BE2619_TOPIC03- Cost Control and Event Budgeting ver 2.0.docx

TOPIC 3: COST CONTROL AND EVENT BUDGETING

Learning Objectives:

After completing this topic, you should be able to:

Understand the different financial philosophy of events

Develop a cost control framework

Explain the purpose of budgeting for events

Apply the different estimating techniques for different stages of event planning

Understand the common mistakes in Budgeting

Explain the process in constructing an event budget.

Explain the different types of budgetary approaches.

Prepare a Cost Revenue budget statement.

Financial philosophy of events

Each event budget represents the financial philosophy of the event. Since different event are designed for different purposes, they may fall into the following categories:

Profit-orientated events

In this type of events, revenue exceeds expenses. Organisers of such events are usually commercial operators.

Examples: Product launches, Concerts, Tradeshows, Conferences.

Break-even events

In this type of events, revenue is equal to expenses. Organisers of such events are mostly associations.

Examples: Medical Association Conferences, Singapore MICE Forum by SACEOS.

Loss leaders events

These events are designed from the very beginning to make a loss i.e. budget given. These events are usually organised for the purpose of promoting a cause or agenda and not designed to make a profit or break even. Government agencies are one of the entities who would organise such events.

Examples: Graduation ceremonies, Olympic Games, National Day celebrations.

Cities who invested billions to host the Olympic Games are hoping the level of tourism and foreign investment that result from hosting can create a large impact in the local economy.

Sometimes, a commercial event may be a loss leader event because its aim is to attempt to create a market share of an industry in hopes of the initial investments of such events would bring in revenues in the future.

An event organizer has to consider the financial philosophy of the event before beginning the budget process.

Developing a Cost-Control Framework for Event Operations

A cost-control framework ensures financial discipline and profitability.

Step 1: Budget Planning

Create detailed budgets for each department (venue, catering, marketing).

Include contingency funds (10–15%).

Step 2: Expense Tracking

Use software to monitor real-time spending.

Compare actual vs. projected costs.

Step 3: Vendor Management

Negotiate contracts and seek bulk discounts.

Consider in-kind sponsorships to reduce costs.

Step 4: Resource Optimization

Reuse materials, share resources across events.

Outsource non-core functions when cost-effective.

Step 5: Post-Event Analysis

Conduct financial audits.

Identify overspending and areas for improvement.

Budgeting for Event Projects/Businesses

Budgeting is a planning system

Provides financial and operational guidance especially for the implementation of policies and directives.

When sourcing and enquiring about resources – helps anticipate incoming expenses and identify income to pay for these expenses.

Through planning, potential bottlenecks can be discovered and activities can be co-ordinated.

Can identify roles and responsibilities of stakeholders e.g. government agencies, partners, suppliers/vendors

Budgeting is an incentive system

Provides basis for performance reviews and rewards.

Provides quantifiable financial objectives for planning and evaluating performance.

Example:

Implications on funding when it comes to attracting event tourism in Singapore

Distribution of rewards in the form of commission to sales staff working on event

Budgeting as an accountability system

Business units and their managers are held accountable for transactions and events under their direct influence and control.

Budgets should provide sufficient details to reflect anticipated revenues and costs for activities.

Generates greater awareness of financial outcomes among stakeholders, especially when deviations arise due to poor management and bad execution.

Example:

Who is responsible and for what?

Is there an agreement on how current available resources could be used?

Budgeting as a control system

By monitoring actuals with budget and analysing trends, business management/event project manager can assess overall financial situation and operational effectiveness and alter plans as required.

Linked to event objectives.

Highlight or pre-empt potential problems.

Example:

Personal event: Wedding

Primary objective: To celebrate wedding/union with loved one

Financial objective: To cost less than S$ 30,000

Budget as a communication system

Platform to allow all personnel involved in event project to know what resources are available to get the work done.

Provides timeline and deadlines for getting the job done.

Provides information on who is responsible and accountable for the task to be done.

