Chapter 12: Reporting Cash Flows - Summary Notes

Chapter 12: Reporting Cash Flows

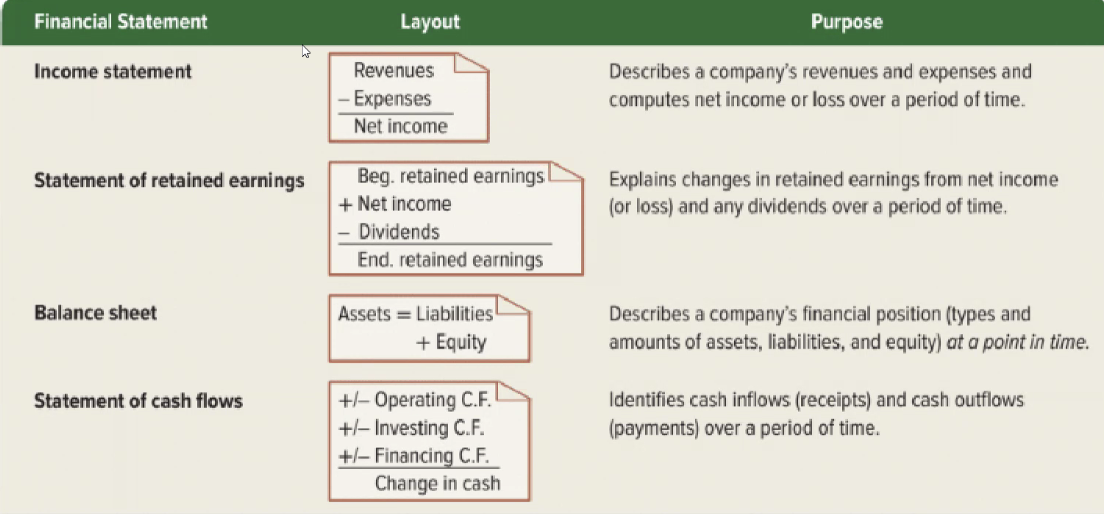

Purpose of the Statement of Cash Flows

Addresses questions such as:

How does a company receive its cash?

Where does a company spend its cash?

Why do income and cash flows differ?

What explains the change in cash balance?

Importance of Cash Flows

Cash flows help:

Users decide if a company has cash to pay its debts.

Users evaluate a company’s ability to pursue opportunities.

Managers plan day-to-day operations.

Managers make long-term investment decisions.

Measurement of Cash Flows

Cash flows include both cash and cash equivalents.

Cash equivalents must:

Be readily convertible into cash, and

Be sufficiently close to maturity so that market value is unaffected by interest rate changes.

Classification of Cash Flows

The Statement of Cash Flows includes three sections:

Operating Activities

Investing Activities

Financing Activities

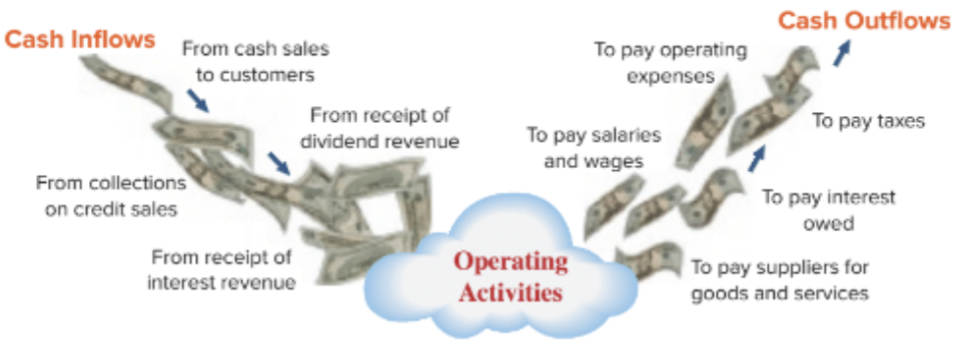

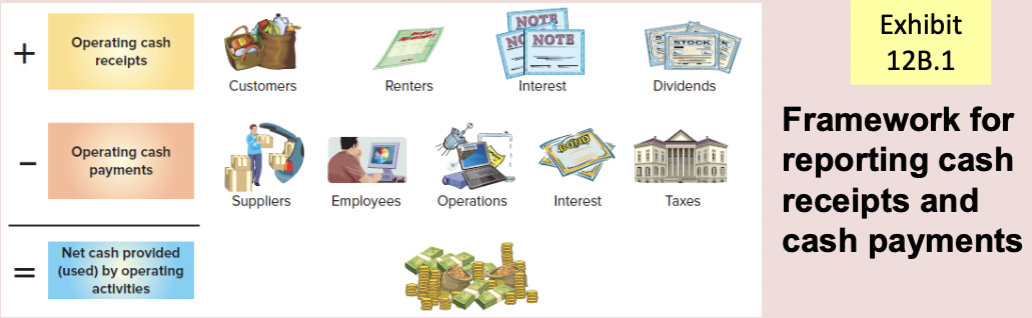

Operating Activities

These activities concern the normal day-to-day running of the business i.e. the business's main revenue-generating activities.

Examples of cash inflows include:

Cash receipts from sales of goods or services

Cash receipts from interest income and dividend income

Examples of cash outflows include:

Cash payments to suppliers for goods and services

Cash payments to employees

Cash payments for interest

Cash payments for taxes

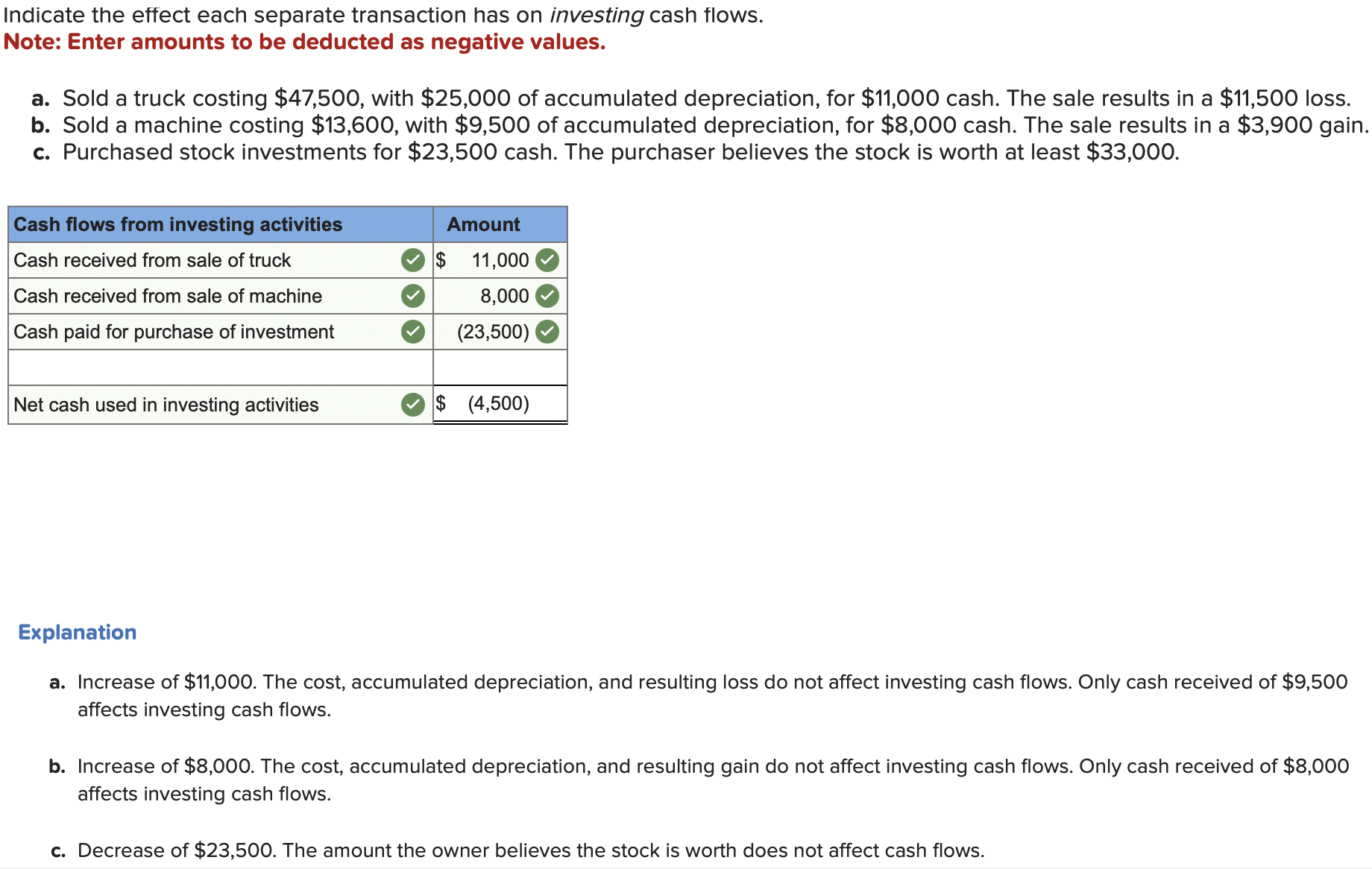

Investing Activities

These activities concern the purchase and sale of long-term assets and include:

Examples of cash inflows include:

Cash receipts from the sale of property, plant, and equipment (PPE)

Cash receipts from the sale of investments in securities

Cash receipts from collection of principal on loans to other entities

Examples of cash outflows include:

Cash payments to purchase property, plant, and equipment (PPE)

Cash payments to purchase investments in securities

Cash payments to make loans to other entities

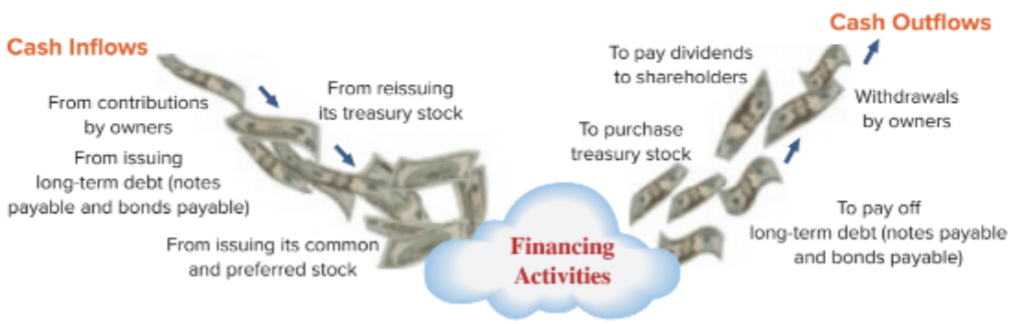

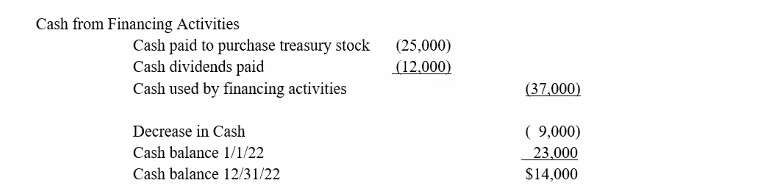

Financing Activities

These concern how the company is financed, including debt and equity.

