Ch.1

Learning Objective 1:

Forms of business organizations

Users and uses of financial info.

Ethics in financial reporting

Vocab:

Sole Proprietorship: Owned by one person, simple to set up, owner-controlled, and tax advantages.

Partnership: By two or more person, simple to establish, shared control, broader skills and resources, tax advantages.

Corporation: A separate legal entity owned by stockholders, investors receives shares of stock to indicate their ownership claim. Shares of stock are easy to sell (transfer ownership). Easier to raise funds. No personal liability.

Accounting: Information system that identifies, records, and communicates the economic events of an organization to interested users.

Internal users: Managers who plan, organize, and run a business. Includes marketing managers, production supervisors, finance directors, and company officers.

External users: Investors (Owners) use to make decisions to boy, hold, or sell stock. Creditors (suppliers) evaluate risks of selling on credit or lending money.

Sarbanes-Oxley Act (SOX): Regulations passed by Congress to reduce unethical corporate behavior.

Notes:

Learning Objective 2:

Financing Activities

Investing Activities

Operating Activities

Vocab:

Financing: It takes money to make money

Liabilities: Amounts owed to creditors in the form of debts and other obligations Ex: Notes payable, bonds payable. Interest payable, wages payable, sales taxes /property taxes payable, and income taxes payable.

Common stock: The total amount paid in by stockholders for the shares they purchase.

Dividends: Cash payments to stockholders, representing a portion of a company’s earnings.

Investing: The purchases of the resources a company needs in order to operate.

Assets: Resources owned by a business Ex: Cash, PPE, Accounts Receivable, Supplies, Inventory

Operating: Selling and making products/services

Revenue: The increase in assets or decrease in liabilities resulting from the sale of goods or the performance of services in the normal course of business. Ex: Sales, service, and interest revenues.

Expenses: The cost of assets consumed or services used in the process of generating revenues. Ex: Salaries, rents, utilities, costs of good sold, selling, marketing, administrative, interest, amd income tax.

Net Income: When revenues exceed expenses

Net Loss: When expenses exceed revenues.

Notes:

Financing Act.

The two primary sources of outside funds for corporations are borrowing money (debt financing) and issuing (selling) shares of stock in exchange for cash (Equity financing).

Creditors claims must be paid before stockholders’ claims. If you loan money to a company, you are one of its creditors. Stockholders have no claim on corporate cash until claims of creditors are done.

Investing Act.

A growing company purchases many resources such as computers, delivery trucks, furniture, and buildings.

Operating Act.

Learning Objective 3:

Income Statement

Retained earnings statement

Balance sheet

Statement of cash flows

Interrelationships of statements

Other annual report elements

Vocab:

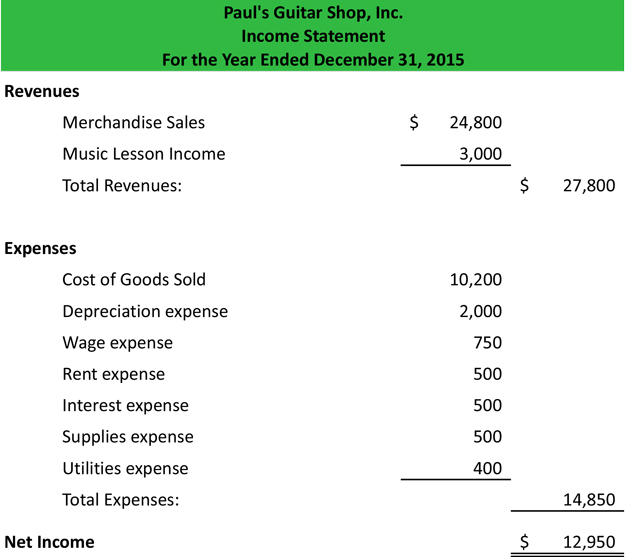

Income statement: To show how successfully your business performed during a period of time, you report its revenue and expenses in an income statement

Retained Earnings Statement: To indicate how much of pervious income was distributed to you and the other owners of your business in the form of dividends, and how much was retained in the business to allow for future growth

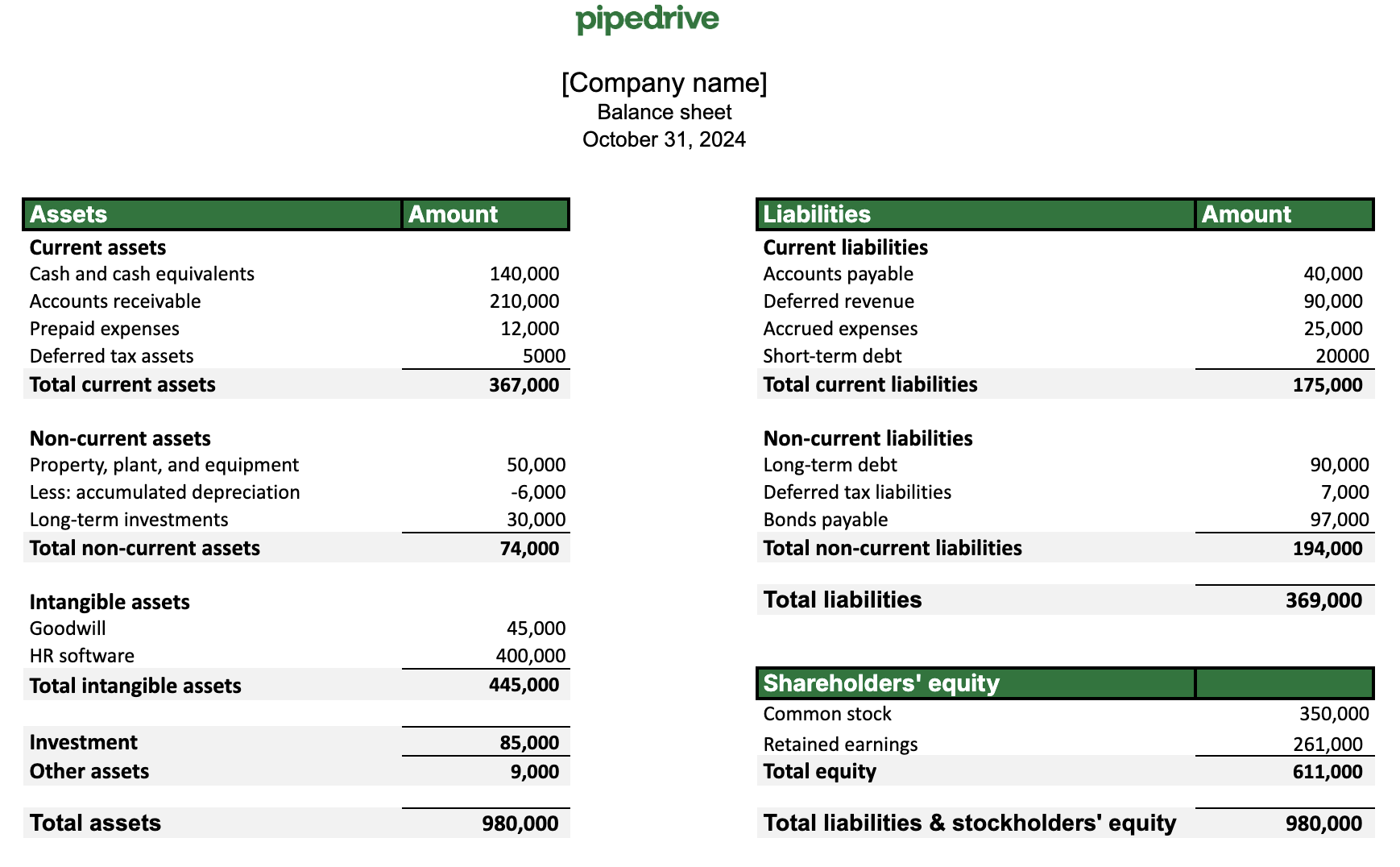

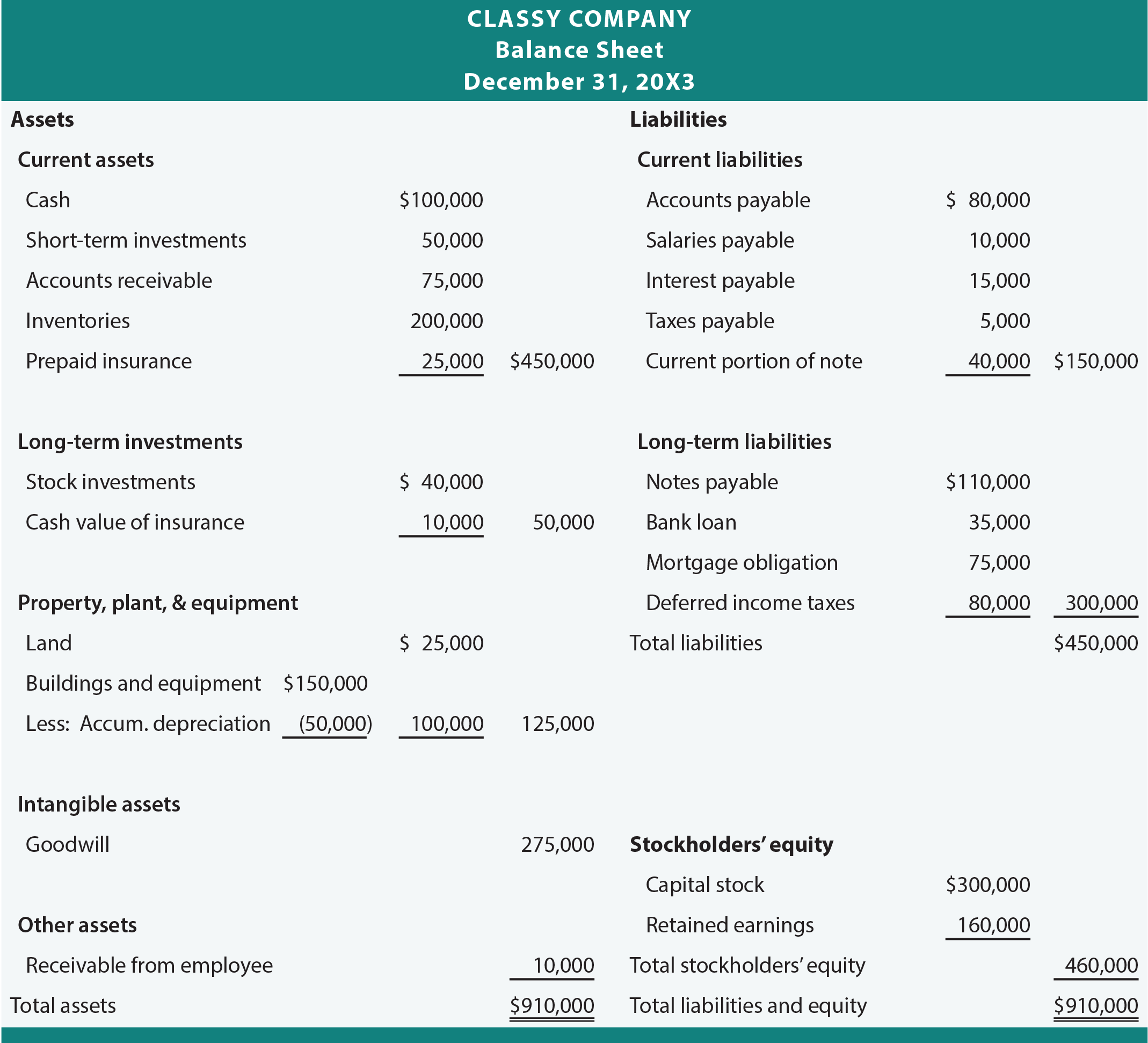

Balance sheet: To present a picture of a point in time of what your business owns (its assets) and what it owes (its liabilities).

Statement of cash flow: To show where your business obtained cash during a period of time and how that cash was used.

Annual report: A report prepared by corporate management that presents financial info. including fin. statements, a management discussion and analysis section, notes, and an independent auditor’s report.

Auditor’s report: A report prepared by an incident outside auditor stating the auditor’s opinion as to the fairness of the presentation of the financial position and results of operations and their conformance with generally accepted accounting principles.

Management discussion and and analysis (MD&A): A section of the annual report that presents management’s views on the company’s ability to pay near-term obligations, its ability to fund operations and expansion, and it results of operation.

Notes:

Income statement info: Lists first revenue followed by it expenses. Determines net loss or net income. Predicts future earnings. When a bank loans money to a company, it believes that it will be repaid in the future. Amounts received from issuing stock are not revenues, and amounts paid out as dividends are not expenses. They are not reported here.

Retained Earnings Statement Info: The net income retained in the corporation. Shows the amounts and causes of changes in retained earnings for a specific time period. Beginning retained earnings amount appears on the first line of the statement. Than adds net income and deducts dividends to determine the retained earnings at the end of the period. If a company has a net loss, it deducts (rather than adds) that amount in the retained earnings statement. Helps users determine the company’s policy toward dividends and growth.

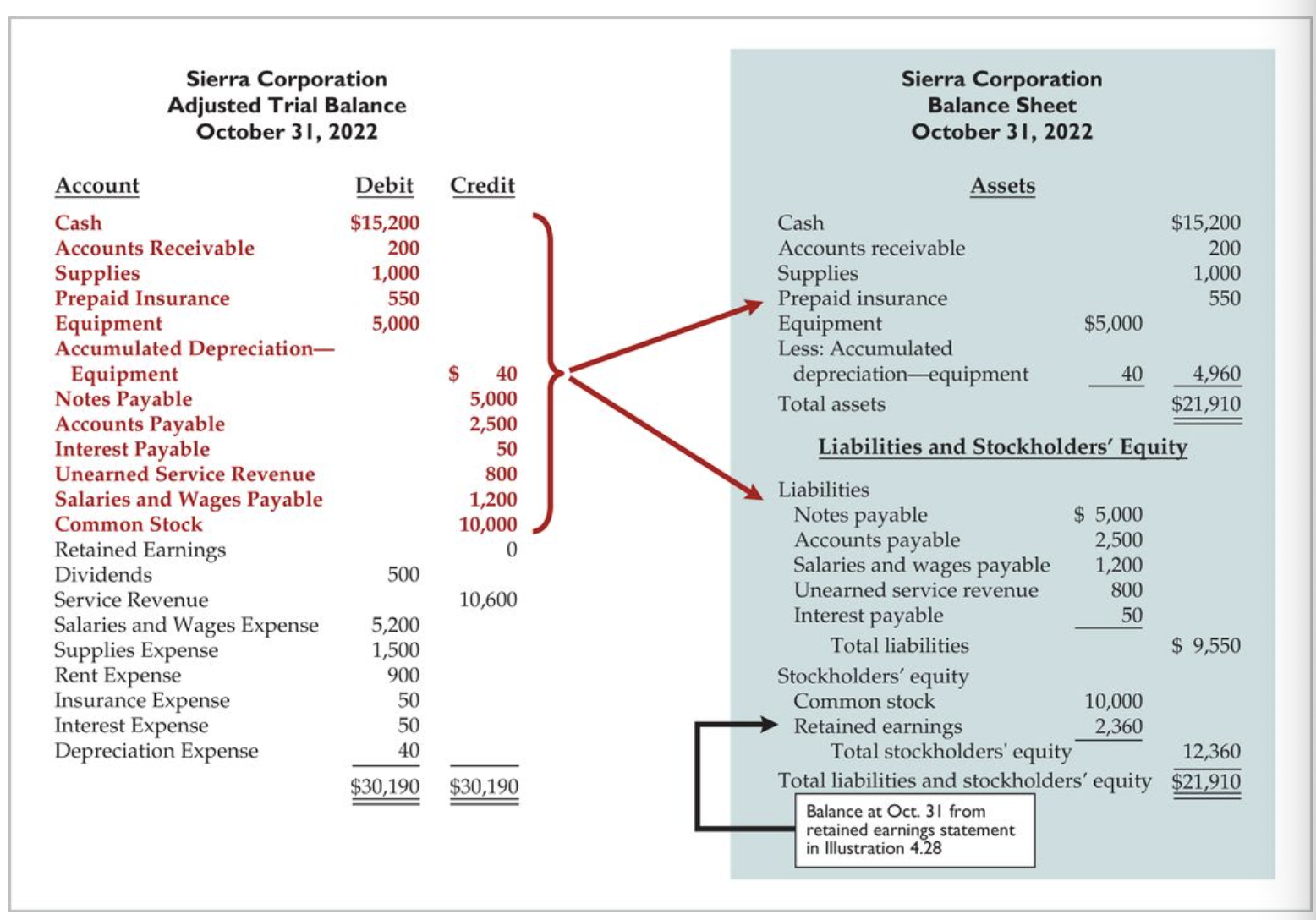

Balance Sheet Info: reports assets at a specific point in time. Puts them into two categories, claims of creditors (liabilities) and claims of owners (stockholders’ equity). Users determine if the company relies on debt or stockholders’ equity to finance its assets. Also how likely they will be repaid, whether cash on hand is sufficient for immediate cash needs. Assets must balance with the claims to assets. A specific date. Assets are listed first and in order to how quickly they can be converted to cash. Followed by liabilities and stockholders’ equity (common stock and retained earnings).

Assets= Liabilities + Stockholders’ Equity

Chapter 2: A Further Look at Financial Statements

Learning Objective 1:

Current Assets

Long-term investments

Property, Plant, and Equipment

Intangible assets

Current liabilities

Long-term liabilities

Stockholders’ equity

Vocab:

Current Assets: Assets that a company expects to convert to cash or use up within one year or its operating cycle, whichever is longer.

Operating cycle: A company is the average time required to go from cash to cash in producing revenue- to purchase inventory, sell it on account, and then collect cash from customers.

Long-term investments: investments in stocks and bonds of other corporations that are held for more than one year, long-term assets such as land or buildings that a company is not currently in its operating activities, long-term notes receivables

Property, Plant, and Equipment: Assets with relatively long useful lives that are currently used in operating the business. Includes land, buildings, equipment, delivery vehicles, and furniture.

Depreciation: The allocation of the cost of an asset to a number of years. Accumulated depreciation shows the total amount of depreciation that the company has expensed thus far in the asset’s life.

Intangible assets: Do not have physical substance and yet often are very valuable. (Goodwill, patents, copyrights and trademarks or trade names that give the company exclusive right of use for a specified period of time.

Current Liabilities: Obligations that the company is to pay within the next year or operating cycle. Includes accounts payable, salaries and wages payable, notes payable, interest payable, and income taxes payable.