Example of a simple budget

S/N | Description | Category | Person-in-charge | Quantity | Cost (S$) | Supplier Company |

1 | Balloons Arch | Inflatable Creations | Mr Jack Tan | 1 | $900.00 | Bez Balloons |

2 | Chairs & Tables | Furniture Rentals | Mrs Fanny Lim | 20 Tables 200 Chairs | $1000.00 | Chuan Lam |

3 | Catering | F&B | Mr Chua | For 200 Pax | $5000.00 | Spice Catering |

Estimating

In order to obtain the correct costs for each of the required event items, there is a process known as estimating, and allocating each element into the correct cost centre.

Three approaches:

Analogous estimating (Top-Down estimating)(conceptual/ballpark estimate)

An analogous estimate or “top-down” estimate is usually used in the following scenario:

Events are held for the first time in the local market.

The early development stage of the event to give the management an idea of what the costs are involved.

Event managers would arrive at these costs based on:

Past Experience – past year’s event.

Comparison to events of same scale/type.

Suppliers or expert judgement.

Analogous estimating would usually have an accuracy of +/- 25%.

Example of Analogous estimating:

Contractor A has been selected to submit a budget proposal to the local F1 Grand Prix organiser to construct a series of spectator grand stands for the inaugural Grand Prix event held locally. With no prior experience on building grand stands, Contractor A decided to seek consultation from the company who have built the Melbourne F1 Grand Stand for estimate of building cost as well as building period.

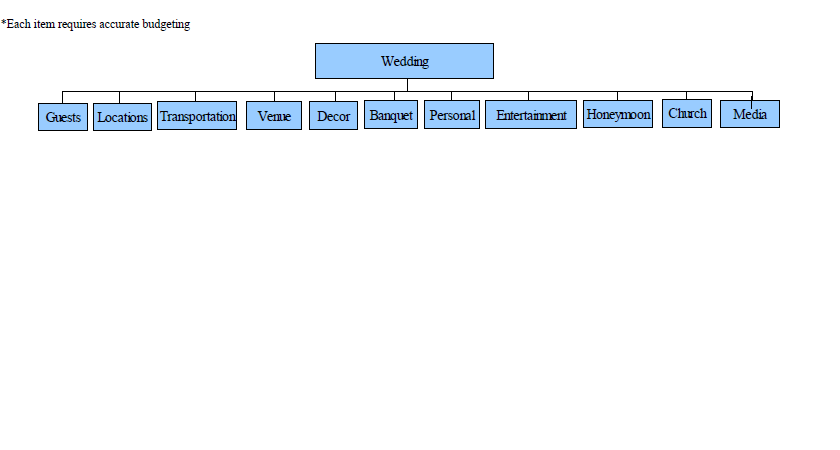

Bottom up estimating

The event is divided into its components and the costs are estimated for each component. This can be done at the planning stage when the Work Breakdown Structure (WBS) is established. During the feasibility study, only the major costs may be identified and estimated i.e. preliminary estimate.

Staff responsible for an activity or with the expertise in a specific area develops the estimates on the lowest level of the WBS and all estimates are added to create estimates for higher level of the WBS and finally for the project level.

Bottom-up estimating comprises estimating the cost of individual component of a project. With all of the costs combined, it would reflect the total cost for the entire event.

This approach would be a more accurate way of estimating in comparison to analogous estimating.

$750

$1050

$1000

$3000

$1700

$8000

$550

$1200

$5000

Free

$300

Grand Total $22,550

(Figure 2.6) Example of a Bottom up estimating of a wedding event

Ways to obtain costs:

Accurate quotes may be obtained by getting suppliers to quote.

Bigger scale events – prices obtained via Tender/Gebiz; Request for quotation (RFQ).

Quote = definitive estimate

Parametric estimating

It is used to estimate the cost of events by using statistical data and mathematical models to estimate the costs of various components of the event.

The following are some of the components of an event that can be estimated using parametric estimating:

Venue costs: The cost of renting the event venue can be estimated by using historical data on venue rental rates, size, location and other factors.

