ch. 10 - stockholders' equity

accounting equation and components of stockholders’ equity

assets (resources) = liabilities (creditors’ claims) + stockholders’ equity (owners’ claims)

paid-in capital - the amount stockholders have invested in the company

retained earnings - the amount of earnings the company has kept or retained (earnings not distributed in dividends to stockholders over the life of the company)

treasury stock - a company’s own issued stock that it has repurchased

invested capital

paid-in capital - the amount of money paid into a company by its owners

corporation - an entity that is legally separate from its owners and even pays its own income taxes

most corporations are owned by stockholders, some owned entirely by one individuals

sole proprietorships are most common, but corporations are larger in sales, assets, earnings, employees

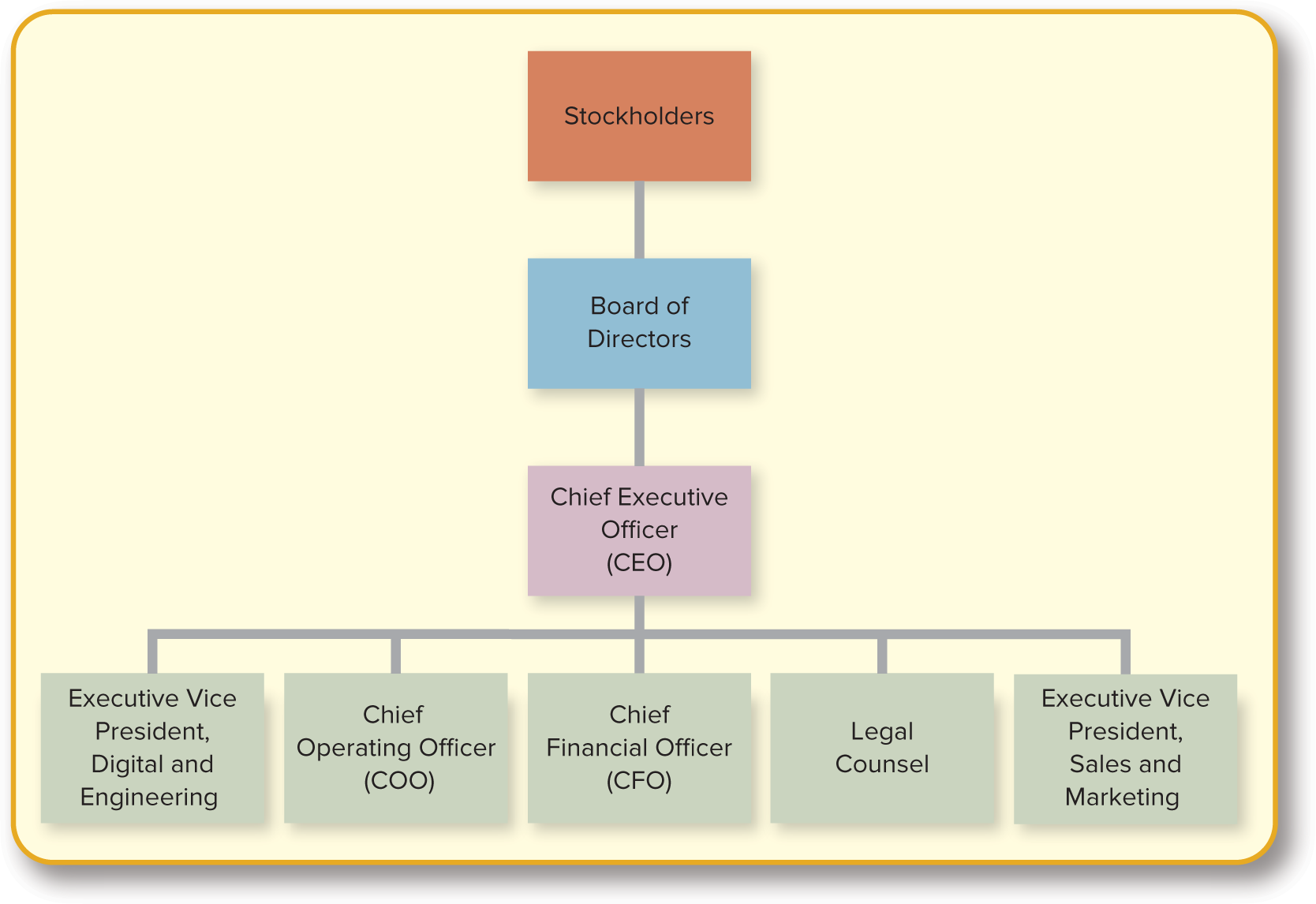

corporations

obj. 10.1 - identify the advantages and disadvantages of the corporate form of ownership

