Basic Economic Ideas and Resource Allocation

SCARCITY, CHOICE AND OPPORTUNITY COST

Economic Problem/Scarcity: When there are limited resources and unlimited wants. The unlimited wants exceed limited resources. People need to make a choice and every choice made has an opportunity cost - the next best alternative given up/forgone.

Choice: Resources are scarce so individuals firms and governments have to consider different alternatives

How do countries/economies/firms allocate resources?

- What to produce? As there unlimited wants and limited resources we need to decide which product to produce to increase efficiency

- How to produce? Using resources/FoP, some firms are capital intensive and some are labour intensive

- For whom to produce? Depends on wether it’s public or private sector. If owned by individuals they will provide products to those able and willing to buy a product. If it’s the public sector they will provide the product to everyone which will increase equality

ECONOMIC METHODOLOGY

Ceteris Paribus: All other factors remain unchanged

Decisions at the margin: A small change in one economic variable will lead to further small changes in other variables

Short-Run:

- Time period when a firm can change at least one factor of production - ‘the variable one’

- Key word: Labour changes

- The firm can increase its output by changing variable factor (labour). However, in a short period of time firms don’t have enough time to change capital and land

Long-Run:

- Time period in which all factors of production are variable with a constant

- Key word: Changing capital or land

Very Long-Run:

- Time period in which all key inputs into production are variable

- Key word: Advanced tech + more research

Economics as a Social Science:

- It studies societies and the human interactions within those societies

- Human interactions are complex and are influenced by many variables

Positive Statement:

- Statements that are based on facts and actual evidence

- Economists don’t give opinion so it is objective

- Can be tested for validity

Normative Statement:

- Statement based on economist’s opinion/ make valuable judgement

- Subjective

- Can be proved/tested for validity

- Keywords:

- Should be

- The best

- The most

- Too much

- Too little

- Ought to be

- Unfair/fair

- Can’t be tested for validity

- opinion/judgement

- Needs to

FACTORS OF PRODUCTION

Factors of Production:

- Resources that are limited in supply and used to produce goods and services to satisfy people’s needs and wants

- Land: Natural resources needed to produce goods and services

- Labour: Human resources that are needed mentally/physically to produce goods and services

- Capital: Man-made resources that are used to produce goods and services e.g. roads, machinery

- Enterprise: Owner of the firm

Geographical Mobility: The ability to move from one location to another

Occupational Mobility: The ability to do more than one task or job

Land:

- Natural resources that are used to produce goods and services

- Reward, income, payment: Rent

- E.g. oil, river, soil, wood

- Geographical Immobile & Occupational Mobile

How to Increase the Quality of Land:

- Better natural fertilisers

- Better irrigation system

- Tractor

- Advanced Technology

- Discovery of new resources e.g. oil field

- Reclaimation of land

Labour:

- Human resources

- Income: salaries/wages

- Geographical and Occupational Mobile (conditional)

- Economically active: Have ability and willingness to work

- Employed: Able and willing + in an active job

- Unemployment: Able and willing to work but they aren’t working and actively looking for job

- Economically inactive:

- Don’t have ability and willingness to work

- Retired ppl over 60/65

- Under-school leaving age (under 16)

- Disabled, too sick

- Without willingness to work

How to increase quality of labour:

- Increase education, training, healthcare to increase productivity

- Increase immigration

- Decrease school leaving age

- Increase retirement age

- Decrease discrimination increase women participation

Capital:

- Man made resources that are used to produce other goods and services

- Capital refers to the factor of production that includes all the human-made aids to production,.

- Capital is a factor of production that can be used in the production process.

- It can be combined with the other factors of production to produce goods and services which can be sold in the market.

- Rewards/ payments: interest

- e.g. tools, equipment, plant, machinery and factories

How to Increase the Quality of Capital:

- Increase investment to increase capital goods

- More advanced technology

- Human capital: The skills and experience acquired by an individual through education, training and/or experience, which add up to his/her value to the process of production

- Physical capital:The inputs such as factories, buildings, plant and machinery, raw materials, etc., are required for further production

- Geographical & Occupational Mobile

Enterprise:

- Risk taking ability of the owner of the business who is responsible of managing all other FoP

- Income: Profit

- Geographical and Occupational Mobile

To increase the quality of enterprise:

- Provide more education and training

To increase the quantity of enterprise:

- Lower taxes to increase profit and decrease cost of production

- Reduce regulations

- More education and training

- Immigration so more people will come and start up their own business

- Provide more subsidies to reduce their cost of production

- Deregulation to make it easier to start a business

- Increase privatisation which will increase competition so more businesses will open in the country

Goods:

- Tangible products used to satisfy needs and wants

- Products w/ physical existence

Services:

- Intangible product

- Do not physically exist

- E.g. medical service, transportation, teaching

Benefits of Factor Mobility

- Increase chance of success

- Increase chances of earning fro workers

- Increase sales, increase profit for business

- Latest tech is available

- Consumers get a variety of products

- Firms able to get best quality + cheaper raw materials

Note:

- Firms usually move to areas for better resources or to discover more natural resources

- Able to produce more goods and services

- Able to produce wider range of goods/services

- Improve quality of product

The Private Sector:

- Aims to maximise profit

- Produces fewer necessities and more luxuries

The Public Sector:

- Aims for collective welfare of society

- Fewer luxury goods and more merit goods and public goods are provided

- Socially optimum merit goods

- Socially optimum demerit goods

- Socially optimum public goods

Division of Labour:

- When a task is broken up into several component tasks

Specialisation

- The process by which individuals, firms, economies concentrate on producing those goods and services where they have an advantage over others

- Increased output of country so increase GDP and increase economic growth

- Increase productivity and efficiency

- Increase quality

- Decrease cost which will decrease price of product

- Increase international competitiveness of the country so increase exports which will increase export revenues + increase variety of goods and services

- Boring or monotonous

- If one worker is unable to do his job the whole productivity process is slowed down

- Could lead to the country becoming too dependent on other countries so there is a risk of lower supply of imported goods if there are disputes between countries

- Workers will become occupational immobile so if there’s less demand for products produced by country unemployment will increase and economic growth will decrease

- Products become too standardised as firm is doing mass production

Role of the Entrepreneur:

- Taking risk as they invest their money in a new business idea that might be successful and lead to earning profits or fail to lose their money. They could also be in debt if they borrowed funds from the bank

- Managing other FoP through deciding the quantity and how they will be used

RESOURCE ALLOCATION IN DIFFERENT ECONOMIES

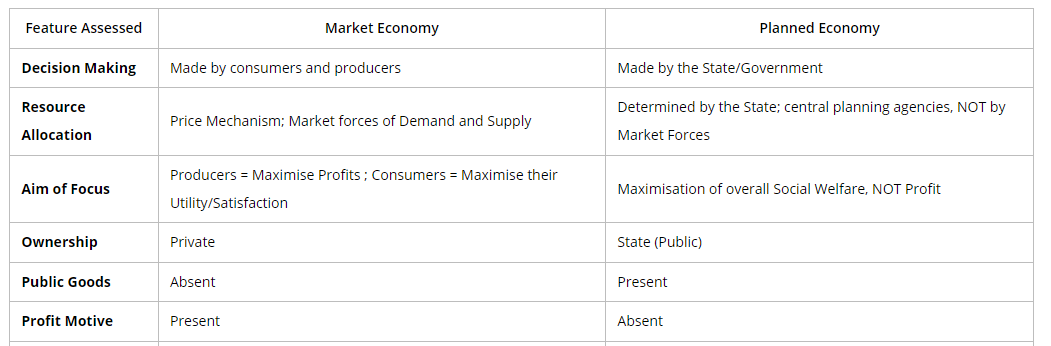

Economic system:

- Is the way in which production ls organized and choices are made in an economy

- It is the way households, government, and firms make decisions related to these the three-resource allocation questions

- There are three main economic systems in a country: market economy, planned economy and mixed economy

What is price/ market mechanism/ price determination?

- when resources allocation decision is taken by individuals "consumers and producers" and there is no government intervention

- Prices are determined by the market forces of supply and demand.

- If the demand for a product increases, the price will increase. As firms have a profit incentive, they will reallocate resources to the product that has high demand so firms will increase supply which will reduce the price of the product.

Market economy:

- An economic system where most decision are taken through the market mechanism.

- It has only the private sector in which resources are owned by individuals

- Resources are allocated by the forces of supply and demand

- The government has no direct control in the economy.

- The government role is to watch what is happening and only intervene when the price mechanism doesn't provide the best allocation of resources

- No certain economy operates under the market economy as it causes market failure.

Advantages of a market economy:

- There is consumer sovereignty as consumers determine what is produced. This will increase flexibility which will encourage firms to respond to changes in consumers' demand.

- Resources will be allocated through price mechanism. Price will act as a signal to transmit consumers' preferences

- There is competition between firms and the profit incentive,increases efficiency leading to lower costs so lower prices and high-quality products produced.

- There are wider choices as a variety of products are produced.

Disadvantages of a market economy:

- Poor consumers will have little influence on what is produced because they have low income so low purchasing power

- Income and wealth might be unequally distributed which will increase the gap between the rich and poor and might increase poverty.

- Monopoly may occur which will abuse its market power. Therefore, monopolies will exploit consumers through charging higher price and reduce the quality.

- Market failure may occur with market forces failing to ensure the maximum benefit to the society as consumers and producers take into account their own private benefit and cost.

- Demerit goods that cause external cost such as cigarettes will be over- produced and over-consumed as people underestimate the private cost and ignore the external cost associated with its consumption due to information failure.

- Merit goods such as education will be under-consumed and under-produced as people will underestimate its private and external benefit if it is charged for a price due to information failure

- Public goods such as national defense will not be provided as private firms don’t have financial incentive to produce since they can’t charge a price for it

Planned Economy:

- A market system where resources are state-owned and allocated body "government"

- The central government and its organization are responsible for the allocation of resources.

- Price control to set the price of most essential items and to determine the wages

- Productive resources,"resources that are available for use" are state-owned.

- They subsidize essential products to keep its price low.

- For example: Cuba and North Korea

- The objective of a planned economy is to achieve a high rate of growth to catch up with advancement in other market economies so they will increase the demand for capital goods.

Advantages:

- Government may decide to directly provide certain goods and services.