Marketing and advertising costs: The cost of marketing and advertising the event can be estimated by using historical data on the cost of similar campaigns and the expected number of attendees.

Example:

The cost of a one full-day meeting package at a 4-star hotel is S$100/attendee

The cost of booth set up for a special design stand is S$800/sqm

Common mistakes in budgeting

The budget of an event is definitely more complicated than revenues and income as it determines whether the event is successful. The event organizing committee must avoid these common mistakes:

Ignoring the objectives of the event when setting the budget.

Not getting accurate quotes from suppliers, but estimating costs i.e. plucking figures out of the air.

Not involving the whole project team for budgeting therefore failing to identify the full range of the costs accurately.

Being over optimistic about the demand of the event.

Overlooking costs such as taxation, safety and security, handling fees, etc.

Not having enough capital or start-up funds for the initial stage of event that leads to shortage of cash for upfront payments.

Staff spending without proper administrative documentation (receipts, invoices, purchase orders), money is unchecked and there is little control or evidence of the money actually spent.

Did not secure venue with the right capacity for the event.

Process in constructing a budget

A key role of a Project Manager is managing the finance and planning the budget of the project.

Figure 2.1 Building up an event’s budget

Budgetary Approaches

For the events industry, we will study the following budgetary approaches:

Line Budgeting

Program Budgeting

Performance Budgeting

Line Budgeting

A line budget, also known as an itemized budget, is a budget that lists individual items or expenses and their associated costs, e.g. event site rental, F&B service, marketing, AV, decoration, entertainment, operation, logistics, manpower, travel/accommodation, marketing, etc. The line budget shows how much money is allocated to each item or expense and is often presented as a table or spreadsheet.

Line budgeting is the most widely used approach in many organisations because of its simplicity and its control orientation.

It is commonly used when considering tendering for a project.

Advantages:

Simple and easy to prepare.

Organised by functional unit and is consistent with the lines of authority and responsibility in organizational units, this enhances organizational control and allows the accumulation of expenditure data at each functional level.

Allows the accumulation of expenditure data by organizational unit for use in trend or historical analysis.

Disadvantages:

Little useful information to decision makers on the functions and activities of organizational units.

Micro-management by administrators as they attempt to manage operations with little or no performance information.

Example:

Figure 2.2 Example of a Line Budget

For a more in depth example of a line budget, refer to section 7.

In this example you would see that all the monetary figures are sorted and grouped under how the funds will be used.

General groupings in a line budget:

- Cash Revenues (cash which the event is projected to receive).

- In-Kind Revenues (items received that has monetary values).

- Expenses (cash which would be spent by the event).

- In-Kind Expenditures (fulfilments which would be carried out by event).

Program Budgeting

A program budget is a budget that is organized around specific programs or initiatives, rather than individual items or expenses. It is typically used to fund a specific set of activities that are aligned with a particular organizational goal or mission.

In events, an event program budget may consist of a chain of sub budgets which link together to form the overall event budget.

A program budget is developed for a large scale event that has multiple elements or segments.

Example: an art festival is being held in the Singapore city centre. The festival has multiple sub events running concurrently at different venues across the area. In order to increase productivity and ease of operation, individual sub budgets would be established for each sub event. Nonetheless, monitoring of the overall Festival budget is necessary i.e. the project manager has to oversee the entire operation and budget of the festival.

Advantages:

It assists in establishing priorities of the event.

It improves the clarity of deliverables for each sub events.

Allows cost monitoring; helps identify areas where excessive funds are used.

This approach increases the responsibility of the event management team as each sub event management team is accountable for its own budget.

Disadvantages:

There would be an enormous information that is required to be processed and requires more time to conclude an accurate overall budget overview.

Overlapping submission of similar expenditure to the budget will result in exponential increase in the margin of error.

Having an accurate performance evaluation of the entire event budget would be challenging as there are different management approaches overseeing different aspects of the event.

Figure 2.3 Difference between a line and program budget

In summary, a line budget focuses on individual items or expenses, while a program budget focuses on specific programs or initiatives. The choice of which type of budget to use will depend on the organization/event personnel's goals, needs and priorities.

