LIFE INSURANCE POLICY TYPES

KEYWORDS: LIFE INSURANCE POLICY TYPES

Prior to reading this chapter, please review the following keywords. An understanding of their basic definitions will improve your comprehension of the chapter content.

Accidental Death and Dismemberment Insurance (AD&D): This is a form of insurance that provides benefits in the event of accidental death; the accidental loss of sight, speech, or hearing; loss of use of limbs (i.e., paralysis); or loss of a member(s), such as the loss of an arm or a leg.

Accidental Death Benefit (ADB): The ADB provides a lump-sum payment for loss of life due to an accident that was the direct cause of death. The cause of the death must be accidental for a benefit to be payable under the policy.

Additional Premium: This provision is used in Universal Life Policies. Additional premiums can be paid into the policy account in an amount above the target premium. Current tax laws limit the amount of excess cash value that can be accumulated in a life insurance policy. The insurance company may not accept the additional premium if it nears this limit without increasing the limit of life insurance (subject to underwriting).

Attained Age: This is the age that a person or an insured has attained as of a given date. For life insurance purposes, the age is based on either the nearest birthday or the last birthday, depending on the practices of the insurance company involved. Attained age is also referred to as “current age.”

Adjustable Life Insurance: This is a type of policy that combines permanent, whole life, and temporary term life into a single plan that provides the policy owner with the flexibility to adjust premiums throughout the life of the policy.

Cash Surrender Value: This is the amount that’s available in cash upon the surrender of a policy by the owner before or after the policy matures (as a death claim or otherwise). This value is also simply referred to as surrender value.

Cash Value: This is the equity portion of a whole life policy that increases with each subsequent premium payment. The insurer pays interest on the cash value, which is tax-deferred. In a whole life policy, the cash value is designed to equal the policy’s death benefit at age 100. Traditional whole life insurance policies are considered to mature when the insured attains the age of 100.

Credit Insurance: This is insurance that’s designed to pay the balance of a loan if the insured dies or becomes permanently disabled before the loan has been repaid in full. Generally, credit insurance is sold by a lender or finance company.

Convertible Term Life Insurance: This is temporary life insurance that provides the policy owner with the right to exchange an existing policy for other policies that are offered by the insurance company. This conversion may be the conversion of individual term insurance to an individual permanent plan that a company sells or the conversion of group disability, life, or health to an individual plan.

Decreasing Term Insurance: This is a type of temporary or pure protection that’s characterized by a reducing face amount each year and the cost of this coverage remains constant. Decreasing term insurance may be referred to as mortgage redemption or mortgage protection insurance since it’s primarily used in conjunction with a debt or loan.

Endowment Contract: This contract pays a face amount after a fixed time period, at a specific age, or upon the death of the insured if it occurs before the end of the period.

Evidence of Insurability: This involves an insurance applicant establishing the fact that they meet the insurance company’s health requirements. Statements of good health, attending physician statements, health history, and an applicant’s current health can all be used as evidence of insurability.

Extended Term Insurance: This is a non-forfeiture option that’s available when a policy is surrendered and the same face amount of the policy is continued in force for a specified additional period; however, the coverage has changed from permanent to level term protection. Extended term insurance is the non-forfeiture option that provides the policy owner with the highest face amount of coverage.

Face Amount: This is another name for the death benefit of a life insurance policy.

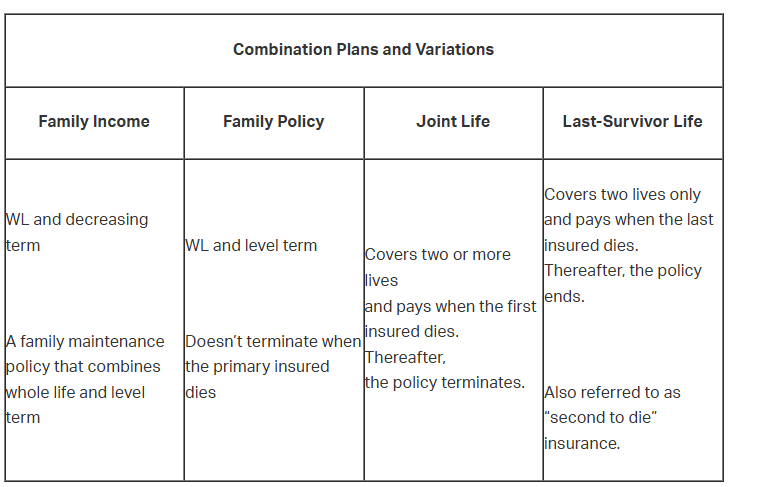

Family Income Policy: This is a policy that combines a whole life policy with a decreasing term rider to provide a death benefit together with monthly income payments to the beneficiary. Monthly income payments are made only from the date of death until the maturity date of the contract. Thereafter, the lump sum part of the whole life coverage is paid.

Family Maintenance Policy: This is a type of policy that combines whole life insurance and a level term rider. It provides for the payment of a monthly income during a stated period of years once the insured dies. The monthly income is payable from the date of death to the end of the pre-selected period. The payment of the face amount of the policy is payable at the end of the pre-selected period.

Family Policy: This is a policy that covers an entire family. Whole life insurance covers the primary insured (i.e., breadwinner) with varying amounts of level term insurance on the remainder of the family.

Guideline Premium: This represents the maximum premium that can be paid into universal life policies and still have the benefit qualify as life insurance under federal tax laws. If a guideline premium is paid regularly, there may be little margin for any additional premium payments into a universal life insurance policy account.

Indexed Contracts: These are contracts in which the policy holder can share in a percentage of the growth of an indexed investment (e.g., a mutual fund tied to the Standard & Poor’s Index). The principle (benefit) is guaranteed, and in many cases, a minimum interest is guaranteed. These products are not considered securities.

Increasing Term Life Insurance: This is term life insurance that provides an increasing face amount over time based on specific amounts or a percentage of the original face amount.

Industrial Life Insurance: This is insurance under which premiums are paid monthly or more often (i.e., weekly). Additionally, the face amount of the policy doesn’t exceed a stated amount, and the words “industrial policy” are printed in prominent type on the face of the policy. Industrial life insurance is also referred to as “debit insurance.”

Joint Life Insurance (First to Die Insurance): This is a life insurance policy that covers the lives of two or more persons. The policy pays a death benefit and ends when the first insured dies. This type of policy is also referred to as “first to die” insurance.

Joint Life Survivor (Last to Die Insurance): This is a life insurance policy that covers the lives of two or more persons. The policy pays a death benefit and ends when the last insured dies. This type of policy is also referred to as “last to die” insurance.

Juvenile Life Insurance: This is a life insurance policy that’s owned by an adult and written on the lives of children.

Level Premium: This describes a premium that remains constant, fixed, or predetermined throughout the life of a policy.

Life Insurance: This represents insurance on the lives of human beings that creates an immediate and guaranteed estate upon the death of an insured or at the end of a predetermined period (in whole life insurance, this is age 100).

Limited Pay Life Insurance: This is a life insurance plan under which the premiums are payable for a specified number of years, after which the policy remains in effect for life without any additional payments. However, the policy still doesn’t mature until age 100.

Maturity Date: This is the date on which a life insurance policy becomes payable due to the death of the insured or as a result of an insured’s living to the end of a specified period (i.e., age 100). In whole life insurance, the cash value is designed to equal the face amount at maturity.

Maturity Value: This is the amount that’s paid under a whole life insurance contract if the insured reaches the age of the mortality table on which the contract was based. If it’s an endowment contract, it represents the cash value amount at the end of the endowment period.

Modified Endowment Contract (MEC): This is a whole life insurance policy under which the amount a policy owner pays in premium during the early years exceeds the sum of premiums required for the first seven years of insurance. The IRS views MECs as the policy owner’s attempt to use the policy as a short-term investment vehicle, and as such, the policy will be designated for tax purposes as an MEC.

Modified Life Policy: This is a whole life plan that’s characterized by a lower premium during the initial years of the contract to make it more affordable for the policy owner. The premium then increases after this introductory period and remains level for the life of the contract.

Mortgage Redemption Plan: This is another name for a decreasing term life insurance policy. This type of plan is used to provide funds for a survivor to pay off a debt. This type of plan is also referred to as mortgage protection coverage or reducing term insurance.

Mutual Insurance Company: This is an insurance company that’s owned and controlled by its policy holders. Mutual insurance companies issue participating policies that may pay dividends to policy holders.

Non-Forfeiture Values: These are benefits that are required by law to be made available to the policy owner if she surrenders the policy by discontinuing premium payments. These values state that the owner will not forfeit or lose all that she has invested in the policy. Also referred to as non-forfeiture options, they include surrender for cash, extended term insurance, and reduced paid-up insurance.

Non-Medical Life Insurance: This is issued without requiring the applicant to submit to a medical examination. The insurer relies on the applicant’s answers to the questions regarding his physical condition, personal references, and inspection reports. However, the insurance company retains the right to require a medical examination if an investigation indicates a need for one.

Non-Participating Insurance: This is a type of insurance policy that’s issued by a stock insurer. This form of insurance contract doesn’t pay dividends to the policy holders.

Ordinary Life Insurance: This is most often described as an insurance policy that’s issued by commercial insurers with face values of $1,000, or multiples thereof.

Paid-Up Insurance: This is life insurance on which future premium payments are not required. Frequently, the term is used to identify a 10, 20, or 30 payment life insurance policy on which 10, 20, or 30 annual premium payments have been paid. Although the policy is “paid-up” at the end of the payment period, the contract doesn’t mature until the age of 100.

Participating Insurance: This is a type of insurance policy that entitles the policy holder to share in the divisible surplus of the insurer through dividends.

Permanent Life Insurance: This is any plan of life insurance that’s designed to last throughout the life of the insured. Level premium, cash value, and non-forfeiture options characterize permanent life insurance.

