1.3 + 1.4 - responsibility accounting & motivation & incentive schemes

responsibility accounting

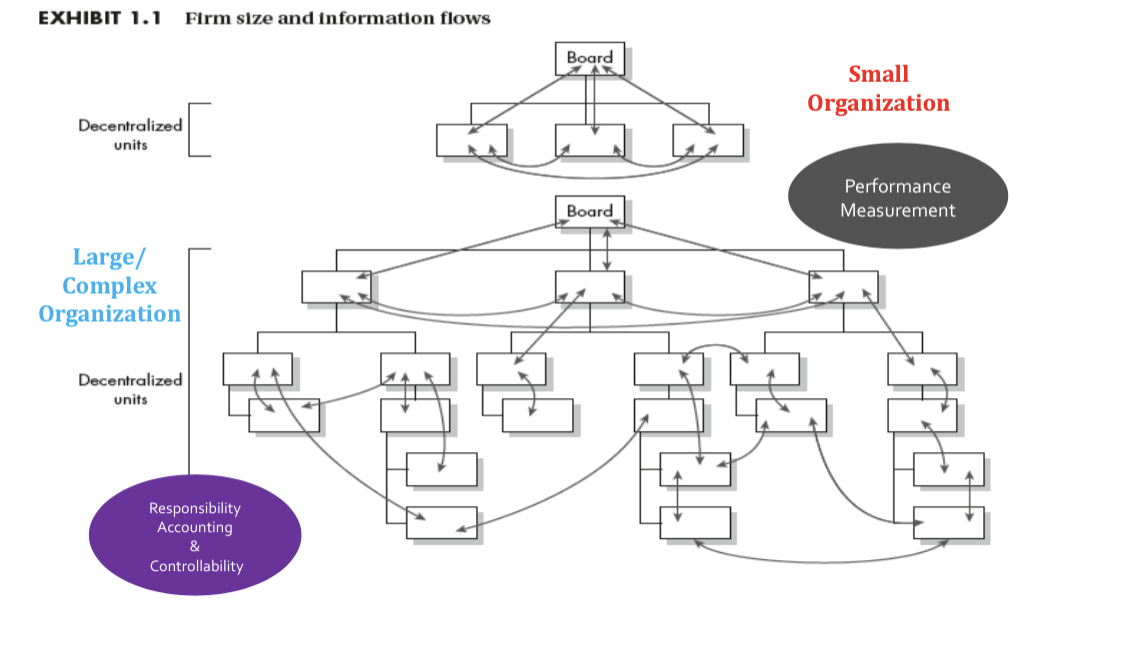

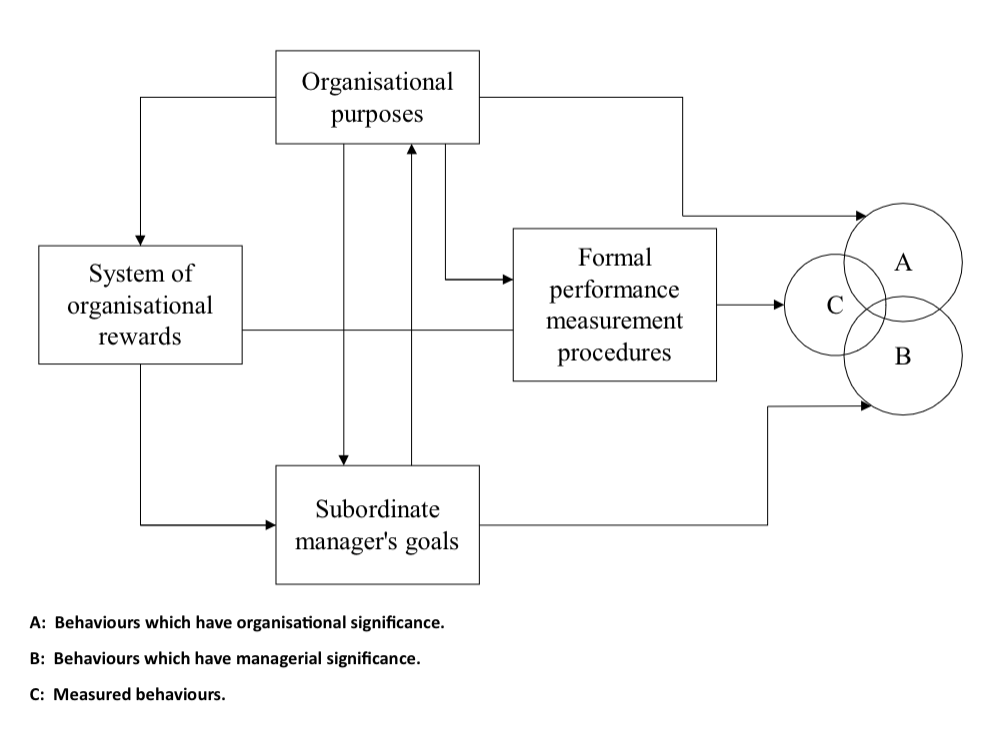

responsibility accounting emerges as a consequence of the way in which organisations are structured and refers to the delegation of organisational responsibility and accountability throughout the organisation

most organisations evaluate performance and control behaviours through their performance measures, typically financial and non financial result controls

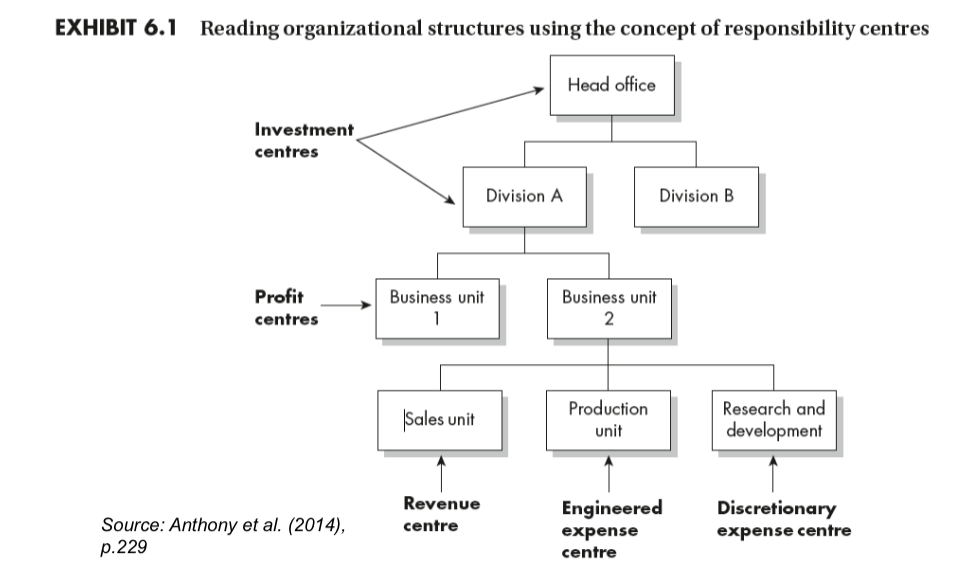

organisational structure & responsibility accounting

financial responsibility

cost centres:

managers are held responsible only for fixed and variable costs within their control

performance measures are based on controllable cost management

revenue centres:

managers are held responsible for revenue streams within their control.

measure based on sales/order books against budgets or quotas

profit centres:

managers are held responsible for income, fixed and variable costs, within their control

measure based on controllable operating profit or controllable contribution

investment centres:

managers are held responsible for investment decisions, income and fixed and variable costs within their control

controllable operating profit includes costs of controllable investment, financing costs of controllable investment

organisational structure and responsibility accounting

controllability principle

what is meant by “the controllability principle“, and how does it relate to responsibility accounting?

