APPLIED ECONOMICS

Unit 1: Introduction to Applied Economics

Lesson 1.1. Economics as a Social Science

Economics is related to the choices that individuals and societies make. Specifically, it is the discipline that seeks to understand how individuals and societies make decisions in consideration of their scarce resources and unique circumstances.

With that definition in mind, it becomes clear that the subject inherently deals with humans, their activities (choices, consumption, etc.), and their environment (governments, nations, etc.). This characteristic, along with the subject’s use of empirical tools and evidence, qualifies economics as a social science.

Basic Economic Concepts Economists recognize that human wants are unlimited. You may see this in the earlier activity where, given the opportunity, you would bring an endless list of supplies to your deserted island. However, this notion of unlimited human wants directly conflicts with the reality that resources are limited. Although you wanted to bring many things to the deserted island, you could not do so because of limitations that are out of your control.

This is the economic problem that we face: human wants and needs are unlimited, but resources are scarce. It is because of this scarcity that individuals are forced to make choices.

Scarcity

In economics, scarcity is defined as the limited availability of a resource, good, or service. When economists say a resource is scarce, they do not necessarily mean only a small number of this resource. Instead, they say that this resource is limited relative to people’s demand for it.

As an example, let us use scarcity of medical supplies during the coronavirus pandemic. In March 2020, the World Health Organization (WHO) reported that it had already shipped out over 500 million sets of personal protective equipment (PPE) to help countries combat the pandemic. While this number might look substantial on its own, economists would still say that there is a scarcity of PPE because they also consider how much of these PPEs are in demand. In the same report, the WHO reported that 89 million surgical masks are needed per month for the pandemic response. Even though the WHO is sending out many masks, it is still considered scarce relative to the even larger number of people who demand it. In this example, we see that scarcity is not related to the number of resources alone, but the number of resources in proportion to the demand.

Choice

Because of the conflict between infinite human wants and scarce resources, people are forced to choose which personal needs and wants they will satisfy. They have to decide how they will allocate their scarce resources to fulfill the never-ending list of wants they might have. Look back on your decision regarding your senior high school strand. Because a student could only have one academic strand for Grade 11 and Grade 12, you were forced to decide among four options.

The limit of one strand represents your scarce resources, and the decision to pursue any of the four options represents your choice. However, the discipline of economics does not just focus on identifying choices. Instead, it tries to understand how to make these choices effectively. The question is: how do individuals and societies decide which choice makes the most sense? How do you conclude which of the strands is your best choice?

Sometimes, choices are made by identifying the amount of utility we can gain from selecting one option over another.

Utility is a measure that economics uses to weigh the satisfaction or usefulness a consumer can receive when using a product.

For example, if you enjoy eating a specific brand of instant noodles, economists would say that you gain or derive utility from consuming that good. Economists believe that as humans, we are rational beings, and as such, will always make choices that help us maximize our utility. However, it is important to remember that deciding solely on what you can gain from a choice is a biased approach. Doing so disregards the reality of limited resources that we need to take into consideration. Instead, economists evaluate decisions primarily by identifying the corresponding costs or consequences that accompany these choices.

Opportunity Cost

By choosing to pursue the GAS or ABM program, you gave up the chance to take STEM or HumSS instead. The strands that you did not pick are your opportunity costs in this decision.

By recognizing and understanding the costs of our choices, we can properly evaluate our decisions. We can say that a decision is good or bad by comparing what we might have gained from the option we took and what we missed out on by letting the alternatives go.

In understanding scarcity and choice and recognizing opportunity costs, we can begin analyzing how decisions are made.

Wrap-Up

Economics is a study of choices and understanding how scarce resources can be allocated to fulfill unlimited human wants and needs.

Scarcity, or the reality that resources are limited, forces humans to choose where to allocate them.

In making choices, we sometimes consider utility, but inevitably have to give up the alternatives.

Opportunity cost represents the value of the next best option or alternative.

The fields of economics differ in the scope of their study. Microeconomics focuses on individuals and smaller economic agents. On the other hand, macroeconomics looks at aggregates and larger economic agents

Lesson 1.2 Economics as an Applied Science

Economic growth is often viewed as a rising tide that should uplift all the boats within it. However, while this is what it should look like, the reality is often very different. In 2010, the Asian Development Bank identified some unique characteristics of the economic growth experienced by the Philippines compared to other Asian economies. First, it has become slower and is more prone to sudden jumps and dips, and second, it has failed to make a marked impact on poverty reduction.

The Philippines seeks to address this issue through the Philippine Development Plan anchored on the long-term vision entitled AmBisyon Natin 2040, the components of which were developed by the National Economic Development Authority (NEDA). One of the key goals of AmBisyon Natin 2040 is to improve the overall living standards of Filipinos and alleviate or significantly reduce poverty rates.

The problem that we now face is the specific means to achieve such a goal. In the process of finding an answer to this problem through this lesson, we will also understand how economics can be applied to build a stronger and more equitable society.

