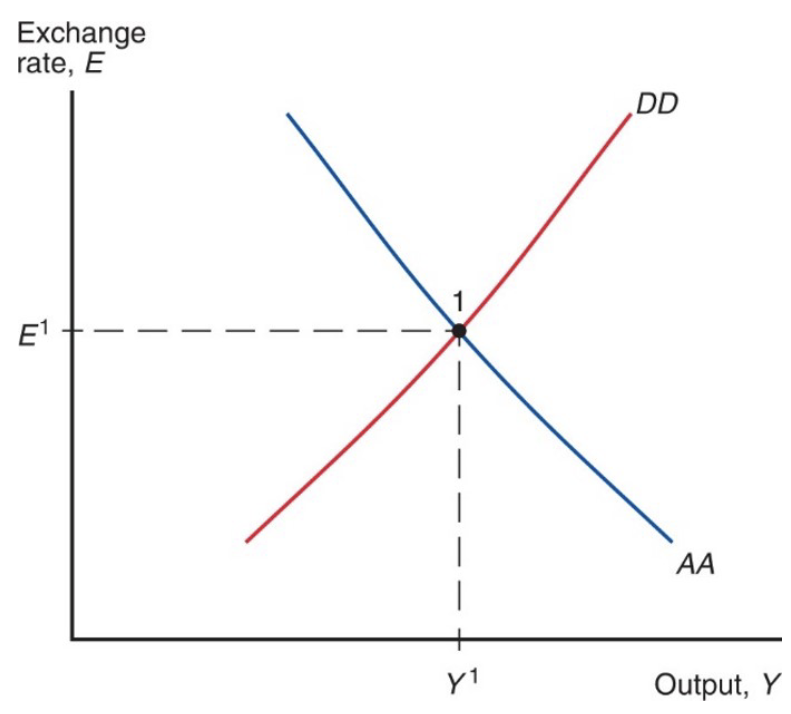

Putting the Pieces Together: the DD and AA Curves

A short-run equilibrium means a nominal ex rate + output level such that:

equilibrium in output markets holds: AD = aggregate output.

equilibrium in foreign ex markets holds: interest parity holds.

equilibrium in money market holds: QS of real monetary assets = QD of real monetary assets.

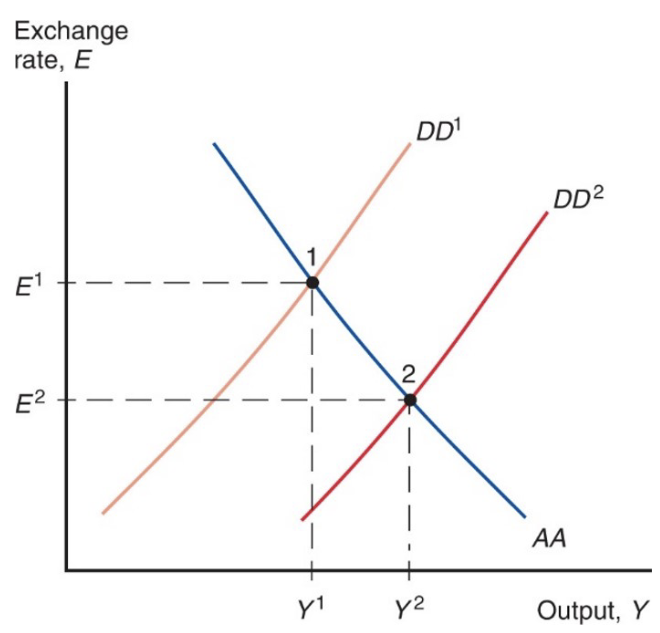

A short-run equilibrium occurs at the intersection of DD and AA curves:

output markets are in equilibrium on the DD curve

asset markets are in equilibrium on the AA curve

Short-Run Equilibrium: The Intersection of DD and AA

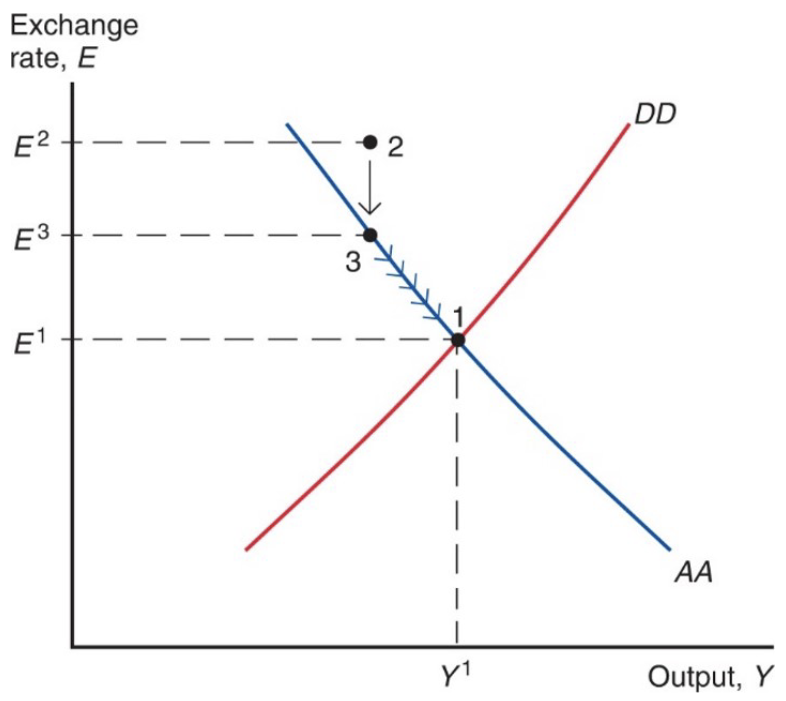

How the Economy Reaches Its Short-Run Equilibrium

Temporary Changes in Monetary and Fiscal Policy

Temporary policy changes are expected to be reversed in the near future;

thus, they don’t affect expectations about ex rates in the long run.

Monetary policy: central bank influences supply of monetary assets; assumed to affect asset markets first.

An increase in QS of monetary assets lowers interest rates in the short run, causing domestic currency to depreciate.

domestic products are cheaper relative to foreign products, so AD + output increase:

Fiscal policy: govts influence spending and taxes; assumed to affect AD + output

first.

An increase in govt spending or decrease in taxes (expansionary policy) increases AD + output in the short run.

DD curve shifts right.

higher output increases demand for real monetary assets therefore ;

increasing interest rates,

causing domestic currency to appreciate.