Stockholders’ Equity: Common stock and retained earnings

Notes:

Classified balance sheet: groups together similar assets and similar liabilities, using a number of standard classifications and sections. Assets: Current assets, long-term investments, PPE, Intangible assets. Liabilities and Stockholders’ Equity: Current liabilities, long-term liabilities, and stockholders’ equity. Helps in whether the company has enough assets to pay its debts as they come due, and the claims of short and long-term creditors on the company’s total assets.

Order of assets: Cash, short-term investments, accounts receivable, inventories, and prepaid expenses and other current assets.

Order of Liabilities: Current, Long-term (long-term debt), including notes payable, lease liabilities, and pension liabilities.

Learning Objective 2:

Ratio analysis

Using the income statement

Using a classified balance sheet

Using the statement of cash flows

Vocab:

Ratio analysis: expresses the relationship among selected items of financial statement data

Ratio: Expresses the mathematical relationship between one quantity and another.

Profitability Ratio: Measure the income or operating success of a company for a given period of time. Earnings per share, measure the operating success of a company for a given period of time.

Liquidity Ratios: Measure short-term ability of the company to pay its maturing obligations and to meet unexpected needs for cash

Solvency Ratios: Measure the ability of the company to survive over a long period of time.

Earnings per share: Measures the net income earned on each share common stock. Helps users compare a company’s performance with that of previous years.

Liquidity: Its ability to pay obligations expected to become due within the next year or operating cycle.

Working Capital: The difference between the amounts of current assets and current liabilities. Working Capital = Current Assets - Current Liabilities. If positive, the company will pay its liabilities.

Liquidity ratios: Measure the short-term ability of the company to pay its maturing obligations and to meet unexpected needs to cash.

Current Ratio: Computed as current assets divided by current liabilities. Helps users determine if a company can meet its near-term obligations. More dependable

Solvency: Its ability to pay interest as it comes due and to repay the balance of a debt at its maturity.

Debt to assets ratio: One measure of solvency. By dividing total liabilities (both current and long-term) by total assets. Measures the percentage of total financing provided by creditors rather than stockholders.

Debt financing: Is more risky than equity financing because dent must be repaid at specific points in time, whether the company is performing well or not. Thus, the higher the percentage of debt financing, the riskier the company. The higher the percentage of total liabilities (debt) to total assets, the greater the risk that company may be unable to pay its debt as they come due.

Notes:

Debt to Assets: This means a company with a high debt to assets ratio has a lower equity “buffer” available to creditors if that company becomes insolvent. Helps users determine if a company can meet its long-term obligations.

Learning Objective 3:

The standing-setting environment

Qualities of useful information

Assumptions in financial reporting

Principles in financial reporting

Cost constraint

Vocab:

International Accounting Standards Board (IASB) An accounting standard-setting body that issues standards adopted by many countries outside of the United States.

International Financial Reporting Standards (IFRS) Accounting standards, issued by the IASB, that have been adopted by many countries outside of the United States.

Securities and Exchange COmmision (SEC): The agency of the US government that oversees US financial markets and accounting standard-setting bodies.

Public Company Accounting Oversight Board (PCAOB): The group charged with determining auditing standards and reviewing the performance of auditing firms.

Generally accepted accounting principles (GAAP): A set of accounting standards that have substantial authoritative support and which guide accounting professionals.

Financial Accounting Standards Board (FASB): The primary accounting standard-setting body in the US.

Relevance:The quality of info that indicates the information makes a difference in a decision.

Materiality: Whether an item is large enough to likely influence the decision of an investor or creditor.

Faithful representation: Information that is complete, neutral, and free from error

Comparability: Ability to compare the accounting principles and methods from year to year within a company

Consistency: Use of the same accounting principles and methods from year to year within a company.

Verifiable: The quality of information that occurs when independent observers, using the same methods, obtain similar methods.

Understandability: Information presented in a clear and concise fashion so that users can interpret it and comprehend its meaning.

Historical cost principle: An accounting principle that states that companies should record assets at their cost.

Fair value principle: Assets and liabilities should be reported at fair value.

Full disclosure principle: Accounting principle that dictates that companies disclose circumstances and events that make difference to statement users.

Cost Constraint: Constraint that weighs the cost that companies will incur to provide the information against the benefit that financial statement users will gain from having the information available.

Notes:

Chapter 3:

Learning Objective 1:

Accounting transactions

Analyzing transactions

Summary of transaction

Vocab:

Accounting info system: The system of collecting and processing transaction data and communicating financial info to decision-makers.

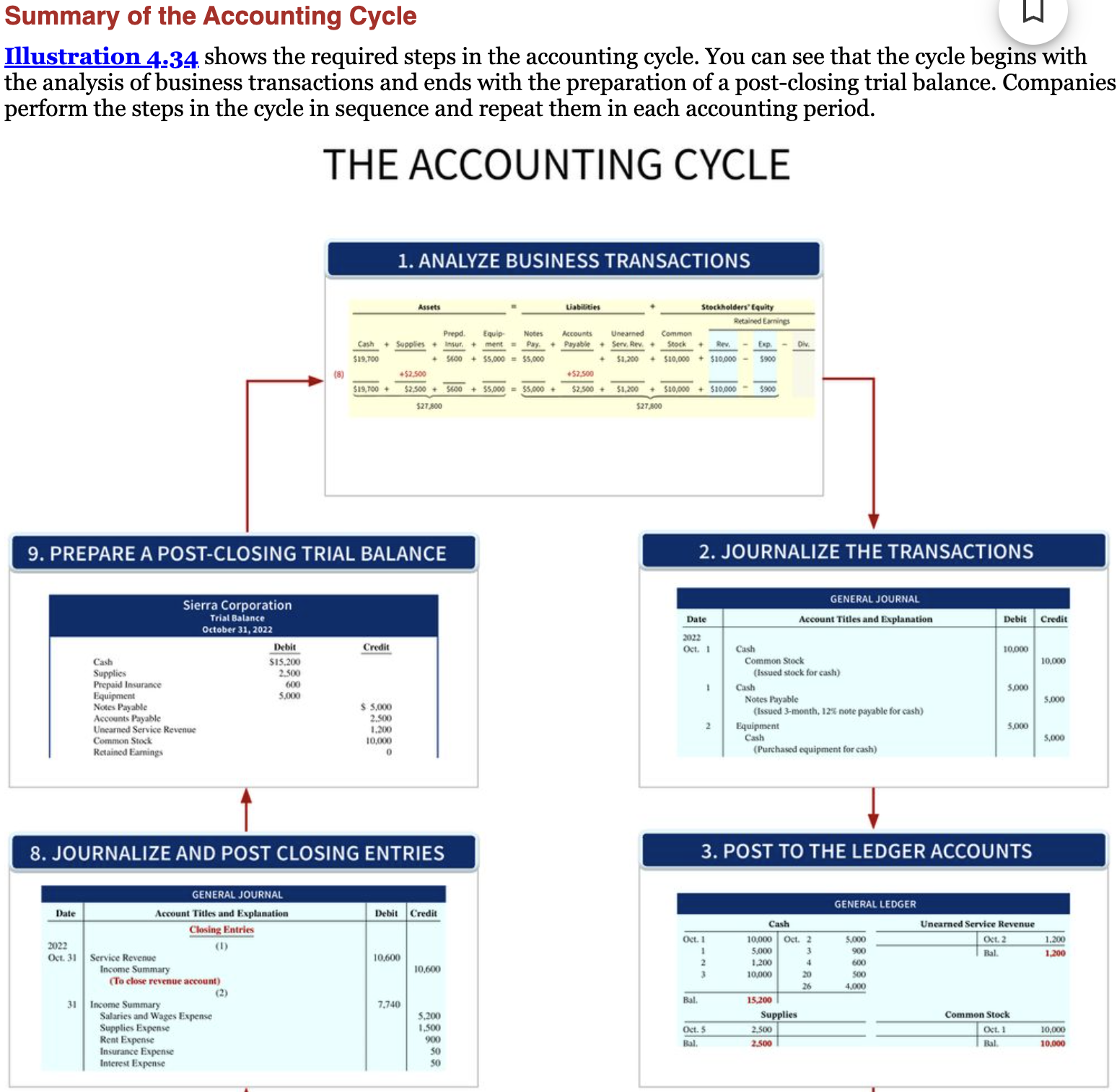

The accounting cycle: Analyzing business transactions, journalize, post, trial balance, adjusting entries, adjusted trial balance, financial statements, closing entries, and post-closing trial balance.

Accounting transactions: Not all events are recorded and reported in the financial statement but it is when assets, liabilities, or stockholders’ equity items change as a result of some economic event.

Transaction analysis: The process of identifying the specific effects of economic events on the accounting equation.

Notes:

The accounting equation must always stay balance. Double sided effect on the equation. For example, a decrease in another asset=increase in a liability or = increase in stockholders’ equity.

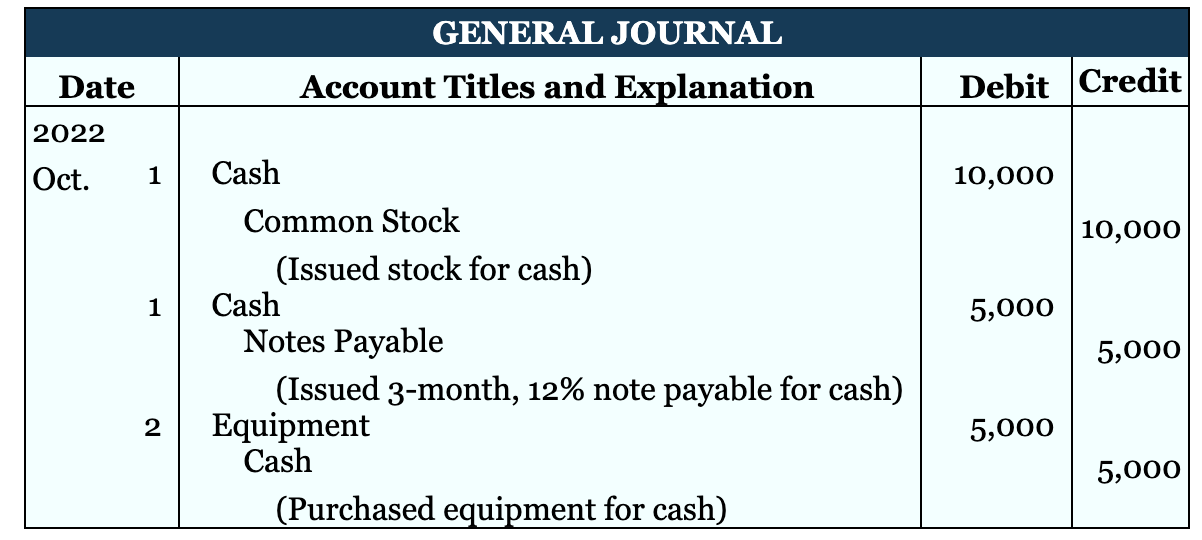

Example: “if a company purchases a computer for $10,000 by paying $6,000 in cash and signing a note for $4,000, one asset (equipment) increases $10,000, another asset (cash) decreases $6,000, and a liability (notes payable) increases $4,000.”

Examples of image up ahead:

10,000 is invested in the business by investors in exchange for 10,000 of common stock.

Borrowed 5,000 from comp. signing a 3-months, 5,000 note payable. results in equal increase in assets and liabilities.

Purchased equipment for 5,000, resulted in equal increase and decrease in assets.

Received 1,200 cash advance from client. Asset. It does not record revenue until it has performed. In this case, it does, but if it didn’t it would be under liability.

Received 10,000 in cash (asset). Revenue increases stockholders’ equity. Results in both asset and stockholders’ Equity increase.

Accounts receivable is when revenues is increase when services are performed but the cash has not been received so this would fall under Assets and Stockholder. Later, when the cash is collected, we deduct from the accounts receivable and add the cash so both cancel out.

Paid its office rent in cash 900, results in a decrease in assets and stockholder. Treated as an expense.

Paid 600 for one-year insurance policy that will expire next year. Payments of expenses will benefit more than one accounting period are identified as assets called prepaid expenses or prepayments. Results in no change in assets.

Purchased supplies on account. Means comp. receives goods that will pay for on a later date. Increase in assets and a liability (Accounts payable).

Hiring new employees does not change since they start on a different date.

Paid 500 cash dividend. Dividends are reductions of stockholders’ equity but not an expense. A dividend is a distribution of the company’s assets to its stockholders.

When empolyees have worked for two week, earning 4,000, Salaries and wage expense is an expense that reduces stockholders’ equity. Both assets and equity go down.

Summary of transactions:

Learning Objective 2:

Debits and Credits

Debit and Credit procedures

Stockholders’ Equity

Summary of debit/credit rules

Vocab:

Account: An individual accounting record of increases and decreases in a specific asset, liability, stockholders’ equity, revenue, or expense item.

T-Account: 1. the title of the account. 2. a left or debit side. 3. a right or a credit side.

Debit: The left side of the account

Credit: The right side of the account

Double-entry system: The two sided effect of each transaction is recorded in appropriate accounts.

Notes:

T-account:

When you make an entry to either side, it is called crediting or debiting.

When debit exceeds credit, debit balance. When credit exceeds debit, credit balance.

Record the increase in cash (asset) in debit and the decrease in cash in credit. The balance is determined by netting the two sides (subtracting one amount from the other). For each transaction, debits must equal credits.

Record the decrease in liabilities, increase in assets. Vice Versa.

Record the decrease in common stock (debit), increase in common stock. (credit).

Record the decrease in retained earnings (debits), increases retained earnings (credit)

Dividends reduce equity, increase in the dividends accounts are recorded with debits.

Revenues accounts are increased by credits and decreased by debits. Expenses decrease stockholders’ equity. Expense accounts are increased by debits and decreased by credits. Revenue (credit). Expenses (Debit).

Summary of Debit/Credit Rules:

Learning Objective 3:

The recording process

The journal

Vocab:

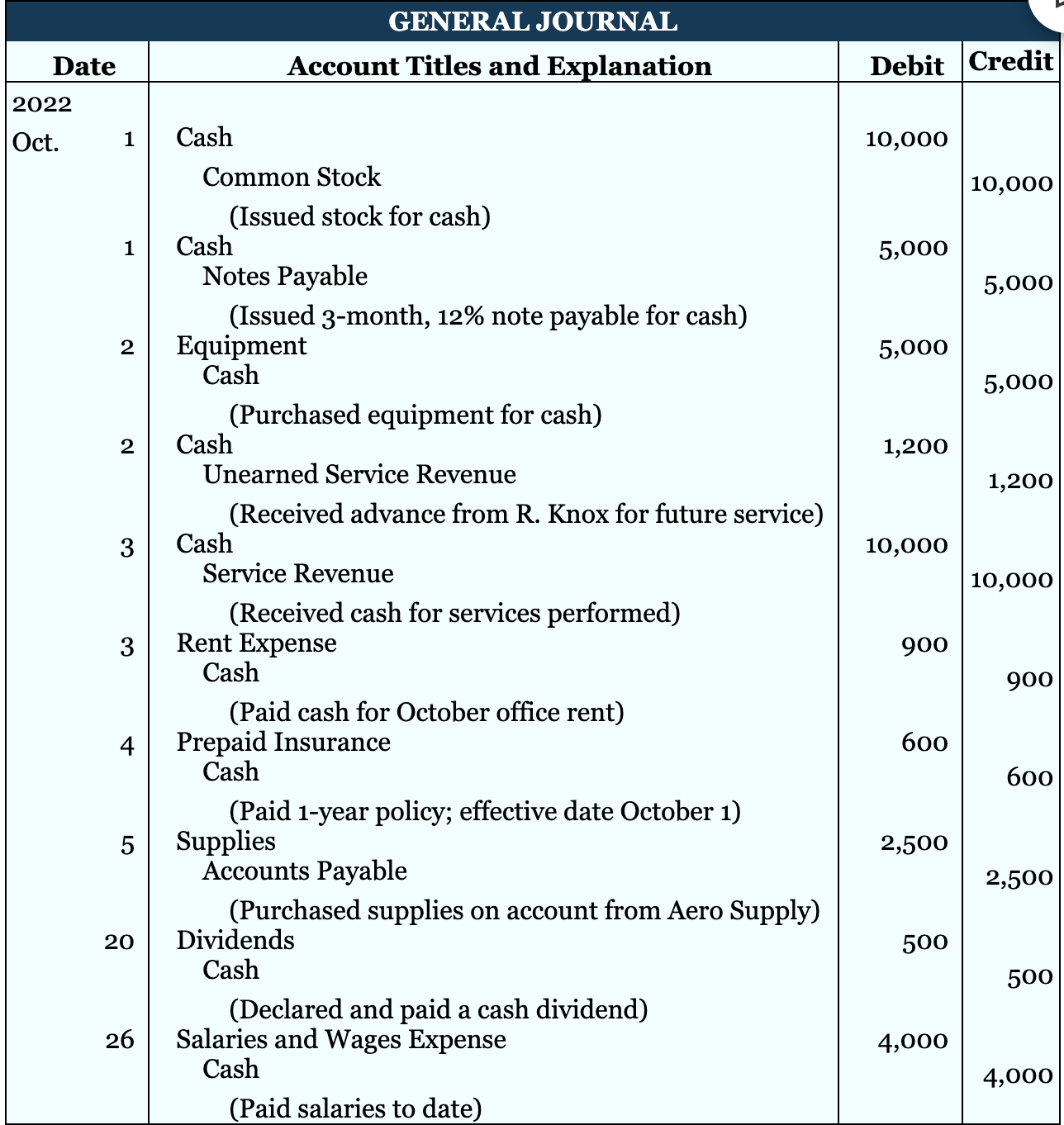

The recording process: Analyze each transaction in terms of its effects on the accounts. 2. Enter the transaction information in a journal. 3. Transfer the journal information to the appropriate accounts in the ledger.

Journal: Transactions are recorded in order in a journal before they are transferred to the accounts.

General journal: It discloses in one place the complete effect of a transaction. 2. It provides a record of transactions. 3. It helps to prevent or locate errors because the debit and credit amounts for each entry can be readily compared.

Notes:

The date of the transaction is entered in the date column.

The account to be debited is entered first at the left. The account to be credited is then entered on the next line, indented under the line above. The indentation differentiates debits from credits and decreases the possibility of switching the debit and credit amounts.

the amounts for the debits are recorded in the debit (left) column, and the amounts for the credits are recorded in the credit (right) column.

The brief explanations of the transaction is given.