Examples of cash inflows include:

Cash receipts from the issuance of stock

Cash receipts from the issuance of bonds and notes payable

Examples of cash outflows include:

Cash payments to repurchase stock (treasury stock)

Cash payments for repayment of debt principal

Cash payments for dividends to shareholders

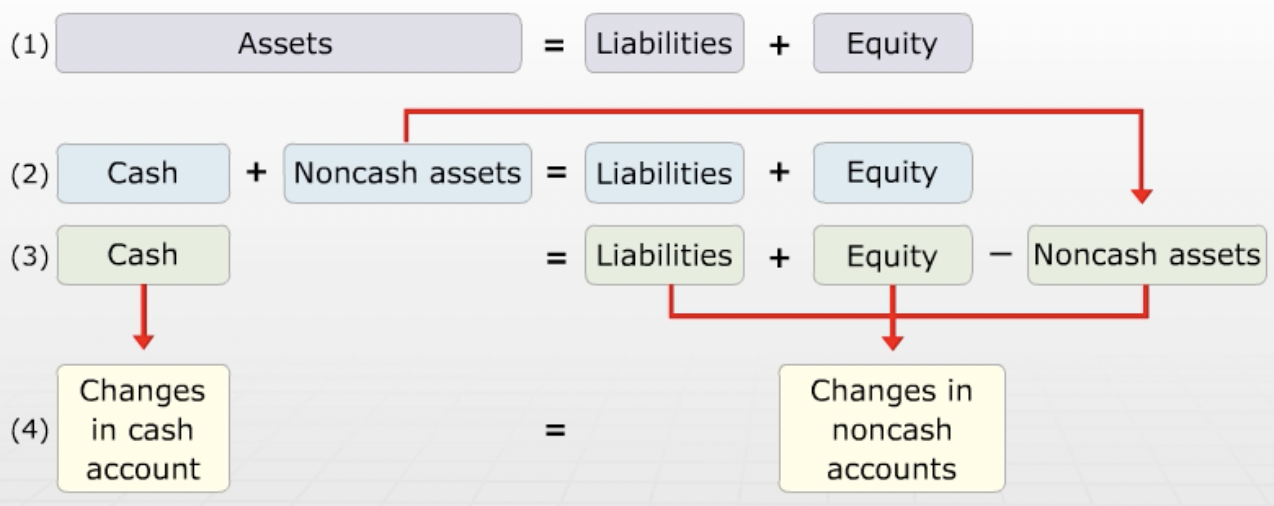

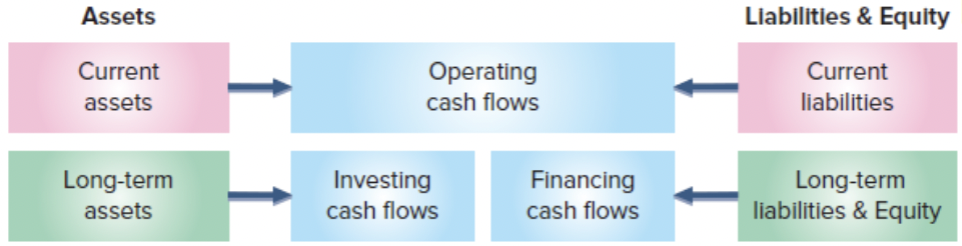

Link Between Classification of Cash Flows and the Balance Sheet

Operating, investing, and financing activities are loosely linked to the balance sheet.

Operating activities are affected by changes in current assets and current liabilities.

Investing activities are affected by changes in long-term assets.

Financing activities are affected by changes in long-term liabilities and equity.

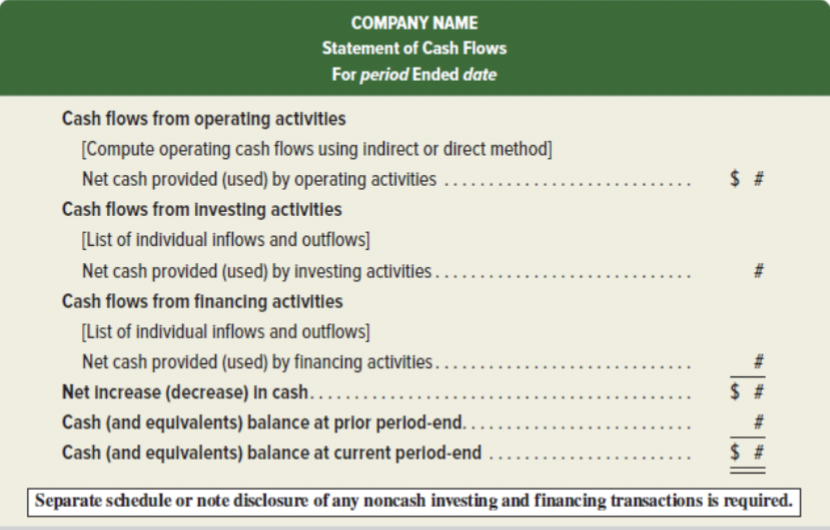

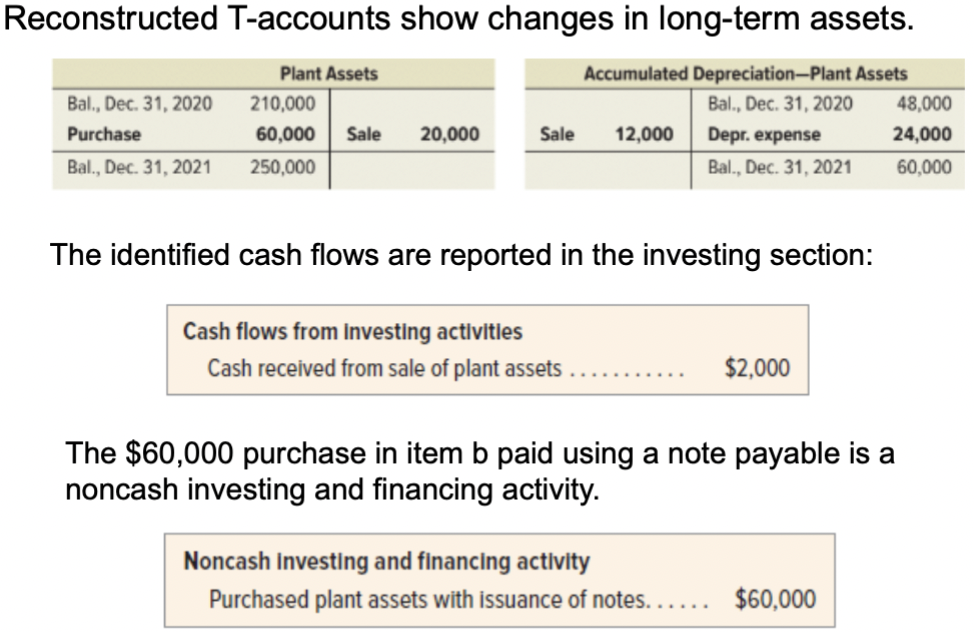

Noncash Investing and Financing Activities

Important noncash activities are disclosed in either a note to the statement or in a separate schedule.

Examples include:

Retirement of debt by issuing stock

Purchase of assets by issuing stock or bonds

Exchange of long-lived assets

Format of the Statement of Cash Flows

The statement presents cash flows from operating, investing, and financing activities in a specific format to facilitate analysis.

Typically includes a reconciliation of net income to net cash flow from operations.

Preparing the Statement of Cash Flows

Compute net increase or decrease in cash

Compute net cash from or for operating activities

Compute net cash from or for investing activities

Compute net cash from or for financing activities

Compute net cash from all sources then prove it by adding it to the beginning cash to get ending cash

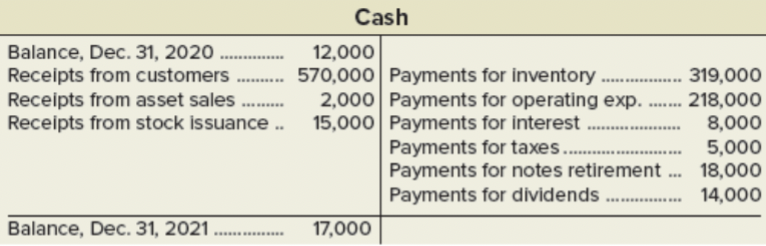

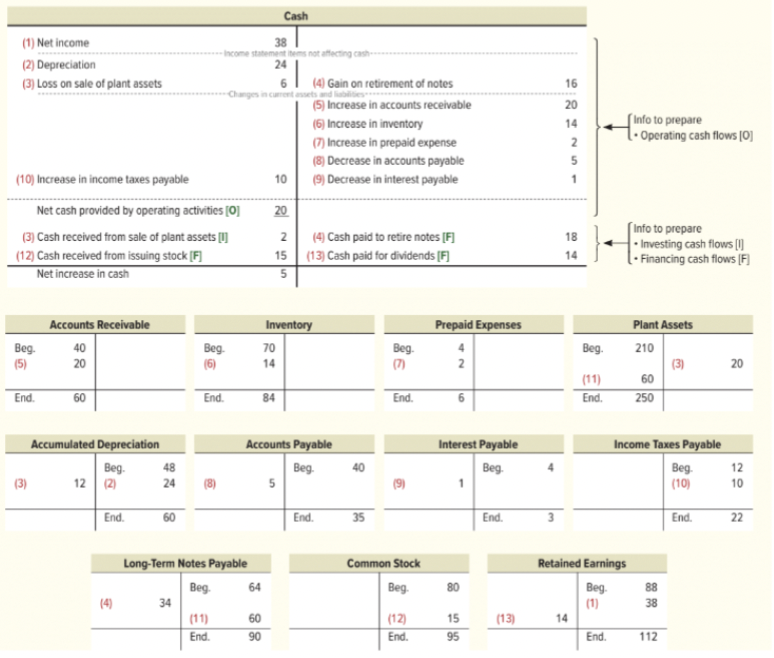

Analyzing the Cash Account

The Cash account is a natural place to look for information about cash flows from operating, investing, and financing activities.