“in the evaluation of a manger’s performance, only the factors under his control should be considered“ - Choudhury, 1986

“accounting texts often say that a performance measure should include whatever is controllable by an employee.“ - Lazear and Gibbs, 2015

what do we do with unpredictable/uncontrollable factors?

issues with applying the controllability principle

controllability principle reflects the issue of accountability

fair assessment of performance - evaluation systems should filter ‘external‘ effects from the managers performance

can we control for the uncontrollable? how to mitigate the risk they pose?

insurance, variance analysis, flexible budgeting

excuse culture

to protect from uncontrollable factors, managers take actions not necessarily in the interests of the organisation, i.e. budget padding/slack income smoothing

relevance and complexity of controllability

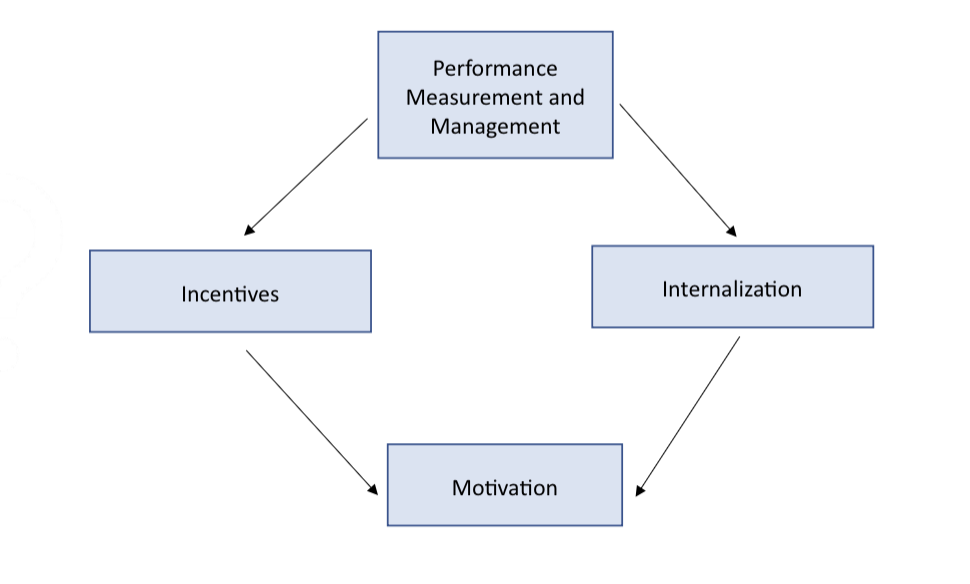

why is motivation important?

motivation and management control systems

why do we need an understanding of motivation to implement management control systems?

