2.7 - mergers and acquisitions

this content introduces the concept of mergers and acquisitions [M&A] within CF&S. the primary focus is on why firms merge, how mergers are valued, financing options, defensive tactics, and post-merger performance

learning objectives

by the end of this unit, students should be be able to:

critically evaluate the motives for mergers - understanding why companies pursue mergers [e.g. growth, synergies, market power]

calculate the gains, costs, and NPV of a merger - analysing whether a merger creates financial value

discuss the efficient markets hypothesis [EMH] - how market efficiency impacts merger valuation

value a target firm using different valuation methods - learning techniques like discounted cash flow [DCF], comparables, and market multiples

examine defence tactics against takeovers - strategies that target firms use to resist hostile takeovers

what is a merger?

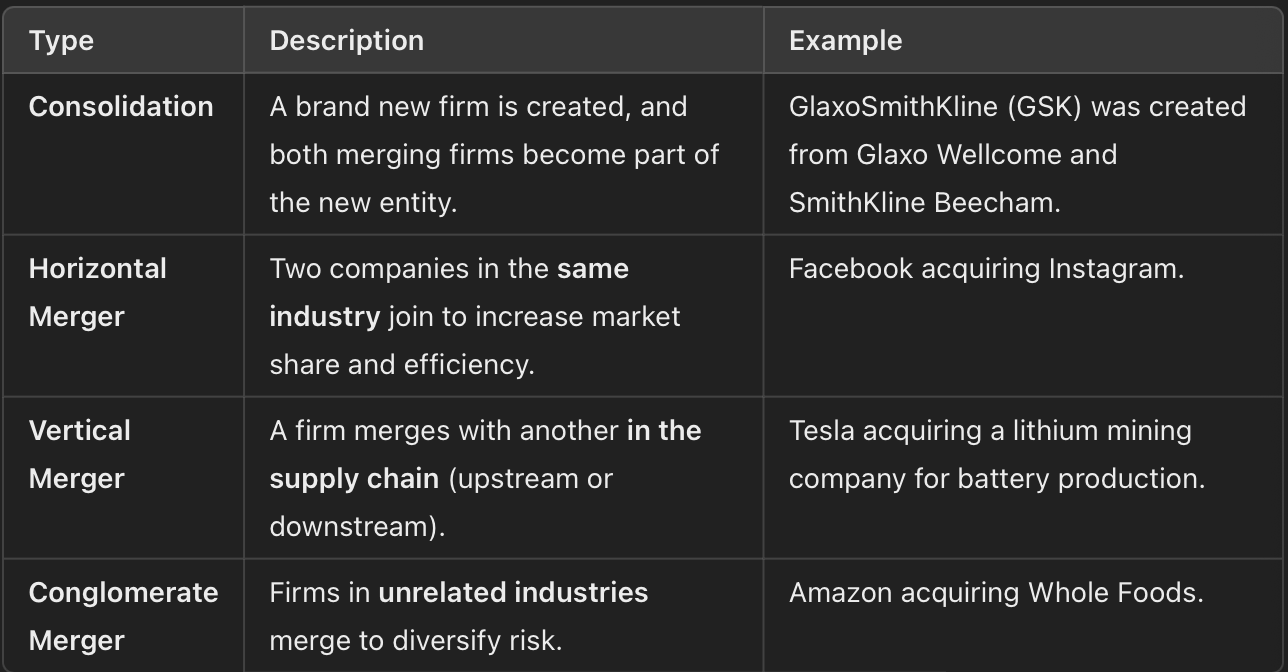

a merger is when 2 firms combine under common ownership

acquirer - the company that initiates and controls the merger

target - the company being acquired

mergers vs. acquisitions:

in a merger, 2 similar sized firms join to create a larger entity

in an acquisition, one firm takes over another [may be hostile or friendly]

investment appraisal of managers

should mergers be evaluated like other investments [DCF analysis]?

challenges:

motivations are diverse [e.g. synergies, market power, diversification]

benefits are hard to quantify [e.g. cost savings, revenue growth]

information asymmetry - target firms may have private information that acquirers don’t

types of mergers

what does this mean in corporation strategy?