The first lesson in applied economics focuses on two things: identifying economics as social science and defining the core concepts that surround the discipline, namely scarcity, choice, and opportunity cost. Understanding economics as a social science allows us to apply these concepts to different situations we might find ourselves in, such as deciding which groceries to buy given our budget, or choosing which track to take in senior high school.

However, using economics as an applied science in our current global and national setting requires understanding applications beyond the individual economic agent. We can start by identifying the different questions that economies have to answer with consideration to the specific resources that need to be properly allocated.

The Three Economic Questions

The main economic problem we face is that human wants are unlimited, but resources are scarce. This is the driving force behind the discipline of economics itself, and it is easy for an individual or a small group of people to visualize this problem. In answering this problem on a larger scale, societies are met with these three questions:

● What should we produce?

● How should we produce it?

● For whom should we produce it?

What Should We Produce?

This question asks what products and services an economy should focus on producing. Should they focus on what they are naturally skilled at? Or should they instead allocate their resources toward gaining experience by producing a good that might have future utility? This question also forces societies to consider which of their members’ needs they will prioritize.

How Should We Produce It?

This economic question asks how the economy will produce these goods and services. Will they focus on manual labor or will they shift to modern technology to improve workflow?

For Whom Should We Produce It?

The last economic question asks for whom the final goods and services should be given. Should goods and services be produced for everyone equally, or should it instead be given to those who are capable of paying for them? How about equitably providing these to those who need them most?

While these economic questions have unique characteristics, consequences, and implications, they all share a similarity in determining resource allocation or the process of assigning limited resources to specific uses. The three economic questions enable society to consider their scarce resources when making choices to provide for people's needs.

Factors of Production

As individuals, the different resources that we have to allocate are our time, money, and the opportunity to have new experiences. However, these resources are only applicable when analyzing economic activities from a micro perspective. From a macro perspective, there are four particular resources that societies must decide on how to allocate. These are land, labor, capital, and entrepreneurship.

Land

Land refers to resources that can conceivably be attributed to the land or the sea. It consists of all-natural resources available to us such as clean water, physical land, and even the trees and plant life around us. Some raw materials are also classified under land, such as coal, oil, solar energy, and wind energy.

Labor

Labor is the tangible human element that is involved in the production of goods and services. It is the contributions made by the workforce, whether physical or mental. For example, efforts made by the waiter serving a meal and the jeepney driver bringing passengers from one place to another are all considered as labor.

Capital

Capital is investments made to improve production. These can come in the form of physical capital which is best represented by the different tools and equipment used to make goods. Hammers, heavy machinery, and transportation vehicles are all examples of physical capital. Another form of capital is human capital, which are investments made toward improving the human element of production. This can come in the form of education to better equip the workforce with the skills and knowledge needed to be productive, or even a well-designed healthcare system that allows individuals to stay healthy and be productive for a longer period of time.

Entrepreneurship

This resource refers to the intellectual capacity to organize and put together with other factors of production (land, labor, and capital) to produce goods and services the society needs. It is the vaguest of the four factors, but it is also arguably the most important because, without the coordination of the entrepreneur, the other elements would be significantly less productive on their own.

With a deeper understanding of the concepts of choice, scarcity, and resource allocation on a macro level, we now move on to a typical goal among economies: economic growth.

Economic Growth vs. Economic Development

Economic growth is considered an important goal that any economy should strive for. However, there is a growing opinion among economists that economic growth is not necessarily what we should strive for. They argue that economic development should be considered as our primary economic goal in order to truly build a better society.

Economic Growth

Economic growth is the overall expansion of an economy. This is seen through an increase in gross domestic product (GDP), a statistical measure of total value of goods and services produced within a country during a specific period of time, usually annually. In essence, economic growth looks at how wealthy an economy is by considering the value of goods and services being produced, measured in monetary units.

The issue with economic growth is that it does not accurately represent the actual welfare or well-being of the people residing in a particular country. For instance, there can be positive economic growth due to an increase in military spending, but this may not necessarily translate to improved living conditions among citizens. You could also argue that economic growth can be limited and concentrated among a small group of wealthy elites.

In pursuit of improved well-being and a better society, economists now believe that economic development must be prioritized over economic growth, as economic growth does not measure other aspects considered to be significant in improving overall living conditions.

Economic Development

Economic development is the measure of the welfare and well-being of the economy’s members. In measuring development, a wider range of statistics is taken into consideration.

Economic development does not only look at how much money the economy is making, but it also accounts for the different factors that contribute to an individual’s standard of living.

Oftentimes, the goal of economic development moves toward the idea of equity being more important than efficiency. This concept argues that the focus should shift from just being able to produce all that we are capable of producing, and instead look toward providing to those who need more in an effort to make life as fair and as comfortable to all involved.