Learning Objective 4:

The ledger

Chart of accounts

Posting

The recording process illustrated

Summary illustration

Vocab:

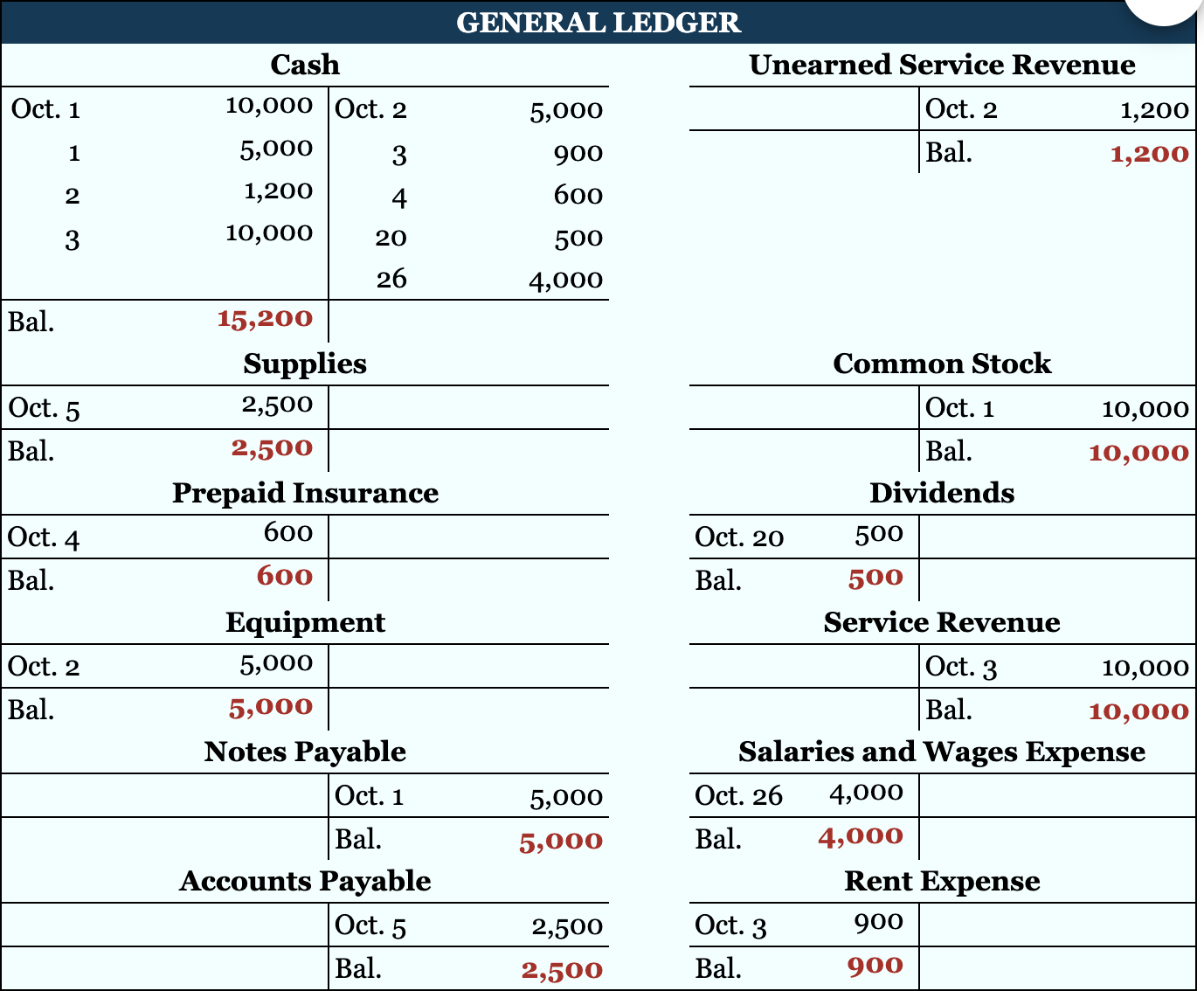

Ledger: The records of all accounts maintained by a company and their amounts. Provides the balance in each of the accounts as well as keeps track of changes in these balnces.

General ledger: Contains all the assets, liability, equity, revenue, expense.

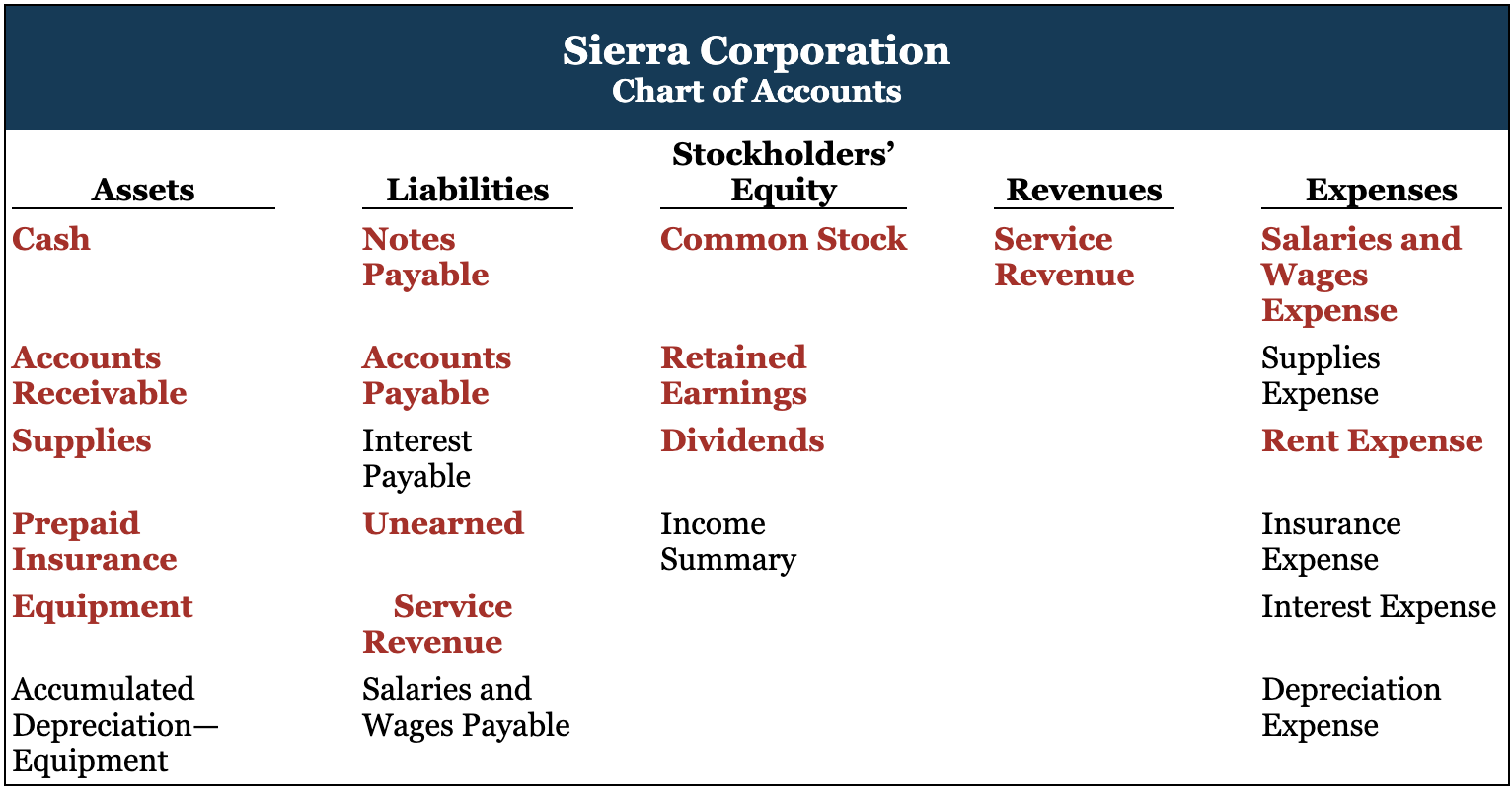

Chart of accounts: A list of the names of a company’s accounts.

Posting: The procedure of transferring jounrnal entry amounts to ledger accounts. This phase of the recording process accumulates the effects of journalized transactions in the individual accounts.

Notes:

General Ledger:

Chart of Accounts:

Posting:

I the ledger, enter the appropriate columns of the debited accounts the date and debit amount

Enter the appropriate columns of the credited accounts the date and credit amount.

The purpose of transaction analysis is first to identify the type of account involved and then to determine whether a debit or credit to account is required.

Learning Objective 5:

Limitations of a trial balance

Vocab:

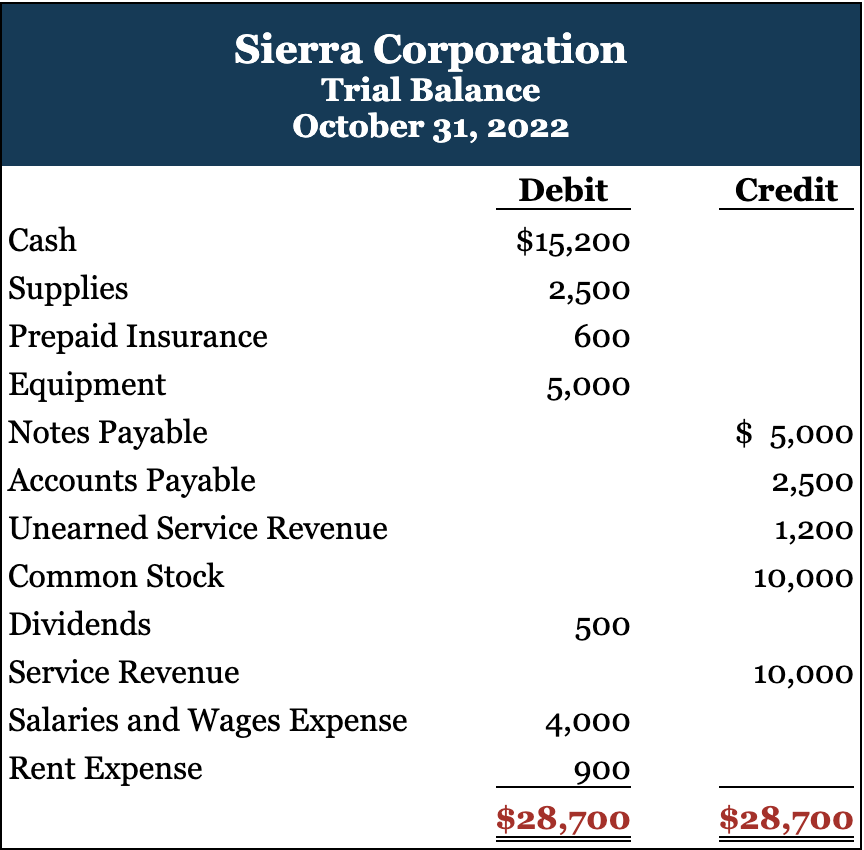

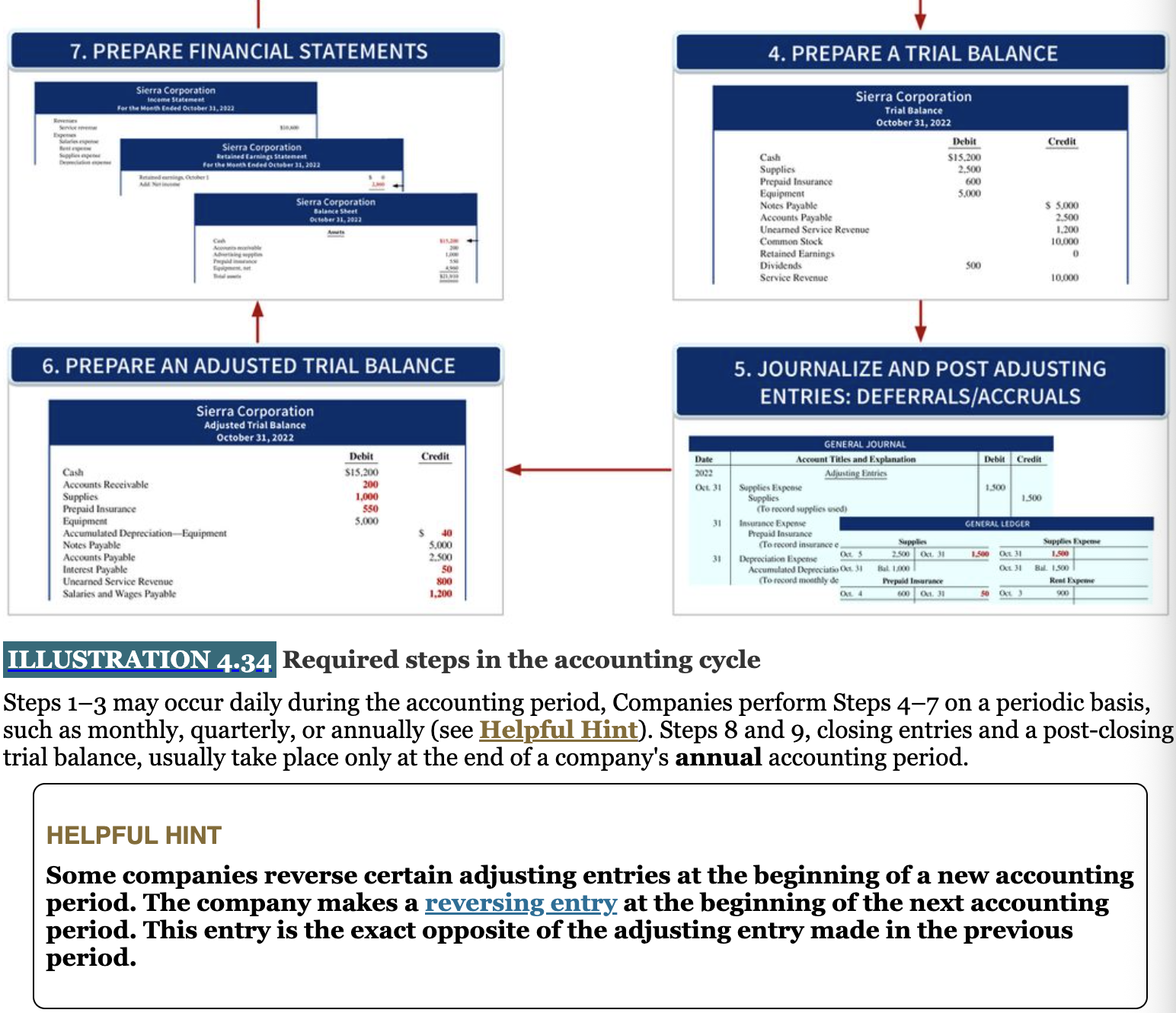

Trial balance: Lists accounts and their balances at a given time. At the end of an accountinf period. Debits are listed left and credit right. Should prove both are equal.

Notes:

Preparing the trail balance:

List the account titles and their balances.

total the debit column and total credit column

Verify the quality of the two columns.

Chapter 13: Financial Analysis: The Big Picture

Learning Objective 1

Sustainable income

Quality of earnings

Vocab:

Sustainable income: The most likely level of income to be obtained by a company in the future. Differs from actual net income by the amount of unusual revenues, expenses, gains, and losses included in the current year’s income. Helps them derive an estimate of future earnings without the “noise” of unusual items.