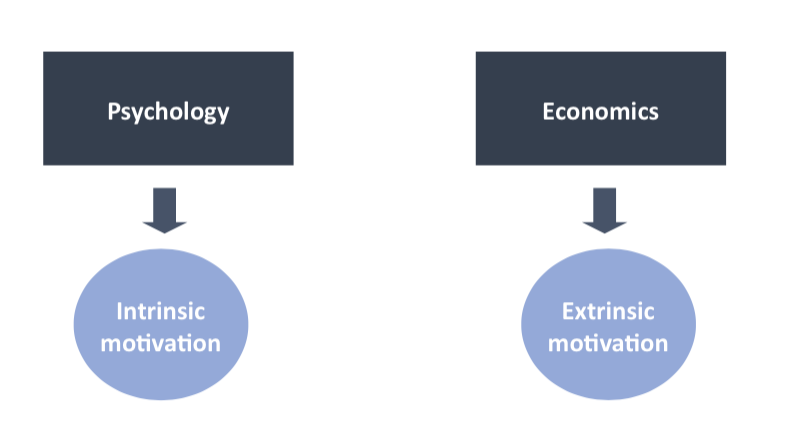

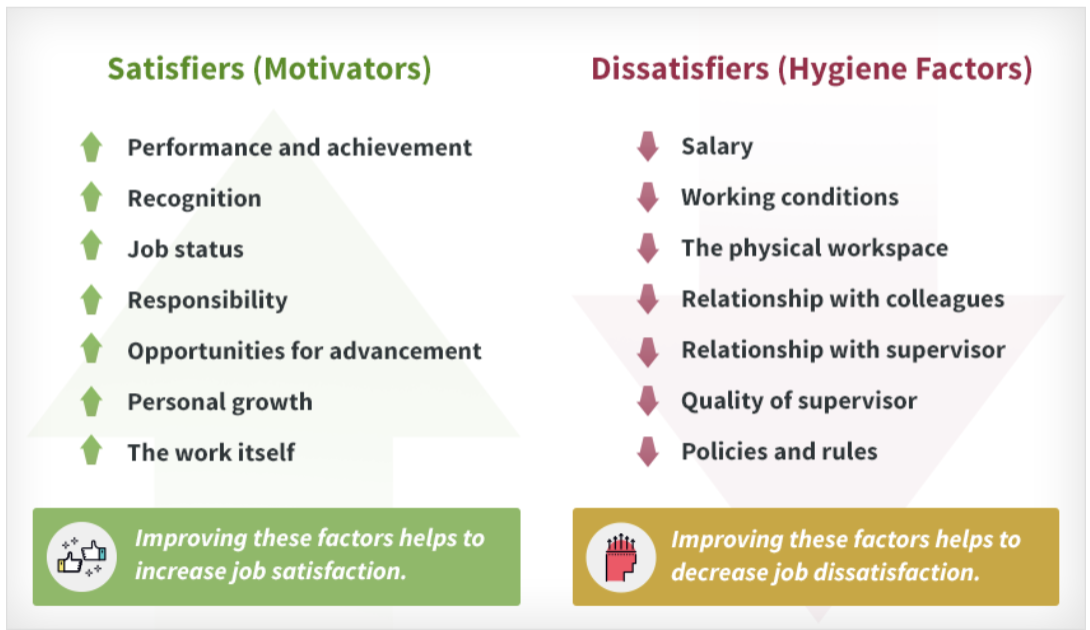

intrinsic and extrinsic motivation

intrinsic motivation

taps into innate ‘psychological’ rewards - the activity is interesting to the individual and therefore it provides its own reward

the motivation is inherent, the activity is meaningful

intrinsic motivation is stimulated by things like receiving recognition, opportunities for challenge and personal development, good treatment at work, autonomy

extrinsic motivation

performing an activity to receive an external reward or to avoid punishment

external motivators

focus is on the consequences/outcome rather than the activity itself

tangible rewards, e.g. salary, fringe benefits, bonuses, promotion, job security

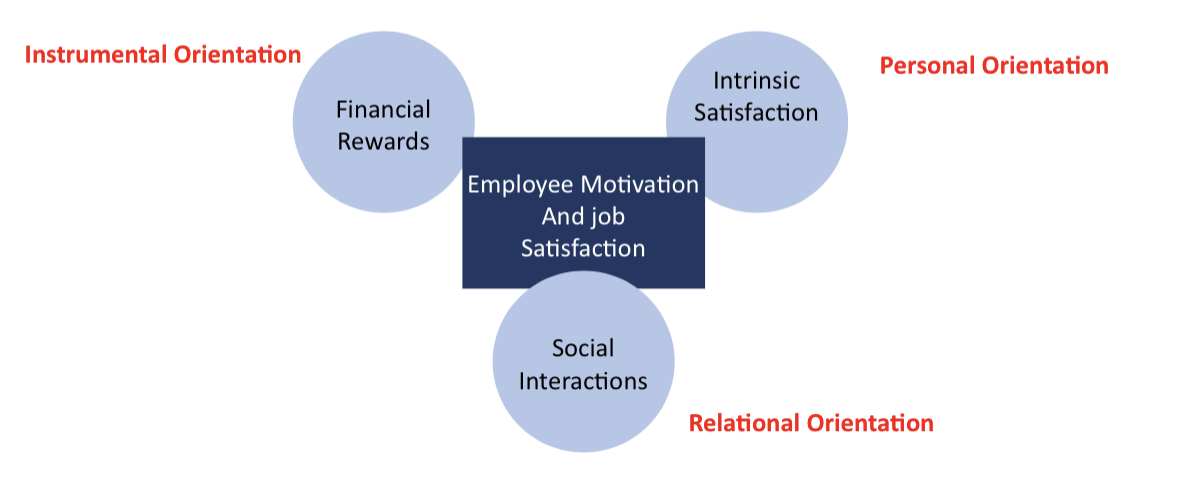

factors affecting/making sense of motivation

complicated relationship between extrinsic rewards and intrinsic motivation

extrinsic rewards/tangible rewards act as control as they are intended to shape behaviours

such rewards then may affect intrinsic motivation as they negatively affect perceived autonomy [e.g. Alfie Kohn on fostering intrinsic motivation on learning/education]

studies suggest that punishment, deadlines, performance evaluation and competition may also undermine intrinsic motivation