Some factors that are taken into account by economic development are the state of poverty in a country, how education and healthcare systems contribute to a productive population, whether or not transportation is viable and easily accessible, and if the environment is kept to a sustainable level, among other factors. These variables can be measured using different statistics such as unemployment rate, literacy rate, average life expectancy of a citizen, and other data that can serve as evidence of improvement in a citizen’s overall well-being.

It is important to acknowledge that economic growth can contribute to economic development. Despite that, economic development looks beyond wealth and takes into consideration other factors that can make a difference in a person’s life.

Sustainable Development

A subset of economic development that has gained traction over the past few decades is the idea of sustainable development. This concept was conceived from the growing reality that while economic growth is (primarily) good and possible, it is not sustainable for future generations if natural resources, such as fossil fuels and other non-renewable resources, are being consumed at a significantly rapid rate.

The concept of sustainable development is defined by the International Institute of Sustainable Development (IISD) as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” This idea asks us to consider not just how to properly allocate resources for current use, but also to take into consideration the world we will leave for later generations.

Inclusive Growth

Going back to the situation presented at the very beginning of this lesson, one of the key goals identified in AmBisyon 2040 was inclusive growth. Inclusive growth is characterized by a growth that not only benefits the elite few but makes equitable provisions for everyone in society. This is growth that helps eliminate poverty, improves the living standards of the majority, and provides opportunities for people to live meaningful lives in a sustainable and environmentally responsible manner.

Why Study Economics?

So, why does it matter if you choose to study economics? It matters because the different lessons you will learn from this discipline will help you make better decisions not just for yourself or the people around you, but also for future generations.

You will be given an opportunity to learn how to discern the actions and policies of local governments and entire nations not just by their explicit costs incurred but also by the different opportunities they forgo. Understanding economics enables you to form well-informed opinions and decisions of your own that represent who you are and what principles you believe in.

Wrap-Up

● The three economic questions are:

○ What should be produced?

○ How should they be produced?

○ For whom should they be produced?

● The four factors of production that societies try to allocate are land, labor, capital, and entrepreneurship.

● Economic growth refers to an increase in the GDP of a country. Economic development focuses on the improvement of the welfare of a country’s citizens.

● Economics is valuable as a discipline because of how it teaches you to make better decisions for yourself, the people around you, and future generations. It also allows you to think critically and form better informed opinions.

Lesson 1.3 Philippine Socioeconomic Development in the 21st Century

The Philippine economy has experienced several ups and downs over the past decades. We have seen periods of continuous positive economic growth and the country was once billed as the “next big thing” in Asia. However, while significantly growing, the economy has also gone through unstable periods of unemployment and poverty. Years of political upheaval, unstable institutions, and the constant ebbs and flows of time have brought us to where we are today.

From martial law to economic booms and recessions, the country and its citizens have witnessed it all. We have firsthand experience of the economic impact of 20 years under a dictatorship, as well as the change in the international perspective after the ousting of a sitting president. Along with the rest of the world, we have survived multiple economic booms and recessions, as well as lived through some of the world’s most calamitous natural disasters and witnessed their impact on our everyday lives.

If anything, all of these experiences should serve as learning opportunities for us to deepen our understanding of our socioeconomic development. We aim to understand the past to put us in the best position to continue striving towards a brighter future.

What characterized these different turning points in our nation’s history? Were there indicators that pointed towards a potential rise or fall for each period? What goals do nations set for themselves when trying to establish a strong economy?

In discussing the different key points of socioeconomic development, there is a need to understand the decision-making process that countries go through in line with the three economic questions. We will also discuss macroeconomic goals, which represent the targets that most economies have in the pursuit of a stronger and more stable economy. The discussion of these goals will be applied through the lens of Philippine economic history.

Economic Systems One of the key takeaways from the previous lesson was the concept of the three economic questions, which refers to the questions that societies have to answer when addressing the economic problem of resource allocation. These questions are: “What do we produce?”, “How do we produce it?”, and “For whom do we produce it?”

In responding to these questions, we are not only after the answer, but we also ask who is making the decision when responding. Is it the government who is answering all three questions, or is it the markets (producers and consumers)? Who dictates the system by which resources are allocated in a specific country? Depending on the answers, different countries will have different economic systems.

Traditional Economic System

In a traditional economic system, the three economic questions are answered through traditions and established trends. In this system, there is very little division of labor, and it is commonplace for sons and daughters to take up their parents' professions.

For example, if Jon was a farmer and had a son named Rick, then under a traditional system, Rick will eventually inherit the farm and work as a farmer himself. Traditional economies are not as widespread as they might have been in the past. However, they are still being utilized in different rural or indigenous communities. There are also characteristics of traditional economies that have influenced certain practices within more modern economic systems.

Command Economic System

In a command economic system, there is a central authority that provides the answers to the three economic questions. The role of this authority is typically filled by the government. In this type of system, the government solely decides how to allocate resources such as labor (who works which kind of jobs) and food (rations).