mergers are a key tool for firms to expand, reduce costs, increase market power, or diversify

valuing mergers correctly is critical to avoid over paying

not all mergers succeed - integration challenges and overvaluation can reduce expected benefits

hostile takeovers lead to defensive tactics by the target firms [e.g. poison pill strategies]

takeovers

a takeover happens when one firm purchases another, gaining ownerships, financial and managerial control over the acquired firm

key characteristics of takeovers

typically, a large company acquires a smaller company by making a cash bid for its shares

shareholder approval from the target company is required for the deal to go through

agency problem - sometimes, the interests of management and shareholders may not align - shareholders may support a takeover, but the target firm’s management may resist it

types of takeovers

hostile takeover

the acquiring company bypasses the target firm’s board of directors and makes an offer directly to shareholders

why is it hostile? the target company’s management opposes the takeover

example - kraft’s hostile takeover of cadbury in 2010

management buyout [MBO]

the company is purchased by its own management team

why does this happen?

the management may feel they can run the business better independently

it may occur when a division of a company is being sold off

example - dell was taken private through an MBO in 2013

leveraged buyout [LBO]

a buyout where the acquisition is financed mostly with debt

the company assets act as collateral for the loan

why do firms use LBOs?

to gain control of a firm without using a lot of upfront capital

often used by private equity firms to acquire companies

example - KKR’s 31 bil. LBO of RJR Nabisco in 1989 [famously detailed in Barbarians at the Gate]

the merger process

mergers are complex and can vary based on the companies involved. however, some key principles apply to all mergers:

st.1 - identify potential target

the acquiring firm searches for a company that aligns with its strategic goals [e.g. growth, market share, cost savings]

due diligence is conducted to assess the target’s financial health, operations, and risks

st.2 - decision to merge [motives, benefits, and costs]

the acquirer must determine:

why merge? - [e.g. synergies, cost savings, diversification]

what are the financial benefits? [e.g. increased earnings, economies of scale]

what are the costs and risks? [e.g. cultural differences, integration challenges]

st.3 - financing the merger

the acquirer decides how to pay for the target company:

cash - immediate payment, requires liquidity

shares [stock for stock] - acquirer issues shares instead of cash, diluting ownership

hybrid [cash + shares] - a mix of both methods

st.4 - valuation - determining how much to pay

the acquirer must determine the target’s value and any premium to offer

common valuation methods include:

discounted cash flow [DCF] - predicts future cash flows and discounts them to present value

market multiples - compares financial ratios [P/E, EV/EBITDA] with similar companies

comparable transactions - analyses prices paid in past mergers

st.5 - formulating the proposal or bid

the acquirer makes an offer:

friendly offer - negotiated with targets management and board

hostile takeover - offer is made directly to shareholders, bypassing management

motives for mergers - why do companies merge?

synergy - the main driver of mergers

synergy occurs when the combined entity is worth more than the sum of its individual parts

formula for synergy gain:

how is synergy achieved?

market power - increasing pricing ability due to reduced competition

economies of scale - cost savings from larger operations

internalising transactions - reducing dependency on third parties [e.g. a car company buying a tire manufacturer]

complementary resources - combining strengths [e.g. a tech company acquiring AI expertise]

entry to new markets - expanding into new regions/industries

tax benefits - using losses from one company to offset taxable income

risk diversification - spreading risk across different markets and business lines

bargain buying [acquiring an undervalued firm]

firms may merge because they identify a company that is worth more than its current market value

a true bargain exists if:

purchase price < PV of future cash flows

why might a firm be undervalued?

inefficient management - poor leadership is lowering profitability

misuse of resources/capital - the company has valuable assets but isnt utilising them effectively

undervalued shares - market sentiment has pushed share prices below intrinsic value

market inefficiency - investors may not have access to full information about the firm

financial distress - the company may be struggling with debt or liquidity issues, forcing a sale

managerial motives for mergers

not all mergers are done for shareholder value! sometimes, management acts in its own self interest

why would managers push for a merger?

higher remuneration - CEO compensation often increases after a merger

status and empire creation - bigger companies give CEOs more power and prestige

thrill of the chase - executives enjoy the competitive challenge of M&A

fame & legacy - CEOs want to be remembered for major deals

hubris [overconfidence] - some managers believe they can run the target company better even if the deal isn’t financially justified

survival - companies may merge to prevent themselves from being taken over

financial engineering - using mergers to manipulate financial metrics [e.g. increasing EPS by acquiring a lower P/E ratio company]

third party motives for mergers

sometimes, mergers are driven by external pressures rather business logic

who pushes companies companies to merge?