Analyzing Noncash Accounts

A second approach to preparing the statement of cash flows is analyzing noncash accounts.

Information to Prepare the Statement

Information to prepare the statement of cash flows comes from three sources:

Comparative Balance Sheets

Current Income Statement

Additional Information

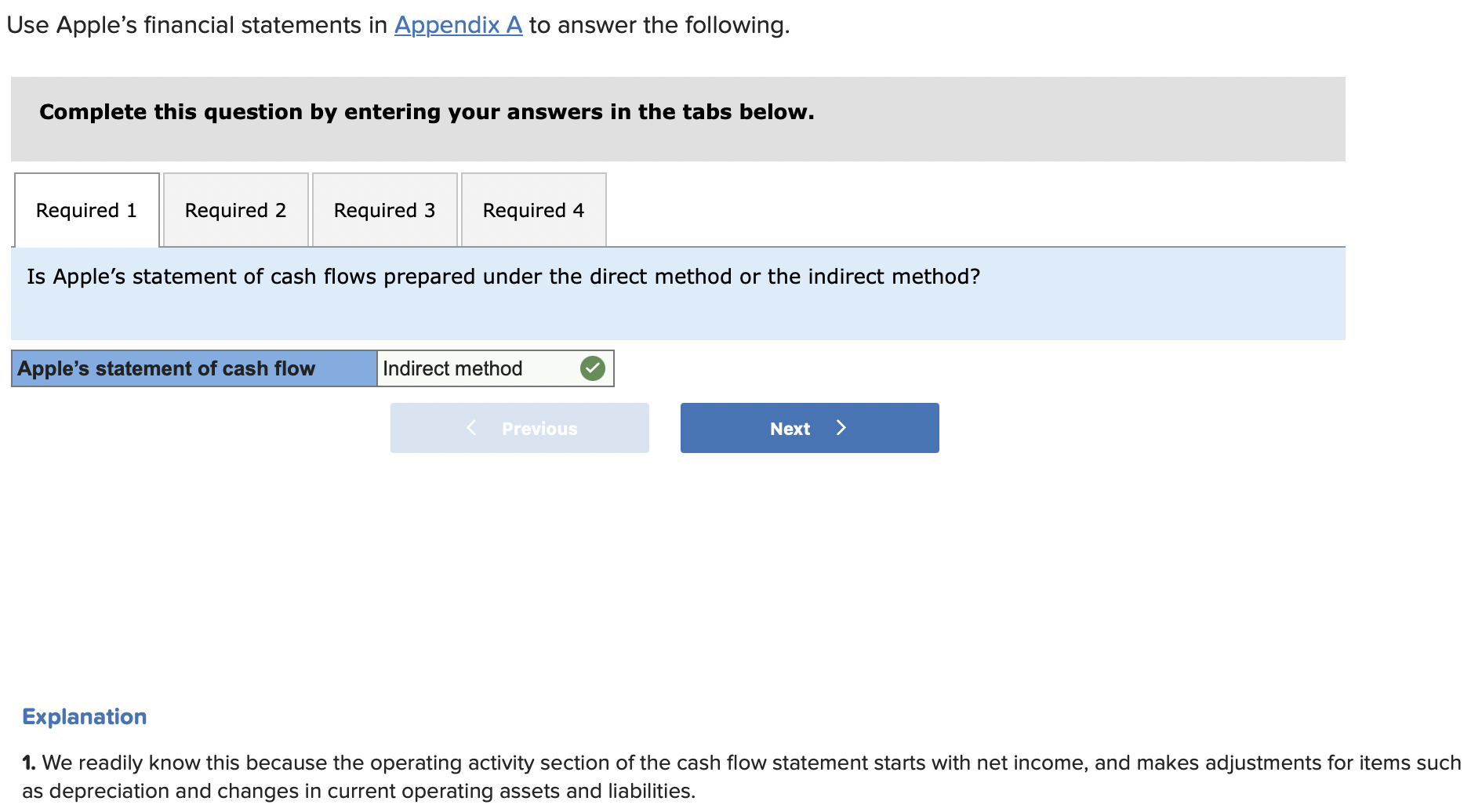

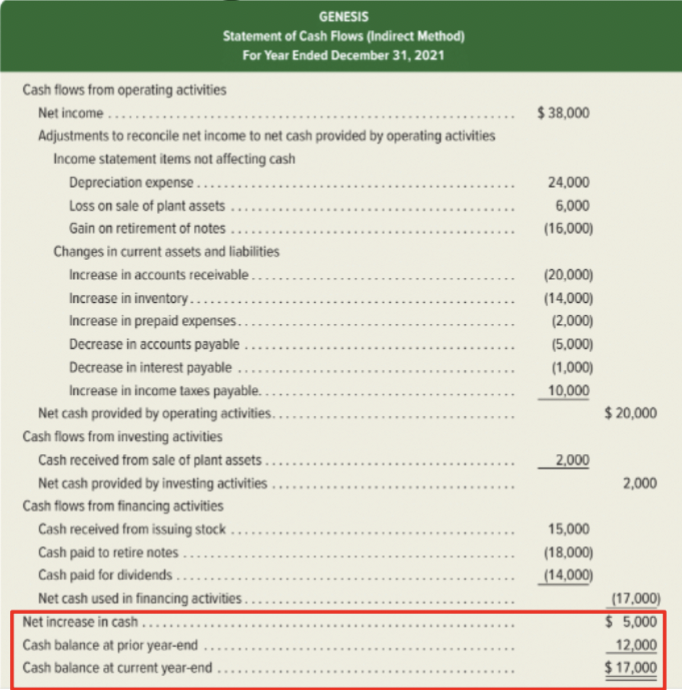

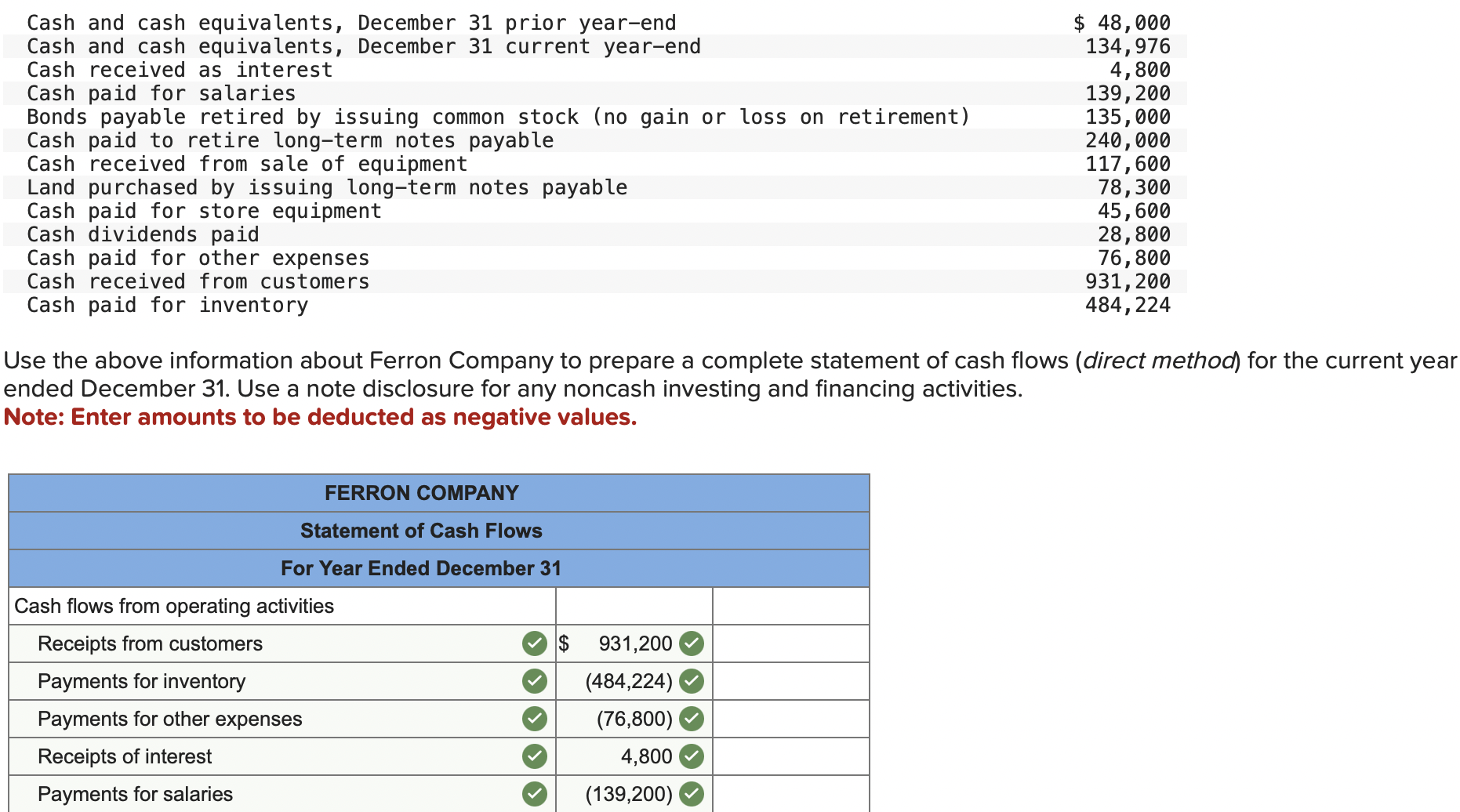

Cash Flows from Operating Activities: Indirect and Direct Methods

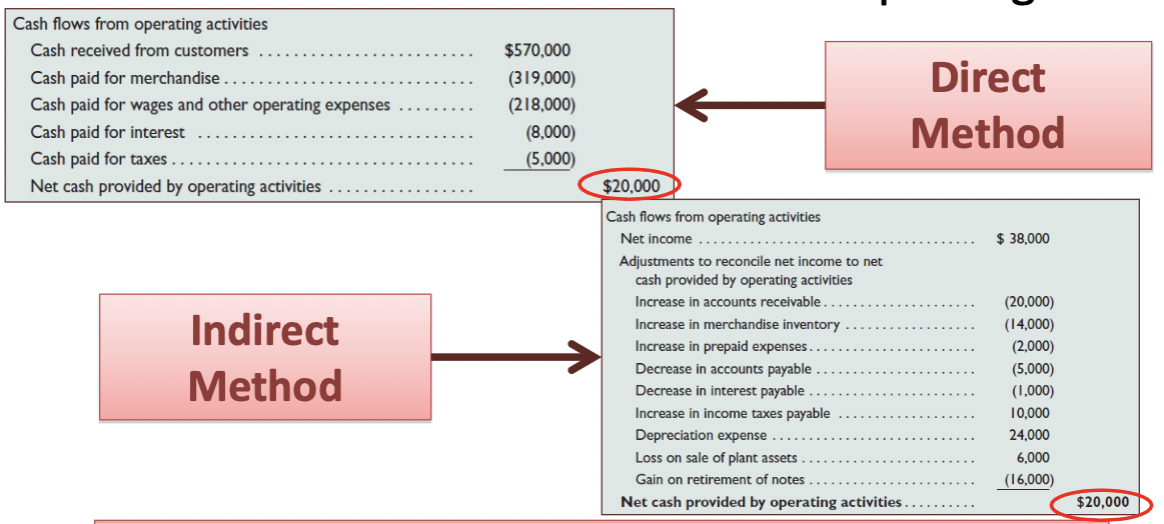

The net cash amount provided by operating activities is identical under both the direct and indirect methods.

Direct Method: Reports cash receipts and cash payments.

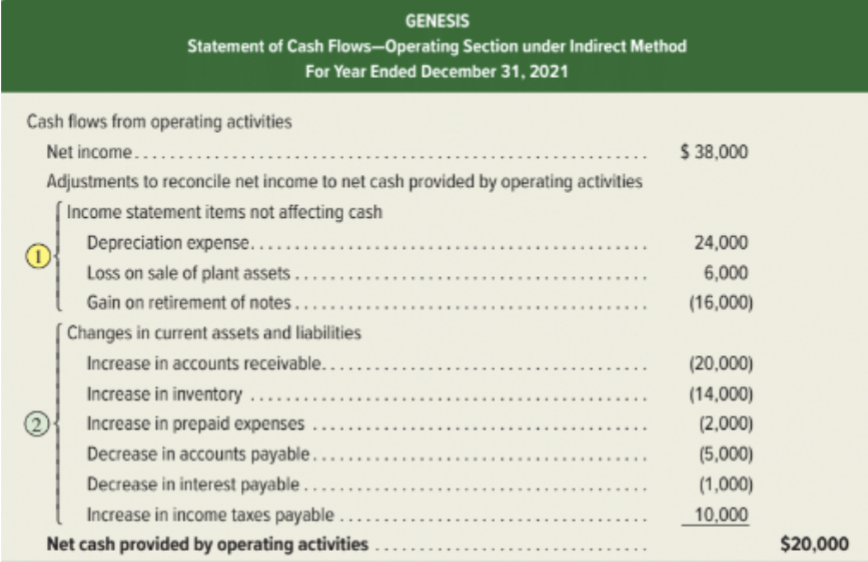

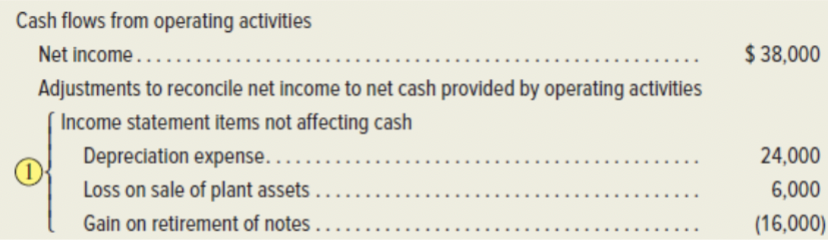

