Job Cost Accounting Review

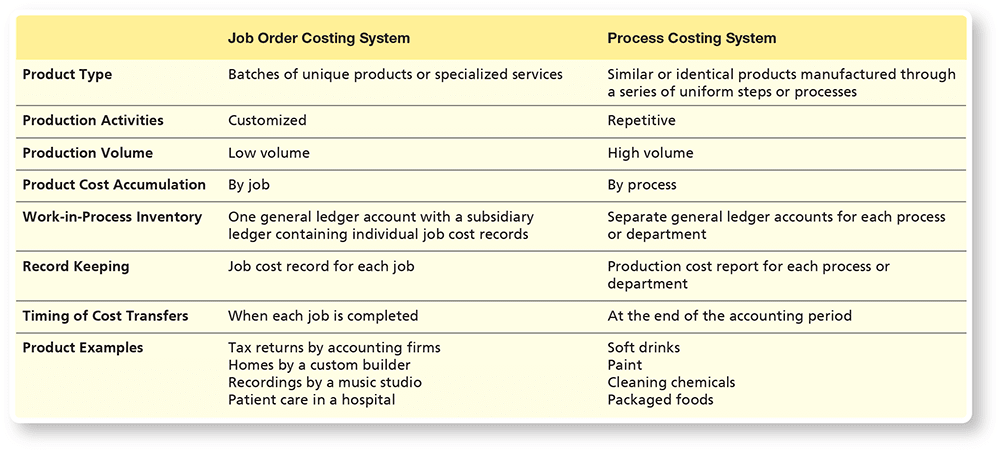

A job order costing system tracks the costs of batches of unique products or specialized services as they are produced. The relative volume of production of a company that utilizes a ob order costing is low when compared to the high volume of mass production tracked by a process costing system.

- VS -

Process costing utilizes repetitive production activities while a job order cost system relies on customized production activities. In a job order costing system, the timing of cost transfers happens when each job is completed as opposed to process costing where cost transfers happen at the end of an accounting period.

Study Concepts: Review

An overallocated amount means there is a credit balance of $2,000 in the Manufacturing Overhead account. To close out the Manufacturing overhead account, there would need to be a debit entry to Manufacturing Overhead (for the $2,000 balance). The credit entry would be to Cost of Goods Sold.

All actual manufacturing overhead costs incurred are debited to the Manufacturing Overhead account. Applied overhead (i.e., 20% of direct labor costs) is not debited to the Manufacturing Overhead account as it is debited to Work-in-Process and credited to Manufacturing Overhead. Depreciation on plant assets is debited to Manufacturing Overhead but not the depreciation on assets outside of the production area - such as the depreciation on the computers used in the accounting and finance department. Since cleaning supplies are an indirect cost of manufacturing, their cost is debited to Manufacturing Overhead.

Sample Q&A:

White Company manufactures furniture. Assume the following information:

Manufacturing overhead is allocated based on machine hours.

Manufacturing overhead is estimated to be $150,000 and machines hours are expected to be 10,000 hours.

The actual manufacturing overhead is $31,000 and there are 2,000 actual machine hours.

How much manufacturing overhead would White Company allocate?

First, determine the predetermined overhead allocation rate.

Predetermined overhead allocation rate | = Total estimated overhead cost / Total estimated quantity of the overhead allocation base |

| = $150,000 / $10,000 |

| = $15.00 per machine hour |

Then calculate the allocated manufacturing overhead cost.

Allocated manufacturing overhead cost | = Predetermined overhead allocation rate x actual quantity of the allocation |

| = $15.00 x 2,000 actual machine hours |

| = $30,000 |

The major features of a just in time production feature are:

Lower inventory costs

Ability to respond quickly to changes in customer needs

More space available for production

Lean management systems are long-term approaches to improving efficiency and quality.