investment banks - earn large fees from M&A transactions

accountants and lawyers - gain business from structuring the deal

media and analysts - influence public perception of potential mergers

suppliers and customers - want stability in their supply chain

government and regulators - may encourage or prevent mergers for economic reasons

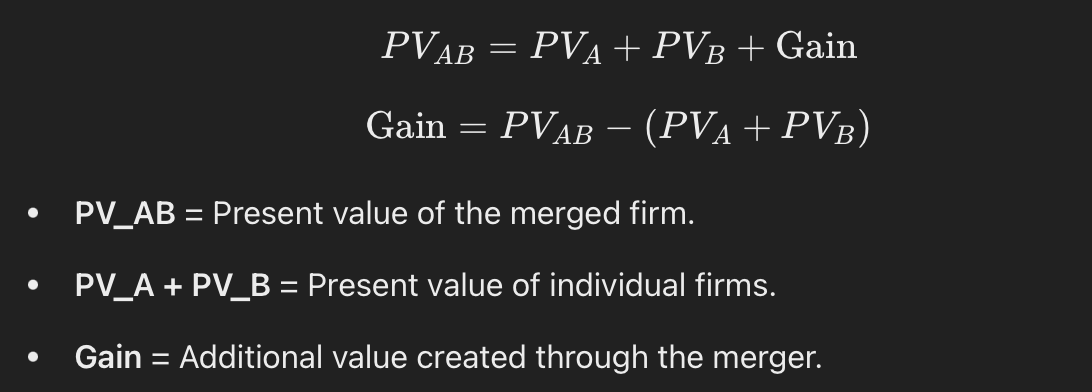

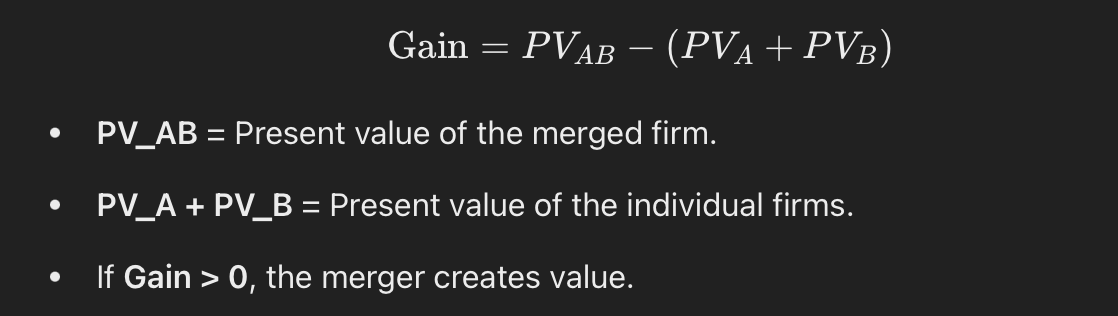

economic gains and costs in mergers

economic gains

a merger is justified if the combined firm is worth more than the individual firms due to synergy

formula for economic gain:

however, gains must be compared to costs before deciding to merge

economic costs - cash payment vs. share exchange

expect exam question on both!

cash payment method

the cost of the merger is the cash paid minus the standalone value of firm B [PVB]:

the NPV of the merger for firm A is calculated as:

key issues:

are the synergy gains large enough to offset the costs?

how are the gains divided between the acquirer and target?

is PVB accurately reflected in market value [MVB]

motives, premiums, and who benefits in a cash merger? [key issue no.4]

in a cash-paid merger, the acquiring firm (firm a) offers cash to buy the target (firm b), usually at a premium above firm b's market value (MVB). this premium reflects the acquirer’s belief in future synergy gains or strategic benefits.

key point:

the target shareholders often benefit the most — they receive a guaranteed cash premium and exit the firm, regardless of whether the merger succeeds in creating value

this outcome is influenced by the acquirer's motives:

if firm a is highly motivated (e.g. to gain market share, tech, or prevent a competitor from buying firm b), they may overpay, driving up the cost.