Indirect Method: Adjusts net income to arrive at net cash flow from operating activities.

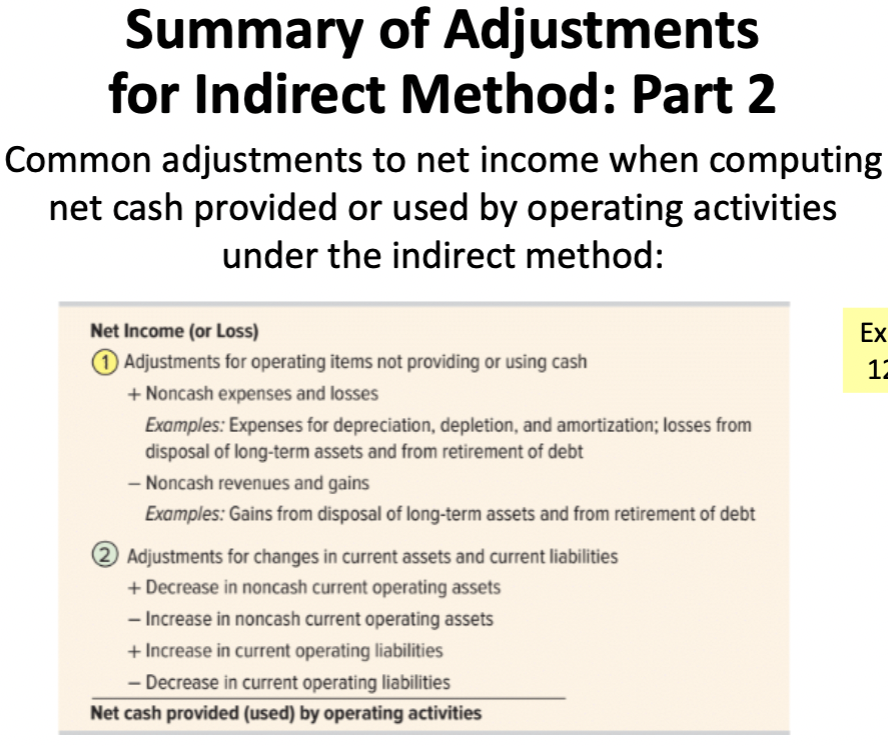

Adjustments for Income Statement Items Not Affecting Cash (Indirect Method)

Expenses and losses with no cash outflows are added back to net income.

Revenues and gains with no cash inflows are subtracted from net income.

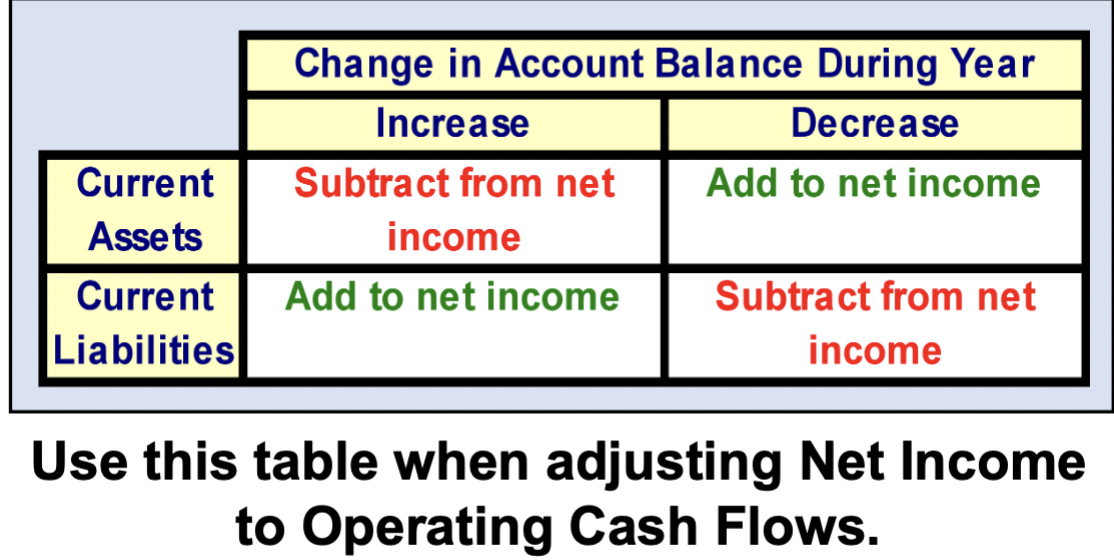

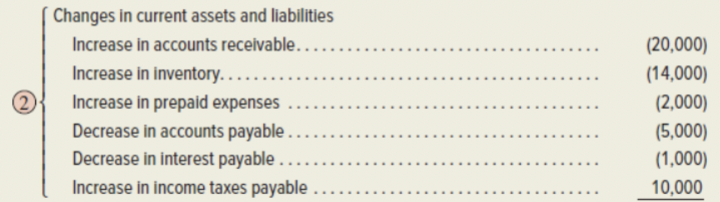

Adjustments for Changes in Current Assets and Current Liabilities (Indirect Method)

Decreases in current assets are added to net income.

Increases in current assets are subtracted from net income.

Increases in current liabilities are added to net income.

Decreases in current liabilities are subtracted from net income.