Policy Proceeds: This refers to the amount that’s paid as a death, surrender, or maturity benefit. In the case of a death benefit, it includes the face value, plus any earned dividends, minus any outstanding loans and interest. If paid as a surrender benefit, the amount includes any cash value, minus surrender charges, outstanding loans, and interest. If the benefit is paid at maturity, the benefit includes the cash value, minus any outstanding loans and interest.

Policy Term: Typically expressed in years, this is the time for which a policy remains in existence.

Renewable Term Life Insurance: This is temporary life insurance that may be renewed at the end of the policy term without evidence of insurability. The premium is based on the attained age of the insured and, as such, increases at each renewal.

Single-Premium Insurance: This form of insurance involves the payment of one premium that’s large enough to cover the cost of a life or annuity contract for life. This is also referred to as a lump-sum premium.

Straight Life Insurance: This is a type of whole life insurance that provides coverage for the entire life of the insured and for which the premiums are payable until death. This is also referred to as continuous premium life.

Stock Insurance Company: This is an insurance company that’s owned and controlled by its stockholders who share in its divisible surplus. Generally, stock insurance companies issue non-participating life insurance; however, some also issue participating life insurance policies.

Target Premium: This represents the suggested premium that’s used in universal life insurance policies; however, there’s no guarantee that there will be adequate funds to maintain the policy. Instead, it may indicate what will be needed (under conservative estimates) to maintain the policy. The validity of a target premium is based on an individual insurance company’s marketing stance, investment performance, and cost control.

Term Life Insurance: This is temporary life insurance that’s generally designed to afford coverage for a limited number of years. The policy includes no cash value and can be described as pure protection.

Universal Life Insurance: This is adjustable life insurance under which premiums and coverage are adjustable. For a universal policy, company expenses are not explicitly disclosed to the insured, but a financial report is provided to policy holders annually.

Variable Life Insurance: This is life insurance whose face value or duration varies depending on the value of underlying securities.

Variable Universal Life Insurance: This form of insurance combines the flexible premium features of universal life with the component of variable life in which excess credited to the cash value of the account depends on investment results of separate accounts. The policy holder selects the accounts into which the premium payments are to be made.

Whole Life Insurance: This is the form of life insurance that may be kept in force for a person’s entire life, and that pays a benefit upon the person’s death.

INTRODUCTION

This chapter will introduce the general concepts of life insurance policy contracts and the various types of life insurance products. Determining the best type of life insurance for a person depends on (among several other factors) how long the person wants the policy to last and how much he wants to pay. This chapter will examine the various types of life insurance policies that are available, their benefits, and how each policy is funded.

The chapter is broken into the following sections:

General Concepts of Life Insurance

Temporary Life Insurance Products

Permanent Life Insurance Products

Alternative Non-Traditional Life Insurance Products

Securities and Exchange Commission (SEC) Regulated Life Insurance Policies

Special Use Life Insurance Products

Other Life Insurance Products

The state-specific portion of this course (located at the end) will detail the specific insurance definitions, rules, regulations, and statutes for your state. In the event of a conflict, state law will supersede the general content.

Review of this chapter will enable a person to:

Understand the general concepts that are used in life insurance contracts

Become familiar with life insurance policies

Identify the different types of term life insurance

Identify the advantages and disadvantages of term life insurance

Understand the general concepts of whole life insurance

Identify the features of whole life insurance

Identify the different types of whole life insurance policies

Become familiar with the types of non-traditional whole life insurance policies

Distinguish between low premium type and high premium type

Understand the concept of modified endowment contracts

Identify and distinguish between the different types of special-use life insurance products

Distinguish between family plan policies and family income policies

Distinguish between joint life policies and joint life and survivor policies

Identify the most notable non-traditional life insurance products

Identify universal life death benefit options

Distinguish between participating versus non-participating policies

GENERAL CONCEPTS OF LIFE INSURANCE

For more than a century, life insurance has been recognized as an essential element in an individual’s or family’s financial planning program. Life insurance involves the transfer of the risk of premature death from one party (i.e., the policy owner/insured) to another party (i.e., the insurer). When a life insurance contract is payable upon the death of the insured, it instantly creates funds for a named beneficiary. In other words, a life insurance contract creates an immediate estate.

Unlike other lines of insurance (e.g., property and casualty), there are no “standard life insurance policies.” Today’s life insurance policies are typically defined by the benefit options available, the intended length of coverage, and how the policy benefits will be paid for or funded. Broadly speaking, all life insurance policies fall into the following categories:

Permanent (whole life or ordinary) or temporary (term life)

Group or individual

Fixed or variable

Industrial, Burial, or Debt insurance

A life insurance company may choose to specialize in any of these types, or just specialize in one or two. These basic coverage types are distinguished by the type of customers, amounts of insurance written, underwriting standards, and marketing practices. Group life insurance will be described later in the course.

TEMPORARY LIFE INSURANCE PRODUCTS

TERM LIFE INSURANCE

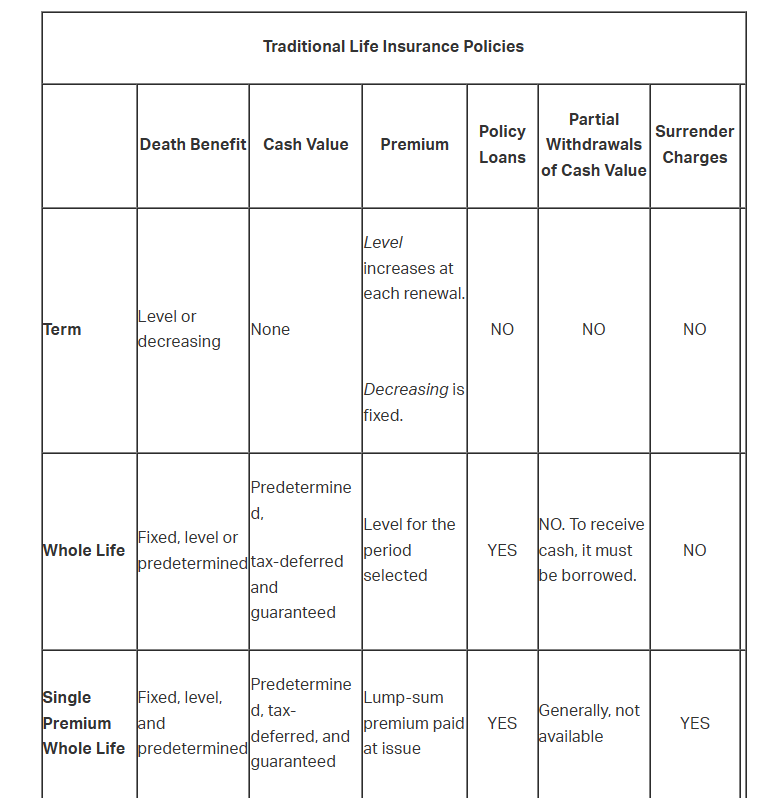

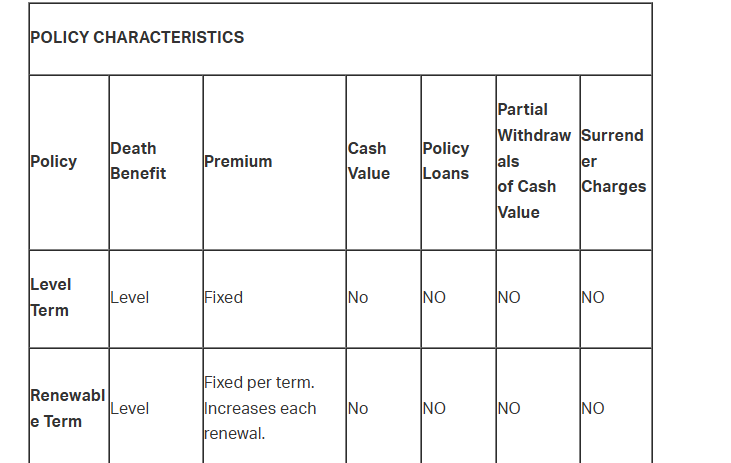

Term life insurance provides pure or temporary protection and is the simplest form of life insurance coverage; essentially, it provides the maximum amount of life insurance at the lowest initial outlay of funds. Term life provides low-cost insurance protection for a specified, limited period and pays a benefit only if the insured dies during that period. Term life is often referred to as temporary life insurance since it provides protection for a temporary period. The period (or TERM) for which these policies are issued can be defined by years (e.g., one-year term, five-year term, or 20-year term) or age (e.g., term to age 65, term to age 70). Term policies that are issued for a specified number of years provide coverage from their issue date until the end of the years specified. Term policies that are issued until a certain age provide coverage from their date of issue until the insured reaches the specified age. Term insurance provides the insured with peace of mind against the financial loss that an early death may cause. However, if the insured survives, there’s no loss and therefore no benefits are paid.

For example, Steve purchases a 20-year $75,000 level term policy on his life and names his sister, Amy, as the beneficiary. If Steve dies at any time within the policy’s 20-year period, Amy will receive the $75,000 death benefit. If Steve lives beyond that period, the policy expires, and nothing is payable to either Steve or Amy. Additionally, if Steve cancels or lapses the policy during the 20-year term, nothing is payable.

Term life policies are able to offer fixed, or constant, level premiums because the premiums are averaged over the term of the policy. Term life insurance provides the greatest amount of death benefit per dollar of initial cash outlay.

The primary advantage of term life insurance is that the premium or cost of the policy is substantially lower than the premium or cost of a permanent, whole life insurance policy that’s issued for the same face value amount. However, unlike permanent (whole) life insurance, term life insurance policies don’t build cash value.

An insurer may offer a selection of several different types of term life insurance policies. The various types of term life insurance policies that are available are primarily distinguished by the characteristics of their face value (death benefit). Basic types of term life insurance policies include level term insurance, decreasing term insurance, and increasing term insurance.