- The government will provide necessities for lower price through price control so it will be affordable by everyone in the economy.

- National Income might be distributed more equally in accordance of the needs of the people. This will increase equality and social welfare.

- The social cost and benefit of an activity will be taken into account by the government which will reduce the external cost for example damage to the environment and pollution

- The government will provide public goods and merit goods which wouldn’t be consumed or under-consumed if there was no government intervention

Disadvantages:

- Due to lack of profit incentive, there will be lack of competition. This will reduce efficiency which will increase the cost of production and increase the price of goods and service, This will also lead to lower quality and lower variety of goods and service which will reduce standard of living

- There is a lack of consumer sovereignty which will lead to less flexibility so the public sector won't respond to changes in consumers demand.

- The use of price control might lead to surplus or shortage of goods and services

- It may lack incentive to invest in the economy which will reduce innovation and reduce the variety of goods and services.

Mixed Economy:

- An economic system in which both market forces and the government are involved in resource allocation decisions.

- Both private sector and public sector have a role in resource allocation.

- There is both private and state ownership of productive resources.

- The resources are allocated using both price control or price mechanism.

- Read page 27 in textbook for examples of economic systems in countries.

Advantages:

- The price mechanism is allowed to operate in many areas, facilitating its functions of rationing, signalling and the transmission of preferences. Therefore the private sector will be able to respond to changes in customers' demand

- A government is able to intervene in a market, e.g., through a maximum price or a minimum price. Maximum price will lead to decrease the price of basic necessities so it will be affordable by the poor and reduce poverty. Minimum prices can be used to increase the pay of the lower-paid workers so increasing standards of living.

- Some industries may be nationalised by the government so customers will not be exploited by the higher price that could be charged by the private sector. This Will increase the social welfare of the economy

- The public sector will follow health and safety standards which will lead to provide more safer goods to be consumed

- The government will provide public goods as it won't be provided by the private sector since they can’t charge a price for it and there is no profit incentive

Disadvantages:

- The workings of price mechanism may be adversely affected by a government, e.g., taxes and subsidies.

- Increasing taxes could reduce the incentive of the private sector to expand and increase output which will lead to lower economic growth. Furthermore could discourage foreign investment from locating in the country

- Natural monopolies might reduce efficiency as they don't have profit motive. This will increase the cost of production and reduce the quality of the products. It will also reduce the variety of goods and services available in the economy

- There is a possibility of market failure.

Transitional Economy:

- Economy that is in the process of changing from a Planned Economy to a more Mixed Economy

- Market Forces assume greater importance and responsibility in resource allocation

- Good Examples: Former Eastern Europe, People’s Republic of China, etc.

Issues of Transition

- Inflation -> Prices become volatile, hence rate of inflation could be higher than in Planned Economy

- Industrial Unrest -> Trade Unions may exploit their stronger authority in order to get higher wages; could result in strikes, protests, etc.

- International Trade Side Effects -> May lead to BOP imbalances of export/imports, could result in current account deficits

- Unemployment -> May arise from workers struggling to adapt to structural employment changes; since planned economies usually have a higher rate of employment than transition economies

- Fall in Output -> Some industries perish when market forces are introduced, leads to a fall in output

- Reduction in Welfare Services -> Standard of living may deteriorate for some when market forces acquire responsibility of welfare provision