this increases the premium, benefiting firm bs shareholders more than firm a’s.

implication - even if the merger doesn't deliver expected synergies, the cost is already paid — firm a takes the risk, while firm b shareholders walk away with a gain.

share exchange method [stock for stock deal]

more complex because new shares are issued instead of cash

the cost of the merger is the value of the new shares issued minus the value of firm B [PVB]:

to determine the no. of new shares issued:

the new share price after the merger is:

key issues:

are firm A and firm B’s values reflected correctly in market prices?

how do stock price movements affect the deal [due to market reactions, rumours, announcements]?

does the efficient markets hypothesis hold, meaning all public info is already priced in?

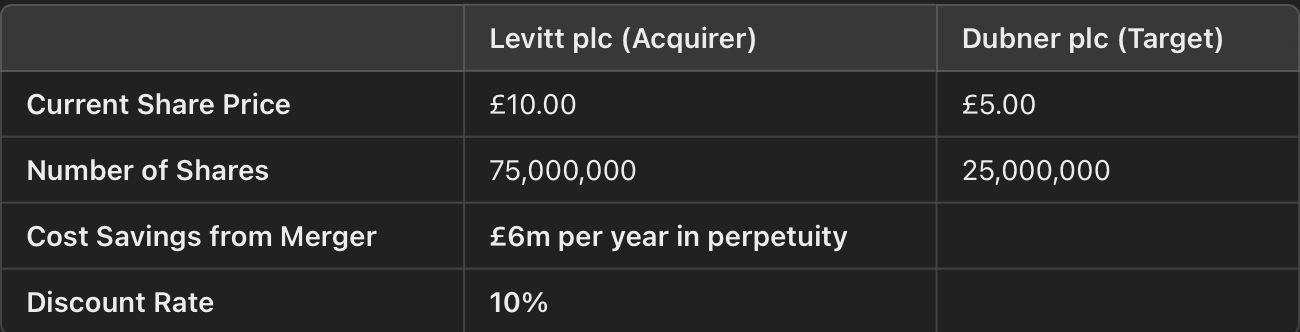

example - levitt plc acquiring dubner plc

cash offer - £7 per share

share exchange - 3 shares in levitt for 4 in dubner

PV [A] = levitt plc

PV [B] = dubner plc

calculate PV of merged firm [PV_AB]

PV[AB] = PV [A] + PV [B] + [annual cost savings/discount rate]

PV [A] = 75 mil. x £10 = 750 mil.

PV [B] = 25 mil. x £5 = 125 mil.

PV [AB] = 750 + 125 + [6/10%] = 935 mil.

gain = PV [AB] - [PV [A] + PV [B]] = 935 - [750 + 125] = 60 mil.

calculate the cost and NPV of the mergers under:

a. the cash offer

st.1 - calculate cost of cash payment

offer price = £7 per dubner share

total cost = [offer price per share x no. of shares] - PV [B]

cost = [7 × 25] - 125 = 50 mil.

st.2 - calculate NPV of cash offer

NPV = gain - cost = 60 - 50 = 10 mil.

since, NPV > 0, the cash offer is beneficial to levitt plc

b. share exchange offer

st.1 - determine new shares issued

exchange ratio - 3 levitt shares for every 4 dubner shares

new shares issued = [25/4] x 3 = 18.75 mil.

st.2 - determine new share price after merger

new share price = PV [AB]/total no. of shares in new firm

new share price = 935/[75 + 18.75] = 9.97

st.3 - calculate cost of new shares issued

cost = [new share price x new shares issued] - PV [B]

cost = [9.97 × 18.75] - 125 = 61.9375 mil.

st.4 - calculate NPV of share exchange

NPV = gain - cost = 60 - 61.94 = -1.9375 mil.

which is better?