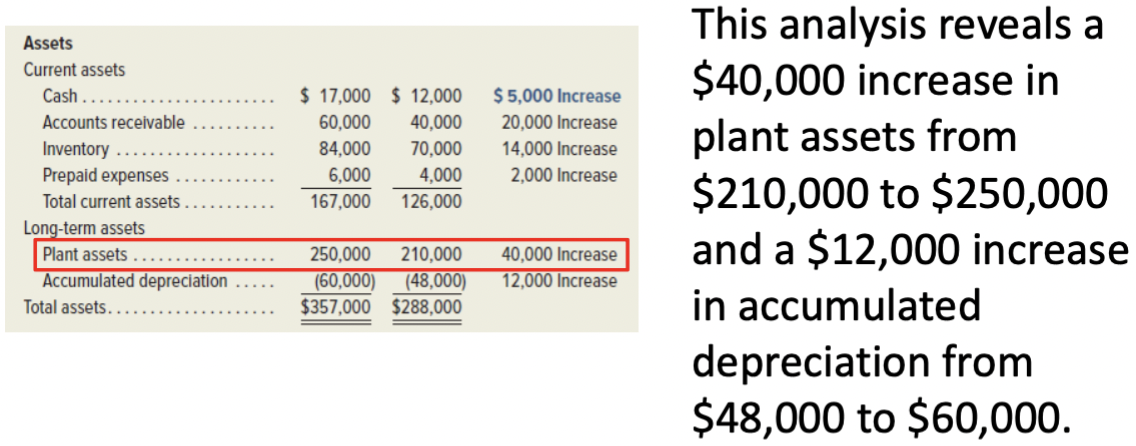

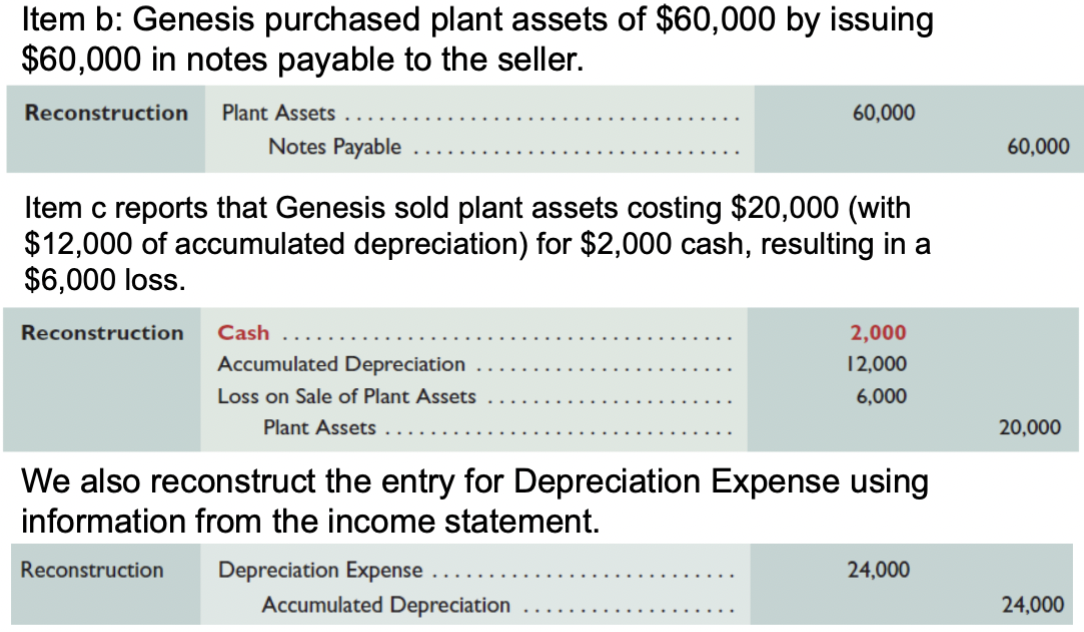

Cash Flows from Investing: Three-Step Analysis

Identify changes in investing-related accounts.

Determine the cash effects using T-accounts and reconstructed entries.

Report the cash flow effects.

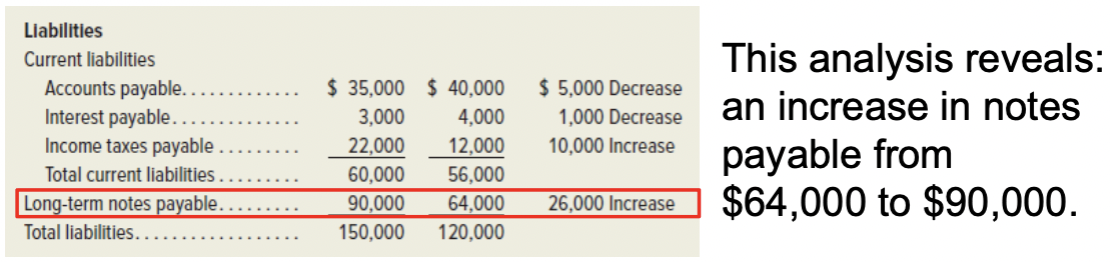

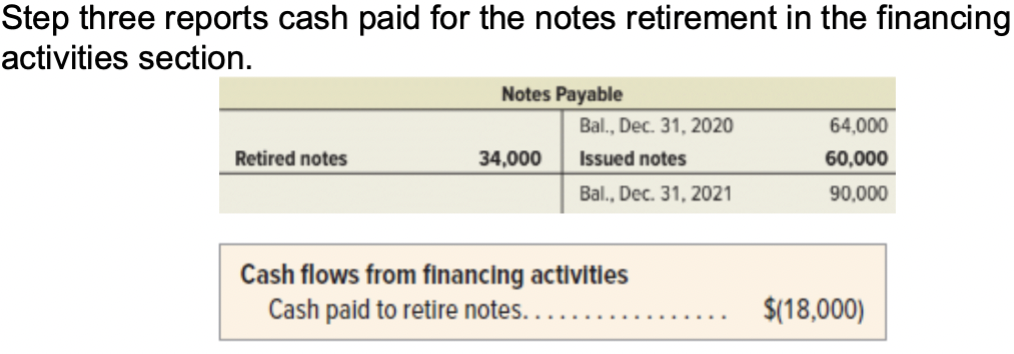

Cash Flows from Financing: 3-Step Analysis

A 3-step process to determine cash provided or used by financing activities:

Identify changes in financing-related accounts

Determine the cash effects using T-accounts and reconstructed entries

Report cash flow effects

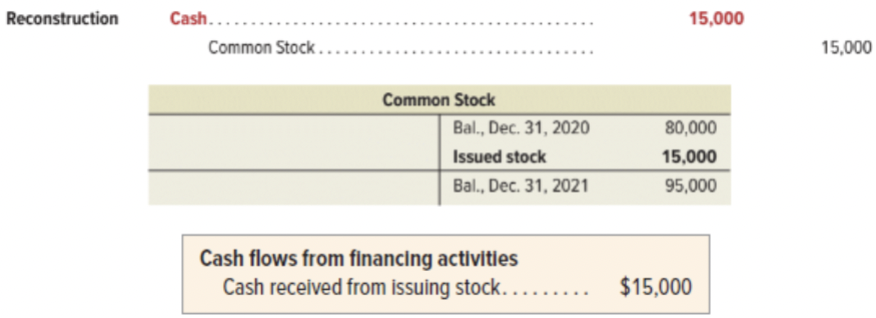

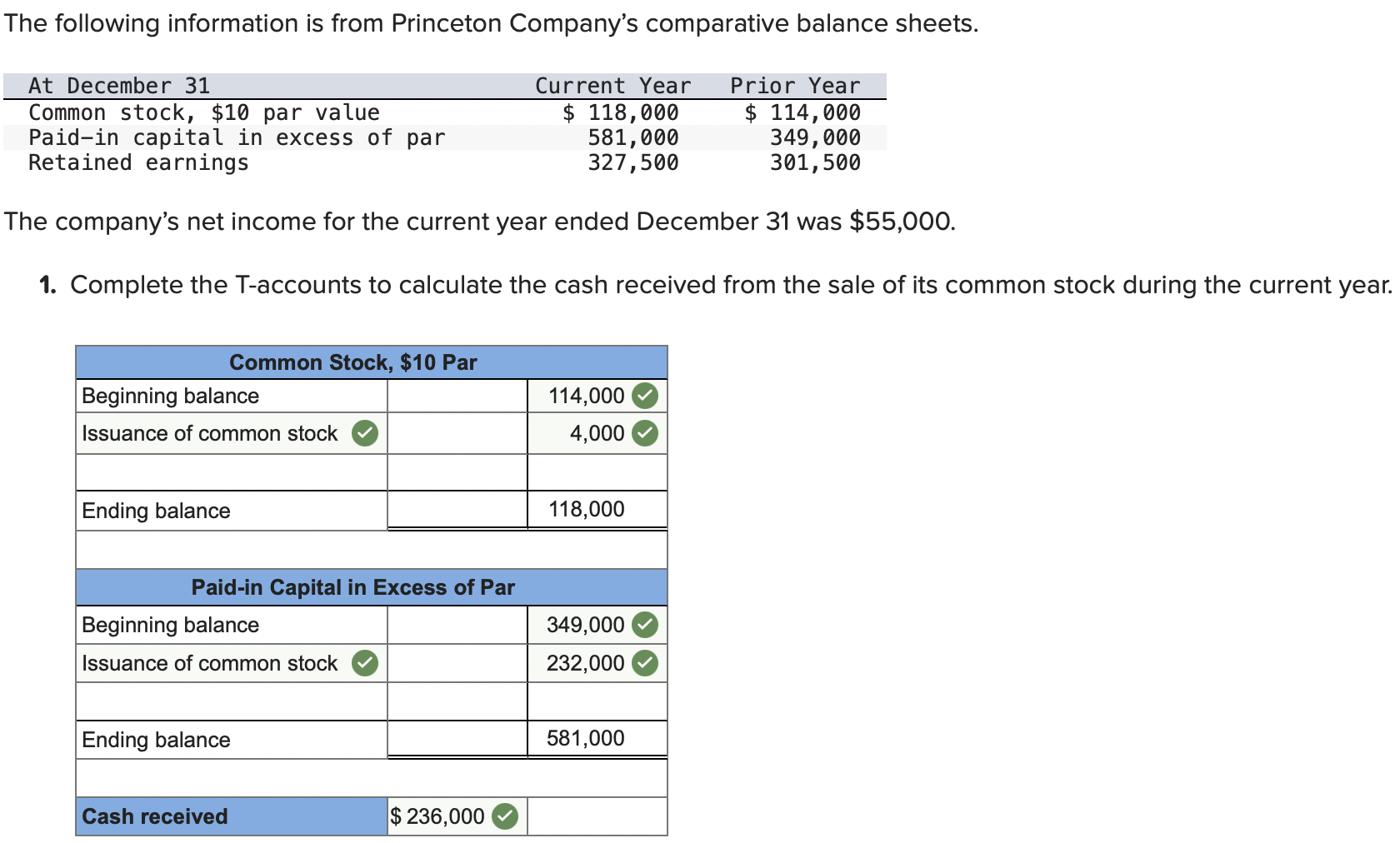

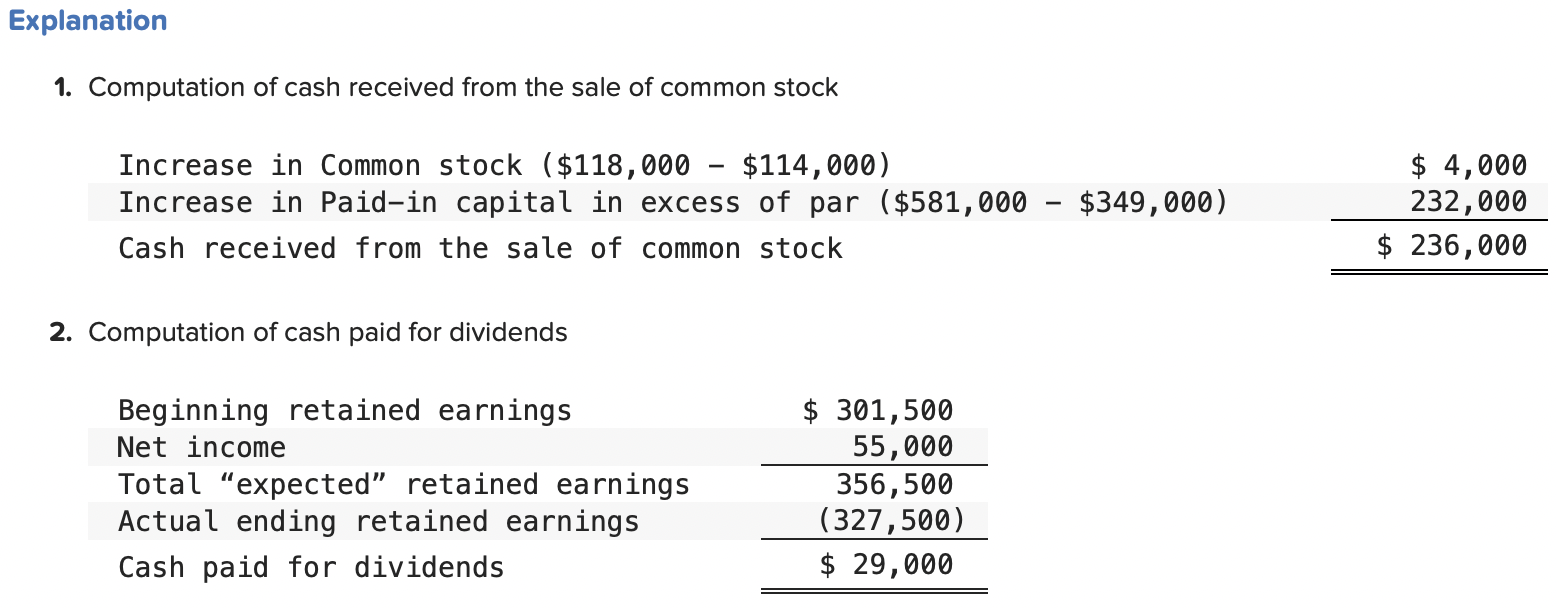

Cash Flows from Financing: Common Stock Transactions

Step one in analyzing stock reviews comparative balance sheets.

Step two explains change such as stock issuance.

Step three reports cash received from stock issuance in financing activities section.

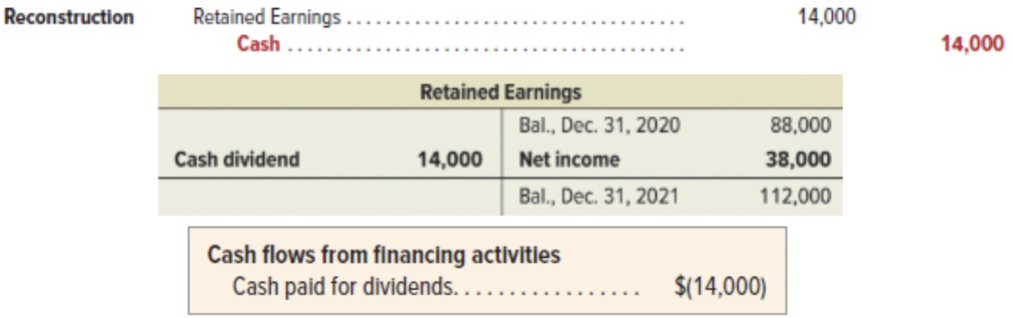

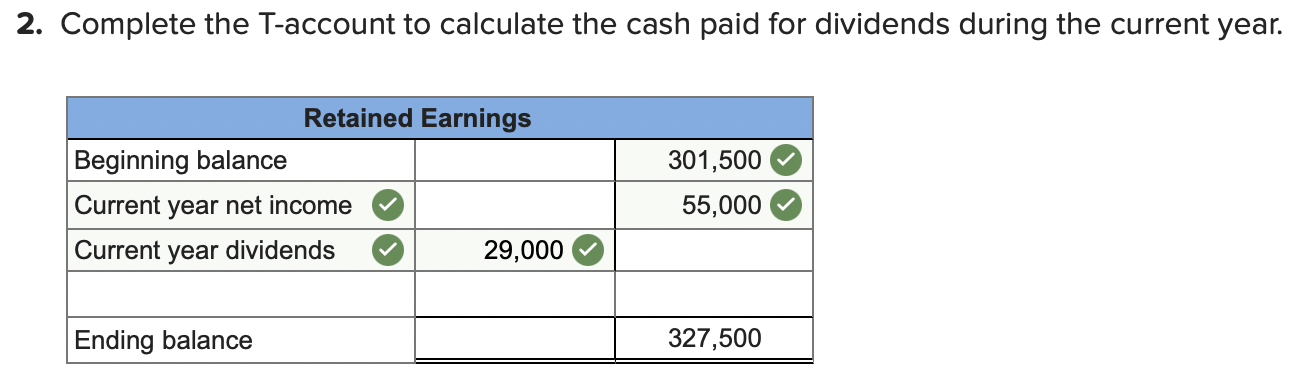

Cash Flows from Financing: Retained Earnings Transactions

Step one in analyzing Retained Earnings reviews comparative balance sheets.

Step two explains change such as cash dividends are paid.

Step three reports cash paid for dividends in the financing activities section.

Proving Cash Balances

Summary Using T-Accounts

Analyzing Cash Sources and Uses

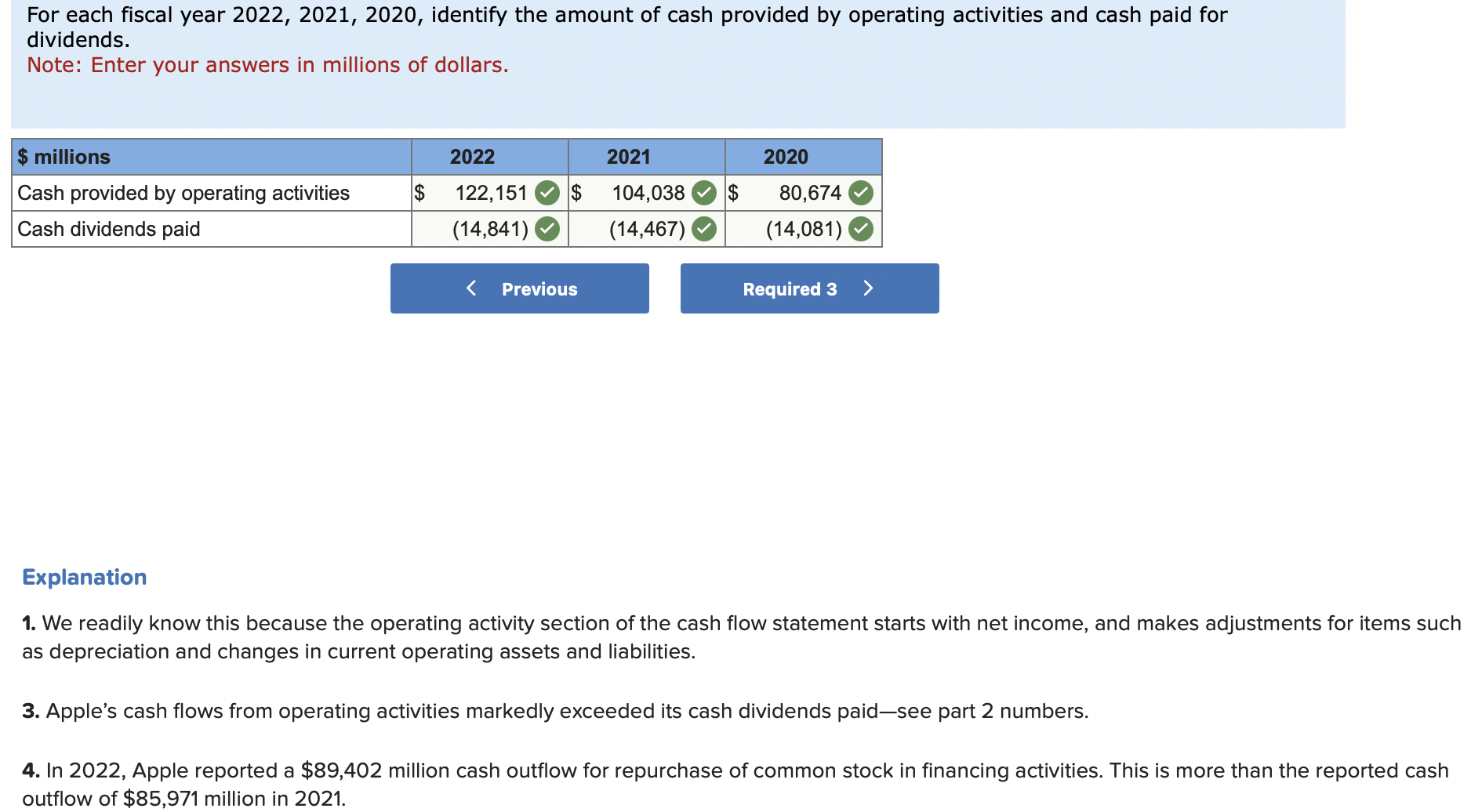

Managers review cash flows for business decisions.