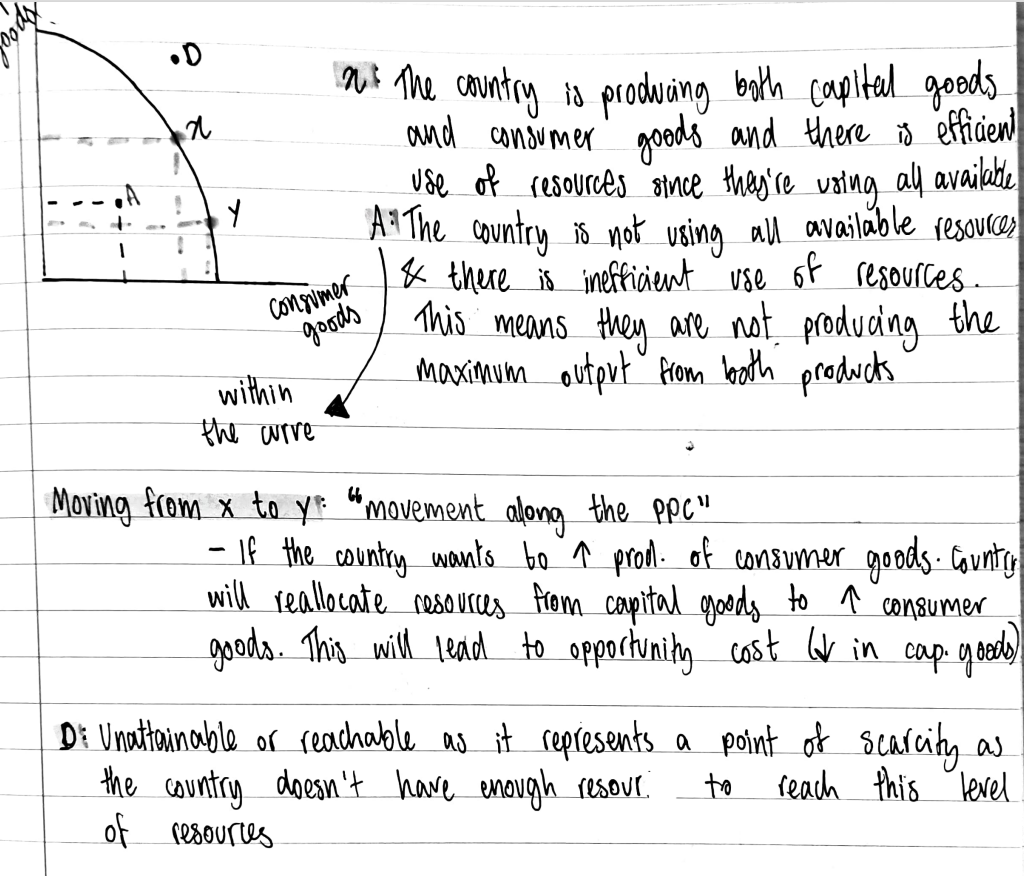

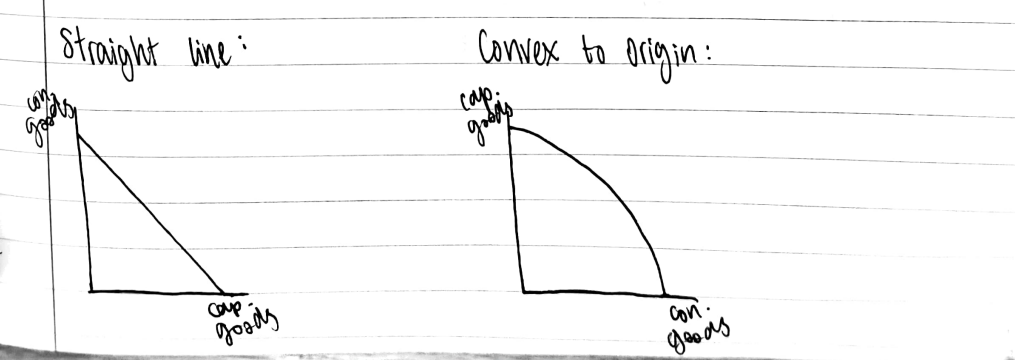

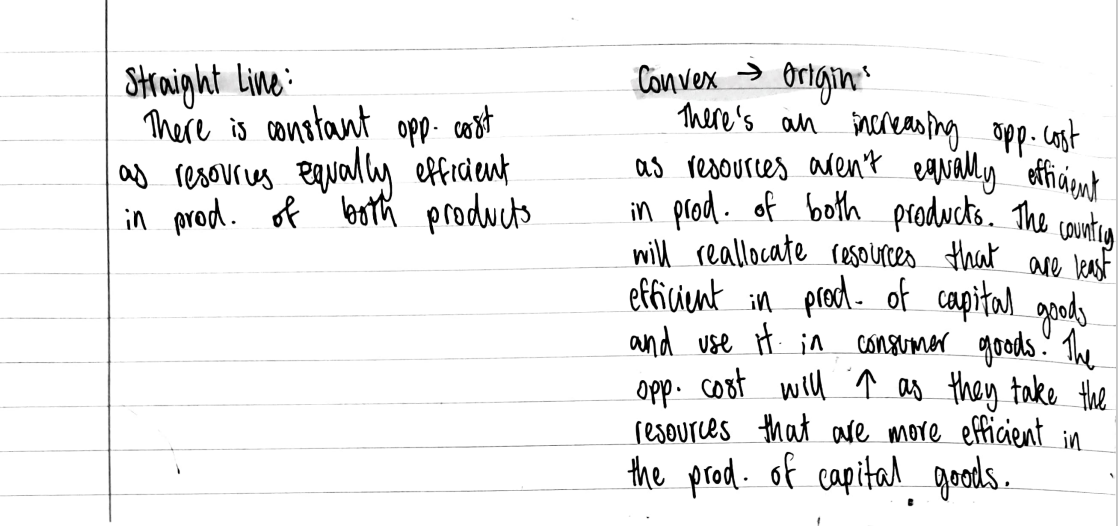

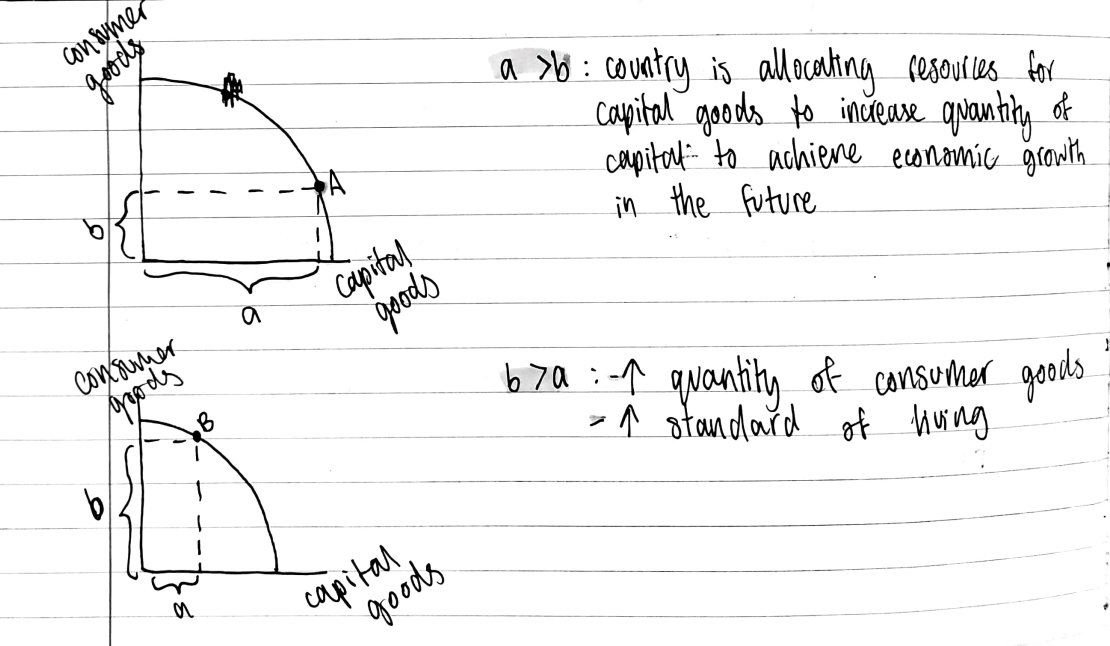

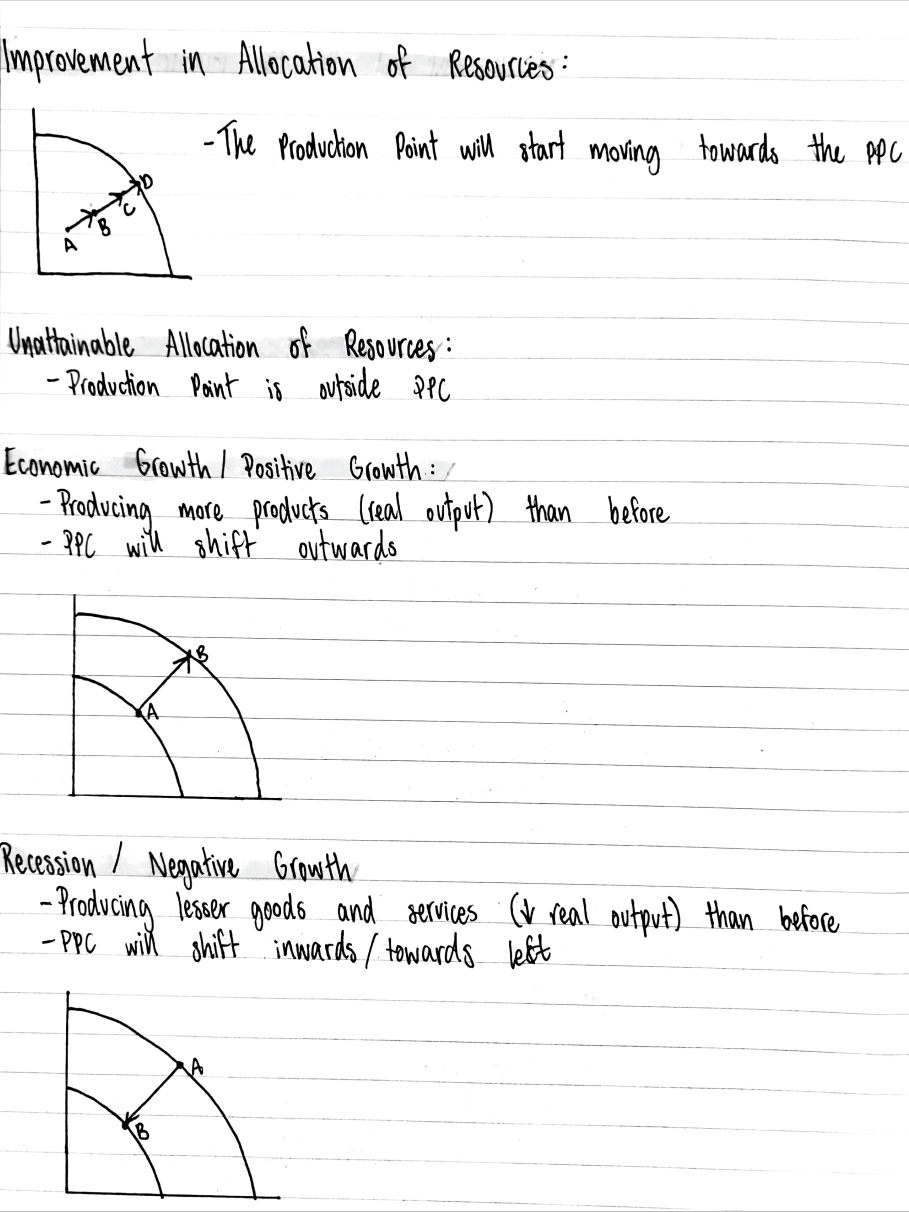

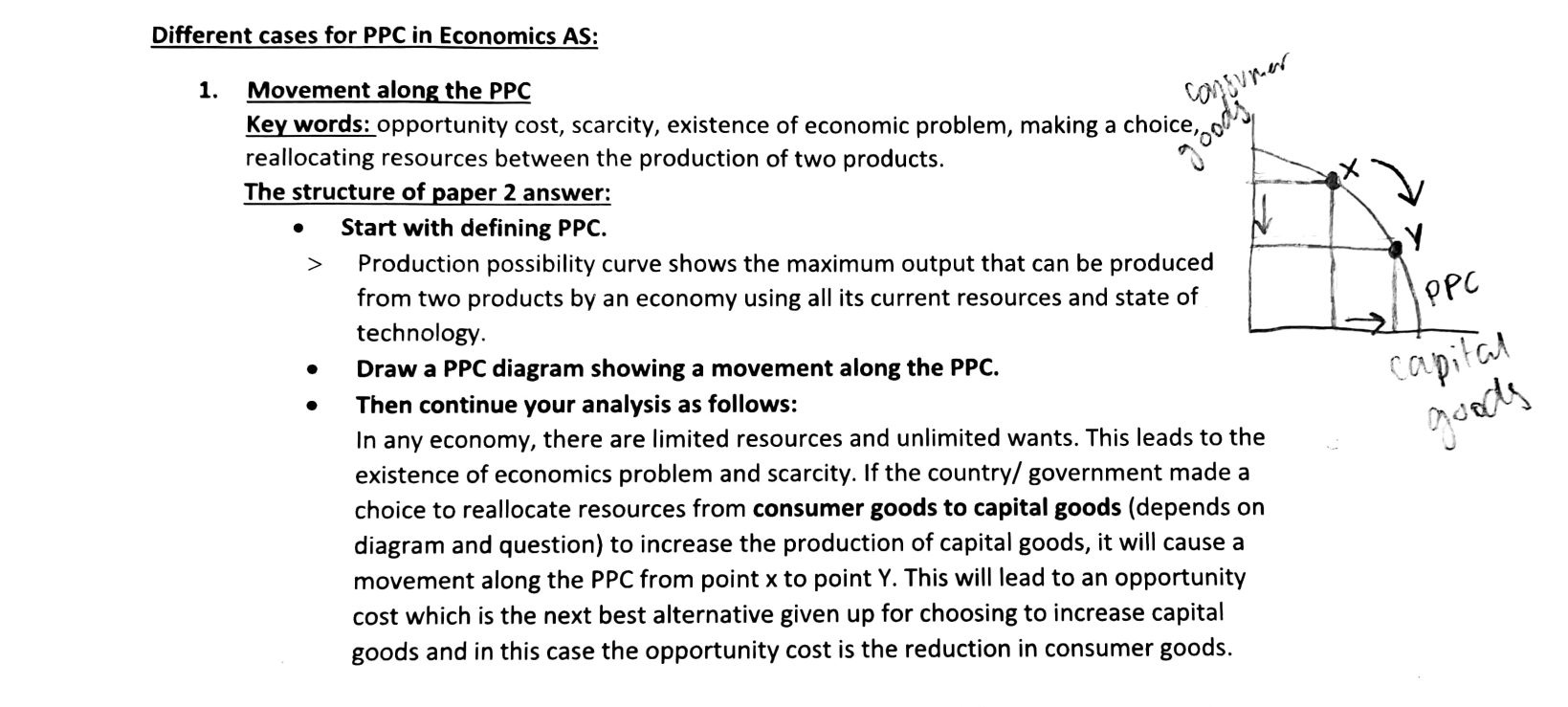

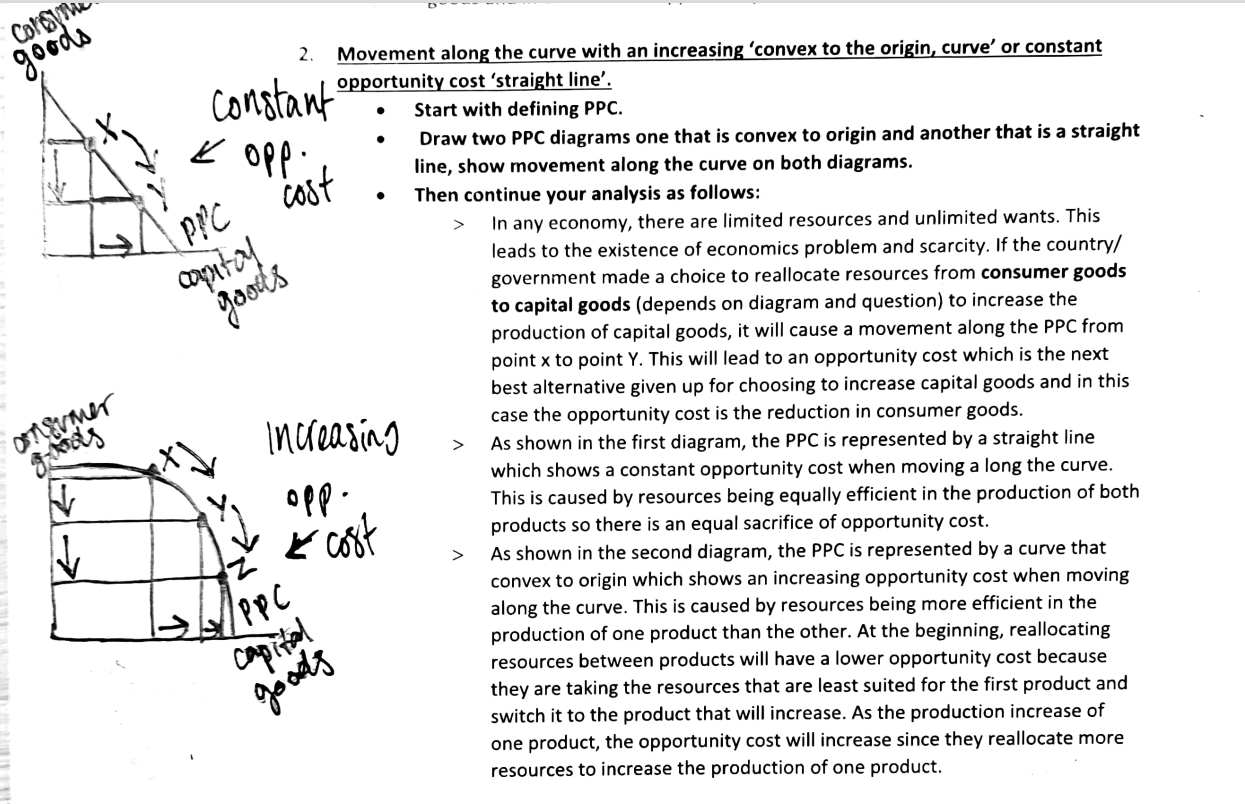

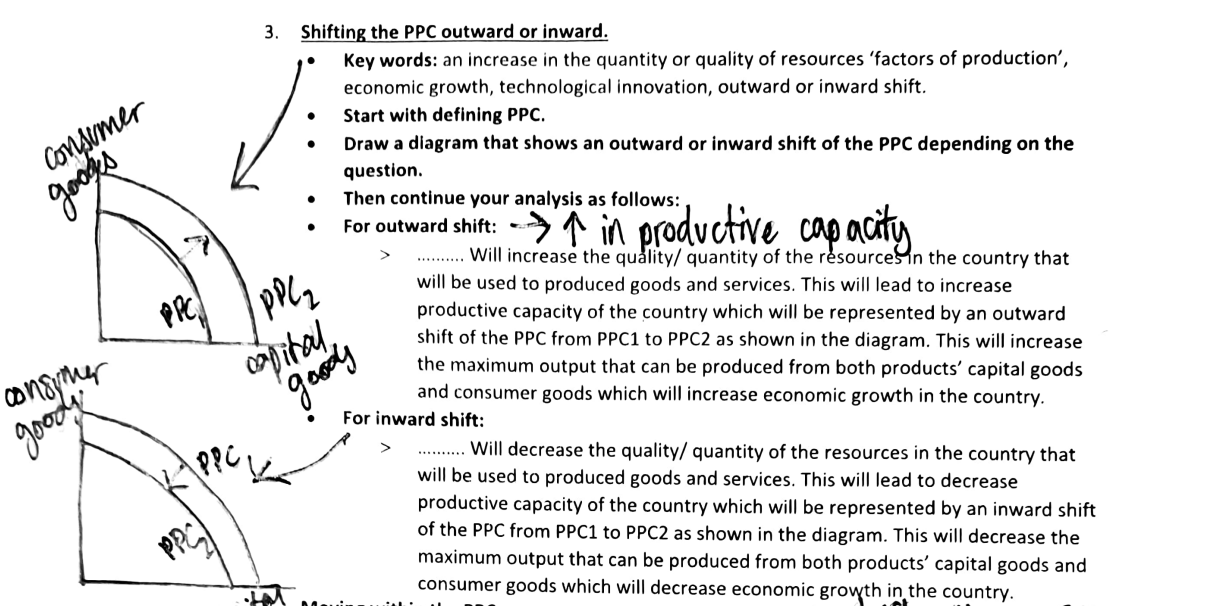

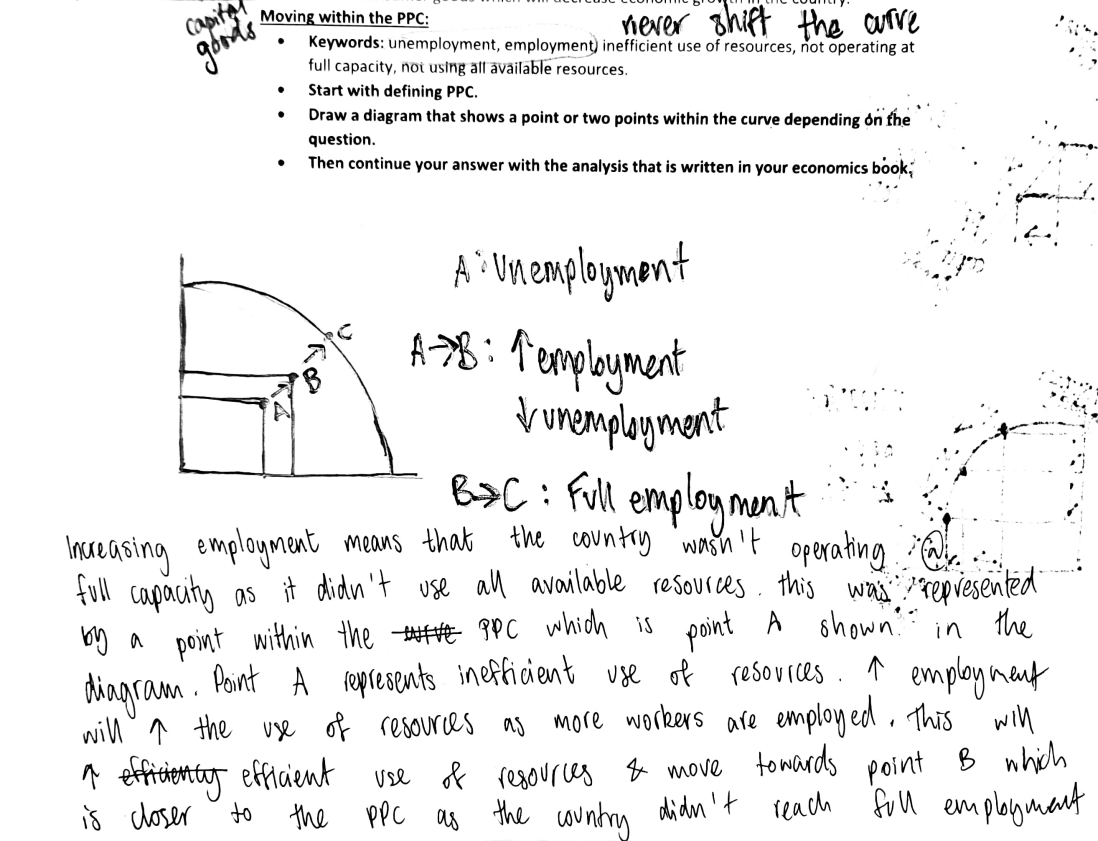

PRODUCTION POSSIBILITY CURVES

- A curve that shows the maximum output that can be produced from 2 products using all current resources and state of technology available

![]()

Reasons for a shift in PPC

- Economic Growth

- Discovery of more natural resources

- Increase supply of labour

- Increase size of working pop.

- Increase immigration of workers

- Increase capital equipment, increase automation

- new/latest technologies

- Increase education, training, skills of entrepreneurs + workers

