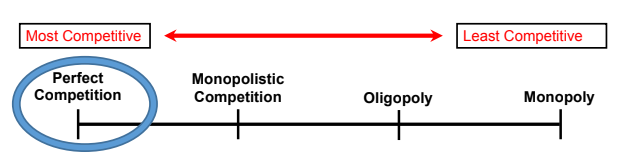

4b. Perfect competition

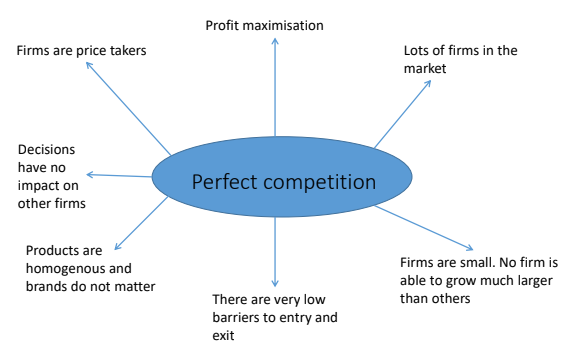

Price taking refers to firms taking the price from industry price due to supply and demand

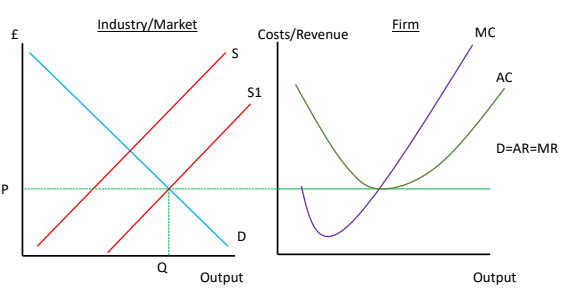

Perfect competition: The demand in perfect competition is perfectly elastic. If a firm was to raise the price then no one would demand their product. If they were to lower it they would not be able to supply sufficiently for the demand. Each unit of output sold brings in the same additional revenue as the unit before.

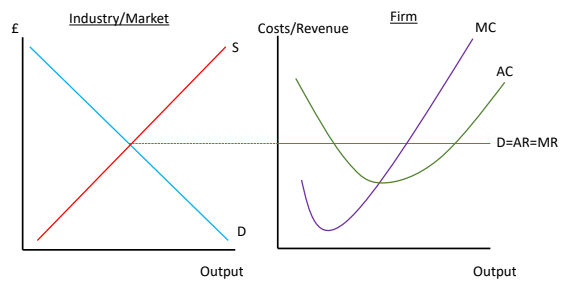

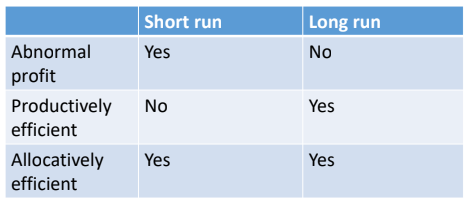

Short run: In the short run firms can make abnormal (supernormal) profit. The price is set by the market supply and demand and the firm (a price take in perfect competition) must sell at this price. If the D=AR=MR curve is above the AC curve then this creates an area of profit.

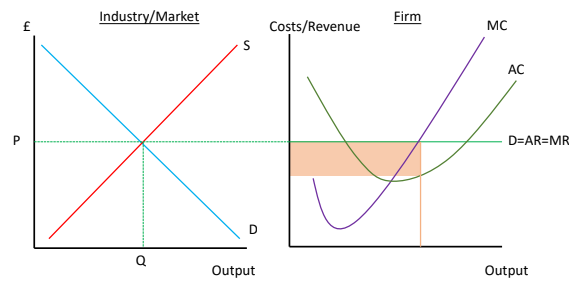

Long run: In the long run more firms will be attracted by the abnormal profits and enter into the market (made possible due to the low barriers to entry). This causes industry/market supply to shift to the right lowering the market price and subsequently the price of the firm so that it makes only normal profit.

