Chapter 1 - Financial Accounting and Business Decisions

Forms of Business Organizations

Sole Proprietorship: A business owned and operated by a single individual, offering simplicity and complete control.

Partnership: A business owned by two or more individuals who share profits and responsibilities.

Corporation: A legal entity that is separate from its owners, providing limited liability protection and the ability to raise capital through stock issuance.

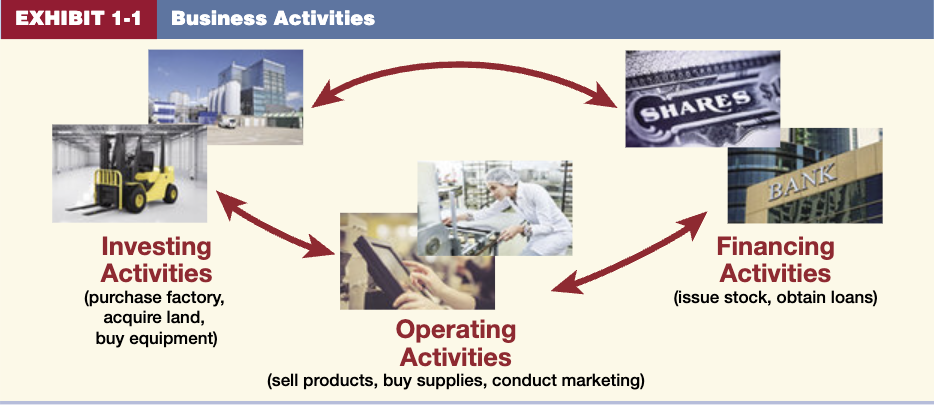

Financing Activities.- How do companies acquire money for their operations to run?

Debt Financing- involves borrowing money from sources such as a bank by signing a note payable or directly by investors or by issuing bonds payable

Equity Financing- involves selling shares of stock to investors in exchange for ownership stakes in the company, allowing businesses to raise capital without incurring debt.

Investing Activities- how do companies purchase long-term resources?

ex: land, buildings, and equipment

involves the acquisition and disposition of factories, office furniture, computer and data systems, delivery vehicles, and other items that will be used to carry out the company’s business plans

Operating activities- What are companies’ date-to-day activities in producing and selling a product or providing a service?

are critical for a business because if a company is unable to generate income from its operations it is very likely that the business will fail.

External Users of Accounting

The process of preparing these publicly available financial statements is referred to as financial accounting.

The process of generating and analyzing such data is referred to as managerial accounting.

Ethics and Accounting

ethics deals with the values, rules, and justifications that govern one’s way of life

The American Institute of Certified Public Accountants (AICPA) has a professional code of ethics to guide the conduct of the members of the CPAs

The Institute of Management Accountants has written standards of ethical conduct for accountants employed in the private sector.

General Accepted Accounting Principles (GAAP) are guides to action that can lead to change over time

U.S Securities and Exchange Commission (SEC) primary focus is to regulate the interstate sale of stocks and bonds

Public Company Accounting Oversight Board ( PCAOB) approves auditing standards, known as generally accepted auditing standards (GAAS)

International Accounting Standards Board (IASB) has taken the lead in formulating international accounting principles.

Financial Statements

4 Basic Financial Statements: the balance sheet, the income statement, the statement of stockholder’s equity, statement of cash flows.

The Balance sheet is a listing of a firm’s assets, liabilities, and stockholder’s equity as of a given date, usually at the end of the accounting period.

The accounting equation states the sum of a business’s economic resources must equal the sum of any claims on those resources

Resources of a Company = Claims on Resources

Assets = Liability + Stockholders’ Equity

Assets: are the economic resources of a business that can be expressed in monetary terms. it represents a probable future economic benefit to a business.

examples: cash, inventory, supplies, land, building’s , equipment

Liabilities: are obligations or debts that a business must pay in cash or in goods or in services at some future time as a consequence of past transactions or past events.

examples: Notes Payable, Wages Payable, Accounts Payable

- Notes Payable : business can borrow money and sign a promissory note agreeing to repay the borrowed money in 6 months. Business reports this as Notes payable

- Wages Payable : owes wages to employees for work already performed

- Accounts Payable: if a business owes money to various suppliers for goods and services already provided

Stockholders’ Equity: refer to the ownership (stockholder claims) on the assets of a business.

- Represent a residual claim ( it is a claim on assets of a business that remain after all liabilities to creditors have been satisfied.

AKA: Net Assets

Assets- Liabilities = Stockholders’ equity = net assets

Income Statement