acquiring companies must carefully assess whether a cash or share offer is more beneficial before proceeding with a merger

valuation

valuation sets a framework for negotiation, but the final price depends on bargaining

different approaches assess value based on:

discounted cash flow [DCF]

earnings based valuation

asset based valuation

important financial metrics to consider:

earnings per share of the acquiring firm

dividends per share for target shareholders

target firm’s asset value

target firm’s current stock price

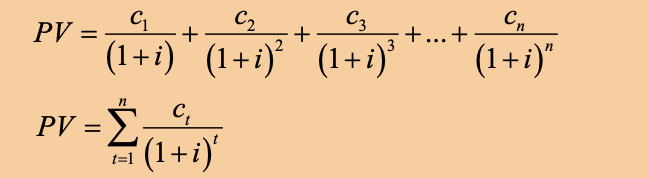

1 - valuation using DCF

DCF estimates how much future cash flows are worth today by applying a discount rate

formula:

key insights:

this method is best when cash flows are stable and predictable

however, it assumes the future can be accurately estimated, which is difficult in volatile industries

2 - maintainable earnings valuation

focuses on a company’s earnings stability over time

steps:

estimate maintainable earnings - take average of the past 5 yrs

establish an acceptable rate of return - find a similar company/industry benchmark

capitalise earnings to get valuation:

value = earnings/required return

since price/earnings [P/E] ratio = 1/required return, this is rewritten as:

value = earnings x [P/E]

key insights:

best for companies with stable earnings history

risk - assumes past earnings will continue into the future

3 - dividends based valuation

similar to earnings based valuation, but focuses on dividends instead of total earnings

steps:

estimate future dividends

establish required dividend yield from a comparable firm

value is given by:

value = dividend/dividend yield

key insights:

useful for valuing companies that pay consistent dividends [e.g. utilities, mature firms]

h/e some firms reinvest profits instead of paying dividends, making this approach less useful

4 - net asset value [NAV] approach

assesses company value based on its assets minus liabilities

NAV = total assets - total liabilities

if price > NAV:

the difference represents goodwill, brand value, or intangible assets

key insights:

best for asset heavy industries [e.g. real estate, manufacturing]

h/e it does not account for future profit potential

5 - super profits method

merges asset based and earnings based valuation

concept - the acquirer is paying for both assets and the ability to generate extra profits [super profits]

steps:

calculate net asset value

determine required return on those assets

calculate ex. profit based on maintainable earnings

find super profits:

super profits = ex. profits - [NAV x required return]

multiply super profits by a chosen number of yrs [e.g. 5 yrs]

final valuation:

value = NAV + [5 x super profits]

6 - berliner method [combination valuation approach]

averages both the maintainable earnings and net asset value

formula:

value = [maintainable earnings value + net asset value]/2

key insights:

balances between earnings potential and asset value

useful when both earnings and asset values are significant

h/e simple averaging may not reflect real economic value if one factor is more important then the other

example - valuation of nibali ltd.

given info:

no. of shares = 150 mil.

net assets = 75 mil.

earnings over last 5 yrs [in mil.]:

2010 - 14

2011 - 11

2012 - 12

2013 - 18

2014 - 25

last yrs dividend = £0.10 per share

industry metrics:

earnings yield [P/E ratio reciprocal] = 15%

dividend yield = 8%

super profits factor = 4 yrs

normal return on net assets = 15%

valuation using different methods

1 - maintainable earnings valuation

average past earnings

[14 + 11 + 12 + 18 + 25]/5 = 16 mil.

capitalised at earnings yield of 15% = 16/15% = 106.67 mil

per share value = 106.67/150 = 0.71

interpretation:

companys value is based on its ability to generate stable earnings

the estimated value per share = £0.71

2 - dividend based valuation

last yrs dividend = £0.10 per share

capitalised at dividend yield of 8%

value per share = 0.10/8% = 1.25

interpretation:

if dividends continue at the same rate, an investor expecting an 85 return would value each share at £1.25

3 - super profits valuation

normal profit calculation:

industry return on assets = 15% of NAV

normal profit = 75 × 15% = £11.25 mil.

super profit calculation:

super profit = maintainable earnings - normal profit

super profit = 16 - 11.25 = 4.75 mil

capitalising super profits over 4 yrs:

4.75 × 4 = 19 mil.

total value [NAV + super profits]:

75 + 19 = 94 mil.

per share value:

94/150 = 0.6267

interpretation:

this approach values the company as the sum of its assets plus the ability to generate extra profits

estimated value per share = £0.63

4 - berliner method [average of earnings and asst based valuation]

