Chapter 3B

Exchange Rates and the Foreign Exchange Market: An Asset Approach

The Demand of Currency Deposits

What influences the demand of (willingness to buy) deposits denominated in domestic or foreign currency?

Factors that influence the return on assets determine the demand for those assets.

Rate of return: the % change in value that an asset offers during a time period.

e.g. the annual return for $100 savings deposit with an interest rate of 2% is

$100 x 1.02 = $102, therefore:

Real rate of return: inflation-adjusted rate of return; represents additional goods + services that can be purchased with earnings from the asset.

e.g. when inflation is 1.5%, the real rate of return for the above savings deposit is:

after accounting for the rise in prices of goods + services, the asset can purchase 0.5% more goods + services after 1 year.

If prices are fixed, the inflation rate is 0% and (nominal) rates of return = real rates of return.

since trading of deposits in different currencies occurs daily, we often assume prices do not change from day to day/ are fixed;

this is a good assumption for the short run.

Other Factors for Demand of Currency Deposits

Risk of holding assets influences decisions about whether to buy them.

Liquidity of an asset, or ease of using the asset to buy goods + services influences willingness to buy them.

But, we assume that risk and liquidity of currency deposits in forex markets are essentially the same, regardless of their currency denomination.

these are of secondary importance when deciding to buy or sell currency deposits.

Investors are primarily concerned about rates of return on currency deposits, which are determined by the:

interest rates the assets will earn

expectations about appreciation or depreciation

Transaction exposure: the extent to which income from individual transactions is affected by fluctuations in forex values.

Translation exposure: the impact of currency value changes on the reported consolidated results and balance sheet of a company.

Economic exposure: the extent to which a firm’s future international earning power is affected by changes in ex rates.

How private firms like BMW dealt with exchange rate risk

Despite rising sales revenue, BMW’s profits have eroded by changes in ex rates since most (83%) of its sales occur outside its base in Munich, Germany.

But BMW did not want to pass the burden of shifts in ex rates to foreign consumers and increase prices. Some implemented approaches include:

Natural hedge: develop ways to spend money in the same currency where sales take place by:

Establishing factories in markets where products are sold.

Sourcing parts overseas (e.g. Mexico, China).

Financial hedge: set up regional centers in US, Singapore, and the UK.

Instruct regional offices to review exposure and report to group treasurer.

Consolidate risk figures globally and recommend actions to mitigate risk.

Interest rates and deposits

A currency deposit’s interest rate is the amount of currency an individual or institution can earn by lending a unit of the currency for a year.

The RoR for a deposit in domestic currency is the interest rate the deposit earns.

To compare the RoR on a deposit in domestic currency with one in foreign currency, consider:

the interest rate for the foreign currency deposit

the expected rate of appreciation or depreciation for the foreign currency relative to the domestic currency.

Model of Foreign Exchange Markets

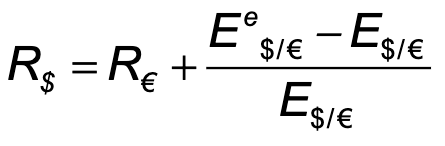

The model is in equilibrium when deposits of all currencies offer the same expected rate of return; called interest parity.

Interest parity implies that;

deposits in all currencies are equally desirable assets.

arbitrage in the forex market is not possible.

has a formula that says:

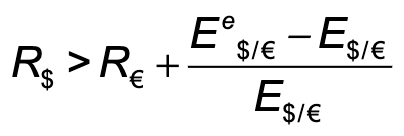

If the interest parity condition did not hold then;

This means that investors would not want to hold euro deposits, driving down demand + price of euros.

then all investors would want to hold dollar deposits, driving up demand + price of dollars.

the dollar would appreciate and the euro would depreciate, increasing the right side until equality (equilibrium) was achieved.

Changes in the current EX and expected RoR of foreign currency deposits

When the domestic currency depreciates today, the initial cost of investing in foreign currency deposits increases, thereby lowering the expected RoR of foreign currency deposits.

When the domestic currency appreciates today, the initial cost of investing in foreign currency deposits decreases, thereby lowering the expected RoR of foreign currency deposits.