LEVEL TERM LIFE INSURANCE

The most common form of term life insurance—level term life insurance—provides a constant or fixed amount of coverage for as long as the policy remains in force. This form is characterized by a level face amount (death benefit) for a specified period. A level term policy expires at the end of the policy period. Remember, the “level” part of the name is really referring to the death benefit. The premium payments are fixed (or level) for the term of the policy as a standard characteristic of term insurance.

For example, a 10-year level term policy with a $100,000 face value provides a flat, level $100,000 of coverage protection for a period of 10 years. If the insured dies at any point within those 10 years, the insured’s beneficiaries will receive the policy’s $100,000 death benefit (or face value). If the insured lives beyond the 10-year term, the life insurance policy will expire, and no benefits will be paid.

A term to age 65 life insurance policy with a face value (or death benefit) of $250,000 provides a level $250,000 of coverage until the insured reaches the age of 65. If the insured dies at any point before age 65, the insured’s beneficiaries will receive the policy’s $250,000 death benefit (or face value). If the insured lives beyond age 65, the life insurance policy will expire, and no benefits will be paid.

[EXAM TIP: Assume an exam question is referring to a level term life insurance policy if the question doesn’t specify the type of term policy and simply indicates, “a term policy.”]

INCREASING TERM LIFE INSURANCE

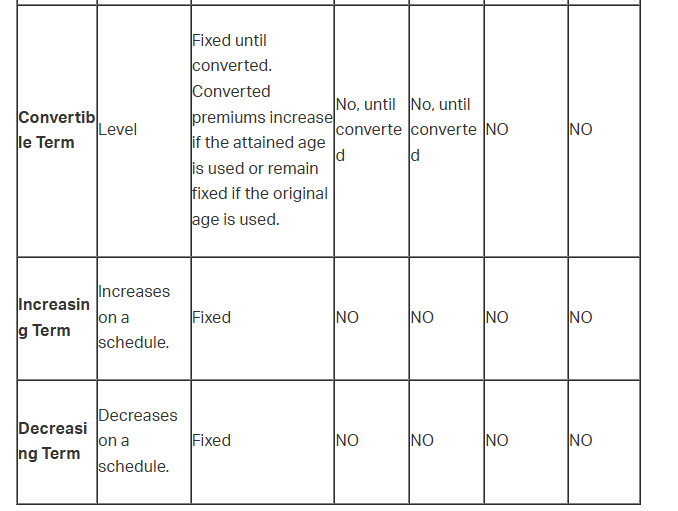

Increasing term life insurance is term life insurance that provides a death benefit which increases at periodic intervals over the policy’s term. The amount of the increase is typically stated as specific amounts or as a percentage of the original amount. The amount may also be tied to a cost-of-living index, such as the Consumer Price Index (CPI). Increasing term insurance may be sold as a separate policy but is generally purchased as part of a package or cost of living rider attached to a policy. Increasing term life insurance is often used to account for anticipated income growth as individuals advance in their careers. Increasing term life insurance may also be referred to as incremental term life insurance.

For example, a 30-year-old physician may choose to take out a term to age 65 life insurance policy with a $100,000 face value that increases by $100,000 every five years to account for growth in his income. This will allow for a maximum of six, $100,000 increases throughout the life of the policy. The face value or death benefit of the insurance policy would increase to $200,000 at age 35, $300,000 at age 40, $400,000 at age 45, $500,000 at age 50, $600,000 at age 55, and $700,000 at age 60.

If the physician dies before the age of 65, the life insurance policy will pay the insured’s beneficiaries the face amount associated with the insured’s current (attained) age. At age 65, if the physician has not yet died, the policy will terminate, and no death benefit will be paid.

DECREASING TERM LIFE INSURANCE

Decreasing term life insurance policies are characterized by benefit amounts that decrease gradually over the term of protection and have level premiums. Decreasing term life insurance is commonly used to pay off the insured’s debt in the event of her death.

For example, a 20-year $50,000 decreasing term policy will pay a death benefit of $50,000 at the beginning of the policy term. That amount gradually declines over the 20-year term and reaches $0 at the end of the term.

Mortgage Redemption Insurance

Mortgage Redemption Insurance is a type of decreasing term life insurance policy, and its purpose is to provide policy holders with a way to have their mortgages paid off if they die before they’re fully paid. Mortgage protection prevents the full burden of paying the mortgage from falling on the shoulders of the surviving family members. With this design, the face value decreases as the balance remaining on the mortgage decreases.

Credit Life Insurance

Credit Life Insurance is a limited benefit (term) policy that’s designed to cover the life of a debtor and pay the amount due on a loan if the debtor dies before the loan is repaid. The beneficiary of this type of policy is typically the lender. The type of insurance used is decreasing term, with the term matched to the length of the loan period (which is generally limited to 10 years or less) and the decreasing insurance amount matched to the outstanding loan balance. Credit life may be issued to individuals as single policies; however, most often, it’s sold to a bank or other lending institution as group insurance that covers all of the institution’s borrowers. The cost of group credit life (or actually any credit life) insurance is typically paid entirely by the borrower.

The maximum benefit for a credit life insurance policy (regardless of individual or group) is the value of the loan. The lender only has an insurable interest in the insured up to the value of the indebtedness. The life insurance policy is not a legal contract if it allows the lender to profit from the death of a debtor.

While credit life or mortgage insurance may be required as a condition of a loan, the creditor cannot require the borrower to purchase the insurance from the organization that’s granting the loan or another specific organization. A lender that requires a borrower to purchase insurance from a specific company as a condition of providing a loan is considered coercion, which is an illegal practice.

CONVERTIBLE TERM LIFE INSURANCE

By definition, term insurance is designed to terminate after a specified period; however, some term policies may contain an option which allows the policy owner to convert the temporary protection to permanent protection. The option to convert must be included in the contract when the policy is purchased and, depending on the insurance company, may specify a time limit for converting (e.g., three years prior to policy expiration) or an age limit for converting (e.g., before the insured reaches the age of 55). Policies that contain the option to convert are named accordingly and are easy to identify.

For example, a term policy that provides life insurance protection for 15 years and also has a conversion privilege is referred to as a 15-year convertible term policy.

The option to convert gives the insured the privilege to convert or exchange the term policy for a whole life (or permanent) policy without evidence of insurability. In other words, the insured is not required to pass a medical exam or demonstrate good health since that requirement was already satisfied before the policy was initially issued.

For example, let’s assume that Steve purchased a 15-year term policy and suffers a massive heart attack 10 years into the policy term. Steve’s heart attack negatively impacts his insurability and due to his increased health risk, it’s unlikely that an insurance company will allow him to purchase a life insurance policy. When his 15-year policy expires, he will be without life insurance and possibly unable to obtain life insurance due to his increased risk. If Steve purchased a 15-year convertible term policy, he would have the option to convert the policy to permanent protection without the need to prove insurability.

Depending on the conversion method, the premium rate for the new whole life policy will reflect the insured’s age at either the time of the conversion (the attained age method) or at the time when the original term policy was taken out (the original age method). The cost of insurance is the most important factor to consider when determining whether to convert term life insurance at the insured’s original age or the insured’s attained age. The method that insurance companies use to develop the premium amount will be examined later in the course, but one of the most significant impacts of the cost of insurance is the insured’s age. The older the insured, the more likely he is to die, and as such, the higher risk he poses to the insurer. While it may seem obvious for the insured to use his original age for conversion, the decision is typically made by the insurance company and is outlined in the provisions of the original term life insurance policy.

When the attained age is used, the policy owner is effectively terminating the pure, term insurance protection and purchasing a new whole life insurance policy without providing any health history information. As described, the insured’s age is one of the largest premium factors, and as such, this method results in higher premiums. Despite this, most conversions are accomplished in this manner.

When the original age is used, the insurer will determine what the appropriate premium would have been had the owner purchased a whole life policy at the “original age” when life insurance was initially purchased. Premiums will be lower using the original age than the attained age. However, if this method is selected, the owner must fund or deposit an amount equal to the difference between what he would have spent on the policy had he started with whole life and what he actually spent on term life the policy so far, plus interest. This deposit guarantees lower premiums and also results in higher cash values. The premium and cash value deposit characterizes the retroactive conversion that exists if this method is selected.

[EXAM TIP: Assume an exam question is referring to the attained age method if the question doesn’t specify the method of conversion.]

Interim Term Life Insurance

Interim term life insurance is a type of convertible term insurance that’s written on a person who wants protection immediately, but who’s not able to afford permanent protection immediately. It provides interim coverage between now with the eventual conversion to permanent protection.

Interim term life insurance is typically written to automatically convert to permanent protection at some point within the first year. While insurability is guaranteed, the premium for the temporary protection is based on the original application age. Whereas the premium for permanent protection is based on the age at the time permanent protection begins (the attained age).

RENEWABLE TERM LIFE INSURANCE

Some term life insurance policies may contain an option which allows the policy owner to renew the term policy before its expiration date without being required to provide evidence of insurability. As with the option to convert, the option to renew must be included in the contract at the time the policy is purchased; it cannot be added later. Term life insurance policies are renewed using the insured’s attained age. The premiums for each renewal period will be higher than the initial period, reflecting the insured’s increased age and increased risk. This steady increase in premium is often referred to as a step-up premium (since the insured climbs up another “step” when he renews the policy). The advantage of the renewal option is that it allows the insured to continue insurance protection, even if he has become uninsurable due to a change in health. However, as the premiums increase each renewal, the cost of the policy typically becomes cost-prohibitive, forcing those who are older, and more likely to need the protection, to terminate or not renew the coverage.

Renewal options typically provide for several renewal periods or for renewals until a specified age. The renewal privilege often expires by the time the insured reaches the age of 65. The option to convert and the option to renew may be combined into a single term policy.