Command economies can easily adapt to changing circumstances. Because the decision-making is delegated to a central group, they can theoretically make decisions that will put the country in the best position to succeed without having to go through the lengthy processes of elections, debates, or legislation. However, a command economy is susceptible to problems with innovation and motivation.

Without the incentive to profit since goods and resources are government-owned, individuals would have no reason or motivation to work harder. Likewise, this will be the case if goods and services are provided equally by the central planning unit or the government. Moreover, individuals who have the ability and capacity to innovate are less likely to do it because they know that their ideas and improvements will not necessarily benefit them.

Market Economic System

A market economic system is characterized by an economy that has little to no government intervention. In this system, the interactions in the free market provide the answers to the three economic questions. Goods and services are produced depending on the level of demand and are typically produced in the most efficient manner. Resources are allocated based on the consumers’ willingness and ability to pay.

Market economies benefit from high levels of personal incentives for each individual. Because there is an opportunity to profit at a high rate, people are inclined to work harder and longer hours to earn more. Entrepreneurs with great ideas are more likely to innovate and take risks to make it big. As such, the rate of growth is usually far greater in a market economy compared to the other systems.

On the other hand, the lack of government intervention can result in several consequences. Governments often work towards providing for all individuals, and without their participation, a free market is likely to pay little attention to the marginalized and vulnerable sectors of the society. Because there is no economic incentive to provide for those who are in need, they are unlikely to improve their socioeconomic situation.

Mixed Economic System

In reality, there is no such thing as a purely traditional, command, or market economy. Instead, what we might find in modern economies is a mixed economic system that takes all the best characteristics from each of the three economic systems to form a balance between the free market and government intervention.

Almost all economies are some type of mixed economy, though there are rarely ever two that are the same. Each country has its own system in place that reflects the principles it holds as a society with some favoring more government intervention and others preferring a freer market.

Macroeconomic Goals

Throughout the history of the world, countries have had to endure the fundamental economic problem of scarcity. In addressing this problem, governments identify similar goals that they push their economies to achieve. Achieving these goals is expected to improve the socioeconomic status of different countries.

Low Unemployment

Unemployment is defined as the state wherein a person is actively seeking but unable to find work. In understanding the state of unemployment in a particular country, we most often rely on the unemployment rate, which is the number of people who are unemployed expressed as a percentage of the total labor force .

In the Philippines, the labor force is the sum of employed and unemployed individuals aged 15 and older. This represents the economically active population or the population of individuals who are capable of contributing to the economy of the country. Those who are not looking for work for reasons such as schooling, disabilities, or housekeeping are excluded from the labor force.

Countries typically strive for an unemployment rate of around 5%. This relatively low number impacts the economy in two ways. For one, a low unemployment rate points towards the country being efficient with its labor resources. This would mean a higher level of production. At the same time, this also reduces the number of individuals who might be dependent on the social support provided by the government.

Stable Inflation Rate

Another target that governments set is maintaining a stable inflation rate. Inflation refers to an increase in the average price levels of an economy’s basket of goods over a period of time. This basket of goods refers to goods and services that are typically consumed by a household. Usually, statistical agencies report the average inflation rate for all the goods and services. In addition, the inflation rate for specific types of goods and services is also computed and made available to the public.

Economies typically set different targets for their inflation rate, but it should be a single-digit rate or less than ten percent. For 2020, the Philippines has set an inflation target of 1.75% to 3.75%. The target varies depending on the different circumstances and factors within each economy.

Having stable price levels brings about a number of benefits to an economy. Having minimal changes in the prices of commodities allows households to properly plan their spending, as well as safeguard them from sudden spikes in prices that might disrupt their budget. At the same time, economies characterized by stable prices make them a preferable trading partner.

Economic Growth

Along with the two macroeconomic goals is the pursuit of economic growth. We had earlier defined economic growth as an increase in gross domestic product or GDP. Gross domestic product (GDP) is the measure of the value of all final goods and services produced in a country over a given period of time, usually one calendar year. Goods and services included are those that can be produced by individuals or companies of different nationalities or ownership located within the country. As previously discussed, GDP can be measured in three ways, namely the expenditure approach, the income approach, and the output approach. The value of total output can be measured by how much money is being spent in an economy, how much money is being earned, or the value of the goods and services produced. Since these three different approaches measure the same thing, they should yield the same value. Any expense made within an economy should theoretically lead to earnings or income of the same value for someone else. In the same vein, the total value of output should equate to the expenses made for those same goods and services.

Solving for GDP using the Expenditure Approach

When solving for the GDP using the expenditure approach, it is important to recognize the different components that make up the measure. These include consumption, investments, government spending, and net exports.

Consumption (C) refers to the purchase of final goods and services by individuals and households. These can range from durable goods such as refrigerators, vehicles, and gadgets, to non-durable goods that are typically consumed quickly such as food, hygiene products, and the like. Services are actions performed by other individuals, such as healthcare and education.