choice and autonomy, feelings, acknowledgement increase intrinsic motivation

relevance for management control

incentive and reward systems

incentive systems and pay for performance

“it took me a long while to learn that people do what you pay them to do, now what you ask them to do.“ - Avon CEO Hicks Waldron

if an incentive system is designed well, it can be an important source of value creation, but if designed poorly, it can be a source of value destruction

purpose of incentives

pay

attraction/retention of employees

flexible compensation

tax considerations/regulations

motivation - inducing and directing effort

goal congruence

types of incentives

fixed pay

short term variable incentives

long term, i.e;

stock options

restricted stock plans

incentives based on non-financial measures

non-financial incentives

group rewards

team based rewards are often used to implement personnel/cultural controls

group members monitor and sanction each other’s behaviour

they rarely provide a direct incentive effect

stock based plans, for instance, provide direct incentives only for a small number of managers at the very top of the firm

quick question

how would you reward a group of professionals that includes product designers, engineers, production personnel, purchasing agents, marketing staff and accountants whose job is to identify and develop a new car?

how would you reward a person whose job is to discover a better way of designing crash protection devices in cars?

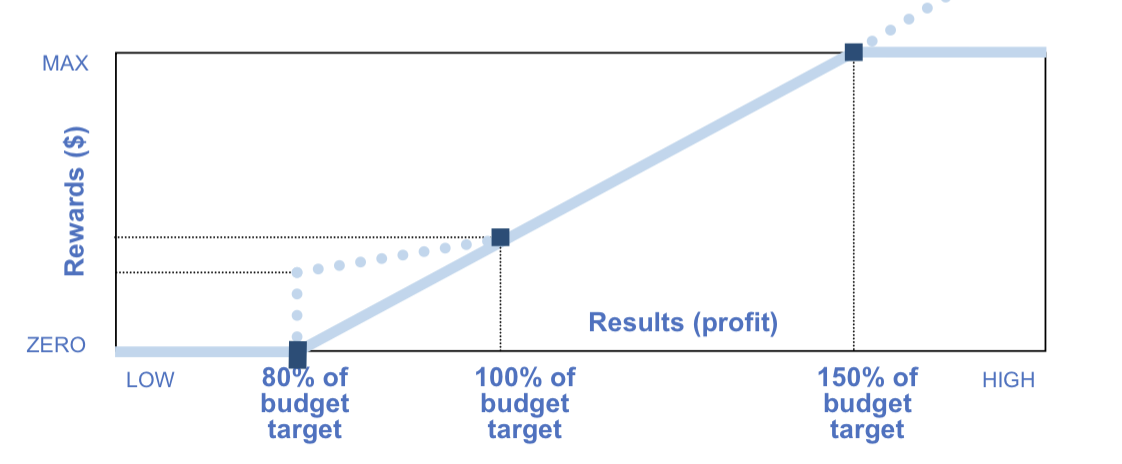

shape of incentives function

commonly, the link between incentives and results is linear, but over a restricted performance range only

designing an effective incentive system

managers should have a clear understanding of:

the measured performance variables for their job

how their behaviour affects the measured performance variables

how the measured performance variables translate into individual rewards

controllability element and based on the nature of work

rewarding outcomes or inputs?

criteria for evaluating reward systems

rewards should be:

valued

large enough to have impact

understandable

timely

durable

reversible

cost efficient

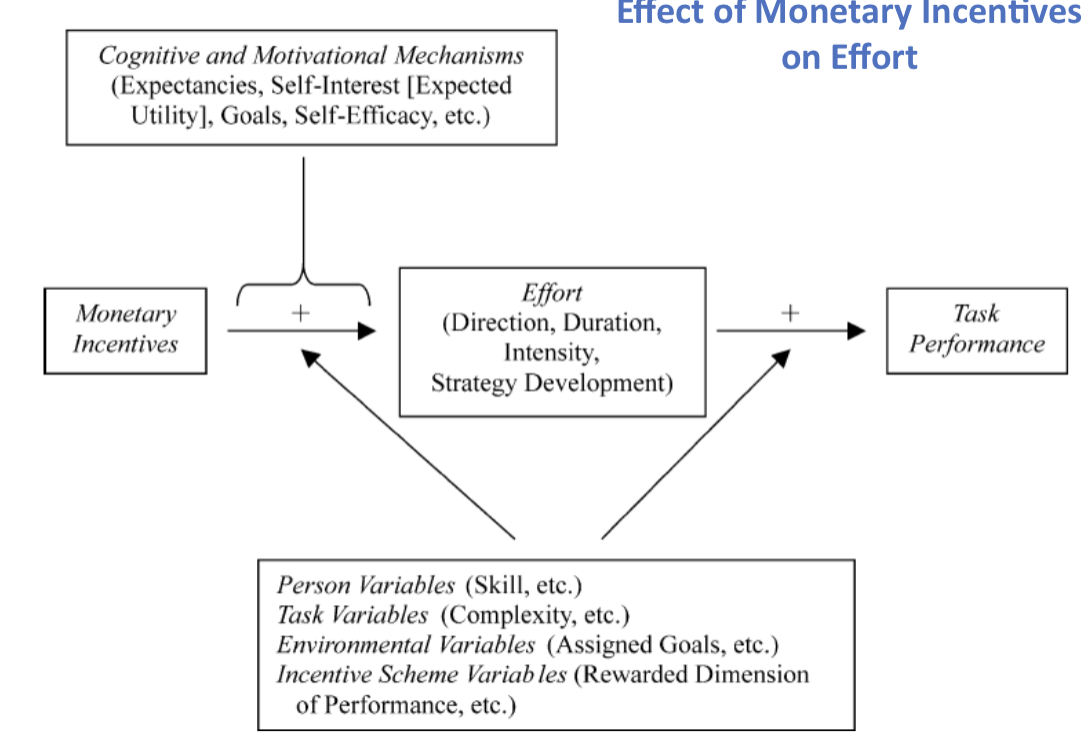

monetary incentives and theories of motivation

how do monetary incentives lead to increased effort/performance?

theories of motivation

content theories - what are people motivated by?

maslow’s hierarchy of needs

content theory of motivation - Herzberg’s 2 factor theory

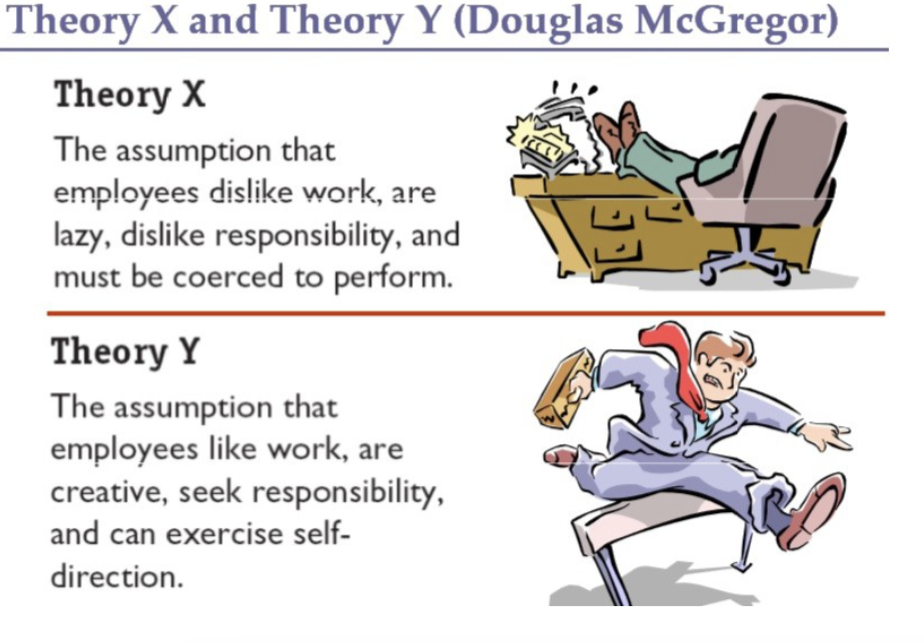

content theory of motivation - McGregor’s theory X and theory Y

how are people motivated?