For example, a $25,000, 10-year renewable, and convertible to age 65 term life insurance policy provides a death benefit (face value) of $25,000 for 10 years. Additionally, it allows the policy owner the privilege of renewing the policy every 10 years until the insured reaches the age of 65. Furthermore, the policy allows the policy owner the privilege of converting the temporary, term insurance to permanent, whole life protection, as long as that conversion happens before the insured reaches the age of 65. The insured is not required to prove insurability if he exercises his privilege to renew or convert. However, the premium will definitely increase each time either of those options is exercised.

Annually/Yearly Renewable Term (A/YRT) Life Insurance

Annually renewable term (ART) or yearly renewable term (YRT) life insurance provides coverage for one year and allows the policy owner to renew coverage each year, without evidence of insurability. Annually renewable term and yearly renewable term life insurance represent the most basic form of life insurance. This renewal is typically automatic and renews with an increased premium cost each renewal period. This type of term life insurance policy provides an insured with two sets of premium rates—a current or scheduled premium (based on the insurer’s current cost of insurance) and a guaranteed maximum premium (based on the maximum the insurer agrees to increase the cost of insurance). For this reason, the premium is said to be a non-guaranteed level.

Re-Entry Term Insurance

Some term life insurance policies include a re-entry feature, which states that the premium can change at renewal based on insurability. The insured has the option of taking the standard renewal rate without proving insurability. However, to maintain the lowest premium rate (or a discount from standard), the insured may be required to prove insurability again upon renewal. If there’s an insurability problem (i.e., the insured fails the medical exam), coverage may be maintained but at a higher premium rate. Re-entry term life insurance is also referred to as revertible term life insurance.

[EXAM TIP: If an exam question references renewing a life insurance policy, the new premium will ALWAYS be higher than the previous or original premium. The cost of insurance will never stay the same or decrease. Additionally, only temporary coverage can be renewed. There’s no need to renew permanent coverage.]

USES OF TERM INSURANCE

Although temporary life insurance protection may not seem ideal at first, it’s essential to note that there’s no such thing as “bad life insurance.” However, every type of insurance is uniquely designed to fill a specific purpose or goal. For term insurance, that goal is typically to provide temporary financial protection in case the insured dies too soon. As with any other type of insurance, there are many uses, advantages, and disadvantages of term life insurance.

Advantages of term life insurance policies include:

Term life insurance is less expensive than permanent insurance.

Term life insurance may protect the insured’s insurability if the policy is renewable and/or convertible.

Term life insurance may be used in conjunction with debts, mortgages, or as a supplement to whole life insurance.

Term life insurance provides the most substantial amount of protection for the lowest cost.

Disadvantages of term life insurance include:

The protection provided by term life insurance policies terminates with the policy terminates. No protection is in effect once the term protection ends.

If the term life insurance policy is renewable or convertible, premium rates rise as the insured ages. This premium increase often leads to policy cancellation prior to the policy terminating.

Due to the temporary nature of term insurance, few death claims are actually paid under term life insurance policies.

Term life insurance policies don’t contain any cash savings or equity elements (i.e., cash value). Since it has no cash value, it doesn’t mature like a whole life policy.

PERMANENT LIFE INSURANCE PRODUCTS

GENERAL CONCEPTS OF WHOLE LIFE INSURANCE

Whole life insurance provides for the payment of a death benefit or face amount of coverage upon the death of the insured, regardless of when the death occurs. This type of policy will provide permanent protection for the insured’s entire (whole) lifetime, from the date of issue to the date of the insured’s death. Whole life policies may also be referred to as straight life, continuous premium life, permanent life, or ordinary life insurance.

A whole life policy is generally described as a fixed death benefit, fixed premium life insurance contract. In other words, it’s characterized by a level death benefit, a cash savings value (i.e., equity build-up), permanent protection, and a fixed, level, or predetermined premium. The death benefit, premium payment, and the interest rate paid on the cash value are all predetermined for the insured’s “whole life.” Also, a whole life policy protects an insured permanently for the remainder of her life. This form of life insurance policy never needs to be converted or renewed, since it remains in force for as long as all premiums are paid in a timely fashion.

FEATURES OF WHOLE LIFE INSURANCE

Generally speaking, there are certain features that are shared by all types of whole life insurance. A traditional whole life insurance policy combines pure death protection with a cash value feature. Additionally, the death benefit (face amount) of the policy remains constant or level throughout the life of the insurance policy. Premiums are set at the time of policy issuance, and they too remain fixed for the policy’s life. Whole life policies are based on the assumption that premiums will be paid by the policy owner throughout the insured’s lifetime or to age 100, whichever occurs first. This means that the whole life policies are designed to “mature” or “endow” at age 100. “Mature” or “endow” means that the cash value accumulations are equal to the face amount. The cash value and endowment (or maturity) are the main features which distinguish whole life insurance from term life insurance and combine to produce additional living benefits for the policy owner.

[EXAM TIP: While term life is designed to provide temporary protection IF the insured dies too soon, whole life insurance is designed to provide permanent protection WHEN the insured dies.]

Cash Values

Unlike term insurance, which only provides death protection, permanent life insurance combines insurance protection with a savings element. This savings accumulation is commonly referred to as the policy’s cash value and builds over the life of the policy. Although it’s an essential part of funding the policy, the cash value is often regarded as a savings element because it represents the amount of money the policy owner will receive if the policy is ever surrendered or voluntarily terminated.

When a policy owner pays the premium for a whole life insurance policy, a portion of that premium is used to pay for the death benefit. This portion of the premium is referred to as the “term” insurance cost or cost of insurance.

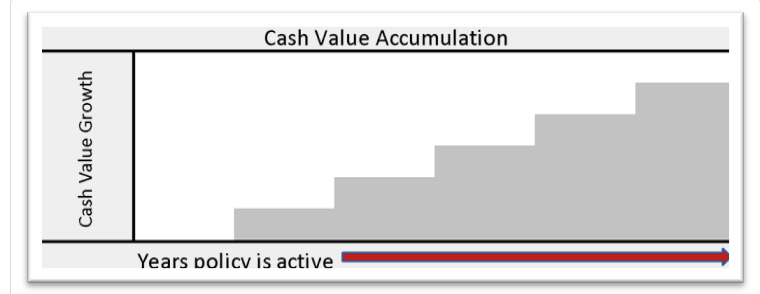

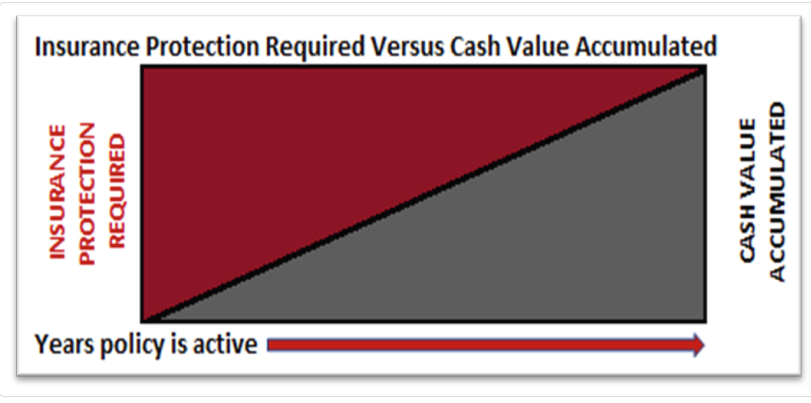

Another portion of the premium is used to cover the costs associated with the insurance company that issued the policy, commissioners, underwriting, medical exams, etc. and the costs of maintaining the policy. After the contract has been in effect for an initial period, the insurer begins depositing a portion of the premium into the policy’s cash value. Some states may have specific requirements as to when the accumulation begins. Still, in most traditional whole life policies, the cash savings value begins to build within two to three years after the policy is issued. Once cash value begins to accumulate, this savings account or “equity’ increases with each subsequent premium payment and continues to build during the life of the contract. The cash value accumulates from the premiums paid plus a guaranteed fixed interest rate. This interest is added to the savings account and allows the cash value to grow exponentially each policy year.

In the policy’s early years, more of the premium money paid goes towards providing the actual insurance protection, but as the cash value grows larger and begins to offset the death benefit, the funds needed to purchase the actual insurance protection decreases. With less money being used for actual insurance protection, more of the premium can go toward growing the cash value during the later policy years. Whole life insurance policies were traditionally designed so that their cash value buildup would equal the policy’s face amount by the time the insured reaches the age of 100. Therefore, if a person purchases a whole life policy today and lives to age 100, she will receive all of her premiums back plus some interest. The premiums paid plus interest equal the total cash value at age 100, which also matches the policy’s face value or death benefit.

Cash Values

Over the past few decades, the mortality tables that are used to determine premiums and maturity have been modified by many insurers. Although some continue to base maturity on the age of 100, many are using age 115, up to age 121.

It’s important to understand that, traditionally, the cash value buildup is not paid to a beneficiary in addition to the death benefit when the insured dies. The policy’s cash value is available to the policy owner at any time. The policy owner may surrender the policy, thereby canceling coverage and receive the amount of the cash value. This is why the cash value is also referred to as the cash surrender value or non-forfeiture value. In other words, it’s the dollar amount that the policy owner will receive if she chooses to surrender or forfeit the life insurance policy. The cash value accumulation also provides the policy owner with the opportunity to borrow some of the policy’s equity funds to borrow against while keeping the policy in force. The borrowing of a policy’s cash value is considered a loan and, as such, interest is charged for it.

