Chapter 11 - Pure Monopoly Notes

Chapter Contents

Introduction to Pure Monopoly

Barriers to Entry

Monopoly Demand

Output and Price Determination

Economic Effects of Monopoly

Price Discrimination

Regulated Monopoly

Introduction to Pure Monopoly

Definition: A pure monopoly is characterized by a single seller in the market.

Characteristics:

Single seller: Only one firm produces the good or service.

No close substitutes: The product offered by the monopolist is unique and has no direct substitutes.

Price maker: The monopolist has significant control over pricing decisions due to the lack of competition.

Blocked entry: There are significant barriers preventing new firms from entering the market.

Non-price competition: The monopolist may engage in public relations and advertising efforts to increase demand for the product.

Example: Public utility companies often serve as instances of monopolies in specific markets.

Barriers to Entry

Definition: Barriers to entry are obstacles that prevent new firms from easily entering an industry.

Types of Barriers:

Economies of scale: Larger firms may produce goods at a lower cost per unit due to scale advantages, facilitating a natural monopoly.

Network effects: Platforms like the Google search engine become more valuable as more users join, creating a competitive barrier.

Legal barriers: Includes patents and licenses that legally protect a firm's market position.

Control/Ownership over essential resources: A monopolist may own critical resources that new entrants need to access.

Pricing and strategic barriers: Existing firms may use pricing to deter new entrants.

Monopoly Demand

Overview

Market Demand Curve: The demand curve faced by a monopolist is identical to the market demand curve.

Downward Sloping Demand Curve: As the monopolist lowers the price, they can sell more, which means their demand curve slopes downward.

Single-Price Monopoly: The monopolist must reduce the price on all units sold to increase total sales, meaning marginal revenue (MR) is typically less than price.

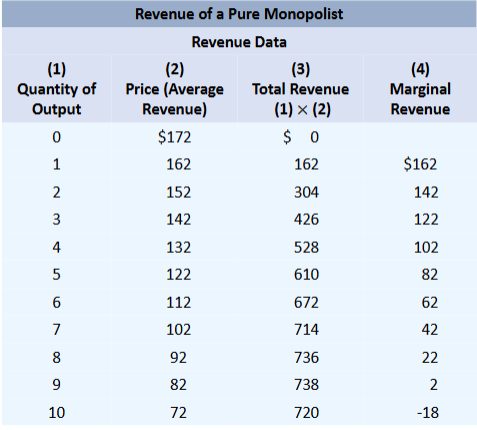

Monopoly Demand Schedule

Revenue Data Table: Outline how revenue changes based on the quantity sold.

Columns:

Quantity of Output

Price (Average Revenue)

Total Revenue (calculated as Quantity × Price)

Marginal Revenue (change in total revenue from selling one more unit)

Price and marginal revenue continuously decrease as more is produced

Example of Revenue Data:

Quantity

Price

Total Revenue

Marginal Revenue

0

$172

$0

-

1

$162

$162

$162

2

$152

$304

$142

…

…

…

…

10

$72

$720

-$18

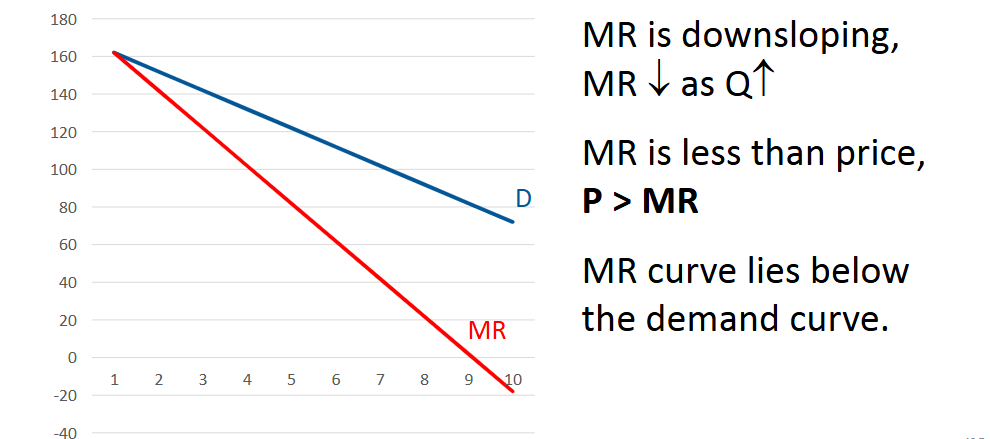

Monopoly Demand, MR, and Price

The marginal revenue curve is downward sloping and lies below the demand curve, highlighting that for a monopolist, P > MR.

Output and Price Decision

To maximize profits:

A monopolist will:

Increase output if MR > MC (Marginal Cost).

Decrease output if MR < MC.