- Improvement in healthcare: healthy + productive workforce

- Investment in modern businesses

- Recession:

- Non renewable resources (once resources are used they are depleted)

- Decrease supply of labour

- Decrease supply of entrepreneur

- Increase emigration (brain drain)

- Old, traditional methods of prod.

- Old training and education techniques

- Old and worn out infrastructure

PPQ MODEL ANSWERS

CLASSIFICATION OF GOODS AND SERVICES

Free Goods:

- Unlimited in supply

- Zero opportunity cost

- No prices and no FoP required to produce them

- E.g. air, water in local river

Private Goods:

- Excludable: It is possible to stop someone from consuming a good or service through charging a price

- Rival: Consumption by one person of a good or service reduces the availability of it for others

Public Goods:

- Non-excludable: It is not possible to stop anyone from using a good

- Non-rival: Consumption by one person of a good or service doesn’t reduce the availability of it for others

- Non-rejectable: consumer doesn’t have a choice of wether to consume the commodity or not

- Providing by public sector/government as they are thought to be necessary for daily life and national development

- E.g. lighthouse, national defense, street lights

- Free riders:

- People who use or overuse a good or service without paying their share for it through taxes to the government

- Occurs due to non-excludability

- Public goods won’t be provided in a free market b/c private sector won’t provide it since there’s no profit incentive since you can’t charge a price for it

- Quasi-public goods: goods that have some but not all of the characteristics od public goods e.g. sandy beach b/c they can be excludable (privately owned beaches) or rival b/c as the beach becomes crowded space is limited, others’ music and convos become louder and enjoyment reduces