process theories

concerned with understanding the variables that make up motivation and actions that are required to influence behaviour

expectancy theory

agency theory

goal-setting theory

social-efficacy theory

equity theory

expectancy theory

cognitive theory assuming individuals are purposive and aware of goals and actions - assumes instrumentality [belief that good performance will lead to valued outcome]

individuals are influenced by the expected results of their actions. people act in order to maximise expected satisfaction.

levels of motivation are not only dependent upon expectancy. it also depends on the likelihood of receiving reward, [instrumentality], and the perceived value of the reward [valence]

monetary incentives and expectancy theory

outcome of interest is the financial reward - monetary incentives have greater valence

motivation is higher when there are monetary incentives. increased efforts

rewards must reflect the effort required, the type of reward desired and promises of rewards must be kept

the principal - agent perspective - agency theory

incentive problem - divergent preference and objective between principals and agents; all individuals act in their own self interest

in MCS, two types of principal-agent relationship

managers prefer more wealth to less, but marginal utility, or satisfaction decreases as more wealth is accumulated

monetary incentives & agency theory

agents are risk averse and therefore expect risk premium

only extrinsic rewards

incentives not contingent on performance do not satisfy economic well being

individuals only engage in tasks that contribute to their own economic well-being. monetary incentives increase economic well being and hence greater effort will lead to a greater probability of improved economic well being

goal setting theory [locke and latham, 1990]

personal goals and intentions are the primary determinant of effort and behaviour

impact on MCS:

goals should be difficult to achieve and specific rather than general ‘do your best goals‘

clear, quantifiable targets provide structure and increased motivation

motivation increases when these targets are demanding, but achievable

feedback on performance is necessary for goal achievement. specific and challenging personal goals lead to greater effort.

monetary incentives and goal setting theory

monetary incentives may:

causes people to set goals they would not normally set

cause people to set more challenging goals than otherwise would - outcome attractiveness by incentives

lead to higher goal commitment than non-contingent incentives or not incentives

social efficacy theory

self regulatory cognitive mechanisms

an individuals belief regarding their ability to achieve a task regulates levels of effort

the extent to which individuals believe in themselves and hence their willingness to take on challenges and setting of high personal goals - individuals regulate their own effort

monetary incentives seem to have similar impact to goal setting theory

equity theory

individuals are motivated by fairness

a feeling of fair compensation has a positive effect on their motivation

if individuals perceive an inequity, they will adjust their inputs - put less effort - so the equation is always in balance

referent groups for comparison can be internal or external of the organisation

do monetary rewards always work?

factors that moderate the effectiveness of monetary incentives:

person variables:

personality, skills, ability

task variables:

complexity, attractiveness, interesting

environmental variables:

time pressure

incentive scheme variables:

magnitude and timing of incentives, issue of controllability

what drives employee engagement?

evidence suggests that monetary incentives do not always lead to greater effort and do not result in improved performance

monetary incentives can detract from intrinsic sources of motivation

helliwell and huang 2006:

trust of your manager - worth 36% pay raise

a job with variety of tasks to perform - 21%

job requiring high level of skills - 19%

having enough time to finish assigned work - 11%

why rewards do not work

rewards get temporary compliance

pay doesn’t motivate

rewards punish

rewards rupture relationships

rewards ignore the causes behind problems

rewards kill creativity

rewards undermine interest

rewards may lead to unethical behaviours

incentive systems are powerful drivers of behaviour

can incentive strucutres encourage the wrong kind of decision making?

what about the subprime market crisis?

bankers bonuses?

mis-selling scandals? PPI scandals?

consequences of poorly designed incentives systems

executive pay/severance pay

Carol Bartz appointed CEO of Yahoo in 2009 with a signing-on package $47.2m in cash and stock options. Left in 2010 with 11.9m pay package, while the company’s revenue fell 2% in that fiscal year

Barclays CEO Antony Jenkins received an exit package of “more than £50m” when he left Barclays in 2009.

Disney’s Michael Eisner was paid $38 million above the industry average when for three out of six years the company’s performance declined in relation to other firms in the entertainment industry

conclusion

management accounting systems need to recognise the importance of incentive compensation plans

motivation affects behaviour rather than performance so incentives may not be successful if there is a weak link between employee efforts and job performance

it is difficult to define the right metric and anticipate exactly how your people will react to it