NAV based value = £0.50 per share

maintainable earnings value = £0.71 per share

berliner value:

[0.5 + 0.71]/2 = 0.6056

interpretation:

the berliner method balances earnings potential and asset value

final estimated value per share = £0.61

bidding and defence tactics in mergers and acquisitions

bidding tactics - how to make successful takeover bid

once the acquirer has decided to make a bid, they must structure it strategically to:

make the offer attractive to the target company’s shareholders

minimise costs for the acquiring firm

increase the chances of shareholder acceptance

key steps in a takeover bid:

hire advisors or a syndicate

investment banks, legal teams, and financial advisors help structure the bid and negotiate terms

offer a premium

shareholders will only sell if they receive an attractive price above the current market value

the premium must be high enough to persuade shareholders but low enough to ensure profitability for the acquirer

acquire a “toe hold“ [strategic shareholding before the offer]

the acquiring firm buys a small percentage of the target company’s shares before making a formal bid

this gives early influence and reduces the overall cost of the takeover if share prices rise after the offer

make the offer and seek shareholder approval

the acquirer needs enough shareholders to accept the bid to take control

in hostile takeovers, the acquirer bypasses management and appeals directly to shareholders

defence tactics - how to resist a takeover

if a company is targeted for acquisition, its board of directors has duty to act in the best interests of shareholders

some shareholders may want to accept the offer, while other may want to resist

the board consults with financial advisors to determine whether the bid fairly values the company

if shareholders choose to fight the bid, they can use the pre-bid, post bid, or more aggressive defence tactics

pre bid defence tactics [before a takeover offer is made]

the target company takes preventative measures to make itself a more difficult or expensive acquisition target

key pre-bid defence strategies:

external vigilance (public Image & valuation)

strengthen the firm’s public image to increase perceived value.

if the company looks more valuable and successful, it becomes more expensive to acquire.

monitor the share register

keep an eye on who is buying shares—an increase in purchases from an unknown party could indicate a hostile bidder.

placing shares in friendly hands

encourage company pension funds, employees, or loyal investors to buy shares.

this makes it harder for a hostile bidder to gain a controlling stake.

strategic defensive investments

The target company buys a significant shareholding in another “friendly” company, which then buys shares in the target firm.

This creates a cross-ownership structure, making a takeover more complex.

post bid defence tactics [after a takeover offer is made]

once a bid is public, the target company can fight back by attacking the bid’s credibility or making itself less attractive

key post bid defence strategies:

attack the bid’s logic & bidder’s reputation

publicly criticise the acquiring firm’s financial stability, management, or long-term plans.

convince shareholders that the offer undervalues the company or the bidder is not capable of running the firm effectively.

mobilise external pressure

encourage trade unions, politicians, regulators, suppliers, and customers to oppose the takeover.

if a company is important to national security or employment, governments may intervene.

revise profit forecasts

if the target company announces a stronger future earnings outlook, its share price may rise, making the bid less attractive.

however, making optimistic forecasts is easy—actually achieving them is harder

pac - man strategy

the target company launches a counter-bid to acquire the bidder instead

this is rare but has been used successfully in the past

more aggressive defence tactics

some defence tactics are more aggressive and may not always be in the best interests of shareholders

key aggressive defence tactics:

white knight strategy

the target firm seeks a more friendly buyer (a White Knight) who will acquire the company instead of the hostile bidder.

sometimes, a friendly company merges with the target firm to block the takeover.

crown jewels strategy

the target sells off its most valuable assets to make itself less attractive to the bidder.

risk: This may weaken the company permanently.

golden parachutes

the target company creates expensive exit packages for top executives if the firm is taken over.

this raises the cost of acquisition for the bidder.

poison pills

various strategies that make the takeover extremely expensive or difficult for the bidder.

examples:

flip-in: allows existing shareholders (except the acquirer) to buy more shares at a discount.

flip-over: target shareholders get the right to buy acquirer shares at a discount if the takeover happens.

shareholder rights plan: grants extra voting rights to existing shareholders, making it harder for the bidder to gain control.

greenmail & arbitrageurs

the target company buys back its own shares at a premium from the hostile bidder to force them to withdraw.

risk: This benefits the hostile bidder financially, but weakens the company’s balance sheet.