Creditors evaluate a company’s ability to generate enough cash to pay debt.

Investors assess cash flows before buying and selling stock.

Cash Flow on Total Assets

Used, along with income-based ratios, to assess company performance.

Formula:

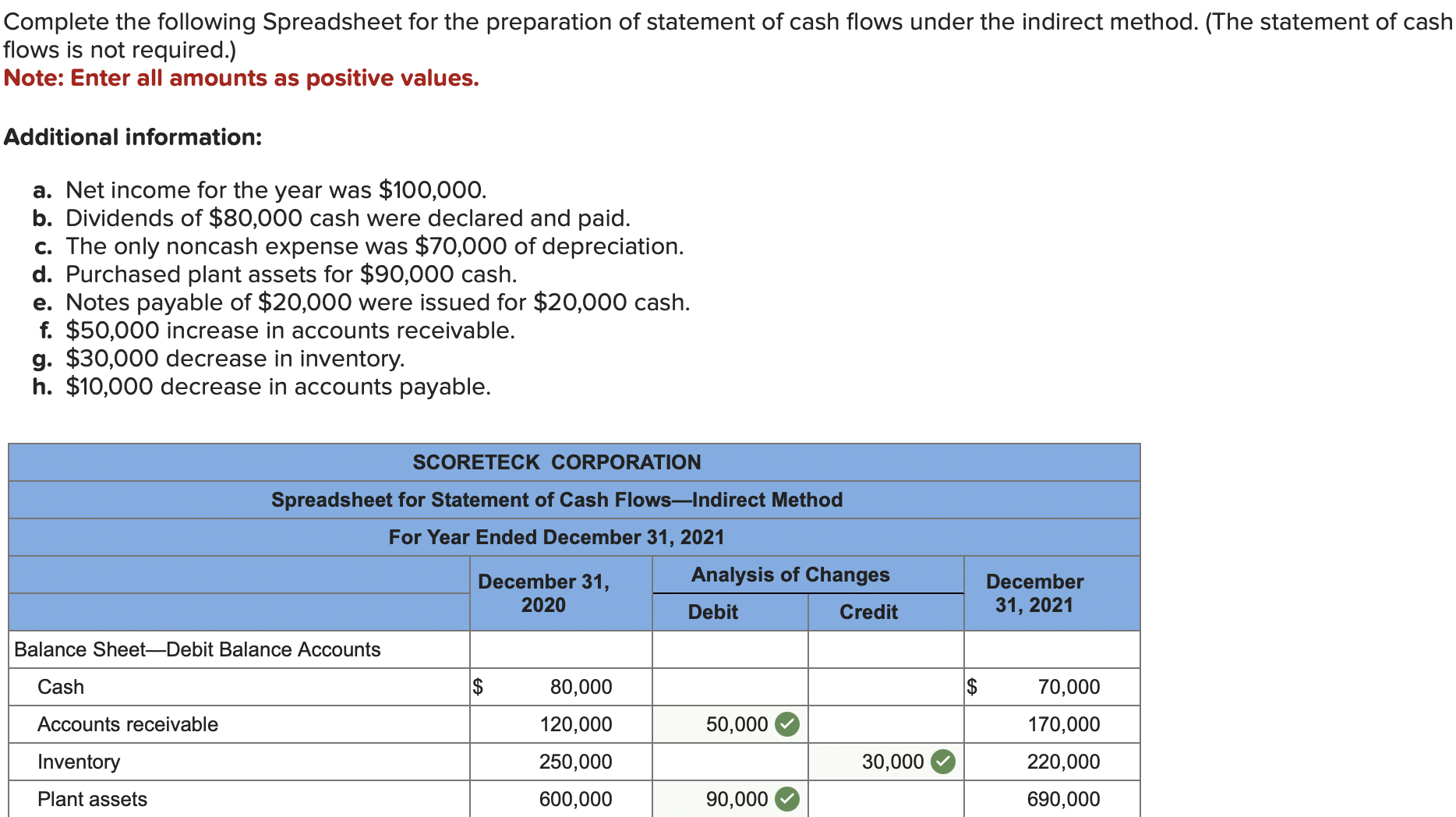

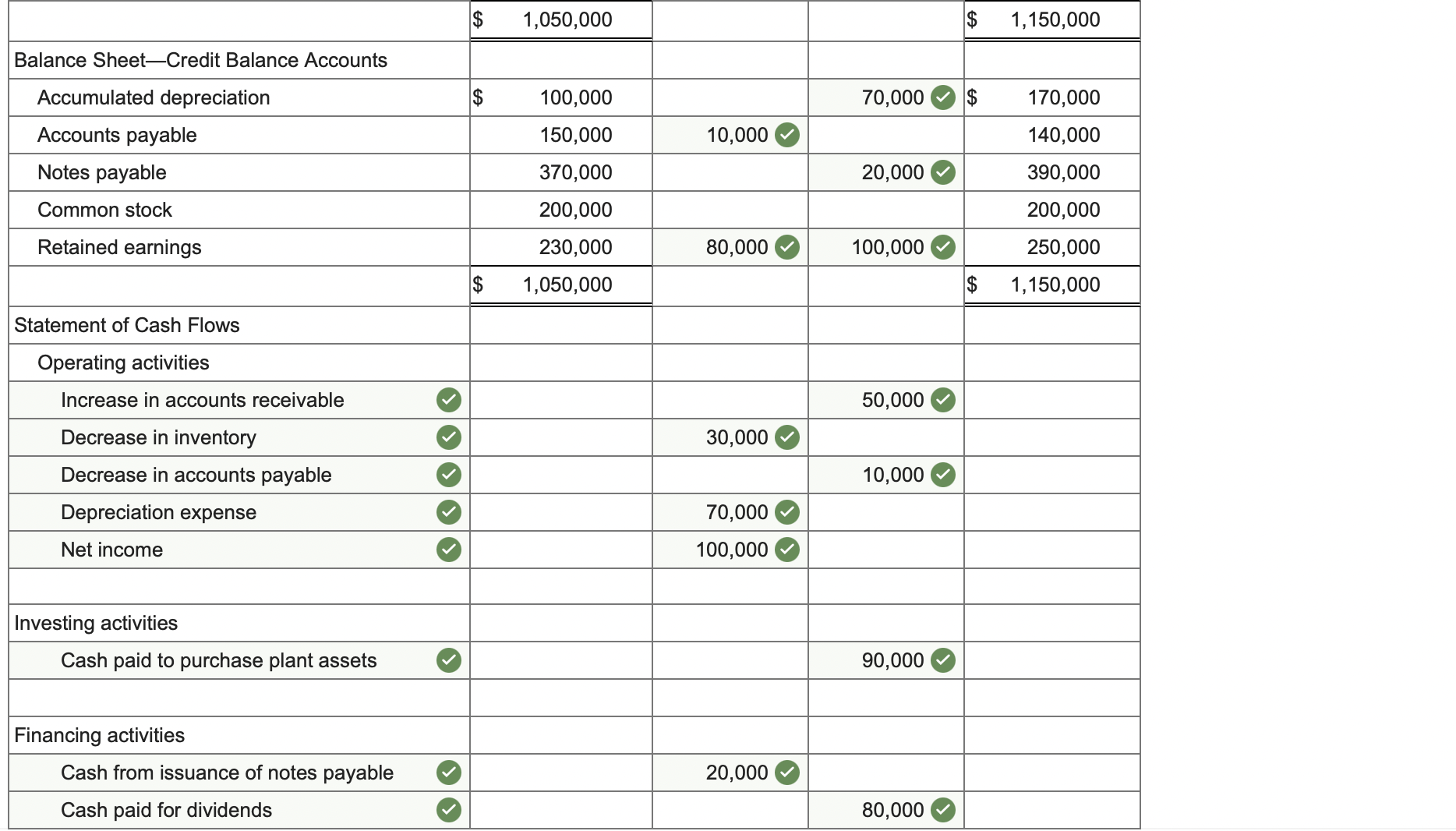

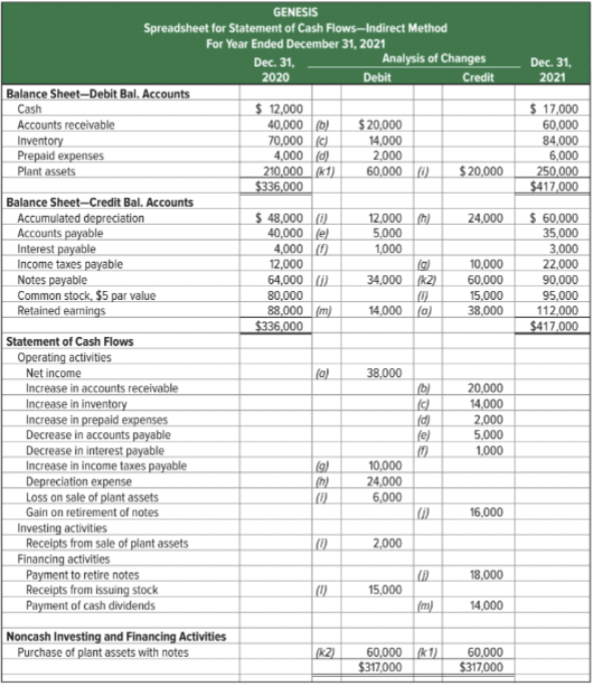

Spreadsheet Preparation (Appendix 12A)

A spreadsheet, also called work sheet or working paper, can help us organize the information needed to prepare a statement of cash flows.