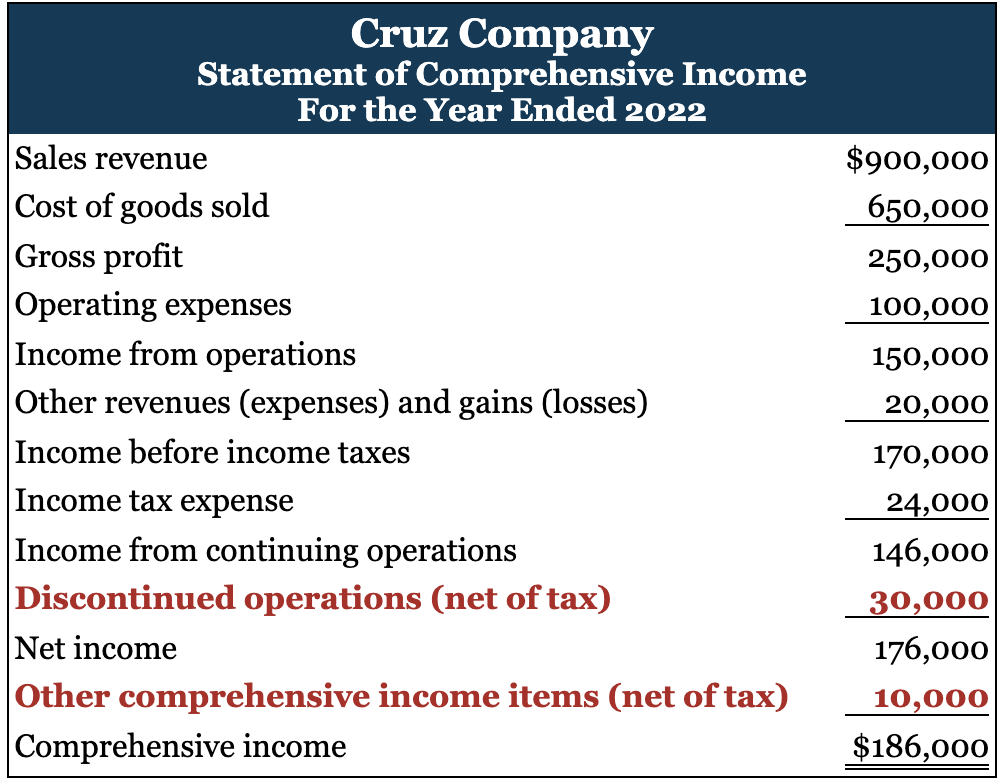

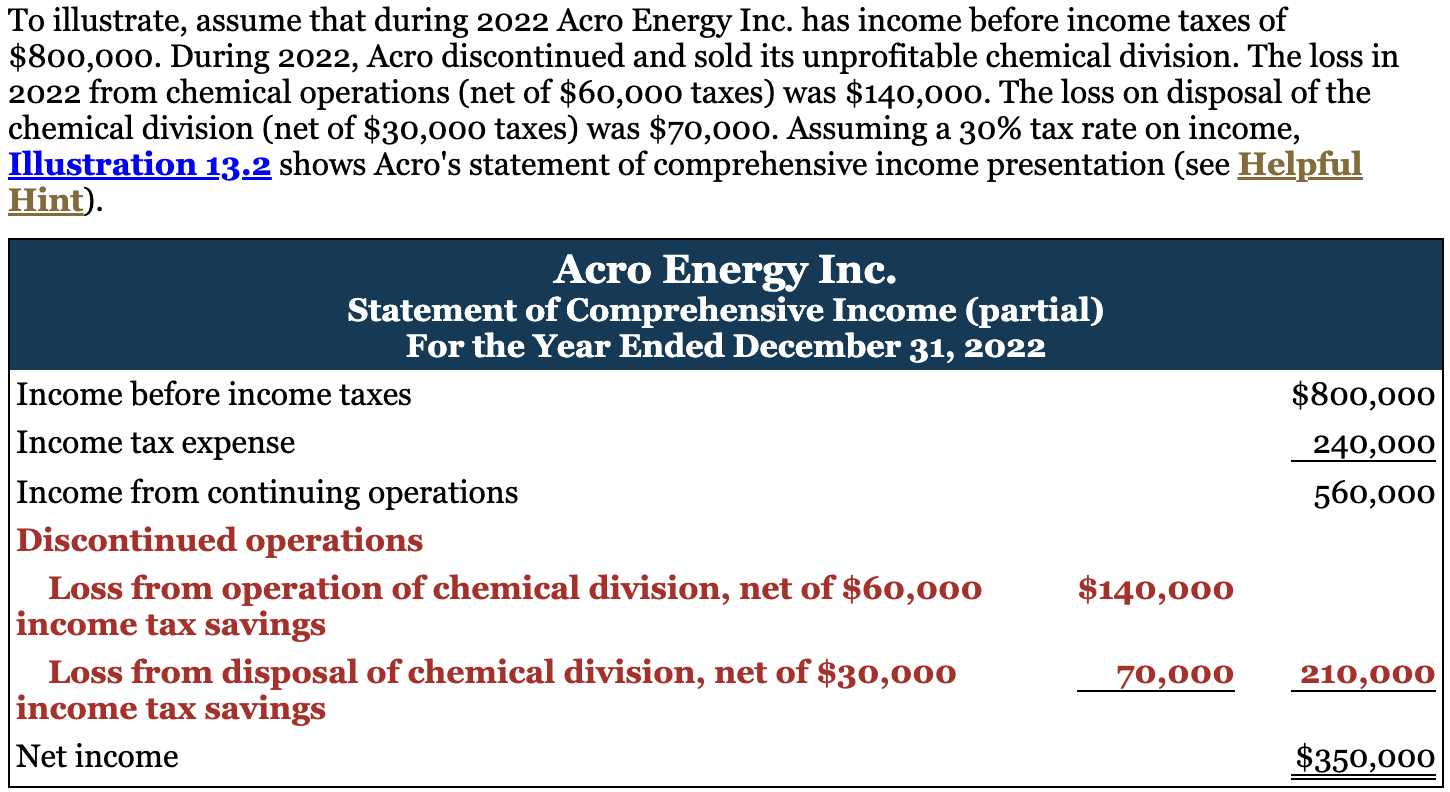

Discontinued operations: Refers to the disposal of a significant component of a business, such as the elimination of a major class of customers or an entire activity. Alerts users to the sale of any of a company’s major components of its business.

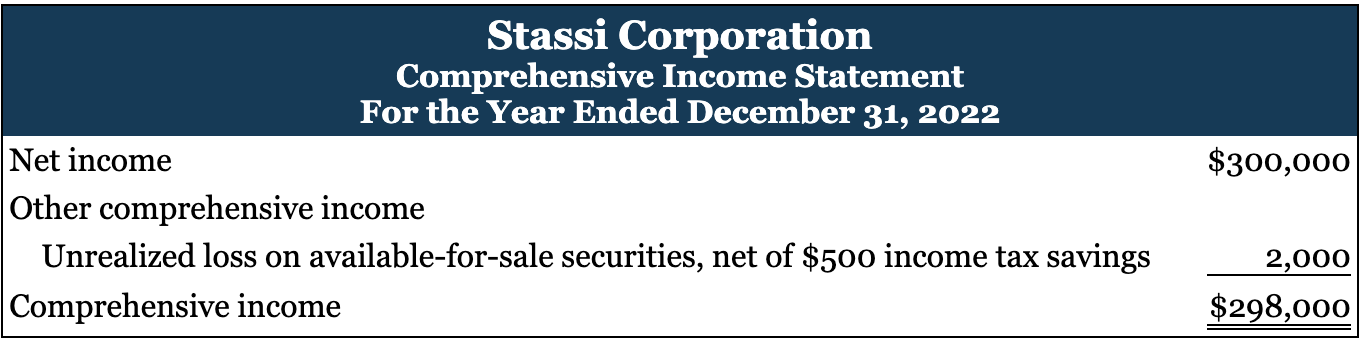

Comprehensive income: The sum of net income and other comprehensive income items.

Trading security: bought and held primarily for sale in the near term to generate income on short-term price differences.

Available-for-sale securities: Held with the intent of selling them sometime in the future.

Change in accounting principle: Occurs when the principle used in the current year is different from the one used in the preceding year. An example is a change in inventory costing methods. Accounting rules permit a change when management can show that the new principle is preferable to the old principle. Helps them determine the effect of this change in current and prior periods.

Quality of earnings: A comp. that has a high provides full and transparent info. that will not confuse or mislead users of the financial statements.

Notes:

Sustainable income info: an income statement provides information on sustainable income by separating transactions from nonoperating transactions. Highlights income from operations, income taxes, continuing operations.

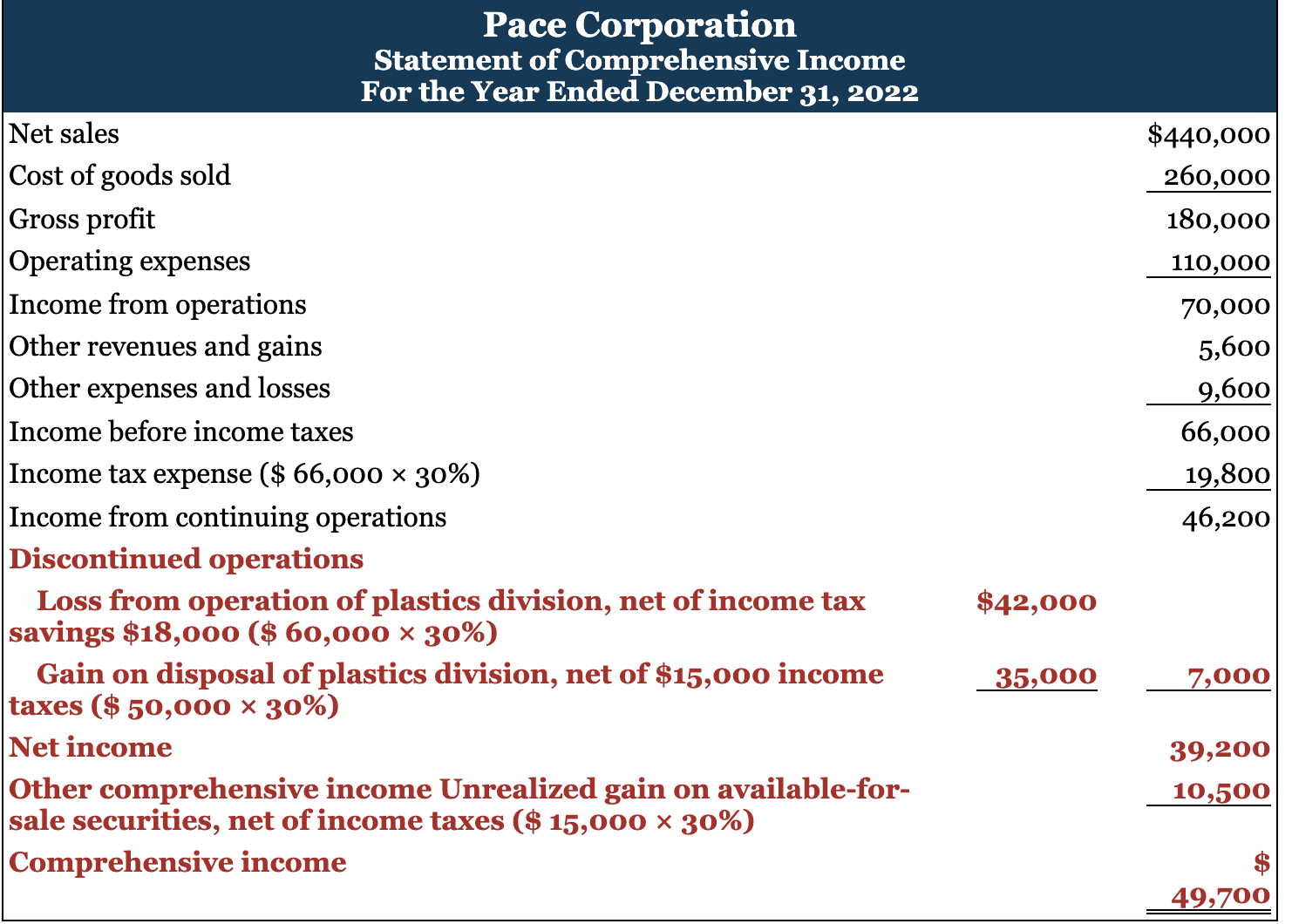

Statement of Comprehensive Income:

Discontinued operations: The income (loss) from discontinued operations consists of two parts: the income (loss) from operations and the gain (loss) on disposal of the component. The new section reports both the operating loss and the loss on disposal net of appicable income taxes.

Comprehensive Income Info: A gain or loss is referred to as unrealized when as asset has experienced a change in value but the owner has not sold the asset. The sale of the asset results in realization of the gain or loss. Companies report unrealized losses on trading securities in the “Other expenses and losses” section of the income statement. The rationale: It is likely that the company will realize the unrealized loss (or an unrealized gain), so the company should report the loss (gain) as part of net income. Companies do not include unrealized gains or losses on available-for-sale securities in net income. Instead, they report them as part of “Other comprehensive income”. Other comprehensive income is not included in net income.

Example of Comprehensive Income: Corp. has a net income of $300,000 and a 20% tax rate, the unrealized loss would be reported below net income, net of tax,

Lower portion of combined statement of income and comprehensive income

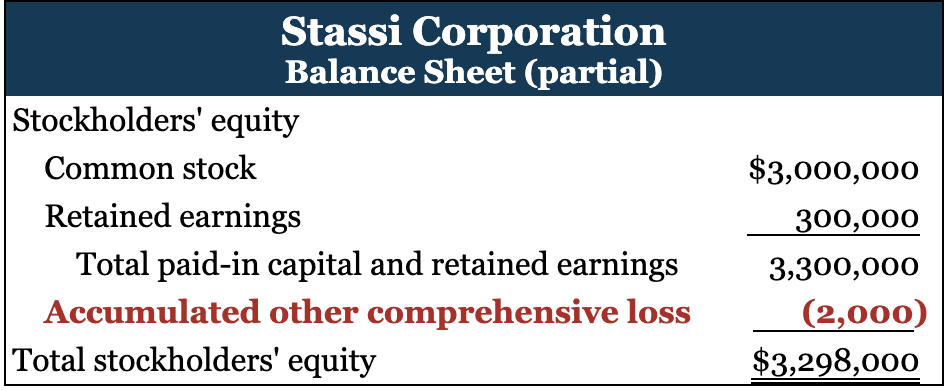

Companies report the cumulative amount of other comprehensive income from all years as a separate component of stockholders’ equity. Corp. has common stock of $3,000,000, retained earnings of $300,000, and accumulated other comprehensive loss of $2,000.

Unrealized loss in stockholders’ equity section

Many companies report net income and other comprehensive income in a combined income. The statement of comprehensive income of corp. presents the type of items found on this statenet, such as net sales, cost, of goods sold, operating expenses, and income taxes. Shows how companies report discontinued operations and other comprehensive income.

factors affecting quality of earnings: Alt. Accounting Methods

Learning Objective 2

Horizontal analysis

Vertical analysis

Vocab:

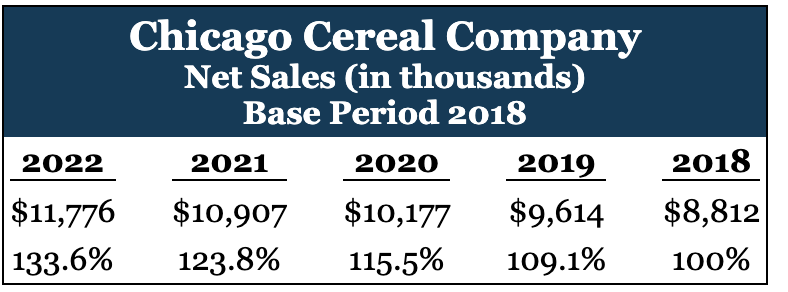

Horizontal analysis- trend analysis, is a technique for evaluating a series of fin. statement data over a period of time. To determine the increase or decrease that has taken place, expressed in amount or %.

Vertical analysis- common-size analysis, is a technique for evaluating financial statement data that expresses each item in a financial statement as a percentage of a base amount.

Notes:

Info on Hor. Analysis: Helps users compare a company’s financial position and operating results with those of the previous period. Can measure all percentage increases or decreases relative to this base period amount.

Can express current-year sales as a percentage of the base period

Current-period sales as a percentage of the base period for each of the five years

This shows if the increase of the financial status throughout the years. Be sure to examine both dollar amount changes and percentage changes. It is not bad if a comp. earnings are growing in a declining rate. The amount of increase may be the same as or more than the base year, but the percentage change may be less because the base is greater each year.

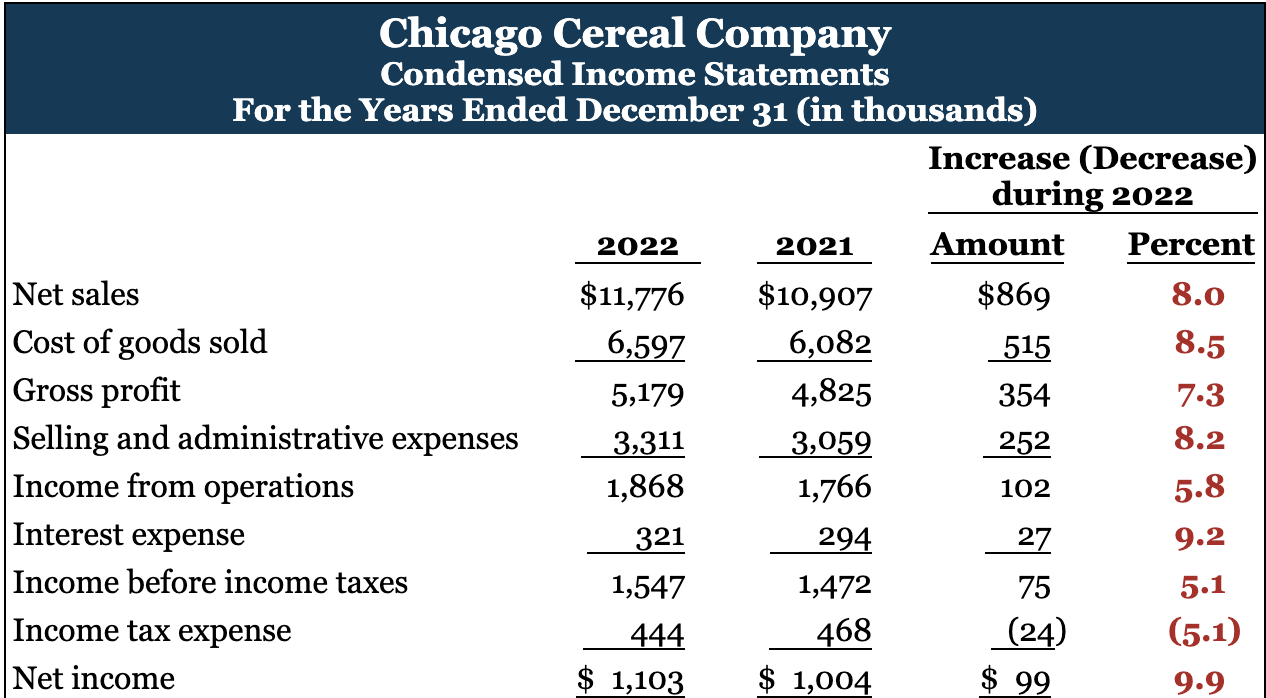

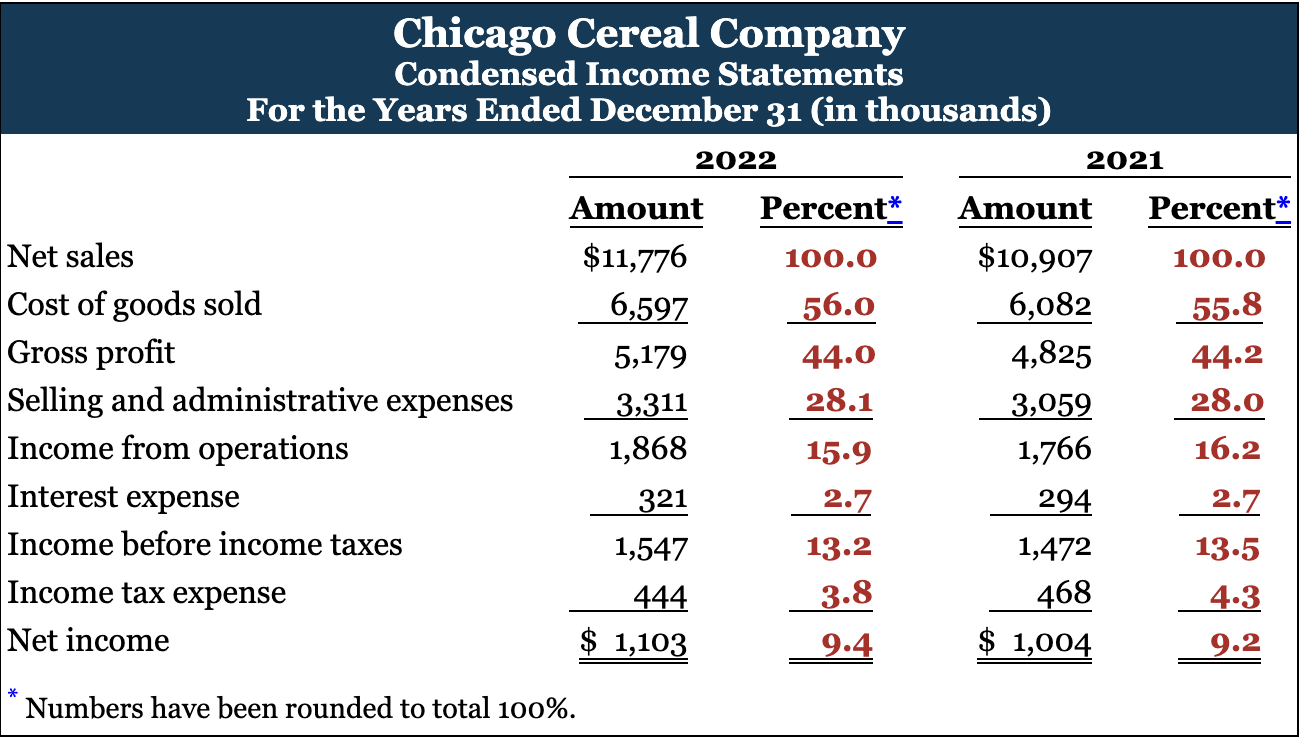

Net sales increased 869 or 8.0% (869/10,907). Cost of goods sold increased 515 or 8.5% (515/6,082). Selling and administrative expenses increased 252, 82% (252/3059). Overall, gross profit increased 7.3% and net income increased 9.9%. The increase in net income can be attributed to the increase in net sales and a decrease in income tax expense.

