exam - mergers and acquisitions

NPV - wk 10 tutorial

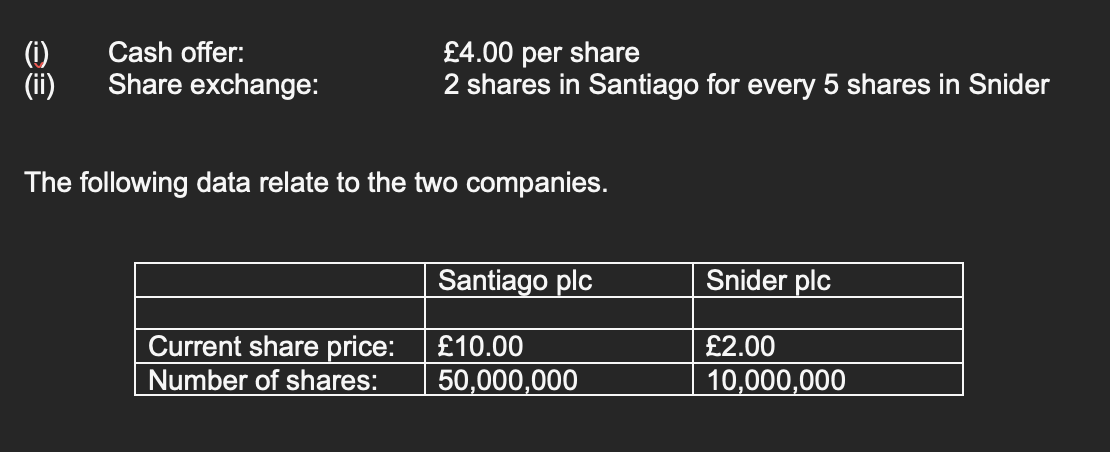

santiago plc is considering a merger with snider plc, a smaller firm in the same industry

santiago plc will be acquiring snider plc

the merger is expected to generate cost savings of 5 mil. per annum in perpetuity

these cost savings, along with the cash flows of both companies, should be discounted at a rate of 10% per annum

santiago plc is evaluating two possible bids for acquiring snider plc:

a. calculate the cost and NPV of the merger to santiago plc under both the cash and share exchange offers

st.1 → calculate market values before the merger

market value → current share price x no. of shares

santiago plc. = 10 × 50 mil. = 500 mil.

snider plc. = 2 × 10 mil. = 20 mil.

st.2 → calculate present value of gains from merger

gain = 5 mil. per yr in perpetuity, discounted at 10%

PV of gains = 5 mil. / 10% = 50 mil.

combined value post-merger = 500 + 20 + 50 = 570 mil.

part. i. cash offer

st.3 → cost of acquisition

santiago pays £4 per share for 10 mil. snider shares:

10 mil. x 4 = 40 mil. → [how much santiago is offering]

cost = extra amount santiago is offering above what snider is worth on the market

cost = 40 mil. - 20 mil. = 20 mil.

snider market value = 20 mil.

st.4 → NPV of the merger

NPV = gains - cost

NPV = 50 mil. - 20 mil. = 30 mil.

part. ii. share exchange offer

st.5 → determine no. of new santiago shares issued

for every 5 snider shares, 2 santiago shares are offered:

2/5 × 10 mil. = 4 mil. new shares issued

there are 10 mil. snider shares

st.6 → new total santiago shares after merger

new total santiago shares after merger = no. of santiago shares + new shares

= 50 mil. + 4 mil. = 54 mil.

new share price of santiago post merger = 570 mil. / 54 mil. = £10.56

570 mil = total combined value [st.2]

st.7 → cost of the merger via shares

no. of shares x new share price = 4 mil. x 10.56 = 42.22 mil.

cost = 42.22 mil. - 20 mil. = 22.22 mil.

20 mil. → snider market value

NPV = 50 mil - 22 mil. = 27.78 mil.

valuations [pricing] - wk11 tutorial

you are given that brandt ltd has:

500,000 shares in total

net assets = 10 mil.

dividend = £2 per share

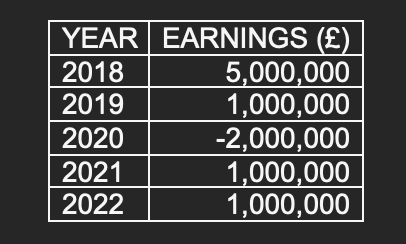

earnings of past 5 yrs:

similar firms:

earnings yield = 15%

dividend yield = 10%

5 years’ purchase of super profits

normal rate of return on net assets = 15%

a. calculate the value of one ordinary share in brandt ltd using each of the following methods:

maintainable earnings method

st.1 → calculate average earnings

5 + 1 + [-2] + 1 + 1 = 6 mil.

6 mil. / 5 = 1.2 mil.

st.2 → capitalise average earnings using earnings yield of 15%

1.2 mil. / 15% = 8 mil.

st.3 → value per share

8 mil. / 500,000 = £16

500,000 = no. of shares

dividend yield method

dividend per share = £2

dividend yield = 10%

£2 / 10% = £20

asset value method

given info:

net assets = 10 mil.

shares = 500,000

value per share = 10 mil. / 500,000 = £20

super profits method

st.1 → calculate super profits earning:

super profits = maintainable earnings - normal earnings

super profits = 1.2 mil. - 1.5 = -300,000

normal earnings = 15% x net assets

normal earnings = 15% x 10 mil. = 1.5 mil.

maintainable earnings = 1.2 mil.

st.2 → capitalise super profits using 5 yrs purchase:

-300,000 × 5 = -1.5 mil.

st.3 → add net assets:

[-1.5] + 10 = 8.5 mil.

st.4 → value per share:

8.5 mil / 500,000 = £17

berliner method

the berliner method takes the average of 2 valuations:

maintainable earnings method value = £16

asset value method value = £20

[16 + 20] / 2 = £18