Optimal Output Condition: The monopolist produces at the output level where

Setting Price: Set the price according to the demand schedule

Find where MR =MC then move the point up to the demand curve

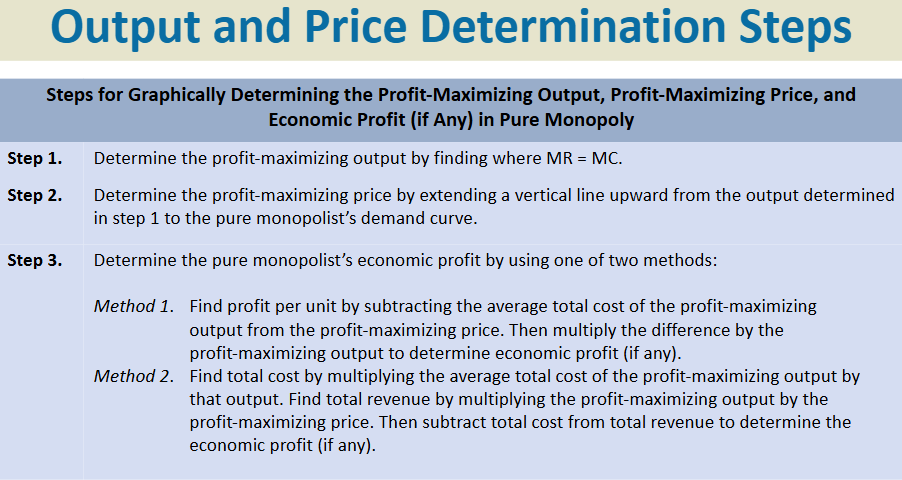

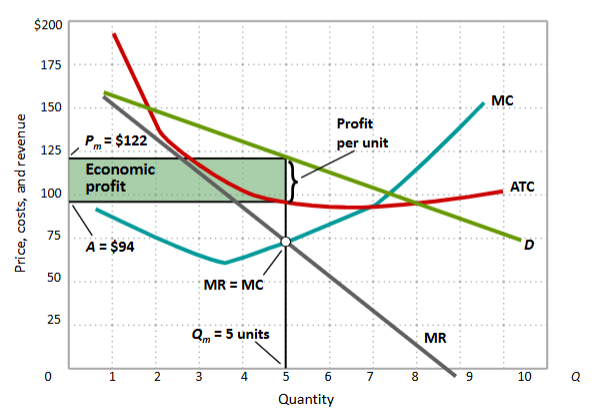

Profit Maximization by a Pure Monopolist

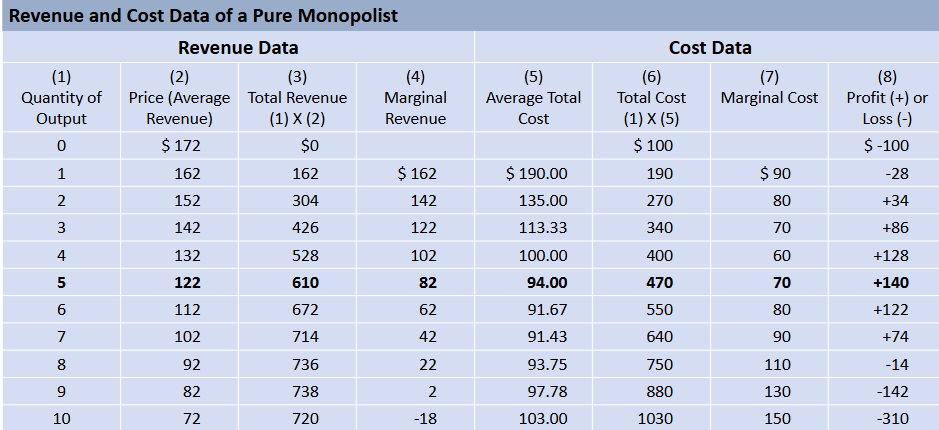

Data Example: Tables capturing total revenue and costs for various output levels.

Revenue and Cost Data:

Graphical Representation: Illustrate the profit maximization process where the output corresponds to the intersection of and .

Misconceptions of Monopoly Pricing

Monopolies do not charge the highest price possible; they aim to maximize total profit rather than unit profit.

Possibility of losses exists if average total costs exceed revenue at output levels.

Inefficiency of Pure Monopoly Relative to a Purely Competitive Industry

Comparison Diagram:

Purely competitive market leads to an equilibrium where .

Monopoly Condition: Monopolists produce less and charge higher prices, failing to achieve allocative and productive efficiency (i.e., P > MC).

Price Discrimination

Definition: Price discrimination involves charging different prices to different buyers for the same product, not based on cost differences.

Conditions for Successful Price Discrimination:

The firm must possess monopoly power.

The market should be capable of segmentation.

There must be a prevention of resale among consumers.

Examples of Price Discrimination

Common applications include:

Business travel

Movie theaters

Golf courses

Railroad companies utilizing different rates for tickets

Coupons and international trade practices

Price Discrimination Applied to Different Groups of Buyers

Economic Framework: Price discrimination may involve adjusting prices for specific consumer groups such as:

Business vs. Small businesses: Charge different rates depending on the buyer's market segment.

Regulated Monopoly

Definition: Refers to the regulation of monopolies to ensure fair pricing and access to consumers.

Types of Pricing Regulation:

Socially Optimal Price: Price set equal to the marginal cost. Often leads to losses for the firm.

Fair-Return Price: Price set equal to average total cost, allowing the firm to earn average profit.

Rate Regulation of a Natural Monopoly

Graph Representation: Illustrate various prices and outputs associated with fair-return and socially optimal pricing in the context of a regulated monopoly.