Shut down point

The shut-down price is said to occur whenever price < average variable cost (P<AVC). For a firm to justify continuing production in the short run it needs to sell at a price that at least covers the variable costs of production.

In the long run a minimum of normal profit is needed to remain in a market for a particular product. This occurs when P=AC (i.e. the price covers both fixed and variable costs).

Is perfect competition realistic?

Very few markets meet the standards of perfect competition

However it useful as an ideal against which real life markets can be assessed.

If a market is very far away from the model of perfect competition, the government may wish to intervene to improve the market.

Explain how a perfectly competitive market moves to its long run equilibrium. (4 marks)

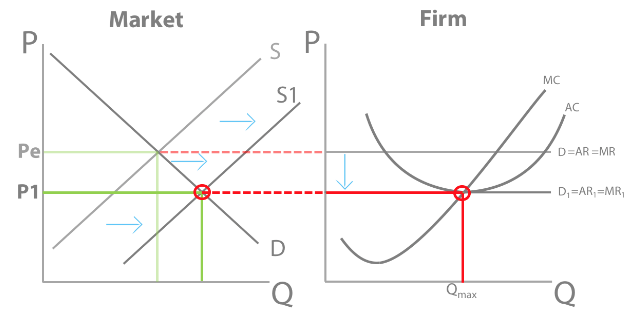

In the long run, perfect information means potential sellers outside the market will see the opportunity to make supernormal profit by entering the market.

There are no barriers to entry, so new firms will enter the market, increasing supply and decreasing price until AR touches the bottom of the firm’s AC and all the supernormal profit is gone.

New firms will no longer enter the market because they can no longer make supernormal profit, so we have reached the long run equilibrium.

Explain how a perfectly competitive market, where firms are making a short run loss, moves to its long run equilibrium. (4 marks)

If firms are making a short run loss, they will leave the market and this is easy to do because there is no barriers to exit.

As firms leave the market, supply decrease and prices will increase back up, until normal profit can be made.

At this point, firms will be covering their opportunity cost - so they’ll no reason to leave the market anymore. Which means we’ve reached our long run equilibrium - where firms are making normal profit!

Assess how consumers AND firms would be impacted by the lower barriers to entry that exist in a perfectly competitive market [10]

AND means 2 KAA for each agent

Consumers gain significant utility from lower barriers to entry in perfectly competitive markets through increased consumer surplus. The greater number of participating firms increases market supply, resulting in downward pressure on market equilibrium price. When new firms can freely enter a market, firms must keep prices low to retain customers who now have more choices. This increased price competition leads to a lower equilibrium price and allows consumers to enjoy greater consumer surplus and allocative efficiency as we can see in the diagram where P is at the lowest point on the AC curve and Industry price falls In addition, lower entry barriers allow smaller niche firms to target specific market segments, increasing product differentiation and innovation. Consumers benefit from access to more customised offerings catered to their preferences. More firms also improve consumer access to products and services by increasing market supply and availability.

Firms are incentivised by supernormal profit to enter the market. There are no barriers to entry so they can easily enter the market. This increases supply from S to S1. This decreases price from Pe to P1, so price = lowest point along AC and all supernormal profit has been competed away. Only normal profit can be made in the long run.

Lower barriers allow entrepreneurs and small businesses to bring innovative ideas to the market, promoting business creation and economic growth. Firms are pushed to improve efficiency, quality in order to maintain market share while competing with new competition. Additionally, when consumers buy from more efficient firms it shifts resources from less efficient to more efficient uses which improves allocative efficiency in the overall economy. Market equilibrium quantity also increases as entering firms bring more supply to the market, providing growth opportunities and niche opportunities also open up for smaller firms targeting specific segments.

However, lower barriers reduce the market power of firms, making it difficult to earn long-run economic profit. Intense competition also pressures firms to keep prices low and constantly improve efficiency to remain competitive. An influx of new firms could also lead to temporary oversupply and product shortages as firms enter and exit the market which could cause uncertainty to consumers as existing firms shut down before new entrants can meet demand. Consumers may be wary of new firms that lack reputation and may doubt quality and reliability.