For example, let’s assume that John purchased a $100,000 whole life policy at 30 years old, which costs $1,000/year. It will likely take about three years for the policy to begin to build cash value. As with all whole life policies, the cash value equals the face value (in this case, $100,000) at age 100. For this example, let’s say the policy’s cash value is scheduled to be $15,000 after 10 years and $50,000 after 35 years. During the initial three-year period, the insurance company needs to provide the full $100,000 of protection. After John has made payments for 10 years (and did not take out any policy loans), the cash value now equals $15,000. The insurance company can use this $15,000 to offset the death benefit, meaning they only need to worry about providing $85,000 of protection. After the policy has been in force for 35 years (provided John did not take out any policy loans against his cash value), the cash value now equals $50,000. In turn, the insurance company only needs to worry about providing $50,000 worth of protection. Again, this means more of John’s premium can be diverted to growing the cash value. Once John reaches the age of 100, the policy endows or matures, the insurance company no longer needs to worry about providing any protection. At this point, John’s protection ends, and the insurance company will issue John (or the policy owner) a check for $100,000.

The amount of a policy’s cash value depends on a variety of factors, including:

The face amount of the policy; the higher the face amount of the policy, the larger the cash values.

The duration and amount of the premium payments; the shorter the premium-payment period, the quicker the cash values grow. The higher the premium amount paid by the policy owner, the quicker the cash values grow.

The length of time that the policy has been in force; the longer the policy has been in force, the faster the build-up in cash values.

[EXAM TIP: There’s a specific “return of cash value” benefit rider that can be added to a whole life policy. If an exam question doesn’t explicitly mention an insurance policy having a return of cash value rider or endorsement, it should be assumed that the policy in question doesn’t include that rider.]

Maturity at Age 100

Whole life insurance was originally designed to mature at the age of 100. From an actuarial standpoint, it’s assumed that every insured will be deceased by the time they would have reached the age of 100. Although some individuals live beyond the age of 100, the number of individuals who do live that long is not a statistically significant portion of the population.

Consequently, the premium rate for whole life insurance is based on the assumption that the policy owner (usually the insured) will be paying premiums for the insured’s whole life. As previously described, the policy is designed in such a way that when the insured attains the age of 100, the cash value of the policy has accumulated to the point that it equals the face amount of the policy.

At that point, the policy has matured or endowed, and no more premiums are owed. In turn, the insurance company will issue a check for the full face value of the policy, minus any policy loans that have not been repaid. Practically speaking, very few individuals live to the age of 100. In fact, it’s far more likely that a whole life policy will be cashed in for its surrender value or that its face amount will be paid out as a death benefit before the policy matures.

Whole Life Insurance Premiums

As noted earlier, whole life is designed with the belief that the insured will live to the age of 100. Accordingly, the amount of premium for a whole life policy is calculated, in part, based on the number of years between the insured’s age at issue and the age of 100. The shorter the payment period, the higher the premium. This span of years represents the full premium-paying period, with the amount of the premium spread equally over that period. This is referred to as the level premium approach. As is also the case with level premium term insurance, the level premium whole life approach allows whole life insurance premiums to remain level rather than increase each year with the insured’s age.

Whole life premiums are referred to as “bundled premiums.” Bundled premiums mean that the insurer is not required to explain to the policy owner how the premium paid is ultimately distributed (i.e., for death protection, commissions, and other expenses). Premium rates are based on a dollar amount per $1,000 of coverage and are typically expressed annually.

For example, an insurance producer may explain to a potential applicant that the whole life insurance policy costs $9 per $1,000 of coverage. If the applicant wants a policy with a $100,000 face value, the cost will be $900 per year ($9 x 100).

BASIC FORMS OF WHOLE LIFE INSURANCE

Remember, whole life insurance provides a fixed, level death benefit or permanent protection with a cash savings feature. It’s characterized by a fixed, level, or predetermined premium for life (or up to the age of 100).

The policy’s cash value increases with every premium payment, and a fixed interest rate is paid on the cash value that’s also fixed for the life of the policy. Therefore, the cash value buildup of a whole life policy equals the face amount at age 100. The contract also includes non-forfeiture options or values in the event the policy owner wants to surrender the policy.

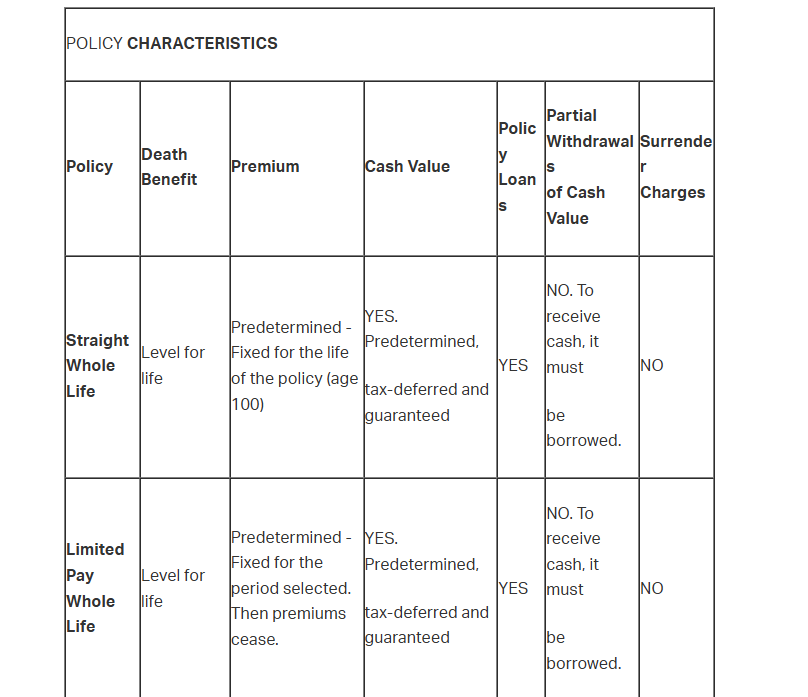

Although it’s been presented that whole life premiums are calculated as if they were payable to the age of 100, they don’t necessarily need to be paid this way. There are actually several different whole life insurance policy types to accommodate different premium-paying periods. The three most common types of whole life insurance are straight whole life, limited pay whole life, and single premium whole life.

Straight Whole Life Insurance Policies

The most basic form of whole life insurance is straight whole life, which may also be referred to as ordinary whole life insurance. Straight whole life insurance is basically the standard definition of whole life as has been described up to this point.

It’s whole life insurance that provides permanent level protection with level premiums from the time the policy is issued until the insured’s death (or age 100). This continuous premium or whole life plan is characterized by level or fixed premiums as long as the contract remains in force.

[EXAM TIP: Unless explicitly specified otherwise, it should be assumed that any exam reference to whole life insurance is referring to straight, whole life insurance.]

Limited Pay Whole Life Insurance Policies

The advantage of this type of whole life insurance policy is to permit the policy owner to cease paying premiums after the limited payment period. At this point, the policy is entirely paid-up for life and no future premiums are required. However, as with a straight life plan, the policy is designed to mature or “endow” at the age of 100. A limited payment whole life policy is characterized by a predetermined, level premium for a limited payment period. There are several types of limited payment policies in existence, such as 10-pay life, 20-pay life, 30-pay life, and life paid-up at the insured’s age 65.

For example, a 20-pay life policy is a whole life insurance policy in which premiums are payable for 20 years from the policy’s inception, after which no more premiums are owed. A life paid-up at 65 policy is a whole life policy in which the premiums are payable to the insured’s age 65, after which no more premiums are owed.

Premiums paid for these policies are initially higher than a straight life policy since they’re only paid for a limited period (i.e., 10 years rather than to the age of 100). Once the payments are finished, the policy is paid-up for life, which means that no additional premiums are due. Whenever the insured dies, the death benefit will be paid to the designated beneficiary. Although the policy is paid-up earlier than a traditional straight whole life policy, it will still not “mature” until age 100 since the contract has been predetermined. Since the initial premiums for these policies are higher than a traditional straight whole life policy, it’s often said that they possess a more substantial savings element or a greater emphasis on savings than the traditional straight whole life contracts.

Since the insurance company is receiving their money in larger premium payments, the cash value builds quicker in a limited pay policy than in a straight life policy. Additionally, cash values build up even faster during the premium paying years than during the non-premium paying years. After the premium paying period, the cash values continue to grow, but more slowly, until the policy matures and the cash value equals the face amount, again, at the age of 100.

It’s important to remember that, despite the fact that the premium payments are limited to a certain period (as with all other types of whole life insurance), the insurance protection is in force until the insured’s death, or to the age of 100.

[EXAM TIP: A limited pay life insurance policy will best suit a prospective insured who’s seeking permanent insurance but doesn’t want to pay premiums indefinitely.]

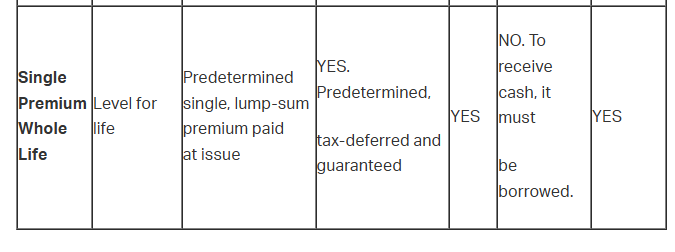

Single Premium Whole Life Insurance Policies

ingle premium whole life insurance is the extreme form of a limited payment policy and is characterized by a lump-sum or single premium payment. Therefore, the policy is fully paid-up upon the payment of a lump-sum premium. Some single premium plans are in existence, which consists of two premium payments, such as a “dual premium” policy. Single premium plans may possess tax advantages and the ability to borrow against the cash value at below-market interest rates.

A single premium whole policy is the most expensive whole life policy initially. The higher up-front cost should be evident due to its single lump-sum premium. However, when compared to a straight life policy over the life of the contract, the single premium life is the least expensive.

For example, let’s assume that an insured is 30 years of age and purchases a $10,000 traditional straight whole life policy with an annual premium of $120. If the insured lives for 40 years, he will have paid $4,800 in traditional straight whole life premiums ($120 per year x 40 years). For a single premium life policy of the same face amount, the lump-sum single premium may only be $3,800.