Info on Vert. Analysis: Helps users compare relationships between financial statement items with those of last year of competitors.

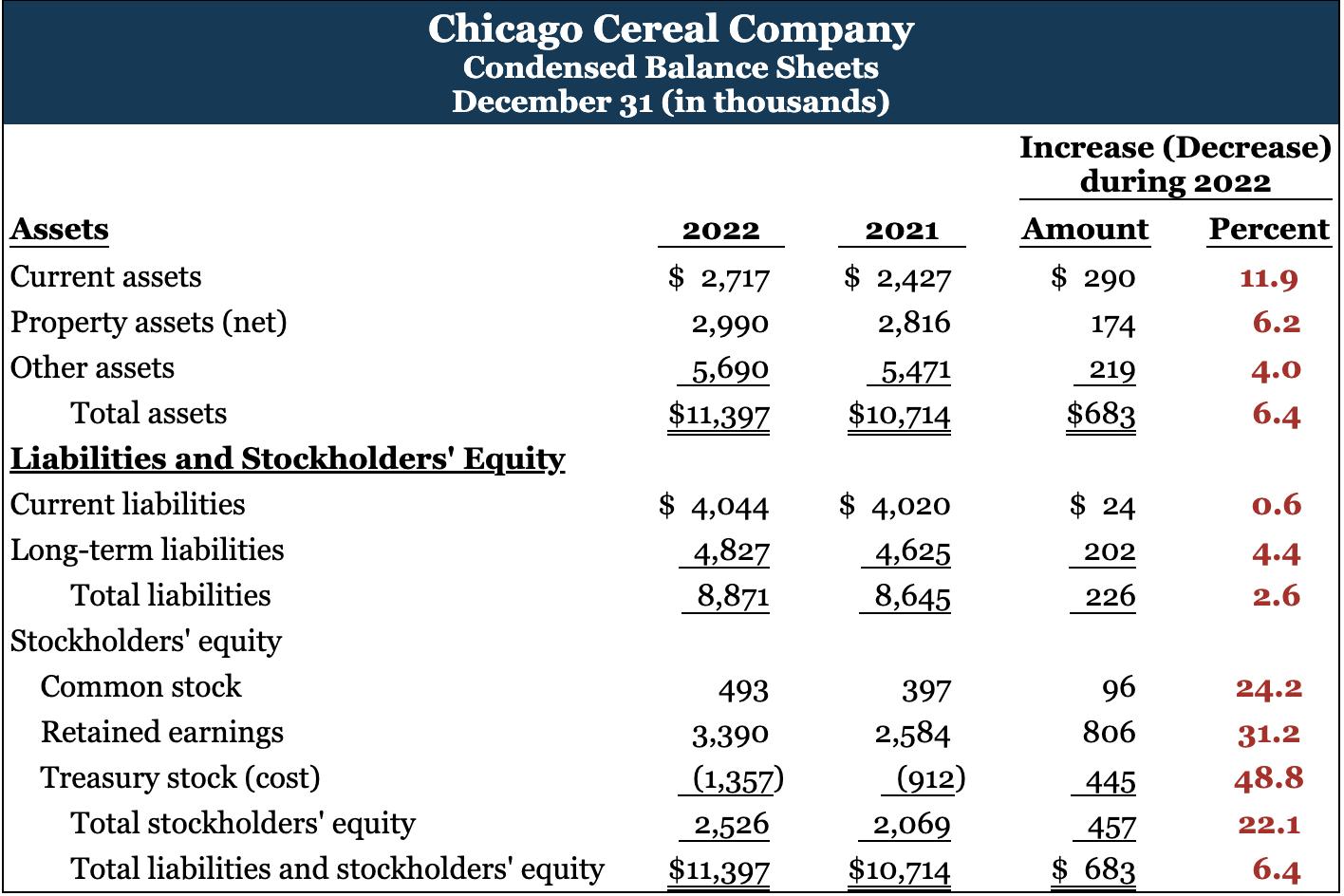

The base for the asset items is total assets, and the base for the liability and stockholders’ equity items is total liabilities and stockholders’ equity.

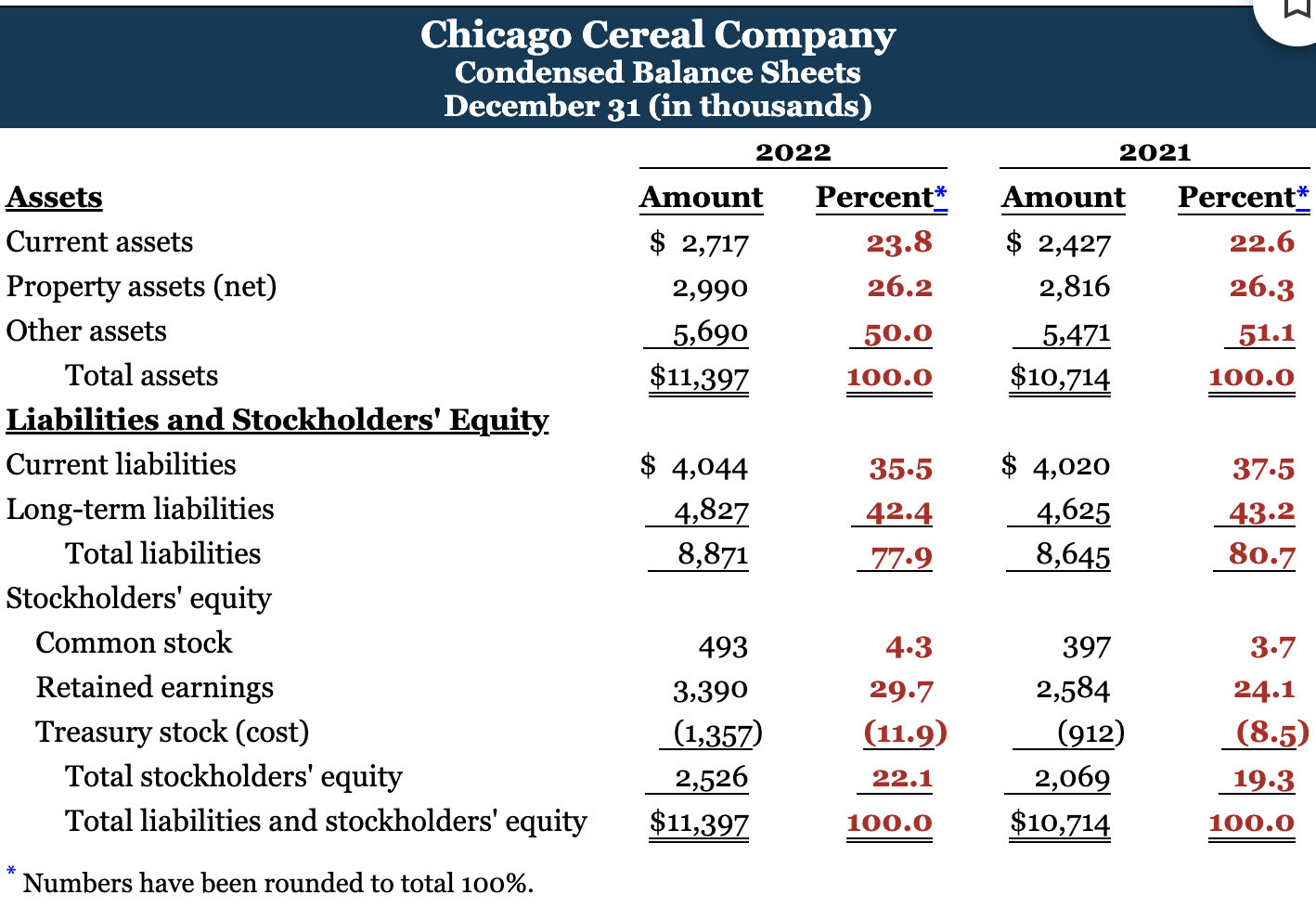

Can show the percentage change in the individual asset, liability, and stockholders’ equity items. Example: current assets increased 290 from 2021 to 2022, and they increased from 22.6% to 23.8% of total assets. Property assets (net) decreased from 26.3% to 26.2% of total assets. Other assets decreased from 51.1% to 50.0% of total assets. The company shifted toward equity financing by relying less on debt and by increasing the amount of retained earnings.

The cost of goods sold as a percentage of net sales increased from 55.8% to 56.0% and selling and administrative expenses increased from 28.0% to 28.1%. Net income as a percentage of net sales increased from 92% to 9.4%. Comp. increase in net income as a percentage of sales is due to the decrease in income tax expense as a percentage of sales.

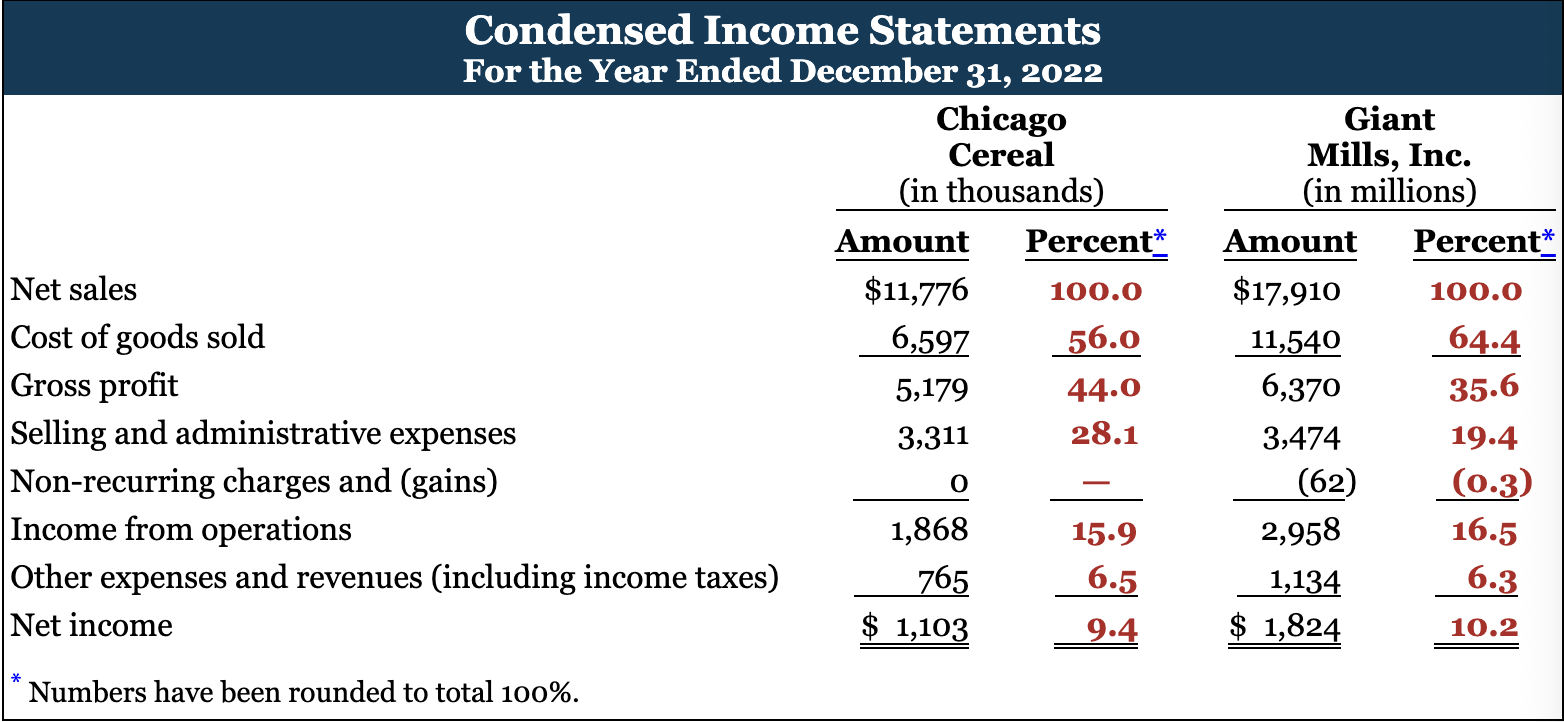

Enables you to compare comps. of different sizes.

This eliminates the impact of this size difference for our analysis. CC jas a higher gross 44% while GM has 35.6%. But CC has 28.1% of net sales while GM has 19.4% of net sales. We see that GM income is higher. From 10.2% to 9.4% with CC.

Learning Objective 3

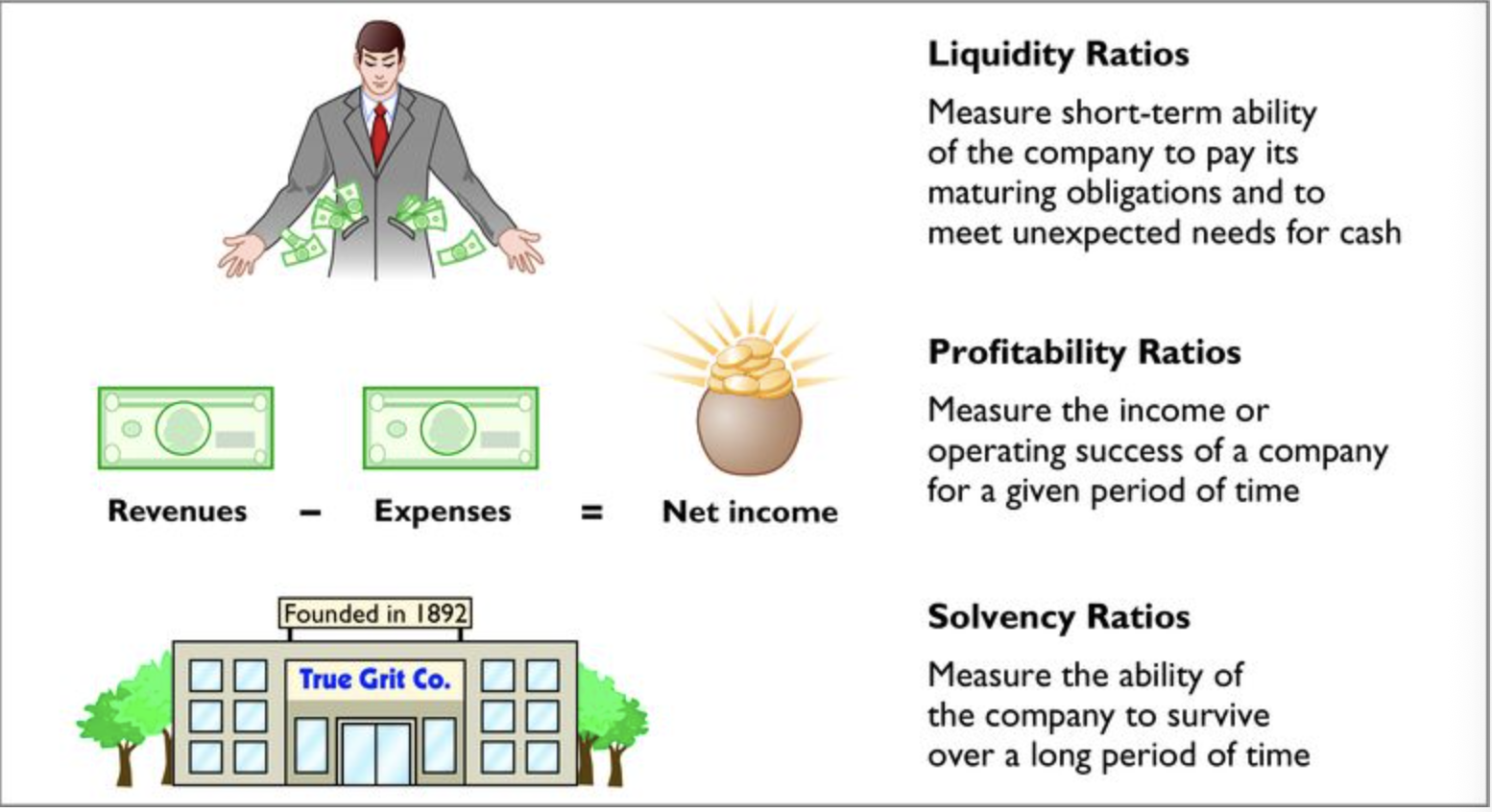

Liquidity ratios

Solvency ratios

Profitability ratios

Financial analysis and data analytics

Comprehensive example

Vocab:

Ratio Analysis- Expresses the relationship among selected items of financial statement data.

Ratio- expresses a percentage, a rate, or simple proportion.

Liquidity ratios- measures the short-term ability of the company to pay its maturing obligations and meet to meet unexpected needs for cash. Short-terms creditors such as bankers and suppliers are particularly interested in assessing liquidity.

Solvency Ratios- Measure the ability of the company to survive over long period of time. Long-term creditors and stockholders are interested in a company’s long-run solvency, particularly its ability to pay interest as it comes due and to repay the balance of debt at its maturity.

Profitability ratio- Measure the income or operating success of a company for a given period of time. A comp. income affects its ability to obtain debt and equity financing, its liquidity position, and its ability to grow. As a consequence, creditors and investors alike are interested in evaluating profitability. This is used as a ultimate test of management’s operating effectiveness.