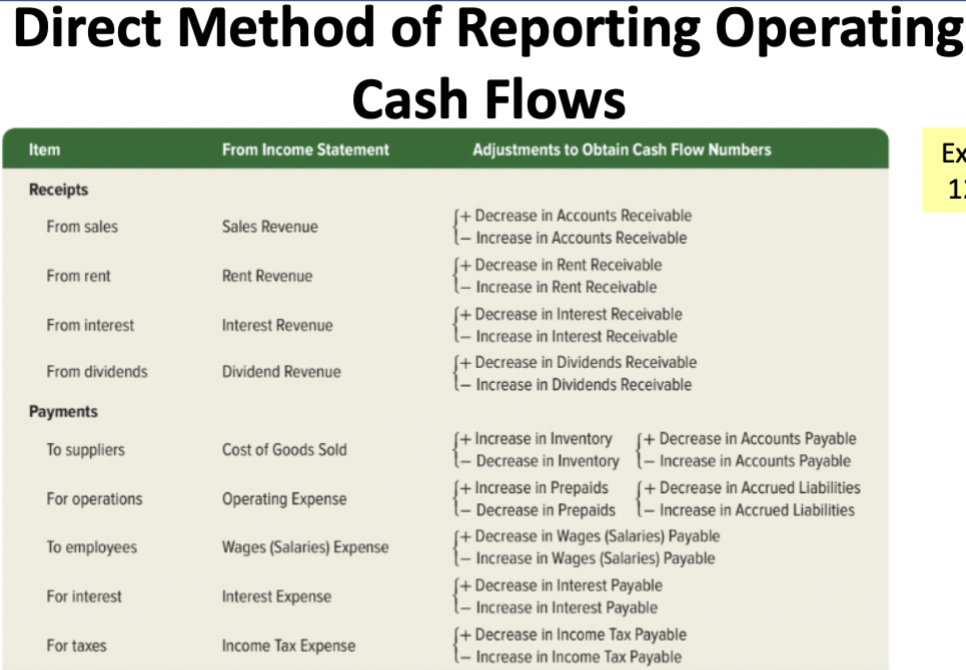

Direct Method of Reporting Operating Cash Flows (Appendix 12B)

Adjust income statement accounts related to operating activities for changes in their related balance sheet accounts.

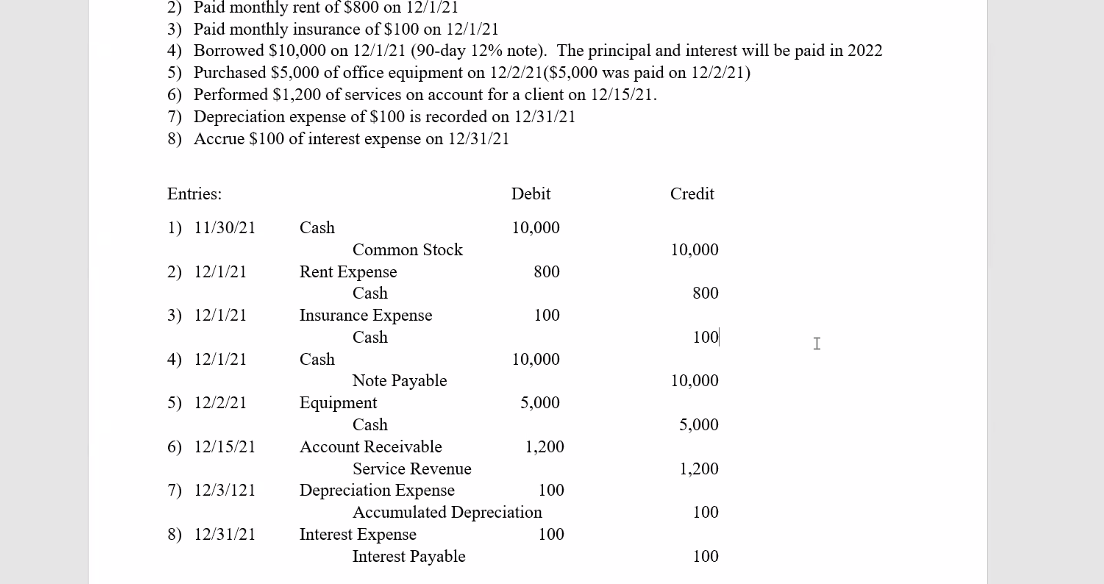

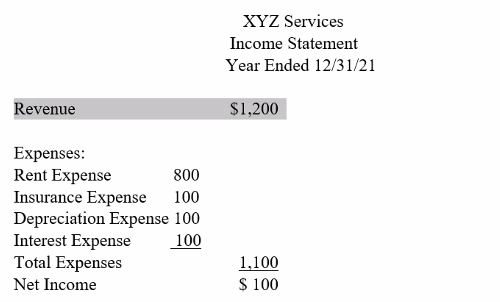

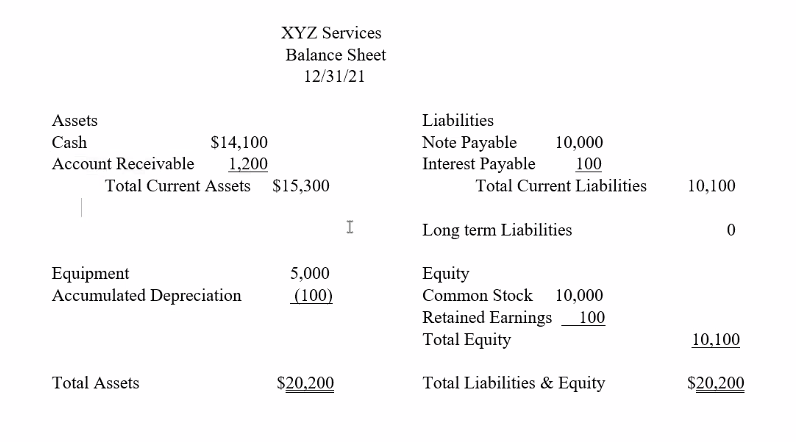

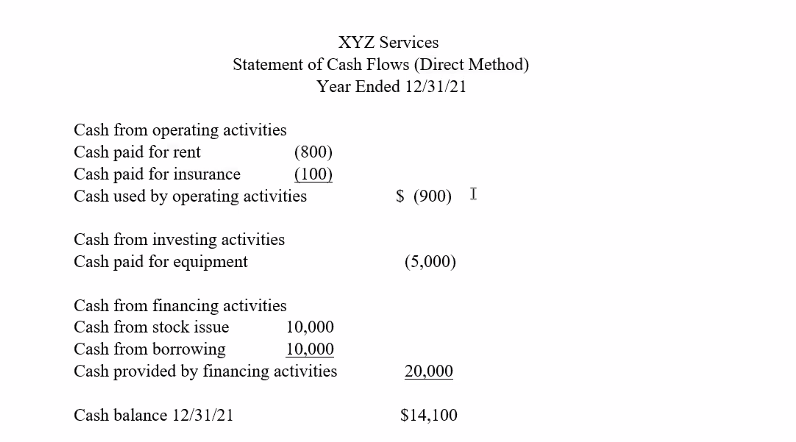

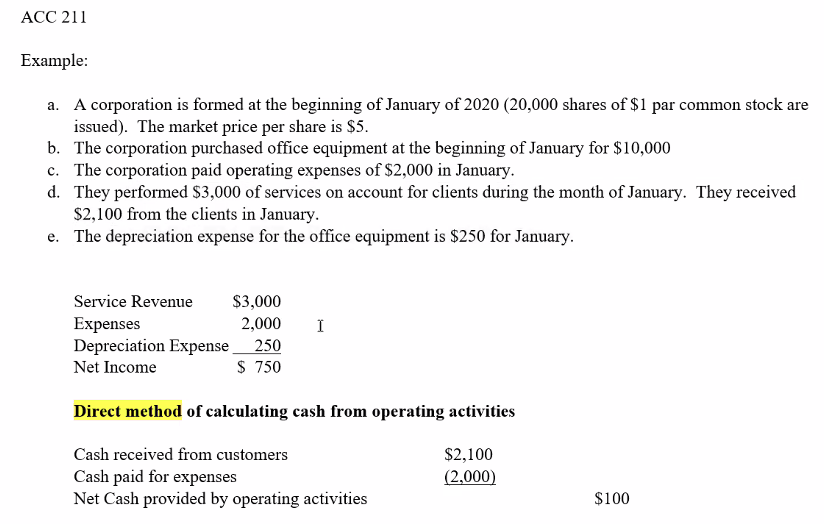

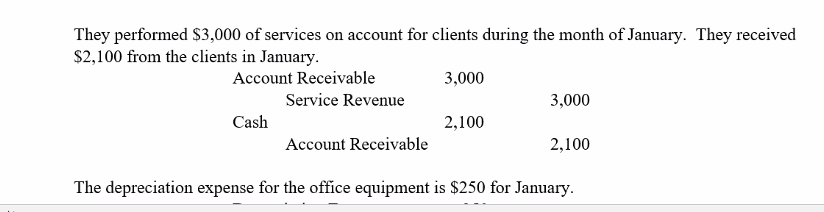

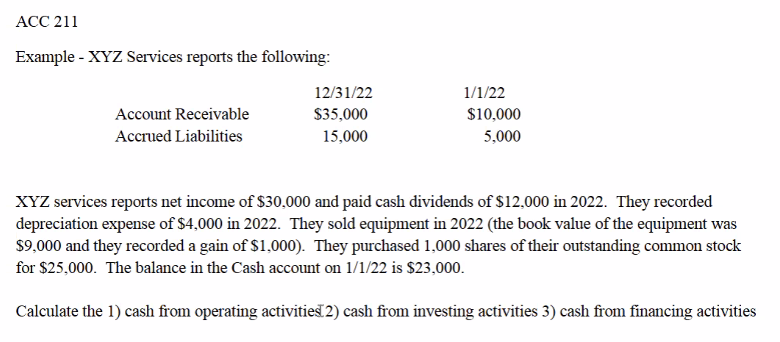

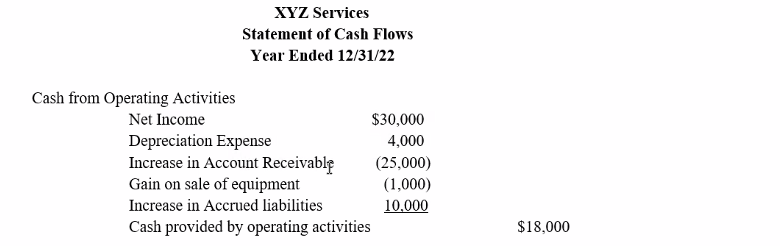

In-class lecture examples:

Cash from operating activities: $18,000

Cash from investing activities: $10,000

Cash received from sale of equipment $10,000

Cash from financing activities:

Ch 12 Assignment Questions

Explanation

The noncash investing/financing section below the statement that contains two items.

(1) Issued common stock to retire $135,000 of bonds payable.

(2) Purchased land financed with a $78,300 long-term notes payable.