Therefore, in most cases, during the life of the policy, straight whole life policies are more expensive than the single premium life plan. However, again, the single premium policy requires a significant initial premium, typically making it cost-prohibitive for most people.

Common traits of a single premium whole life policy include:

An immediate non-forfeiture value (cash value) is created.

A large part of the premium is used to set up the policy’s reserve.

The advantage offered by a single premium policy is that the policy owner will pay less for the policy than if the premiums were stretched over several years.

NON-TRADITIONAL WHOLE LIFE INSURANCE

Again, additional types of whole life plans alter the method by which premiums are paid. The premium charged for these plans is less than that for a straight life insurance policy in the first few years of the policy. Cash values also accumulate with each premium payment. Insureds who need permanent protection but cannot afford the higher traditional whole life premiums required, will buy this type of policy.

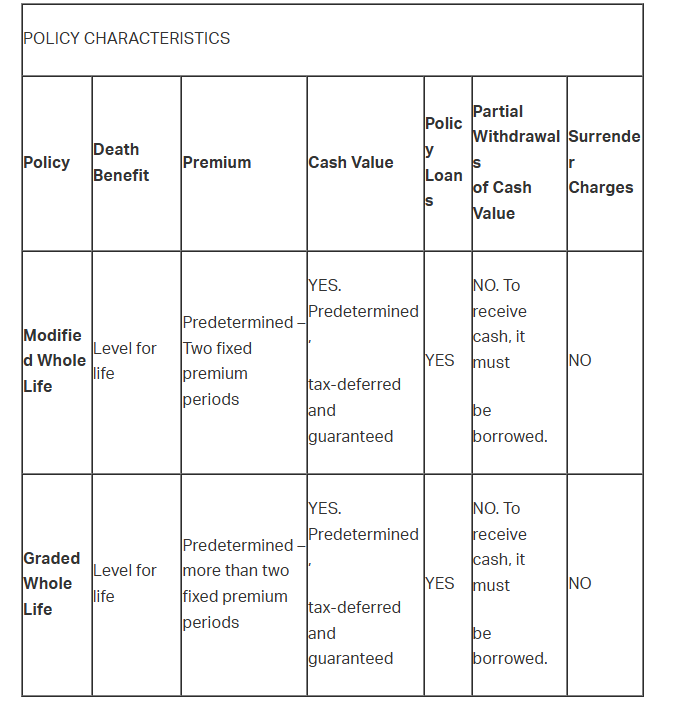

Modified Whole Life Insurance Policies

Modified whole life insurance is a type of whole life insurance policy that’s characterized by an initial premium which is lower than straight whole life insurance for an introductory period. The policy owner will pay a lower initial premium, as compared to the straight life premium, for the first few years. After this time, the premium will increase to an amount that’s higher than what the initial straight whole life premium would have been.

Once the premium “jumps” following the initial period, it will remain level or constant for the life of the policy. Therefore, modified whole life premium is characterized by two fixed premiums —a lower initial premium for five years that increases in the sixth year to an amount higher than the traditional straight whole life premium would have been and then remains level for life.

Again, modified whole life insurance policies alter the method by which premiums are paid. The premium charged for these plans is less than that for a straight life insurance policy in the first few years of the policy. As with all other types of whole life insurance, the life insurance protection is in force until the insured’s death, or to the age of 100. Also, cash values accumulate with each subsequent premium payment.

The purpose of modified whole life policies is to make the initial purchase of permanent insurance more accessible and more attractive, especially for individuals who have limited financial resources, but also the promise of an improved financial position in the future. Any individuals who are seeking permanent protection but cannot afford the higher traditional straight whole life premiums required, will buy this type of policy.

Graded Premium Whole Life

A graded premium whole life plan is a contract that’s characterized, like modified life, by a lower premium than whole life in the early years of the contract. However, premiums increase annually or every year for the initial period. Thereafter, it jumps to an amount that’s higher than the whole life premium and remains fixed for life. The premiums for these policies are predetermined, but are not level in the traditional sense, as they would be in the traditional straight whole life or limited pay whole life plans.

Enhanced Whole Life Insurance (Economatic / Extraordinary Life)

An enhanced whole life insurance policy (also referred to as economatic life or extraordinary life) is a low premium based participating permanent insurance policy. The contract’s face amount is reduced each year. Any dividends that are paid are set aside and used to purchase either paid-up additions or one-year term insurance which is equal to the reduction of death coverage. This policy provides a guaranteed death benefit in the early years of the policy, even if dividends are insufficient to maintain level coverage.

Indeterminate Premium Whole Life Insurance

Indeterminate premium whole life insurance is a type of whole life policy that provides low initial premium costs for a specified period. After that period, the insurer may then increase premiums. The characteristics of and benefits provided by this policy are similar to other contracts. However, an indeterminate premium whole life policy allows for a change of premium due to a change in the investment income of the insurer. Therefore, future premium adjustments are based on the insurer’s investment performance, mortality experience, and expenses.

Premiums may be raised or lowered by the company, but they can never exceed the guaranteed maximum. Insurers adopted this innovative type of policy in an attempt to offer lower-cost life insurance. Today, term insurance may also be written with indeterminate premiums.

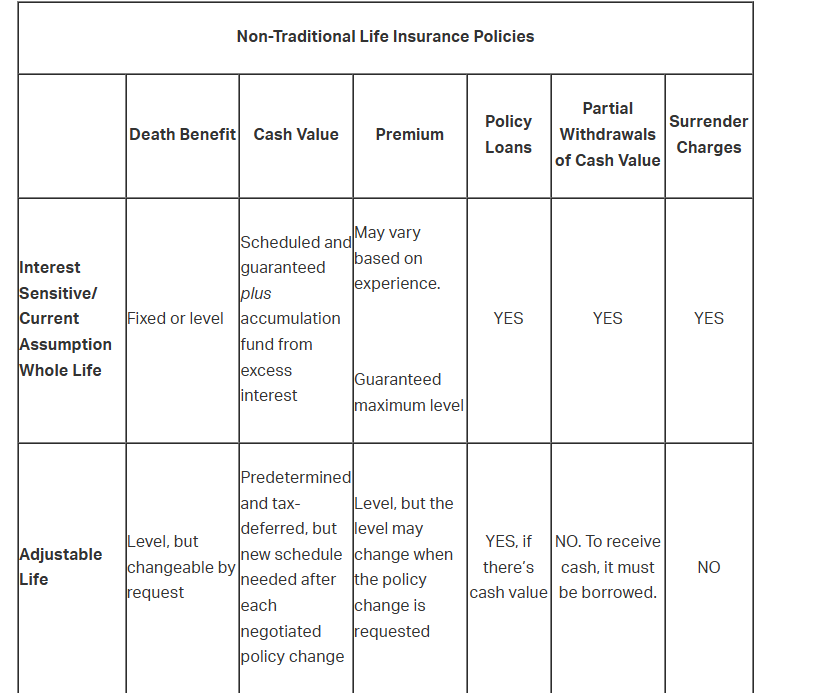

Current Assumption Whole Life (CAWL) / Interest Sensitive Whole Life

Current assumption whole life, also referred to as interest-sensitive whole life and excess interest whole life, is characterized by premiums that vary to reflect the insurer’s changing assumptions concerning its death, investment, and expense factors. However, interest-sensitive products also provide that the cash values may be higher than the guaranteed levels. If the company’s underlying death, investment, and expense assumptions are more favorable than expected, policy owners will have two options—lower premiums or higher cash values. Underlying assumptions could also turn out to be less favorable than anticipated, which would call for a higher premium than that at policy issue.

The policy owner may then either pay the higher premium or choose to reduce the policy’s face amount and continue to pay the same premium. An interest-sensitive life insurance policy owner may be able to withdraw the policy’s cash value interest-free. The provision that allows this is referred to as the partial surrender provision.

CAWL policies are either of the low premium or high premium variety. Both possess several characteristics, including but not limited to:

The use of an accumulation account which is made up of the premium, less expense and mortality charges, and credited with interest based on current rates

Minimum guaranteed cash value and rate of return

Maximum annual premium

Use of a surrender charge, fixed at issue, which is deducted from the accumulation account to derive the policy’s surrender value, and

Use of a fixed death benefit and maximum premium level at the time of issue

Low Premium Type - The low premium type includes an indeterminate premium that’s initially low. It also contains a redetermination provision, which states that after a specified period, the insurance company can refigure the premium.

High Premium Type - With the high premium type, the initial premium is relatively high. It possesses an optional pay-up provision which states that the policy owner may cease paying premiums once the policy’s values are sufficient to pay-up the contract.

Indexed Whole Life Insurance

This policy offers a face amount that increases along with rises in the Consumer Price Index (CPI). These policies are classified according to whether the policy owner or the insurer assumes the inflation risk. If the policy owner assumes the inflation risk, the death benefit increases each year in accordance with the CPI and the insurer will bill the policy owner each year for the new, higher amount of insurance. The insurer agrees not to require the insured to demonstrate insurability for any increase in protection as long as the policy owner accepts each year’s increase in the coverage amount.

If the insurer assumes the inflation risk, it’s similar to the previously mentioned approach, except that the premium being charged initially by the insurer is loaded in anticipation of future face amount increases. These increases in face amount don’t alter the premium level paid. These policies possess a cap as to the maximum total permitted.

Equity Index Whole Life Insurance

Another type of indexed life insurance product is equity indexed life insurance. This type of policy combines most of the features, benefits, and security of traditional life insurance with the potential of earned interest based on the upward movement of an equity index. Rather than the policy including a specific interest rate (as in a traditional whole life plan), interest earnings are credited based on increases in the specific equity index (e.g., the S&P 500 Index) to which the policy is linked. Therefore, credited interest is linked to an index without the downside risk connected with directly investing in the stock market. These policies are characterized by a guaranteed minimum interest rate, tax deferral of interest accumulations, and policy loan access. The equity index returns are designed to keep pace with or beat inflation, which protects the policy holder against downside market risk. Equity indexed life insurance contracts combine term life insurance with an investment feature, similar to a universal life plan (described later). Death benefit amounts are based on the coverage amount selected by the contract owner plus the account value.