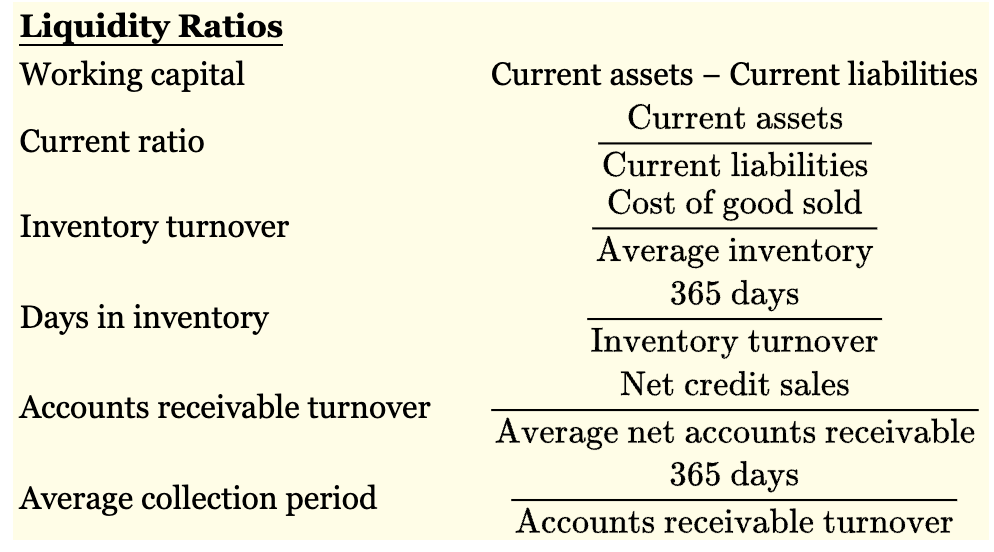

Current ratio- expresses the relationship of the current assets to current liabilities, computed by dividing current assets by current liabilities.

Accounts receivable turnover- measures the number of times, on average, a company collects receivables during the period. The accounts receivable turnover is computed by dividing net credit sales (net sales less cash sales) by average net accounts receivable during the year.

Average collection period- Done by dividing the accounts receivable turnover into 365 days.

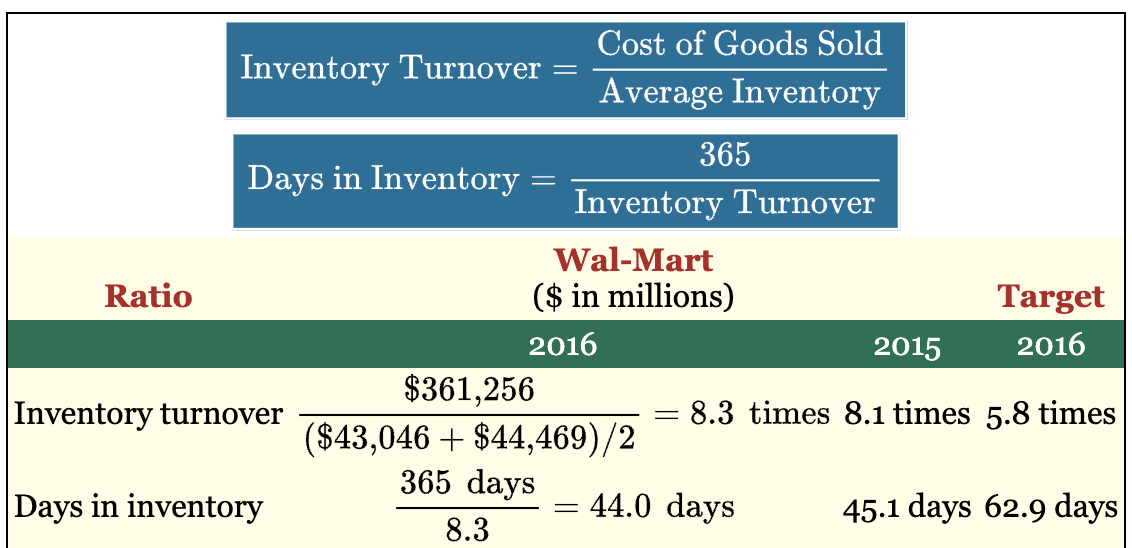

Inventory turnover- Measures the number of times average inventory was sold during the period. Its purpose is to measure the liquidity of the inventory.

Days in inventory- Measures the average number of days inventory is held.

Debt to assets Ratio- measures the percentage of total financing provided by creditors. It is computed by dividing total liabilities (both current and long-term debt) by total assets. This ratio indicates the degree of financial leveraging.

Times interest earned- (also called interest coverage) indicates the company's ability to meet interest payments as they come due. It is computed by dividing the sum of net income, interest expense, and income tax expense by interest expense.

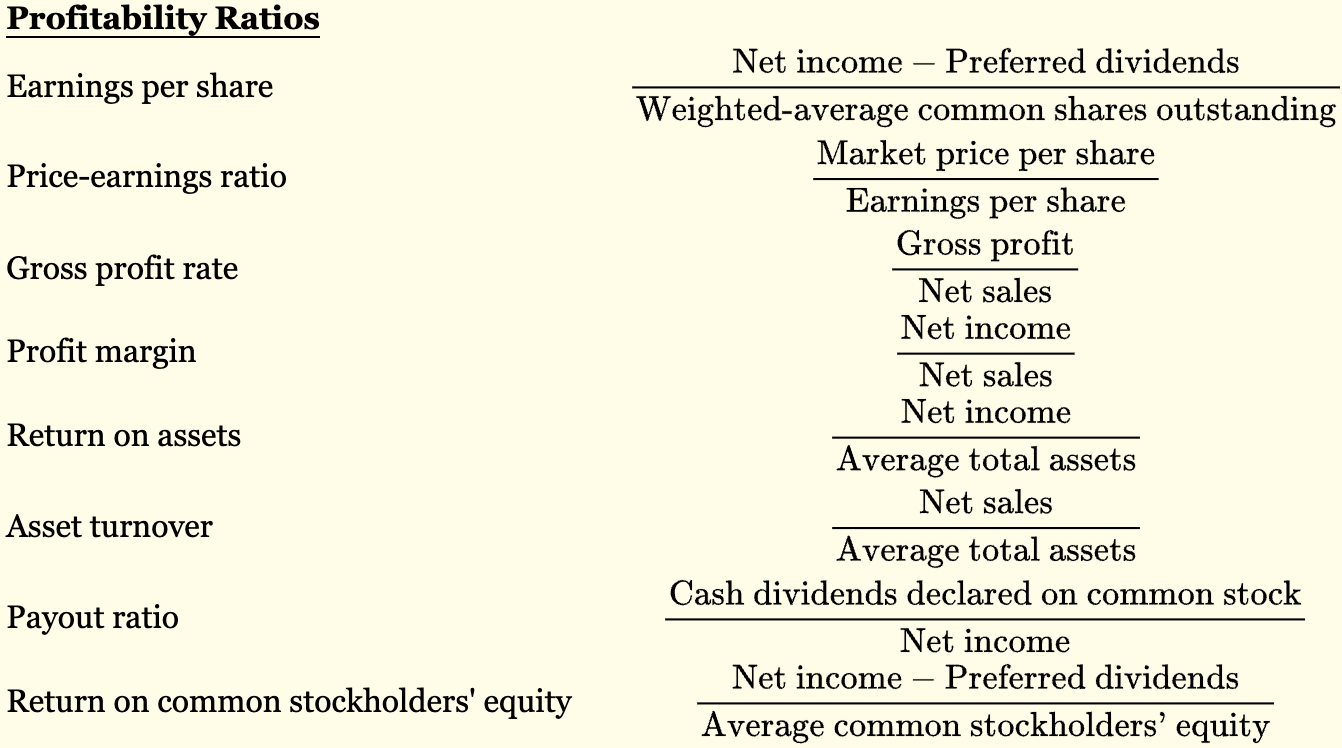

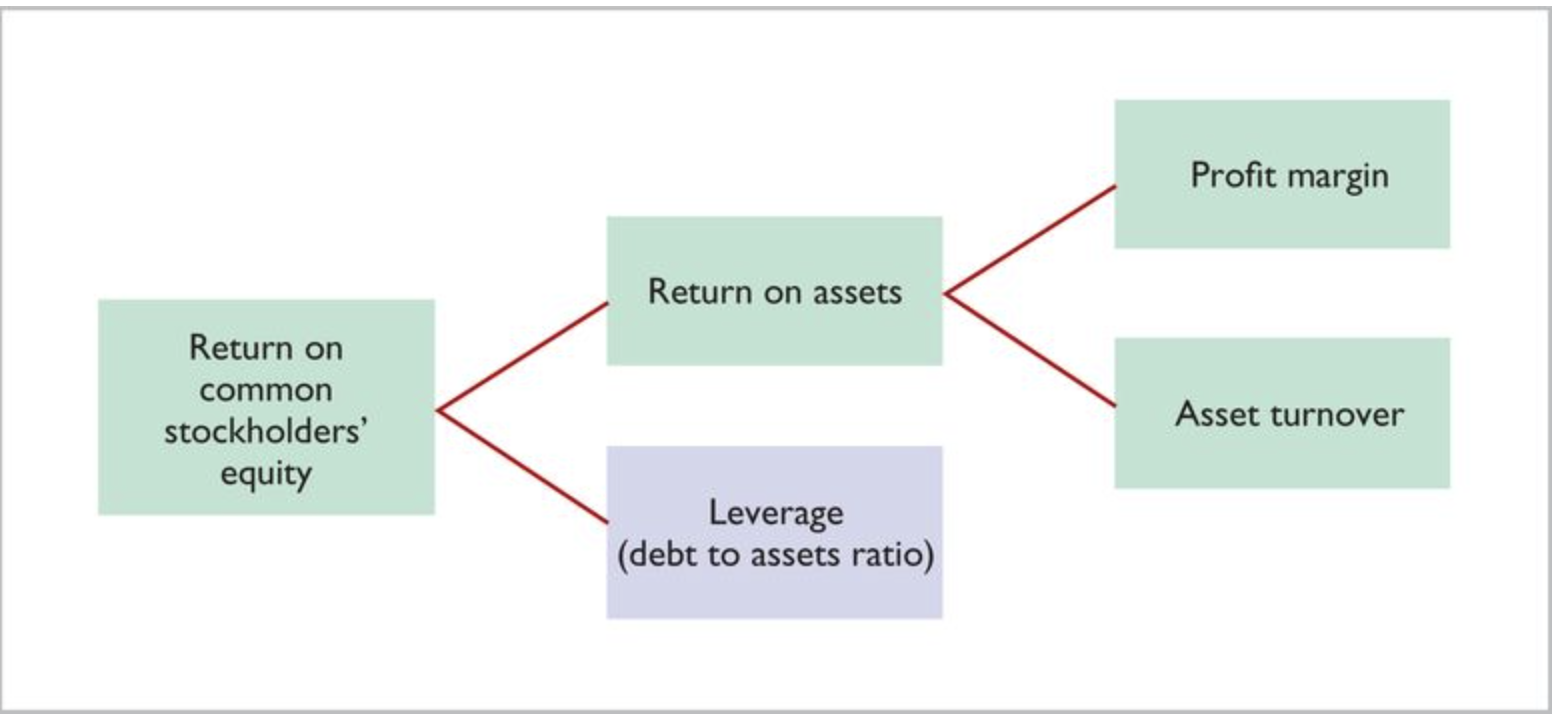

Return on common stockholders’ equity (ROE)- This ratio shows how many dollars of net income the company earned for each dollar invested by the owners. It is computed by dividing net income minus any preferred dividends—that is, income available to common stockholders—by average common stockholders' equity.

Return on assets- measures the overall profitability of assets in terms of the income earned on each dollar invested in assets. It is computed by dividing net income by average total assets.

Leveraging/Trading on the equity- the company has borrowed money at a lower rate of interest than the rate of return it earns on the assets it purchased with the borrowed funds. Leverage enables management to use money supplied by nonowners to increase the return to owners.

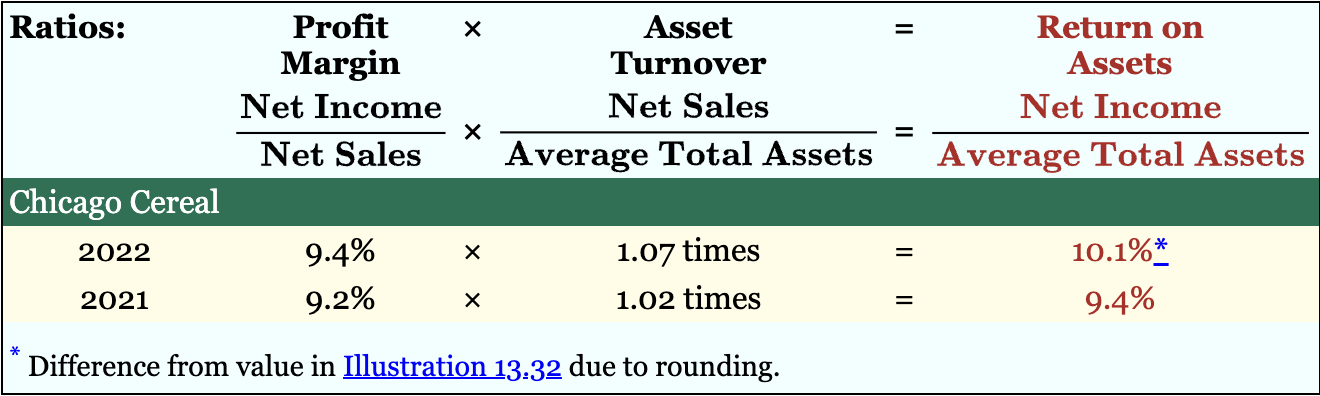

Profit Margin- rate of return on sales, is a measure of the percentage of each dollar of sales that results in net income. It is computed by dividing net income by net sales for the period.

Asset Turnover- measures how efficiently a company uses its assets to generate sales. It is determined by dividing net sales by average total assets for the period.

Gross profit rate- determined by dividing gross profit (net sales less cost of goods sold) by net sales. This rate indicates a company's ability to maintain an adequate selling price above its cost of goods sold.

Earnings per Share- measure of the net income earned on each share of common stock. It is computed by dividing net income by the average number of common shares outstanding during the year.

Price-earning ratio- an oft-quoted statistic that measures the ratio of the market price of each share of common stock to the earnings per share. The price-earnings (P-E) ratio reflects investors' assessments of a company's future earnings. It is computed by dividing the market price per share of the stock by earnings per share.

Payout ratio- measures the percentage of earnings distributed in the form of cash dividends. It is computed by dividing cash dividends declared on common stock by net income.

Notes:

Info on Ratio Analysis:

Helps users evaluate mathematical relationships between financial statement items and compare across years, competitors, and industry. Can be used to provide clues to underlying conditions that may not be apparent from individual financial statement components.

Example: Has current assets of 13,626 million and current liabilities of 3,926 milion. We can find the relationship between these two measures by dividing ca by cl.

Info on Liquidity Ratio:

Info on Solvency Ratios:

Info on Profitability Ratios:

Under Liquidity:

Current Ratios- expresses the relationships of ca to cl, computed by dividing ca by cl. Used to evaluating a comp. liquidity and short-term debt-paying ability.

Tells us the current ratio is .67 meaning for every dollar of current liabilities, it has $0.67 of current assets. Can be seen as .67:1.

Accounts receivable turnover: Measure liquidity by how quickly a company converts certain assets to cash. A low value for the current ratio can sometimes be compensated for if some of the company’s current assets are highly liquid. measures the number of times, on average, a company collects receivables during the period. The accounts receivable turnover is computed by dividing net credit sales (net sales less cash sales) by average net accounts receivable during the year.

The turnover of 11.9 times is higher than the industry average of 11.2 times, and slightly lower than GM turnover 12.2 times. A higher value suggests better liquidity because the receivables are being collected more quickly.

Average collection period: From ART converts into this. Done by dividing the accounts receivable turnover into 365 days. Used to asses the effectiveness of a comp. credit and collection policies. The general rule is that the collection period should not greatly exceed the credit term period. (the time allowed for payment which is usually 30)

11.9 times is divided into 365 days to obtain 31 days. This means that the ACP for receivables is about 31 days. A shorter CP means receivables are being collected more quickly and thus are more liquid.

Inventory turnover: measures the number of times average inventory was sold during the period. Its purpose is to measure the liquidity of the inventory. A high measure means the inventory is being sold and replenished. COmputed by dividing the cost of goods sold by the average inventory during the period. Computed from the beginning and ending inventory balances.

CC turnover of 7.5 times is higher than the industry average of 6.7 times. The faster the inventory turnover, the less cash is tied up in inventory and less the chance of inventory becoming obsolete. A downside of high IT is it results in lost sales because if a comp. keeps less inventory on hand, it is more likely to run out of the inventory when it is needed.

Days in inventory: Measures the average number of days inventory is held.

Of 7.5 divided into 365 is 49 days. An average selling time of 49 days is faster than the industry average.

Under Solvency Ratio:

Debt to assets ratio: Measures the percentage of total financing provided by creditors. Computed by dividing total liabilities (both current and long-term debt) by total assets. Indicated the degree of fin. leveraging. It also provides some indication of the comp. ability to withstand losses without impairing the interests of its creditors. The higher the DTA, the greater the risk the comp. may be unable to meet its maturing obligations.

78% means the creditors have provided financing sufficient to cover 78% of the comp. total assets. It would have to liquidate 78% of its assets at their book value in order to pay off all its debts. Same follows with debt to equity ratio.

Time interest earned: (also called interest coverage) indicates the company's ability to meet interest payments as they come due. It is computed by dividing the sum of net income, interest expense, and income tax expense by interest expense. This ratio uses income before interest expense and income taxes because this amount represents what is available to cover interest.

Interest coverage was 5.8 times, which indicates that income before interest and taxes was 5.8 times the amount needed for interest expense. A low debt to assets ratio and high times interest earned suggested better solvency.

Under Profitability Ratio:

Return on common stockholders’ equity (ROE); This shows how many dollars of net income the comp. earned for each dollar invested by the owners. Computed by dividing net income minus any preferred dividends, income available to common stockholders by average ROE.

Unusually high

Return on assets: Measures the overall profitability of assets in terms of the income earned on each dollar invested in assets. Computed by dividing net income by average total assets.

A comparison of the rate of return on assets with the rate of interest paid for borrowed money indicates the profitability of trading on the equity. If you borrow 8% and your return rate on assets is 11%, you are trading on the equity at a gain. However, if you borrow money at 11% and earn only 8% on it, you are trading on the equity at a loss.