Investments (I) refer to spending by firms and households on certain capital and long-term goods. Firms can consider spending on capital goods such as equipment, buildings, and machineries as an investment, while households are more likely to consider purchasing a house, land, or an apartment unit as an example of personal investment.

Government spending (G) refers to all government purchases and spending, which include salaries for employees on government payrolls as well as purchases for government projects such as infrastructure. Note that transfer payments or money given out to those who need social support are not considered government spending. This is because these transfer payments do not represent any additional production of goods and services.

Net exports (NX) is a measure of the value of all exports subtracted from the value of all imports. Exports can be defined as goods produced in the country and sold abroad, while imports are goods entering the country from producers elsewhere. When exports are greater than imports, there is a trade surplus.

Meanwhile, when exports are smaller than imports, there is a trade deficit. As such, the formula for GDP under the expenditure approach is GDP = C + I + G + NX.

Assuming you are provided with the details of a country’s expenditure, you can compute the value of GDP.

Step 1: Identify the different expenses incurred by the economy as well as their respective monetary costs.

Step 2: Multiply each expenditure by its respective monetary cost.

Step 3: Add together all of the expenses to find the gross domestic product.

Let’s Calculate

Example 1 : Assume that the economy only has the following goods and services. In a given year, the economy produces 35 books that cost ₱ 450 each, 12 factory machines that cost ₱ 7,500 each, 4 road repair projects that cost ₱ 94,000 each, and finally ₱ 22,500 in net exports. What is the GDP of the economy for that year?

Solution

Step 1: Identify the different expenses incurred by the economy as well as their respective monetary costs. In the aforementioned economy there are:

1. 35 books worth ₱ 450 each

2. 12 factory machines worth ₱ 7,500 each

3. 4 road repair projects worth ₱ 94,000 each

4. Net exports worth a total of ₱ 22,500

Step 2: Multiply each expenditure by its respective monetary cost.

Books: 35 x ₱ 450 = ₱ 15,750

Factory machines: 12 x ₱ 7,500 = ₱ 90,000

Road repair projects: 4 x ₱ 94,000 = ₱ 376,000

Net exports: 1 x ₱ 22,500 = ₱ 22,500

Step 3: Add together all of the expenses to find the gross domestic product.

₱ 15,750 + ₱ 90,000 + ₱ 376,000 + ₱ 22,500 = ₱ 504,250

GDP = ₱ 504,250

Solving for GDP using the Income Approach

When solving for the GDP using the income approach, we can understand the total to be equal to the value of total national income (TNI).

Total national income (TNI) refers to the income generated by the different factors of production, including all wages, rent, interest, and profits earned by members of the economy in a given period. These refer to the income generated by the different factors of production.

Wages (W) are the income generated by the labor force from jobs and self-employment. These are income earned from jobs and self-employment.

Rent (R) is the income that comes from ownership of land.

Interest (I) is the increase in the value of capital goods. This also represents the income generated by this factor of production.

Profit (P) is the income generated by firms operating in the country. This is the income attributed to the factor of production of entrepreneurship.

As such, the formula for GDP under the income approach is GDP = W + R + I + P. Assuming you are provided with the necessary information, you can compute the value of GDP.

Step 1: Identify the different sources of income of an economy as well as their respective monetary gains.

Step 2: Multiply each source of income by its respective monetary gain.

Step 3: Add all of the income to find the gross domestic product.

Let’s Calculate

Example 2 Assume that the economy only has the following factors of production: In a given year, the economy has 15 hairstylists who earn ₱ 180,000 each, with 5 of them earning additional income through the rental of apartment units they own which amounts to ₱ 120,000 each. The economy also has 4 salons that report profits of ₱ 250,000 each. What is the GDP of the economy for that year?

Solution

Step 1: Identify the different sources of income of an economy as well as their respective monetary gains. In the aforementioned economy there are:

1. 15 hairstylists earning ₱ 180,000 each in wages.

2. 5 hairstylists earning ₱ 120,000 each in rent.

3. 4 salons who report profits of ₱ 250,000 each

Step 2: Multiply each source of income by its respective monetary gain.

Hairstylists’ wages: 15 x ₱ 180,000 = ₱ 2,700,000

Hairstylists ‘ rental income: 5 x ₱ 120,000 = ₱ 600,000

Profit of salons: 4 x ₱ 250,000 = ₱ 1,000,000

Step 3: Add together all of the income to find the gross domestic product.

₱ 2,700,000 + ₱ 600,000 + ₱ 1,000,000 = ₱ 4,300,000

GDP = ₱ 4,300,000

Nominal vs. Real GDP

There are two types of GDP, namely the nominal GDP and real GDP. The Nominal GDP refers to the value of the gross domestic product that is not adjusted for inflation. This measure takes the overall value of goods and services produced in a given period with respect to current prices. As such, it is incorrect to compare nominal GDP data over time since we have yet to take into account the changes in prices.