corporations are formed in accordance with the laws of individual states

state incorporation laws guide corporations as they write their articles of incorporation

articles of incorporation - describes the nature of the firm’s business activities, the shares to be issued, and the composition of the initial board of directors

the board of directors establishes corporate policies and appoints officers who manage the corporation

a corporation’s stockholders control the company

stockholders determine the makeup of the board of directors who appoint the management to run the company

stages of equity financing

most corporations that end up selling stock on a major stock exchange don’t begin that way—there’s a progression of equity financing stages leading to a public offering

most corporations start off by selling stock to the founders of the business and to their friends/family

as equity financing needs grow, companies prep a business plan and seek investment from “angel investors” and venture capital firms

angel investors - wealthy individuals in the business community willing to risk investment funds on a promising business venture

venture capital firms - provide additional financing, often in the millions, for a percentage ownership in the company

many look to invest in promising companies where they can add value through business contacts, financial expertise, or marketing channels

most corporations don’t consider issuing stock to the general public until their equity financing needs exceed $20M.

initial public offering (IPO) - the first time a corporation issues stock to the public

major event requiring the assistance of an investment banking firm (underwriter), lawyers, and public accountants

major investment bankers charge up to 6% of the issue proceeds for their services

public or private

corporations can be public or private

publicly held corporation - allows investment by the general public and is regulated by the securities and exchange commission

the stock of a publicly held corporation trades on the NYSE, NASDAQ, or OTC

NYSE - new york stock exchange

most large companies (walmart, exxonmobil, general electric) are traded on NYSE

NASDAQ - national association of securities dealers automated quotations

NASDAQ is home to many large high-tech companies (apple, microsoft, intel)

OTC - over the counter

takes place outside one of the major stock exchanges

all publicly held corporations are regulated by the SEC, resulting in significant additional reporting and filing requirements

privately held corporation - does not allow investment by the general public and normally has fewer stockholders

corporations whose stock is privately held do not need to file financial statements with the SEC

companies begin as small, privately held corporations, then as success broadens for expansion, the corporation goes public

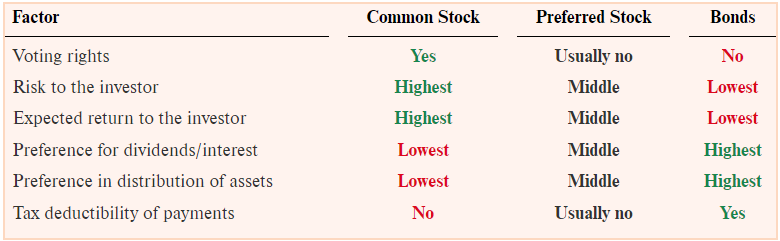

stockholder rights

stockholders are the owners of the corporations and have certain rights

right to vote - stockholders vote on matters, including the election of corporate directors

right to receive dividends - stockholders share in profits when the company declares dividends. the percentage of shares a stockholder owns determines his or her share of the dividends distributed

right to share in the distribution of assets - stockholders share in the distribution of assets if the company is dissolved. the percentage of shares a stockholder owns determines their share of the assets, which are distributed after creditors and preferred stockholders are paid

advantages of a corporation

limited liability - stockholders in a corporation can lose no more than the amount they invested in the company

in contrast, owners in a sole proprietorship/partnership can be held personally liable for debts the company has incurred, above and beyond the investment they have made

ability to raise capital and transfer ownership - since corporations sell ownership interest in the form of shares of stock, ownership rights are easily transferred

investors can sell their ownership interest anytime without affecting the structure of the corporation of its operations, so attracting outside investment is easier for a corporation than for a sole proprietorship or a partnership

disadvantages of a corporation

additional taxes - corporate income is taxed once on earnings at the corporate level and again on the dividends at the individual level

double taxation - corporate income is taxed once earnings at the corporate level and again on dividends at the individual level

owners of sole proprietorships and partnerships are taxed once, when they include their share of earnings in their personal income tax returns

more paperwork - federal and state governments impose extensive reporting requirements on the company to protect the rights of those who buy a corp’s stock/who lend money to a corp

additional paperwork ensures adequate disclosure of the information investors and creditors need