Profit Margin/Rate of return on sales: measure of the precentage of each dollar of sales that results in net income. Computed by dividing net income by net sales for the period.

High-volume (high inventory turnover) businesses such as grocery stores and pharmacy chains generally have low profit margins. Low-volume businesses such as jewelry stores and airplane manufacturers have high profit margins.

Asset Turnover: Measures how efficiently a comp. uses its assets to generates sales. COmputed by dividing net sales by average total assets for the period. The resulting number shows the dollars of sales produced by each dollar invested in assets.

In summary, Chicago Cereal's return on assets increased from 9.4% in 2021 to 10.0% in 2022. Underlying this increase was an increased profitability on each dollar of sales (as measured by the profit margin) and a rise in the sales-generating efficiency of its assets (as measured by the asset turnover).

Gross Profit Rate; Determined by dividing gross profit (net sales less cost of goods sold) by net sales. Indicates a comp. ability to maintain an adequate selling price above its cost of goods sold. As an industry becomes more competitive, the ratio declines.

Earnings per Share (EPS): Measure of the net income earned on each share of common stock. Computed by dividing net income by the average number of common shares outstanding during the year. “net income per share” refer to the amount of net income applicable to each share of common stock. If there are preferred dividends declared for the period, we must deduct them from the net income to arrive at income available to the common stockholders.

Price-earnings ratio: An oft-quoted statistic that measures the ratio of the market price of each share of common stock to the earnings per share. The price-earnings (P-E) ratio reflects investors’ assessments of a comp. future earnings. Computed by dividing the market price per share of the stock by earnings per share.

Its lower P-E ratio suggests that the market is less optimistic about CC than about GM, however it might also signal that CC stock is underpriced.

Payout Ratio: Measure the percentage of earnings distributed in the form of cash dividends. Computed by dividing cash dividends declared on common stock by net income. Comps. who have high growth rates are played by low payout ratios because they reinvest most of their net income in the business.

A lower payout ratio means a comp. has chosen to pay out a lower percentage of its net income as dividends. The payout ratio will increase if a comp. net income declines but the company keeps its total dividend payment the same. Unless the comp. returns to its previous level of profitability, maintaining this higher dividends payout ratio is probably not possible in the long run.

Ch. 4 Accrual Accounting Concepts

Learning Objective 1

Revenue recognition principle

Expense recognition principle

Accrual vs. cash basis

Need for adjusting entries

Types of adjusting entries

Vocab:

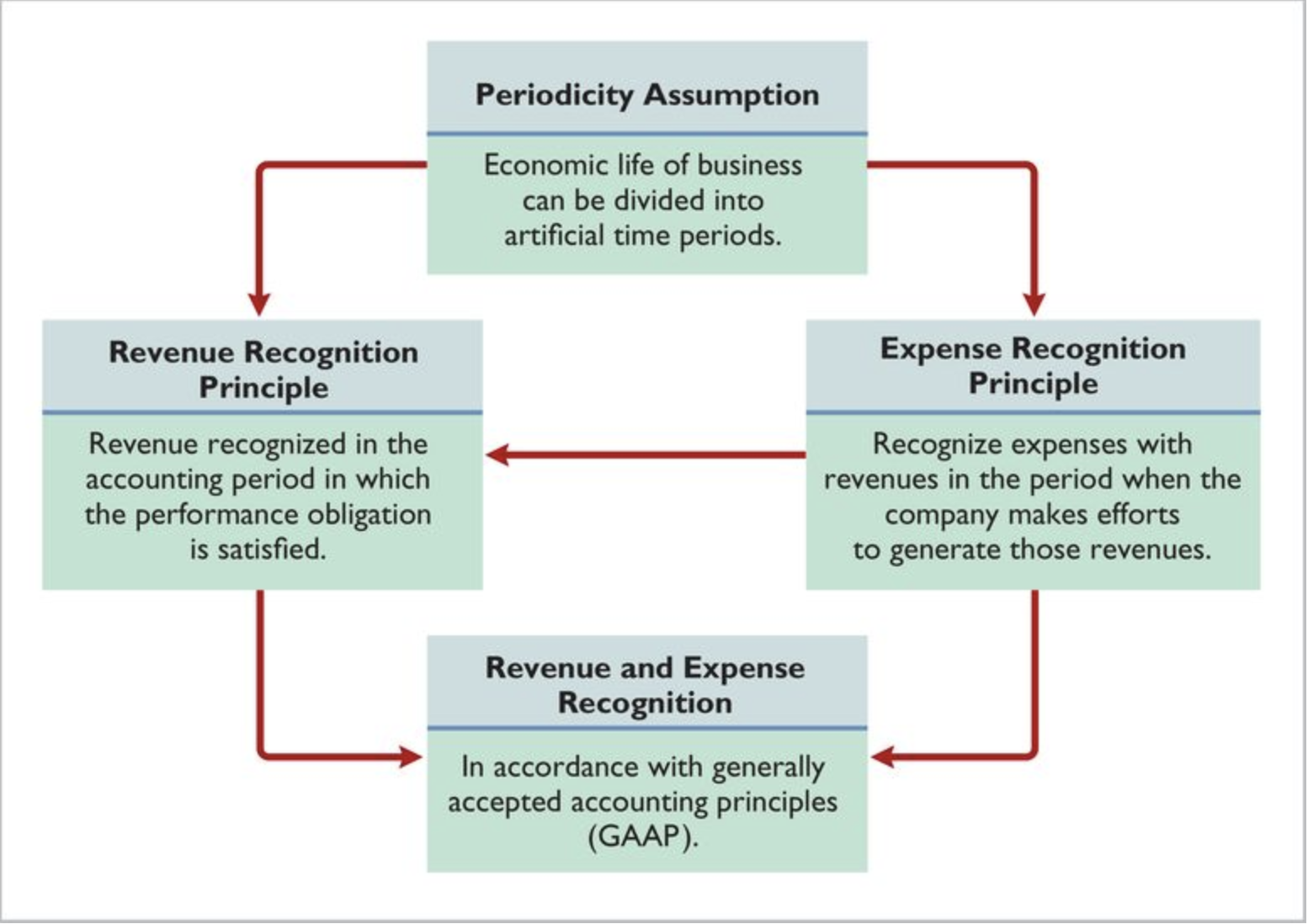

Periodicity Assumption- Accounting divides the economic life of a business into artificial time periods.

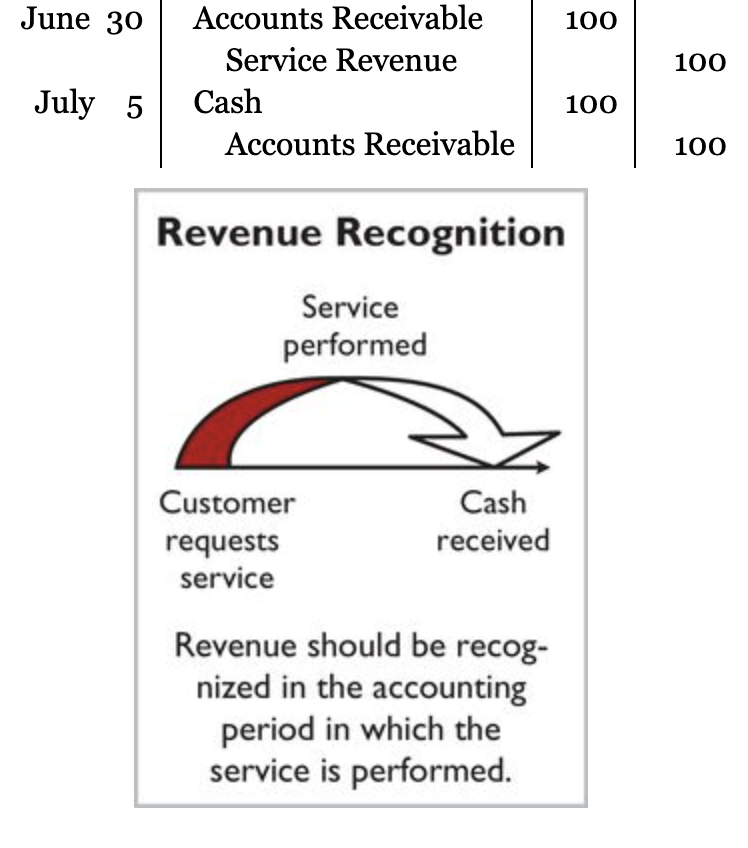

Revenue Recognition Principle- requires that companies recognize revenue in the accounting period in which the performance obligation is satisfied.

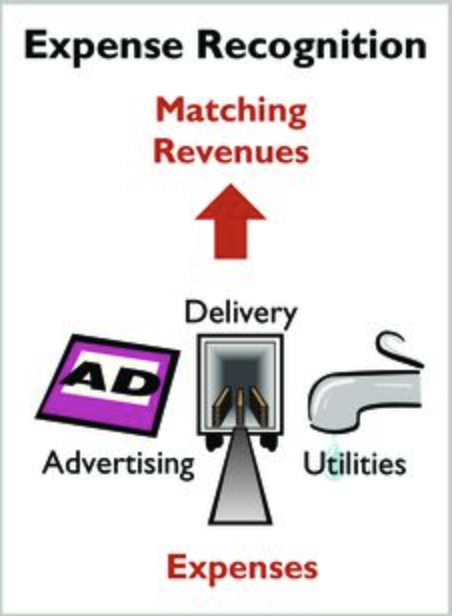

Expense recognition principle- It dictates that efforts (expenses) be recognized with results (revenues) in the period when the company makes efforts to generate those revenues

Accrual-basis accounting- means that transactions that change a company's financial statements are recorded in the periods in which the events occur, even if cash was not exchanged

Cash-basis accounting- companies record revenue at the time they receive cash. They record an expense at the time they pay out cash. The cash basis seems appealing due to its simplicity, but it often produces misleading financial statements.

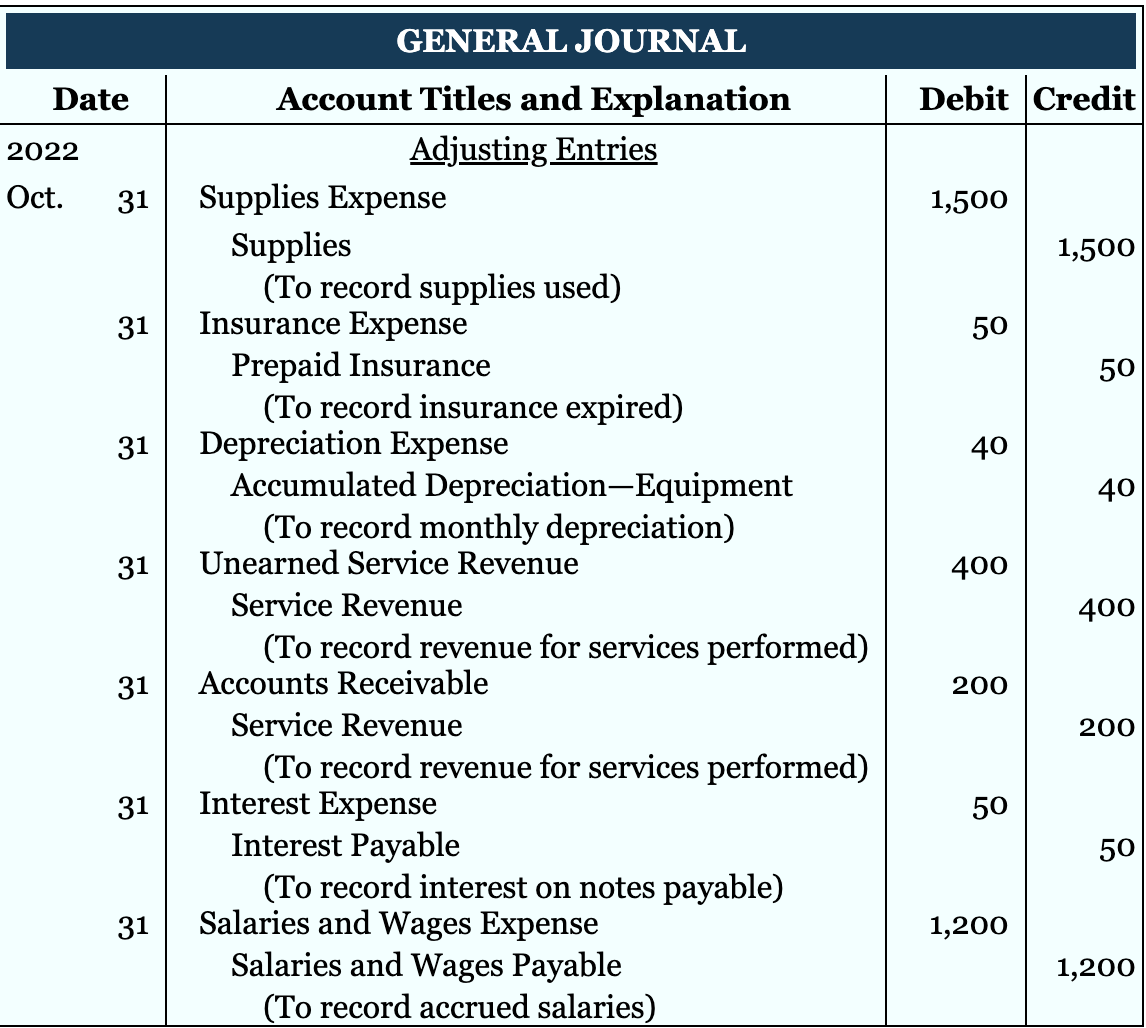

Adjusting entries- ensure that the revenue recognition and expense recognition principles are followed. Adjusting entries are necessary because the trial balance—the first pulling together of the transaction data—may not contain up-to-date and complete data.

Notes:

Accounting divides the economic life of a business into artificial time periods. Accounting time periods are generally a month, a quarter, or a year. One year long is called a fiscal year. There are two steps to help understand of the nature of the company’s business. Revenue recognition principle and the expense recognition principle.

The revenue Recognition principle:

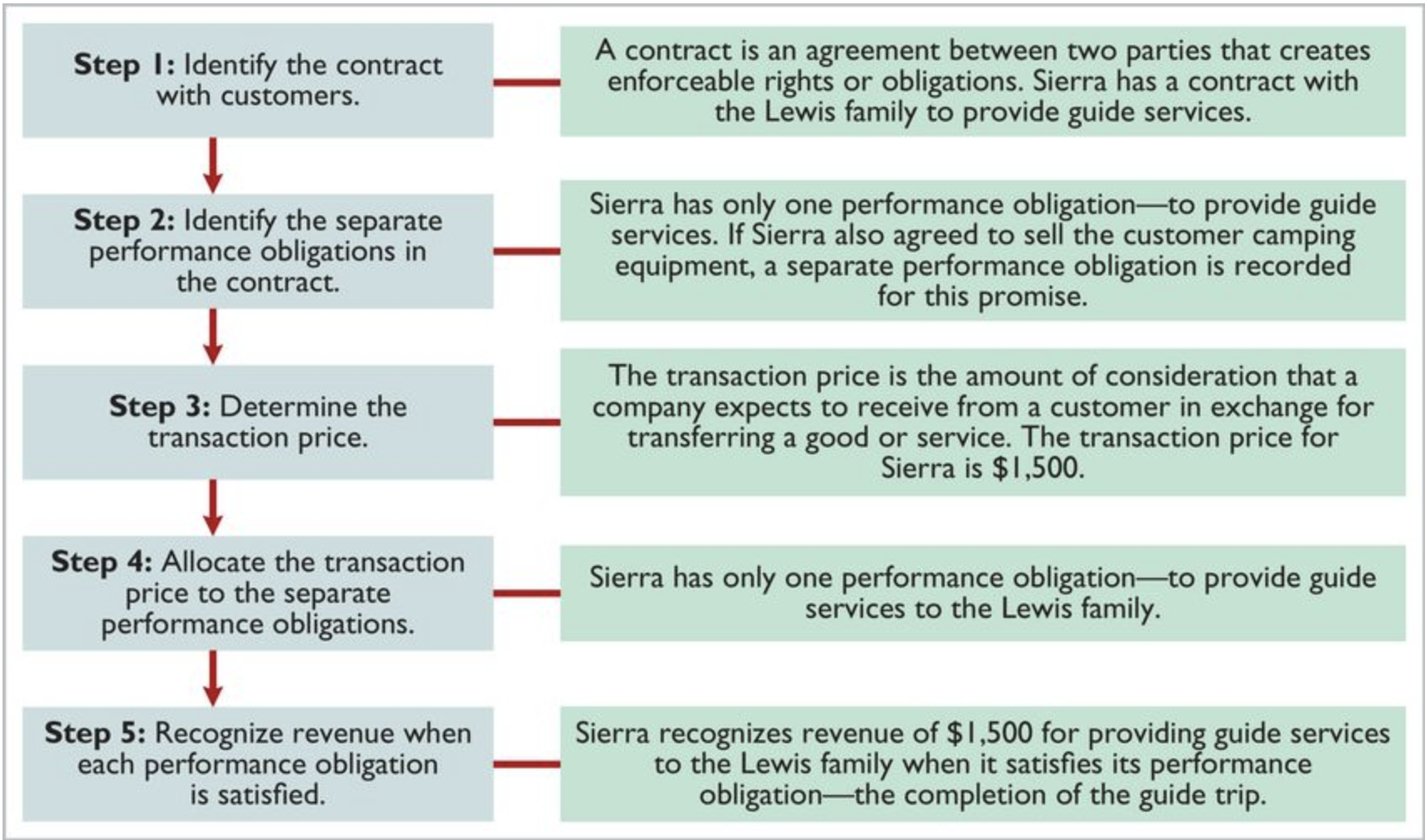

When a comp. agrees to perform a service or sell a product to a customer, it has a performance obligation. Requires that companies recognize revenue in the accounting period in which the performance obligation is satisfied

There is a five step revenue recognition process.

The Expense Recognition Principle:

“Let the expenses follow the revenues” It is tied to Rev. Recognition. Can be referred to matching principle. It dictates that efforts (expenses) be recognized with results (revenues) in the period when the company makes efforts to generate those revenues.

Both help to ensure that companies report the correct amount of revenues and expenses in a given period.