Alternatively, Real GDP focuses on the value of goods and services produced within a given time period with constant prices. The use of constant prices means that the measure is computed using the prices of a specific year called the base year. As such, computing for real GDP with 2010 as the base year would mean that all computations would use the prices of 2010. This would mean that whether you were computing for the real GDP of 1995 or 2015, you would still use the prices of 2010. Computing for GDP using constant prices allows us to account for the changes in price levels. As such, it becomes easier to compare year on year because goods and services are measured using a single price (which is the price of the base year).

Solving for real GDP is similar to the steps mentioned earlier for computing for GDP. However, one has to take into consideration the use of the prices of the base year in making these computations.

Step 1: Identify the different expenses incurred by the economy in a given year.

Step 2: Identify the monetary cost for each expense for the given base year.

Step 3: Multiply each expenditure by its monetary cost in the given base year.

Step 4: Add together all of the expenses to find the real gross domestic product.

Let’s Calculate

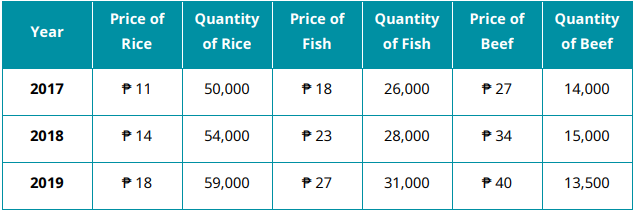

Example 3: Assume that an economy only consumes the following goods: rice, fish, and beef. The data on expenses over the past three years are shown in the table below:

Using 2017 as the base year, what is the real GDP of the economy in 2019?

Solution

Step 1: Identify the different expenses incurred by the economy in a given year. Since we are being asked to solve for real GDP in 2019, we can identify the following expenses for that year:

1. 59,000 units of rice

2. 31,000 units of fish

3. 13,500 units of beef

Step 2: Identify the monetary cost for each expense for the given base year. Take note that the base year is 2017. With that in mind, the costs for each expense in 2017 are:

1. Rice costs ₱ 11 per unit

2. Fish costs ₱ 18 per unit

3. Beef costs ₱ 27 per unit

Step 3: Multiply each expenditure by its monetary cost in the given base year. Since we are solving for the real GDP in 2019, we will use the quantity consumed for each expense in 2019 but multiply them against the prices of 2017 or our base year.

Rice: 59,000 units x ₱ 11 = ₱ 649,000

Fish: 31,000 units x ₱ 18 = ₱ 558,000

Beef: 13,500 units x ₱ 27 = ₱ 364,500

Step 4: Add together all of the expenses to find the real gross domestic product.

₱ 649,000 + ₱ 558,000 + ₱ 364,500 = ₱ 1,571,500

Real GDP in 2019 = ₱ 1,571,500

Another measure of economic activity that can be considered in measuring economic growth is the Gross National Product (GNP). The gross national product consists of similar components to GDP, plus net income from abroad. By taking this into account, GNP effectively represents the value of goods and services produced by all of the citizens of a country wherever they are located. As such, an overseas Filipino worker (OFW) working in the United States would contribute to the GNP of the Philippines but an American working in the Philippines would be contributing to the GNP of the United States.

Positive economic growth usually leads to a higher average income and offers more incentive for innovation in technology, medicine, and other similar fields. Higher economic growth could also be indicative of improved competitiveness in the global market wherein locally produced goods are considered at par with foreign-produced goods or even better.

However, similar to the discussion in the previous lesson, we identified some of the shortcomings of using economic growth as the measure used when trying to understand improvements in an individual's quality of life. More and more economists start to believe that economic growth, while a reliable indicator of economic progress, does not accurately reflect the well-being of its citizens.

Equity in Income Distribution

To specifically address the issue that economic growth does not represent the social reality of inequality, a macroeconomic goal that most nations also take into consideration is equity in income distribution.

To start, we must first differentiate the concept of equality from equity. While equality focuses on providing the same type and amount of resources to everyone, equity focuses on fairness. This would mean redistributing resources towards those who are in need to make the allocation fair to everyone.

Income distribution talks about how the output of a country is distributed or shared with the population. Having an equal distribution of income would mean that every single person in an economy would earn an equal amount of income. As some people earn significantly more while others are barely earning anything, income inequality rises. This can lead to a situation wherein some live extremely exorbitant lifestyles while others are unable to fulfill even their most basic needs.

The idea of achieving equity in income distribution is one that hopes to provide all individuals with an opportunity to have a high quality of life. People would have an opportunity to make an honest, liveable wage that would be enough to provide for their needs. On top of this, an equitable income distribution would also leave incentives for others to innovate and exert more effort towards being a productive member of society. If an economy pursued an equal income distribution, there would be no reason for people to work hard knowing that they would receive the same benefits with those who are not as productive.