Merit Goods:

- Goods which are considered to be highly desirable for the welfare of the citizens

- E.g. healthcare and education

- Underproduced and underconsumed in a market economy

- Have positive externalities or external benefit (beneficial effect to 3rd parties who are indirectly involved w/ production/consumption)

- This means that social benefits (private + external) > private benefits

- Private benefits: for producers = profit, revenue and for consumers = satisfaction,utility

- Information failure as consumers are unaware of the private benefit and ignore the external benefit of consumption

- E.g. education:

- Private benefit = consumers develop skills that can get them a high paying job

- External benefit = more skilled workers which increases efficiency which increases economic growth

Demerit goods:

- Goods which are considered to be undesirable for the welfare of the citizens

- E.g. cigarettes and alcohol

- Overproduced and overconsumed in a market economy due to addictive nature

- Have negative externalities or external cost (negative effect to 3rd parties who are indirectly involved w/ production/consumption)

- This means that social cost (private cost + external cost) exceeds private cost

- Information failure as consumers underestimate private cost and ignore external cost

- E.g. cigarettes can cause harm to smokers and to others around them (second hand smoke)

- Private cost: for producers = cost of production and for consumers = price/harm

*The under-consumption of merit goods and the over-consumption of demerit goods can lead to market failure

*Merit and demerit goods are private goods but the govt. Can provide merit goods in a mixed/planned economy AND they can impose regulations/taxes on demerit goods in a mixed economy