Note: At business level, a big firm may have many different projects running at a single time. Therefore, it is important to set the goals and objectives of each individual project, along with its budget. The program budget for the business allocates resources to different projects, which helps in monitoring the performance of the projects and increases accountability.

Performance Budgeting

Performance budgeting is a system of planning, budgeting, and evaluation that emphasizes the relationship between money budgeted and results expected.

This is used when evaluating the success of the project and whether the company should tender for the project again the following year.

Performance budgeting:

Focuses on results. Functional units are held accountable to certain performance standards.

Is flexible. Money is often allocated in lump sums rather than line-item budgets, giving managers the flexibility to determine how best to achieve results.

Is inclusive. It involves policymakers, managers and stakeholders in the budget “discussion” through the development of strategic plans, identification of spending priorities and evaluation of performance.

Has a long-term perspective. By recognizing the relationship between strategic planning and resource allocation, performance budgeting focuses more attention on longer time horizons.

Example:

Figure 2.4 Example of a Performance Budget

Overall, an event performance budget emphasizes the importance of achieving results and outcomes, rather than simply tracking inputs or money spent on various event activities. The goal is to ensure that the organization is achieving its objectives effectively and efficiently.

Sample of Line Budget

Sample of Program Budget

Event Name: Industry Innovation & Sustainability Conference

Event Type: Physical Conference (1 Day)

Target Audience: Industry professionals & partners

Expected Attendance: 150 pax

Budgeting Approach: Program-based (by event objective)

Program 1: Knowledge & Content Delivery

Objective: Deliver high-quality industry insights and thought leadership

Cost Item | Description | Budget (SGD) |

Keynote Speaker Fees | 2 keynote speakers | 4,000 |

Panel Speakers Honorarium | 4 panelists | 2,000 |

Moderator / Emcee | Professional facilitator | 1,200 |

Content Development | Agenda design, speaker coordination | 800 |

Program 1 Subtotal | 8,000 |

Program 2: Event Experience & Production

Objective: Ensure professional event execution and positive attendee experience

Cost Item | Description | Budget (SGD) |

Venue Rental | Conference hall | 7,000 |

Audio-Visual & Technical | Sound, screen, livestream | 3,000 |

Stage, Backdrop & Branding | Stage design, signage | 2,000 |

Event Operations Crew | Event manager, technicians | 2,500 |

Program 2 Subtotal | 14,500 |

Program 3: Audience Engagement & Outreach

Objective: Attract target participants and maximise attendance

Cost Item | Description | Budget (SGD) |

Marketing & Promotion | EDMs, social media ads | 2,500 |

Event Collaterals | Program booklet, signage | 1,000 |

Registration Platform | Online ticketing system | 600 |

Photography & Media | Event documentation | 1,200 |

Program 3 Subtotal | 5,300 |

Program 4: Participant Hospitality

Objective: Provide a comfortable and professional networking environment

Cost Item | Description | Budget (SGD) |

Catering (Meals & Refreshments) | 150 pax × $35 | 5,250 |

Speakers’ Hospitality | Meals & lounge access | 750 |

Program 4 Subtotal | 6,000 |

Program 5: Sustainability & Risk Management

Objective: Ensure compliance, safety, and sustainability outcomes

Cost Item | Description | Budget (SGD) |

Event Insurance & Licences | Public liability | 400 |

Sustainable Materials | Digital programs, eco signage | 600 |

Waste Management | Recycling & disposal | 300 |

Contingency | ~5% of total budget | 1,700 |

Program 5 Subtotal | 3,000 |

Program Budget Summary

Program | Budget (SGD) |

Program 1: Content Delivery | 8,000 |

Program 2: Event Production | 14,500 |

Program 3: Engagement & Outreach | 5,300 |

Program 4: Hospitality | 6,000 |

Program 5: Sustainability & Risk | 3,000 |

Total Event Budget | 36,800 |

Sample of Performance Budget