ALTERNATIVE NON-TRADITIONAL LIFE INSURANCE PRODUCTS

Most whole life insurance policies are characterized by a fixed or level premium. As such, traditional whole life policies are referred to as level death benefit, level (or fixed) premium life insurance. During the 1970s, insurers developed a new type of policy that provided greater flexibility for the policy owner. These “non-traditional” policies are characterized by flexible coverage amounts and premiums. The following are other types of more modern and newer life insurance plans in existence that are characterized by a flexible, adjustable, or variable death benefit or premium. They function a bit differently than traditional whole life policies in several ways.

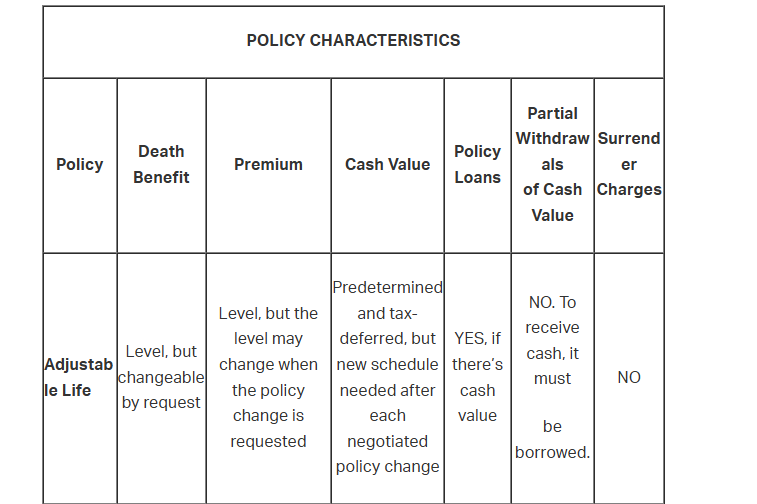

ADJUSTABLE LIFE

This type of permanent insurance product combines elements of traditional fixed premium whole life insurance with the potential to adjust the coverage or face amount based on the policy owner’s changing needs. The best description of adjustable life is Prentice-Hall, 1985:

“At any point in time, adjustable life is a level-premium, level-death benefit policy that may assume the form of any traditional type of life insurance.”

Characteristics

Adjustable life provides an adjustable death benefit and cash value, while also possessing all of the features of traditional whole life policies. Its distinguishing characteristic is a provision that’s referred to as the adjustment provision. The advantage of this policy is that it permits the policy owner to make prospective adjustments (i.e., in the future) to the policy’s coverage amount. The policy premium is fixed for the policy year if an adjustment in coverage is made (obviously, if more coverage is purchased, then the consumer pays more).

An individual whose income has been fluctuating during the past several years or a couple who plans to have children over the next several years are examples of prospective clients who may purchase an adjustable life policy so that they possess flexibility to satisfy their “changing needs.” Therefore, this is the type of life insurance policy that’s available to an individual who wants to have the opportunity to make changes or alterations to her contract each year.

There may be some confusion regarding premiums for adjustable life. Although the policy owner may pay more or less per year in the future than the original premium, the premium is adjustable. However, remember the original definition. At any point in time adjustable life insurance is a level-premium, level-death benefit policy. This means that whenever a coverage amount is increased, the premium that’s due is level for the upcoming policy year. If the policy owner decides to increase the coverage amount, the insured party must always prove insurability. To simplify, an adjustable life policy is a traditional whole life policy with an adjustable death benefit. This type of policy is characterized by prospective (i.e., future) adjustments only.

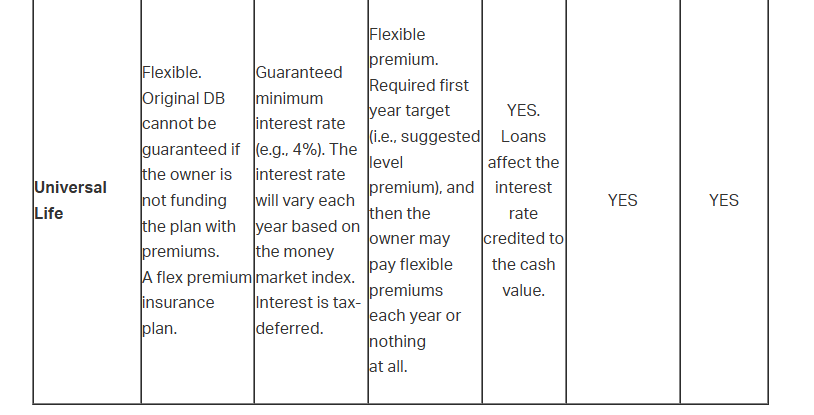

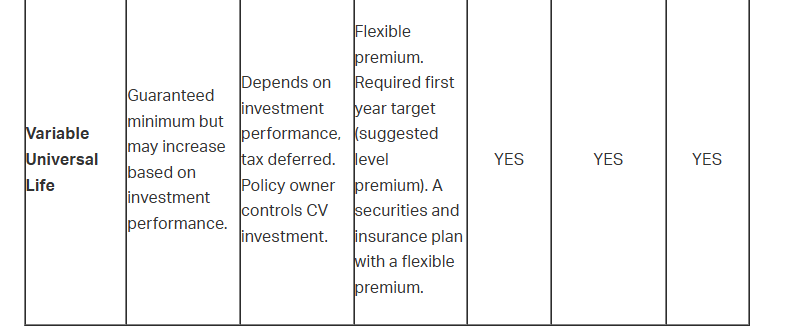

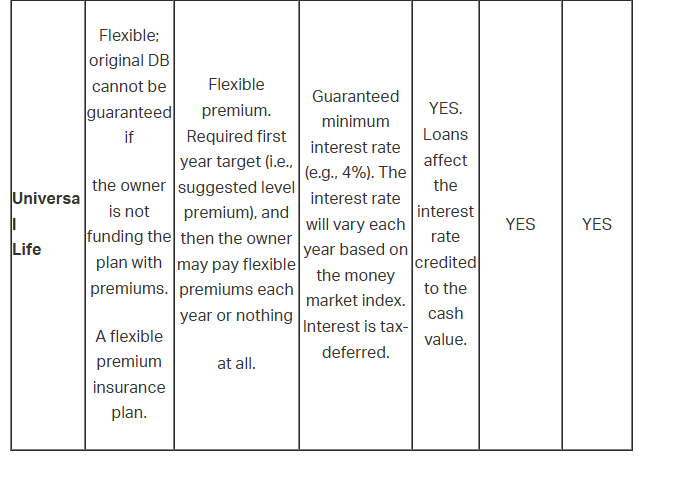

UNIVERSAL LIFE

As with adjustable life, universal life insurance provides its owner with more flexibility than a traditional whole life plan. It may be referred to as an adjustable form of life insurance since it allows the contract owner to change the coverage amount at his discretion. This type of policy may be characterized as an interest sensitive life product since it utilizes changing interest rates (or rate of return) to determine cash values. These changing interest rates are not used to determine death benefits or future premiums.

Universal life premiums pay for pure protection (i.e., term insurance), and a portion is deposited into its cash value. In this policy, the cash value may be referred to as: (1) a cash value fund; (2) a cash savings plan; (3) policy equity; or (4) a savings feature. As with traditional whole life policies, a fixed interest rate is paid on the cash savings plans as it accumulates. The minimum fixed interest rate paid on the cash value of a universal life contract is equal to the maximum paid (3% to 4%) on the cash value of most traditional whole life policies. This interest rate that’s paid on the cash savings plan will vary (i.e., interest sensitive) depending on market conditions and is responsible for the yearly increase in the cash savings.

Therefore, the interest rate is guaranteed for the policy year. If the contract owner pays a monthly premium, each month the insurer subtracts mortality charges and other applicable expenses from the cash savings plan. If the premium is paid annually, this deduction occurs once per year.

Most importantly, universal life is also characterized by a flexible premium. Therefore, the policy owner may pay whatever amount of premium she wants to pay each year. This flexibility could be a disadvantage for the owner of the policy if it’s not appropriately managed. For example, if premiums are not paid following the first year to keep coverage in force, the cost of death protection will be withdrawn from the cash savings plan. In this manner, the policy can pay for itself for as long as there are sufficient cash savings. If no additional premiums are paid, the policy uses the cash value to keep coverage in force. However, in the future, if there’s not enough cash to pay for death protection, the policy could lapse.

If only a small amount of cash value remains, the owner can use the cash available to purchase as much protection as the cash will buy. Therefore, in a universal life policy, the death benefit may not be guaranteed and, in some cases, may be dependent on the amount of cash value available (if the contract owner is not funding the policy by paying premiums).

When considering a universal life policy, a person must remember:

The death benefit may not be guaranteed (i.e., if not appropriately managed).

The interest rate paid on the cash value is guaranteed (i.e., for the policy year).

At times, the amount of coverage provided for the year will be dependent on the amount of cash value available.

Unique Characteristics of Universal Life

In a universal life insurance policy, the premiums, cash value, and the face amount can be adjusted. However, it’s neither identical to adjustable life nor is it backed by equities as in variable life products. Let’s closely examine the characteristics that make universal life insurance policies unique.

Unbundled Premium

Universal life policies are transparent since they’re characterized by unbundled or decoupled premiums. This means that the contract owner is provided with information describing where the policy costs are allocated. In other words, the contract owner receives a breakdown of premiums, death benefits, mortality charges, expenses, and cash values. This breakdown shows the contract owner the disposition of the policy funds.