limited liability and beneficial tax treatment

S corporation - allows a company to enjoy limited as a corporation, but tax treatment as a partnership (best of both worlds)

major restriction - corporation cannot have more than 100 stockholders, so S corps appeal more to smaller, less widely held businesses

two additional business forms evolved in response to liability issues and tax treatment—LLCs and LLPs

most accounting firms in the US adopt these b/c they offer limited liability and avoid double taxation, but with no limits on the # of owners as in an S corporation

the primary advantes of the corporate form of business are lmited liabilty and the ability to raise capital. the primary disadvantrages are additonal taxes and more paperwork

common stock

obj. 10.2 - record the issuance of common stock

authorized, issued, outstanding, and treasury stock

authorized stock - the total number of shares available to sell, stated in the company’s articles of incorporation

shares available to sell ( = issued + unissued )

issued stock - the number of shares that have been sold to investors. a company usually does not issue all of its authorized stock

shares actually sold ( = outstanding + treasury )

issued shares

outstanding stock - the number of issued shares held by investors. only these shares receive dividends

shared issued and held by investors

treasury stock - the number of issued shares repurchased by the company

shares issued and repurchased by the company

par value

par value - the legal capital per share of stock that’s assigned when the corporation is first established

originally indicated the real value of a company’s shares of stock

today, par value has no relationship to the market value of the common stock

no-par value stock - common stock that has not been assigned a par value

laws in states permit corporations to issue no-par stock

in some cases, a corporation assigns a stated value to the shares

stated value - the legal capital assigned per share to no-par stock

treated and recorded in the same manner as par value shares

accounting for common stock issues

when a company issues no-par value stock, the corporation records the equity account entitled common stock

example

example

assume Canadian falcon issues 1000 shares of no-par value common stock at $30 per share:

debit | credit | |

cash ( = 1000 shares x $30 ) | 30,000 | |

| 30,000 |

income statement

R - E = NI (no effect)

balance sheet

A (30,000 cash) = L + SE (30,000 common stock)

if the company issues par value stock rather than no-par value stock, we credit two equity accounts

credit common stock account for the number of shares issued times the par value per share and we credit additional paid-in capital for the portion of cash proceeds above par value

preferred stock

obj. 10.3 - understand unique features and recording of preferred stock

some corporations issue preferred stock in addition to common stock to attract wider investment

preferred stock - stock with preference over common stock in the payment of dividends and the distribution of assets

preferred stockholders have first rights to a specified amount of dividends. if the board of directors declared dividends, preferred shareholders will receive the designated dividend before common stockholders receive any

preferred stockholders receive preference over common stockholders in the distribution of assets in the event the corporation is dissolved

about 20% of the largest US companies have preferred stock outstanding, but unlike common stock, most preferred stock does not have voting rights—control of the company remains with common stockholders

accounting for preferred stock issues

we record issuance of preferred stock similar to how common stock is issued

debit | credit | |

cash ( = 1,000 shares x $40 ) | 40,000 | |

| 30,000 | |

additional paid-in capital (difference)

| 10,000 |

income statement

R - E = NI (no effect)

balance sheet

A (+40,000) = L + SE (+30,000 pref. stk, +10,000 addl. PIC)

features of preferred stock

convertible - a bond feature that allows the lender (or investor) to convert each bond into a specified number of shares of common stock

shares can be converted into common stock

redeemable - shares can be returned to (or redeemed by) the corporation at a fixed price

redemption privilege might allow preferred stockholders the option, under specified conditions, to return their shares for a predetermined redemption price—shares may be redeemable at the option of the issuing corporation

cumulative - preferred stock shares receive priority for future dividends, if dividends are not declared in a given year

shares receive priority for future dividends, if dividends are not declared in a given year

dividends in arrears - unpaid dividends on cumulative preferred stock

if specified dividends are not declared in a given year, they become dividends in arrears, and accumulate until the company ny does declare dividends

debt or equity

these features of preferred stock give it attributes somewhere between common stock (equity) and long-term debt (liabilities). investors in commons

investors in common stock are owners of the corp b/c they have voting rights, and some preferred stock may be convertible to common stock.

investors in long-term debt, such as bonds, are creditors who have loaned money to the corp.

these investors have the right to interest payments each year and then the face amount of the bond at maturity. this financing ar arrangement is similar to preferred stock that pays cumulative dividends and is redeemable by stockholders

dividends for preferred stock

preferred stock is usually cumulative, but if dividends are not declared in a given year, they accumulate until the company does declare dividends