Pursuing this macroeconomic goal brings about the potential to significantly alleviate poverty. Reducing and potentially eliminating poverty affects not only the individual but society as a whole. Individuals can lead good lives and at the same time be in a position to contribute to society. Rather than always having to provide government programs for short-term relief, a pursuit of equitable income distribution could lessen the government's burden of providing social support and move towards positive economic growth.

Socioeconomic Development of the Philippines in the 20th Century

With a deeper understanding of the different economic concepts that characterize a nation’s pursuit of socioeconomic development, we are now better equipped to discuss the different highlights in the country’s history. We will be moving from the theoretical and conceptual side of economics and applying these directly to the economic history of the Philippines.

The 1970s and 1980s: Martial Law in the Philippines

This period is often regarded as the “Martial Law Era” of the country. It was during this time that the former president Ferdinand Marcos had the country completely under his rule. Several key economic events and developments characterized former President Marcos’s presidency.

Initially, this period in Philippine history experienced significant positive economic growth attributed to the rise in demand for local raw materials. There were also well-publicized and large scale infrastructure projects that provided numerous job opportunities and helped fuel the economy. However, these pillars of the Philippine economy at the time eventually collapsed. The Marcos administration had a practice of awarding government projects to loyal administration allies. This crony capitalism allowed the closest friends and families of the president to rake in wealth through widespread corruption in the different government projects or positions given to them.

All of these came to a head towards the end of Marcos regime. At this point, inflation was skyrocketing with commodity prices increasing by over 50% by 1984. There were reports of wages for both skilled and unskilled workers falling across the board. The agricultural sector was one of the hardest hit, with a drop of almost 30% in average income being felt by farmers across the country. This fall in wages coupled with the rising prices led to a rise in poverty in the country at the time.

To finance the projects of the administration, the government needed to borrow money abroad and eventually the Philippines’ foreign debt skyrocketed. All the money borrowed helped fund the initial growth that the country experienced in the early years of the administration. However, this short-term thinking led to many long-term consequences that we are still enduring now.

The last few years of the Marcos administration were characterized by the two worst economic contractions the country has experienced garnering the Philippines the title “Sick Man of Asia.” The GDP shrank by 7.3% in 1984 and 1985, representing some of the worst periods of Philippine economic performance. This economic nosedive further fueled the unrest of the Filipino people, eventually culminating in the People Power Revolution of 1986 and the eventual ousting of the Marcos regime.

The late 1980s and early 1990s: The Aquino Administration

Former President Corazon Aquino’s administration inherited a debt-ridden economy that was in a very tough situation. The first agenda that the Aquino administration laid out towards the goal of a more stable economy were efforts and programs to pay off the almost $28 billion in debt the Philippines owed to different countries and international organizations. The unpaid large amount of debt was the first major hurdle the country had to overcome in its pursuit of economic growth. Despite efforts made by the government to reduce the amount of debt, by the end of Aquino’s term it moved in the opposite direction as the debt had slightly increased.

Despite being unable to lessen our foreign debt, the Philippine economy experienced positive growth for the first time in years. Though it was initially slow, momentum picked up towards more respectable growth rates. This was mainly attributed to an initial rise in consumption from private households. However, over time the international community began to develop more faith in the nation’s economy and supported it through investments and other financial aid initiatives.

While the Aquino administration did make strides towards improving the economy of the Philippines, it was not without fault. Programs and legislations towards the alleviation of poverty and the equitable distribution of wealth and income were ineffective and full of loopholes. One of the most prominent examples of this would be the Comprehensive Agrarian Reform Program (CARP) of 1988. The land reform acts aimed to provide farmers with an opportunity to legally own the land they worked on, giving them a better foundation from which to rise out of poverty. However, these programs and laws were poorly designed and implemented as the bodies in charge of executing them had an interest in keeping these resources for a small group of people.

The Rest of the 1990s: The Ramos and Estrada Administrations

Former president Fidel V. Ramos succeeded former president Corazon Aquino as the next president of the Philippines, and it was under his administration that the country became more open to the global economy. One of the main highlights of his administration was the country’s participation in the World Trade Organization (WTO) which brought more opportunities for international trade and economic growth. The administration also put a staunch emphasis on addressing the widespread issue of corruption in the country.

The Ramos administration also faced serious problems, such as the 1997 Asian Financial Crisis and the national power crisis of the early 1990s. The Asian Financial Crisis was the widespread devaluation of currencies throughout Asia that started with the Thailand Baht. The national power crisis of the Philippines began in 1990 wherein Metro Manila and 33 provinces in Luzon experienced brownouts of up to 4 hours per day. Both of these instances significantly halted the country's ability to grow at a rapid pace, which held back our economic growth.

Efforts to curb poverty were also made but failed to be properly executed. Land reform projects from the previous administration were continued but poorly implemented. Although the country experienced positive economic growth, the immense increase in population prevented this growth from impacting the common Filipino. Having more mouths to feed meant needing to stretch resources further. Though programs were put into place to encourage better family planning and reduce population growth, these were insufficient h to make a real impact on poverty reduction.