Some insurers offer a target premium to allow contract owners to plan premium payments regularly. Since the premium is flexible, many contract owners who don’t manage the plan may see their coverage lapse. To avoid possible tax problems, premium allocations to a universal life policy’s cash value must comply with tax law (IRS) guidelines.

Cash Value

Funds that are withdrawn from the cash savings plan may not be subject to interest payments when they’re used to pay premiums. As premiums are paid, and as cash values accumulate, interest is credited to the contract’s equity. The interest credited may be a current rate based on current market conditions or on a guaranteed minimum rate that’s listed in the policy.

Fixed interest rates that are paid on the cash value traditionally include a guaranteed minimum of 2% to 4%; however, this will vary based on market conditions (although some have included rates as high as 7%, recently they’ve been in the lower single digits). Therefore, interest may be paid at either the contract’s guaranteed minimum rate or at the current interest rate as declared by the insurer. The fixed interest rate may change each year based on money instruments (i.e., Treasury bill rates, money-market rates, etc.).

Since the interest rate paid on the cash value changes each year and the amount of cash value changes, an annual statement must be provided to the contract owner each year by the insurer. This annual statement identifies the upcoming interest rate for the coming year, the cost of coverage, the current cash value amount, other applicable expenses, and additional relevant information. Also, contract owners may utilize a partial withdrawal from the cash value, unlike a traditional whole life policy, which requires the owner to borrow against the cash value (i.e., a loan) to access funds in the cash value.

Death Benefit

Universal life policies offer two death benefit patterns by including Option A and Option B. Under Option A (also referred to as Option One), a level death benefit is provided. The net amount at risk (NAR) is adjusted after each month. As such, a mortality charge is deducted from the policy’s cash savings plan monthly. Therefore, the cash value and NAR (benefit) together provide a fixed death benefit. Option B (also referred to as Option Two) provides an increasing death benefit as the cash value increases. As such, the death benefit equals the face amount plus the cash value at the time of death.

Tax Considerations

The amount of pure insurance protection above the cash value is often referred to as a corridor. In order for a contract to qualify as life insurance for tax purposes, there must be “space” between the total death benefit and the cash value of the policy. An automatic increase in the death benefit results when the cash value approaches the initial face amount under Option A.

Again, if this space is not present, the policy will lose its favorable tax treatment since it will not meet the Internal Revenue Code’s definition of life insurance. In addition, for cash value accumulations to receive favorable tax treatment (i.e., tax deferral), a specific percentage of universal life premiums must be used to purchase the death benefit amount.

Universal Life Riders

Waiver of Monthly Deduction Rider (Waiver of the Cost of Insurance)

Some insurers offer a “waiver of monthly deduction” rider to be added to a universal life policy. This rider waives the monthly portion of the premium that pays for the expenses of the policy (e.g., contract expenses and mortality charge), but not the portion that’s allocated to the cash value.

No Lapse Guarantee Rider

A no lapse guarantee rider may be added to a universal life policy. Universal life insurance offers the contract owner with premium flexibility that could result in insufficient premiums being paid to support the policy. As previously described, paying insufficient premiums could cause the policy to lapse. The no lapse guarantee benefit rider prevents a lapse by imposing a premium payment schedule, which requires minimum premiums on a regular payment schedule. In other words, the no lapse guarantee rider guarantees that the policy will not terminate before a determined date if specified amounts of premium are paid, and any policy loan plus accrued loan interest don’t exceed the cash surrender value. The length of the policy’s guarantee period generally ranges from five to 40 years, depending on the age of the insured when the policy was issued. Some (but not all) insurers charge an extra premium for this rider.

Indexed Universal Life

Universal life insurance comes in many different models, from fixed rate models to variable ones. In a variable model, a person may select various equity accounts in which to invest. An indexed universal life (IUL) allows the owner to allocate cash value amounts to either a fixed account or an equity index account. Policies offer a variety of indices, such as the S&P 500. These policies are more volatile than fixed account plans, but less risky than variable life policies since no funds are invested in equities.

Indexed universal life plans also offer tax-deferral of cash accumulation while maintaining a death benefit. Individuals who seek permanent protection but want to take advantage of an equity index may use these plans to fund various programs such as key-person insurance for business owners or estate planning. These plans are considered advanced life insurance products since they may be difficult for the average consumer to comprehend.

Guaranteed / No-Lapse Guarantee Universal Life

Guaranteed universal life insurance—which is also referred to as no-lapse guaranteed universal life or guaranteed death benefit universal life—is a type of life insurance that provides a policy owner with a guaranteed death benefit, as long as the required premiums are paid. Therefore, even if there’s insufficient cash value within the contract to support the death benefit, the policy will continue to remain in force due to the coverage protection guarantee. For this guarantee to be provided, the contract stipulates that minimum premiums must be met and paid on time. As such, a guaranteed universal life insurance contract will still pay out a death benefit even if the accumulated cash value decreases or goes to zero.

As with most types of universal life insurance, guaranteed universal life offers flexible premium options that can vary based on an individual’s ever-changing financial situation. However, a minimum premium (or premium target) must still be met to prevent the policy from lapsing. Also, any variation in premium amounts will affect the interest rate within the contract, which will affect the cash value accumulations. The focal point of this type of product is the guaranteed death benefit rather than the cash value accumulations.

Most insurers allow a policy owner to select a guaranteed coverage period (e.g., age 90 or age 120). In effect, this means that the contract provides permanent protection with the flexible premium structure of a traditional universal life insurance plan. Additionally, some insurers provide the policy owners with the flexibility to change the coverage period as their needs or situations change.

Survivorship Guaranteed Universal Life

As with a survivorship life insurance policy, a survivorship universal life insurance contract is often referred to as second-to-die insurance. The contract covers two people and pays a benefit only after both covered individuals have died. Since it costs less than two individual permanent policies, it’s an affordable option for a person who wants to leave a larger nest egg for his heirs or a favorite charity. First-to-die versus second-to-die life insurance is reviewed more extensively later in this chapter.

SECURITIES AND EXCHANGE COMMISSION (SEC) REGULATED LIFE INSURANCE POLICIES

The Securities and Exchange Commission (SEC) regulates securities transactions, which include the trading of stocks, bonds, and variable insurance products. The Financial Industry Regulatory Authority (FINRA) is the entity that oversees securities firms in the United States. Formerly, the National Association of Securities Dealers (NASD), this regulatory body governs securities activities, administers securities exams, and issues licenses. Therefore, producers who want to solicit variable products must hold a life insurance license as well as a securities license.

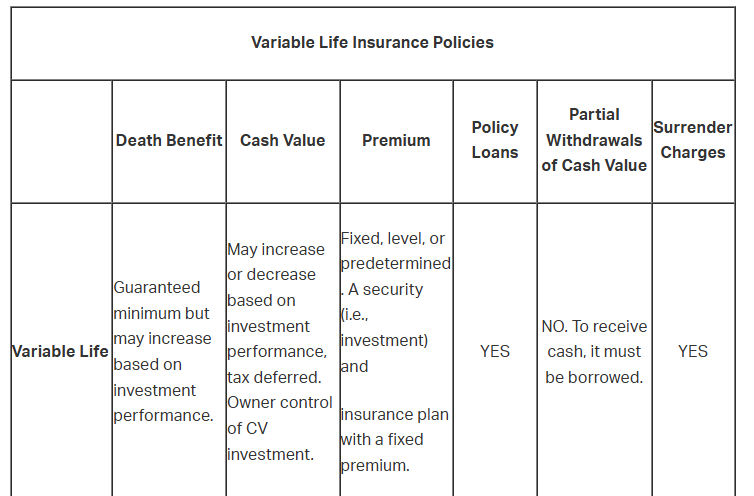

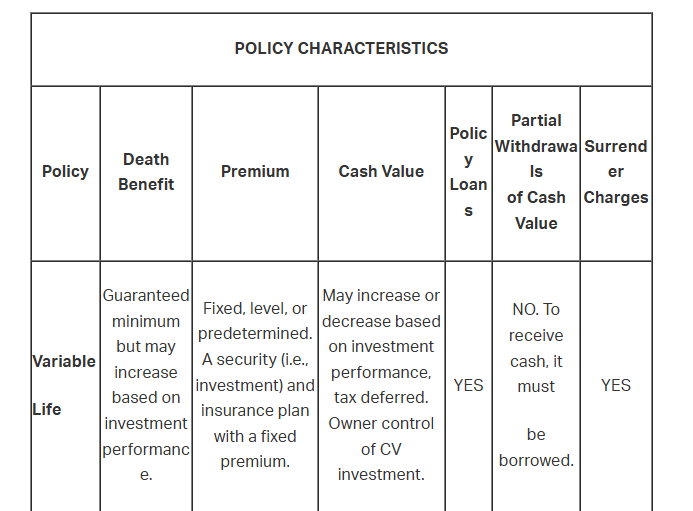

VARIABLE LIFE

Variable life insurance (VL) combines the protection and savings features of whole life insurance with the growth potential of securities, such as common and preferred stocks, bonds, and other similar investments. Variable life insurance is a type of permanent (i.e., whole life) insurance that’s characterized by fixed (level) premiums and a guaranteed minimum death benefit. Part of the premium paid is placed into a separate account, which is invested in a stock, bond, or money market fund. Although the death benefit is guaranteed, the cash value of the benefit can vary considerably based on the rise and fall of the stock market.

The policy’s death benefit can also increase if the earnings of that separate fund increase. Variable insurance products don’t guarantee contract cash values, and it’s the policy owner who assumes the investment risk.

Variable life insurance contracts don’t provide guarantees as to either interest rates or minimum cash values. Instead, these products offer the potential to realize investment gains which exceed those that are available with traditional life insurance policies. The potential for more significant investment gains is offered by allowing policy owners to direct the investment of the funds that back their variable contracts through separate account options.