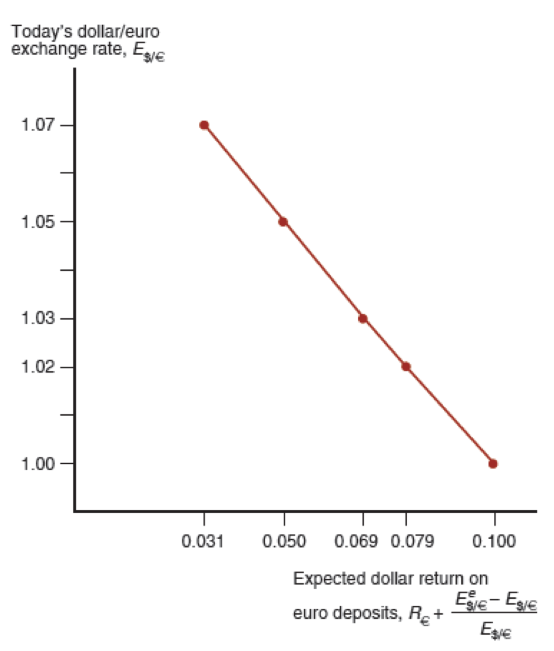

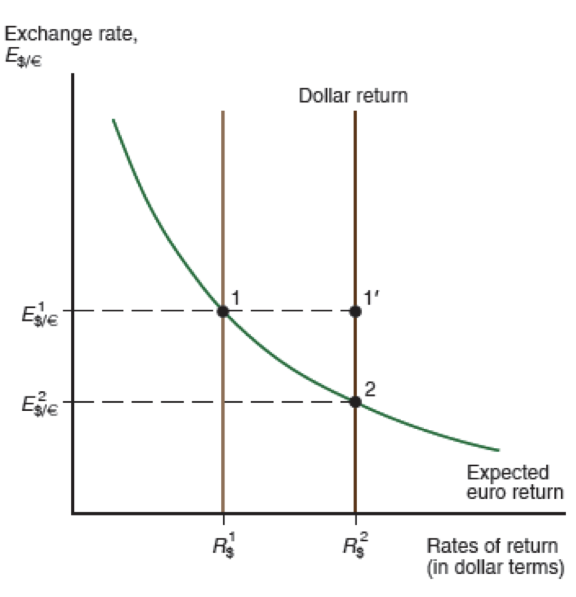

The Relation Between the Current Dollar/Euro Exchange Rate and the Expected Dollar Return on Euro Deposits

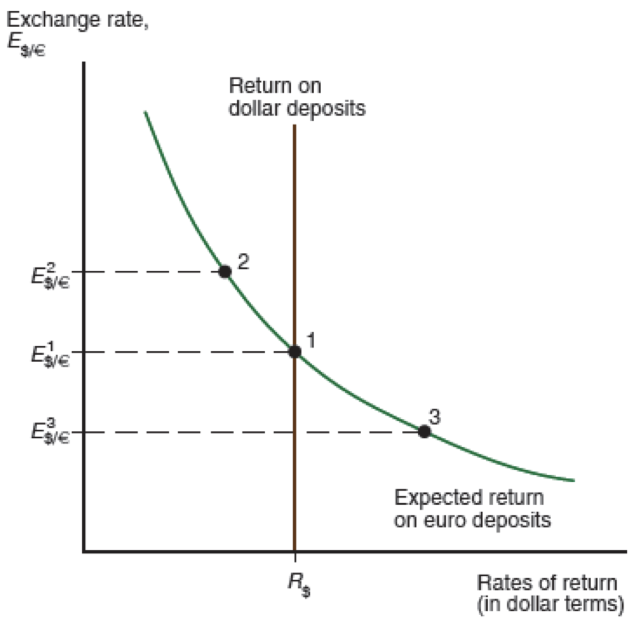

Determination of the Equilibrium Dollar/Euro Exchange Rate

Equilibrium in the foreign exchange market is at point 1, where the

Equilibrium in the foreign exchange market is at point 1, where the

expected dollar returns on dollar and euro deposits are equal.

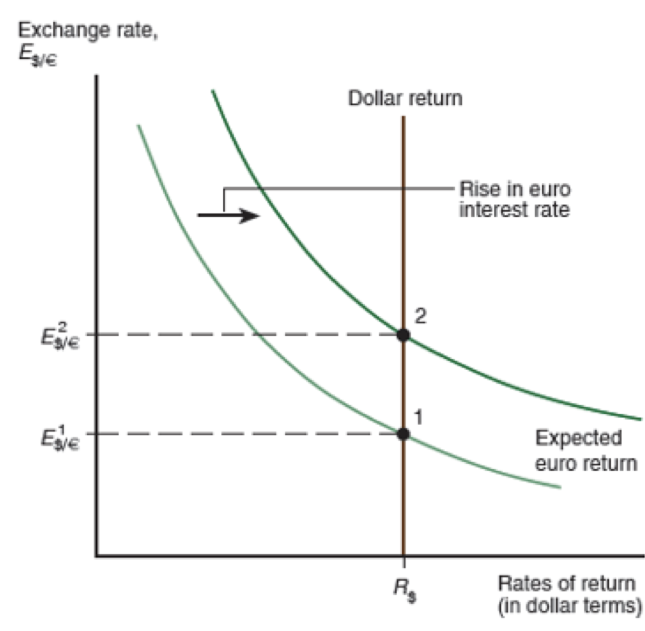

The effects of changing interest rates:

An increase in the interest rate paid on deposits denominated in a currency will increase the RoR on those deposits.

This leads to an appreciation of that currency.

Higher interest rates on dollar-denominated assets cause the dollar to appreciate.

Higher interest rates on euro-denominated assets cause the dollar to depreciate.

Effect of a Rise in the Dollar Interest Rate

Effect of a Rise in the Euro Interest Rate

The Effect of Changing Expectations on the Current Exchange Rate

If people expect the euro to appreciate in the future, then euro-denominated assets will be paid in euros, so these future euros will be able to buy many dollars and many dollar-denominated goods.

Therefore, the expected RoR on euros increases.

An expected appreciation of a currency leads to an actual appreciation (a self-fulfilling prophecy).

An expected depreciation of a currency leads to an actual depreciation (a self-fulfilling prophecy).

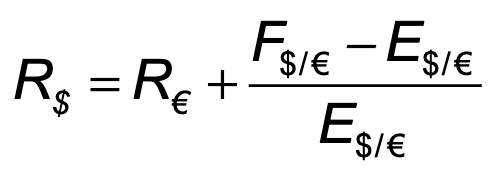

Forward Exchange Rates and Covered Interest Parity

Covered interest parity (CIP) relates interest rates across countries and the rate of change between forward exchange rates and the spot exchange rate:

It says that RoR on dollar deposits and “covered” foreign currency deposits are the same.

How could you earn a risk-free return in the foreign exchange markets if covered interest parity did not hold?

Covered positions using the forward rate involve little risk.