Following former president Fidel V. Ramos was the incumbent vice president Joseph Estrada. The famous actor was able to convert his mainstream popularity into a successful political career on both the local and national stage. His campaign promised a “pro-poor” stance, and this made him a popular choice among voters. However, his administration was marred by accusations of widespread corruption and cronyism.

While the administration did have bright spots in its pursuit of poverty alleviation as well as increasing the poor’s access to basic social services, the overwhelming reports of corruption led to the early end of Estrada’s presidency. There were reports of misuse of public funds as well as reported payouts received by the administration for protecting different jueteng lords in the late 1990s. In January 2001, the second EDSA revolution brought an end to the Estrada administration and the start of the nine-year term of former President Gloria Macapagal Arroyo.

Modern Economic Problems of the Philippines

Having taken the time to discuss and understand the history of the Philippines’ socioeconomic development in the 20th century, we now move towards understanding the modern economic circumstances of our nation since the start of the 21st century.

Poverty

One of the main problems that every administration faces is widespread poverty. Poverty is defined as the condition wherein individuals lack the financial and material resources to meet their basic needs. In the Philippines, poverty is measured using a poverty threshold or an estimated monthly figure that allows a household of five to meet their basic food and non-food needs. In 2018, the poverty threshold was estimated to be at ₱ 10,727 per month. Achieving the goal of poverty reduction requires the alignment of necessary conditions such as a rise in economic growth, more equitable distribution of income as well as the provision of more employment opportunities for the masses.

Data suggests that the Philippines has been able to reduce the poverty rate of the country over the past two decades, with poverty declining from 26.6% in 2006 to 21.5% in 2015 and finally 16.7% in 2018.

Some of the programs recently established by the government to alleviate poverty include the Pantawid Pamilyang Pilipino Program or the 4Ps, the TRAIN law which sought to reform the current tax systems, as well as the introduction of an improved land reform act that hoped to transfer land from hacienda owners to local farmers. However, these programs had varying levels of success in eliminating poverty.

Corruption

The overwhelming reason behind the failure of implementation of some of the aforementioned projects was due to the corruption happening in both the local and national government. Corruption refers to the misuse of public power in the pursuit of private gain, usually at the expense of the people and society.

Since the onset of the new century, several corruption cases have battered the nation. Included in these are reports of electoral fraud under the Arroyo administration, the well-known Priority Development Assistance Fund scam (better known as the Pork Barrel Scam) of Benigno Aquino III’s term, and recently the PhilHealth 15-B fund corruption.

Each instance of corruption in the country has led to the inefficient allocation of resources that could have been better used to the benefit of the majority (rather than the gain of the few). Other regular instances of corruption at the local level, while considered negligible individually, add up to also serve as an additional roadblock to the development of the nation.

Sustainable and Inclusive Economic Growth

The pursuit of economic growth is something that the Philippines consistently has been able to achieve year in and year out. In recent years the country has been able to maintain GDP growth rates of about 6 to7%, buoyed primarily by a stronger agricultural industry, as well as continuous growth in the industrial and service sectors. Despite the 2008 Global Financial Crisis which caused a dip in the economy’s growth, the Philippines has done well to be the 36th largest economy in 2019.

Despite the promising signs shown by the country, there are still questions that beg to be answered; namely how sustainable and inclusive our current growth trends are. The pursuit of this sustainable and inclusive growth is one of the main rationales behind AmBisyon 2040 which serves as the long-term vision for the Philippines’ socioeconomic development.

While we have achieved high economic growth rates, just how inclusive has this growth been? Experts argue that while we are growing fast as a nation and the poverty rate is indeed going down, too many are still being left behind in the process. Particularly those in the vulnerable sectors such as those working in agriculture who still find it difficult to improve their living conditions. There is also the question of environmental sustainability, with the Philippines ranking 31st in carbon dioxide emissions in 2018, and how the country contributes to the solution. The onset of the coronavirus pandemic also presented a curveball to the positive trend we were working towards, with the closure of businesses and other economic activities causing our economy to experience its worst recession ever.

Wrap-Up

● An economic system dictates how the three economic questions are answered.

○ Traditional economies follow accepted practices from the past.

○ Command economies have a central authority to make decisions.

○ Market economies allow the laws of supply and demand to decide.

○ Mixed economies take the best characteristics of each system.

● The four macroeconomic goals represent the targets most economies strive toward in the pursuit of socioeconomic development. These include:

○ Low unemployment

○ Stable inflation rate

○ Economic growth

○ Equity in income distribution

● The Philippines’ history of socioeconomic development is rife with both high and low points. Each administration brought about some effective and ineffective policies and decisions that led us to the current state of affairs.

● The primary economic problems that the country has to contend with are poverty, corruption, and the pursuit of sustainable and inclusive economic growth.