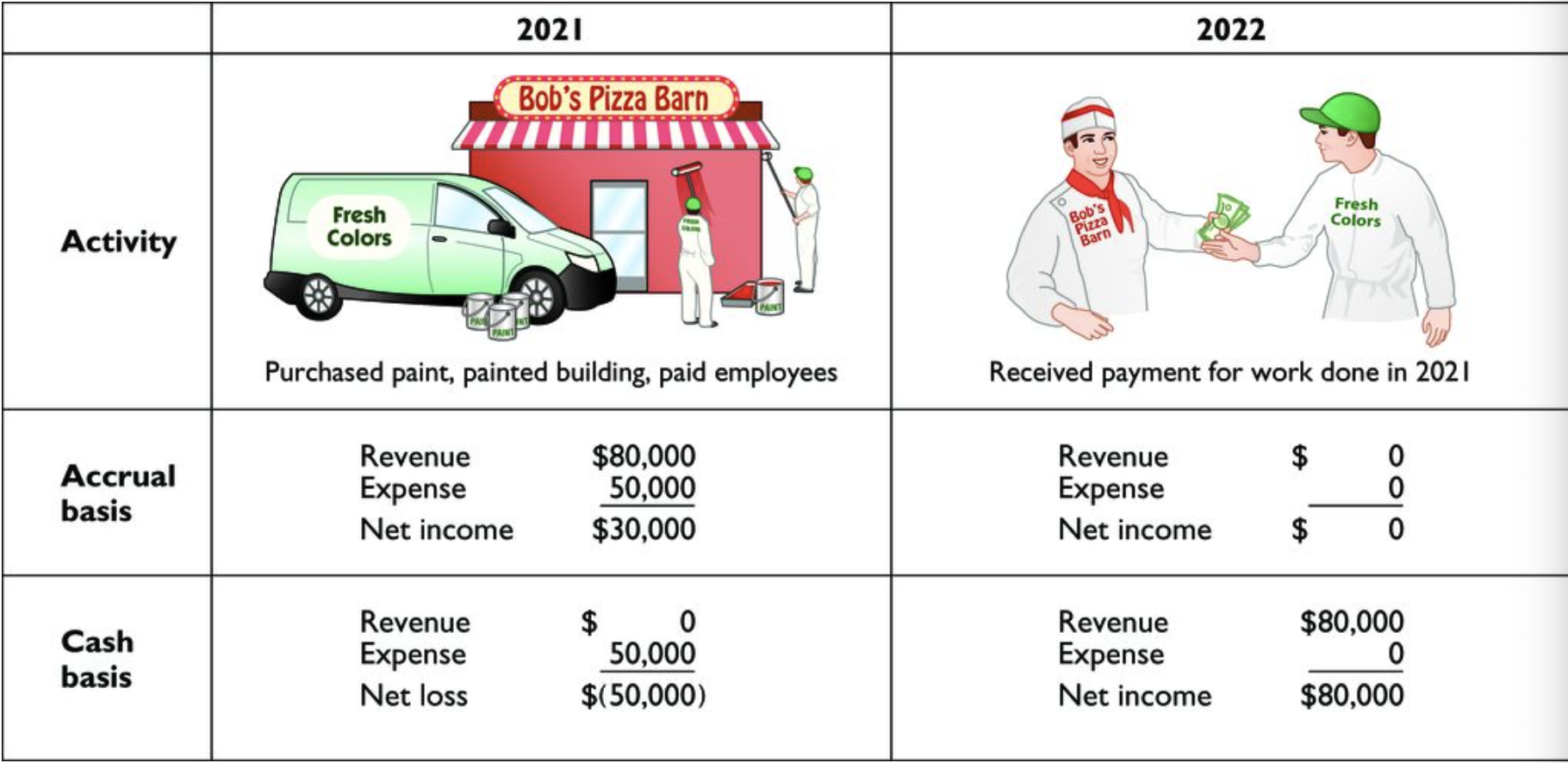

Accrual versus Cash Basis of Accounting:

Accrual:

Means that transactions that change a company's financial statements are recorded in the periods in which the events occur, even if cash was not exchanged (see International Note). For example, using the accrual basis means that companies recognize revenues when they perform the services (the revenue recognition principle), even if cash was not received. Likewise, under the accrual basis, companies recognize expenses when incurred (the expense recognition principle), even if cash was not paid.

Used as a central standard

Versus

Cash Basis:

Companies record revenue at the time they receive cash. They record an expense at the time they pay out cash. The cash basis seems appealing due to its simplicity, but it often produces misleading financial statements. For example, it fails to record revenue for a company that has performed services but has not yet received payment. As a result, the cash basis may not reflect revenue in the period that a performance obligation is satisfied.

Not generally accepted accounting principles

If it used cash basis, it would report 50,000 of expenses in 2021 and 80,000 of revenues during 2022. It would report a loss of 50,000 in 2021 and net income of 80,000 in 2022. The cash-basis measures are misleading because the fin. performance of the company would be misstated for both 2021 and 2022.

The Need for Adjusting Entries:

In order for rev. to be recorded in the period in which the performance obligations are satisfied and for expenses to be recognized in the period in which they are incurred. Adjusting entries ensure that the revenue recognition and expense recognition principles are followed.

Adjusting entries are necessary because the trial balance—the first pulling together of the transaction data—may not contain up-to-date and complete data.

This is true because:

Some events are not recorded daily because it is not efficient to do so. Ex: Use of supplies/earnings of wages by employees.

Some costs are recorded during the accounting period because these costs expire with the passage of time rather than as a result of recurring daily transactions. Ex: charges related to the use of buildings and equipment, rnet, and insurance.

Some items may be unrecorded. Ex: Utility service bill that will not be received until the next accounting period.

The comp. analyzes each account in the trail balance to determine whether it is complete and up-to-date for financial statement purposes. Every adjusting entry will include one income statement account and one balance sheet account.

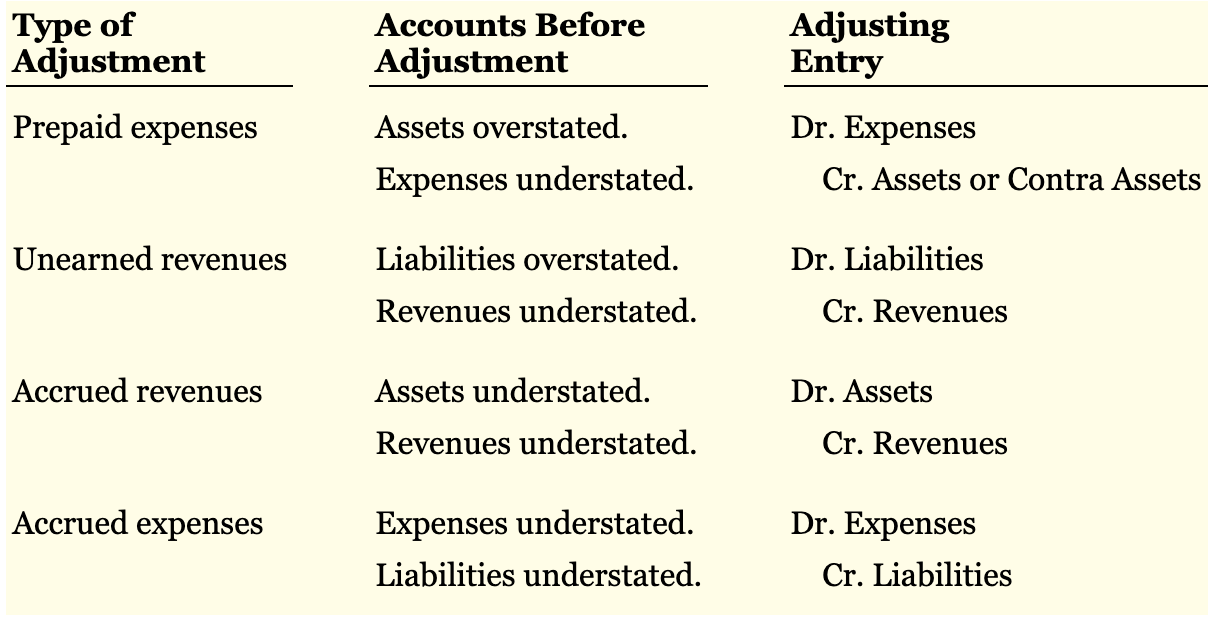

Types of Adjusting Entries:

Learning Objective 2

Prepaid expenses

Unearned revenues

Vocab:

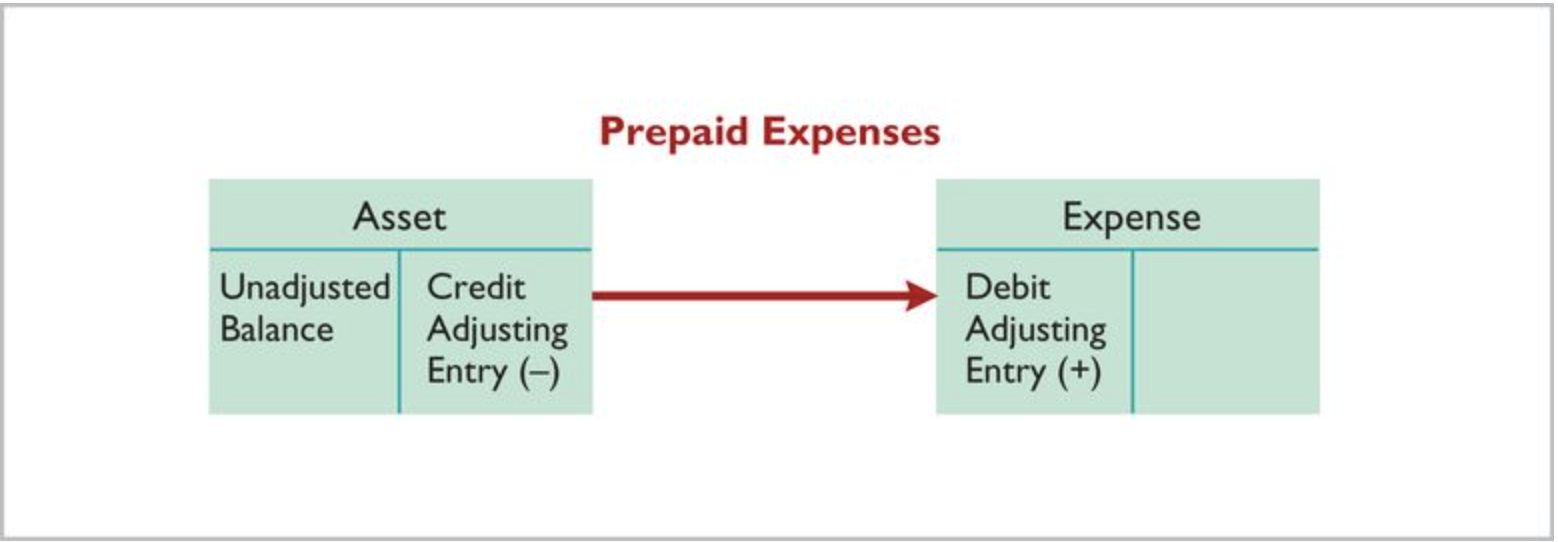

Prepaid Expenses/Prepayments- expenses paid in cash before they are used or consumed. When expenses are prepaid, an asset account is increased (debited) to show the service or benefit that the company will receive in the future. Examples of common prepayments are insurance, supplies, advertising, and rent. In addition, companies make prepayments when they purchase buildings and equipment.

Useful life- A company typically owns a variety of assets that have long lives, such as buildings, equipment, and motor vehicles. The period of service of the asset.

Depreciation- the process of allocating the cost of an asset to expense over its useful life.

Contra Asset Account- Accumulated Depreciation. Such an account is offset against an asset account on the balance sheet

Book Value- the difference between the cost of any depreciable asset and its related accumulated depreciation.

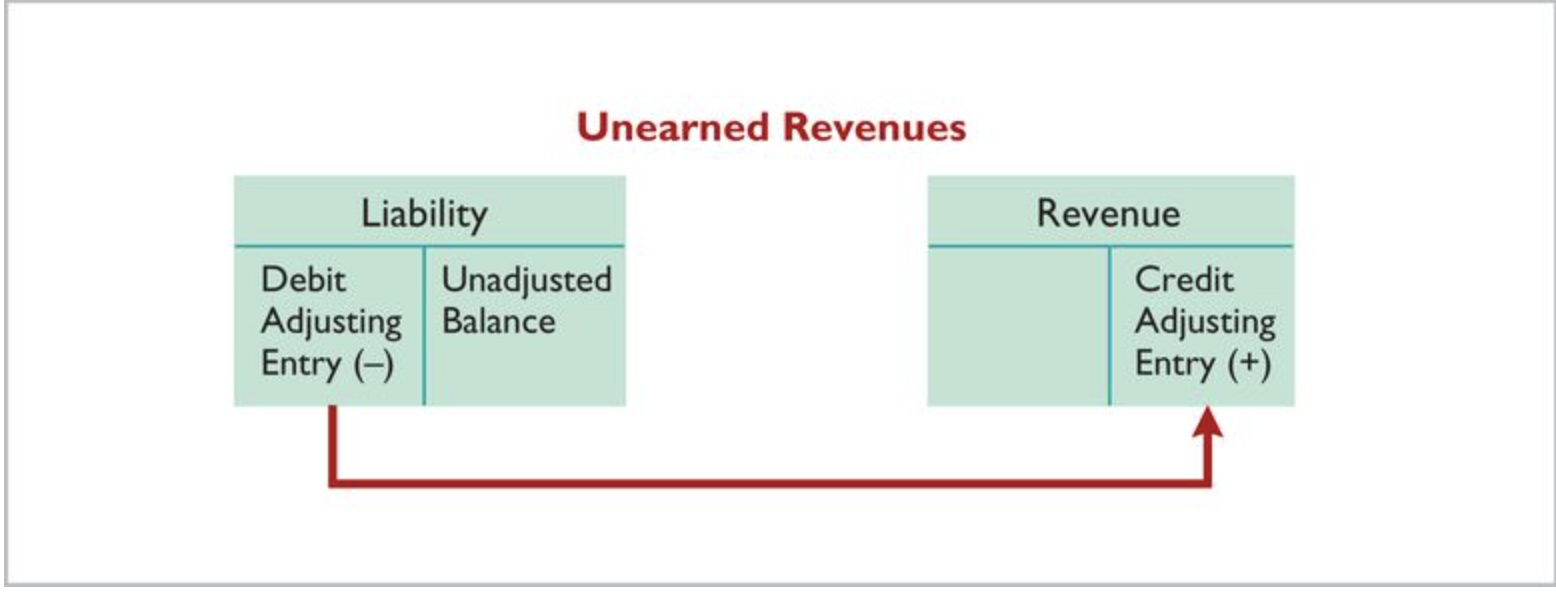

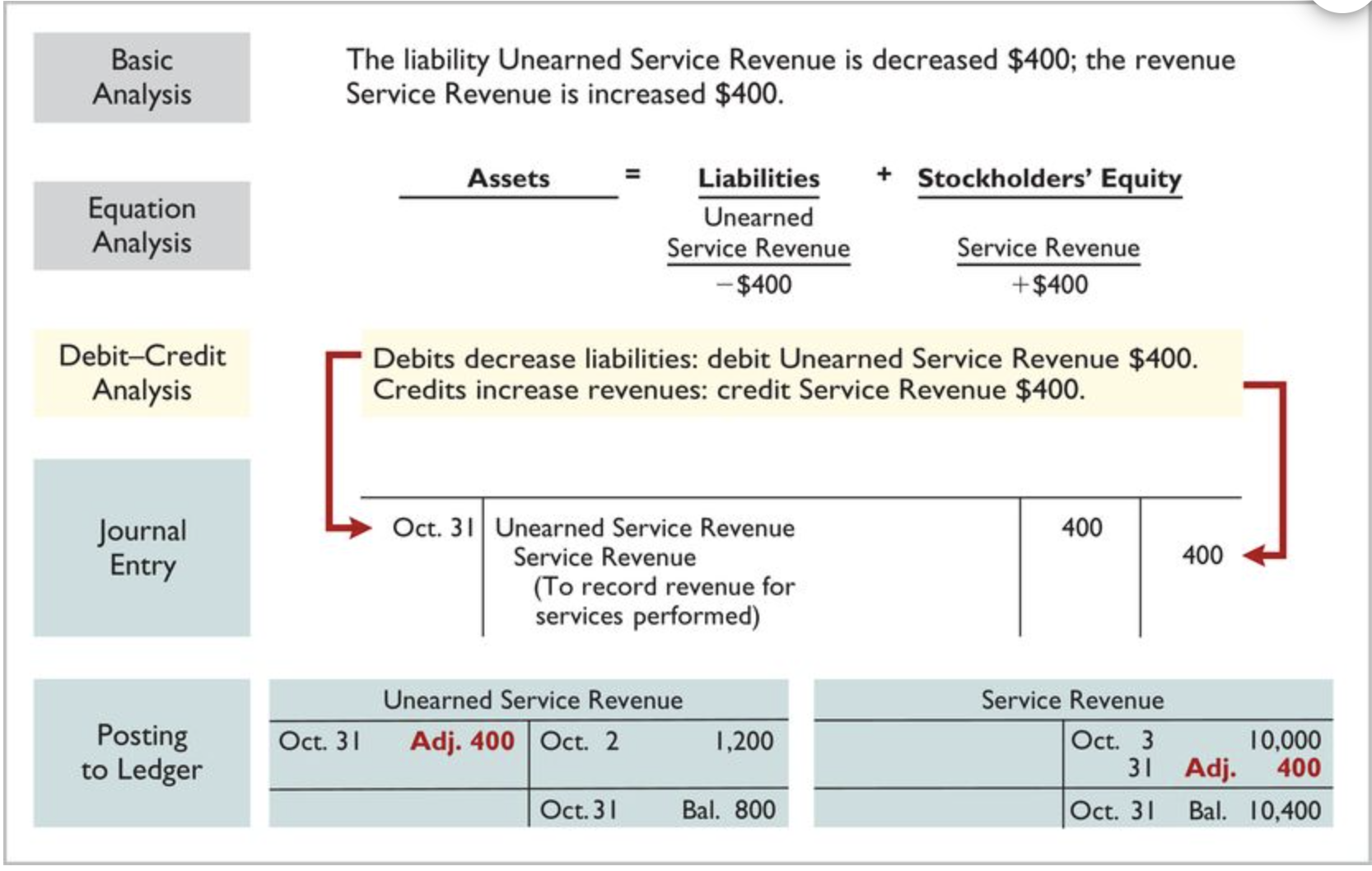

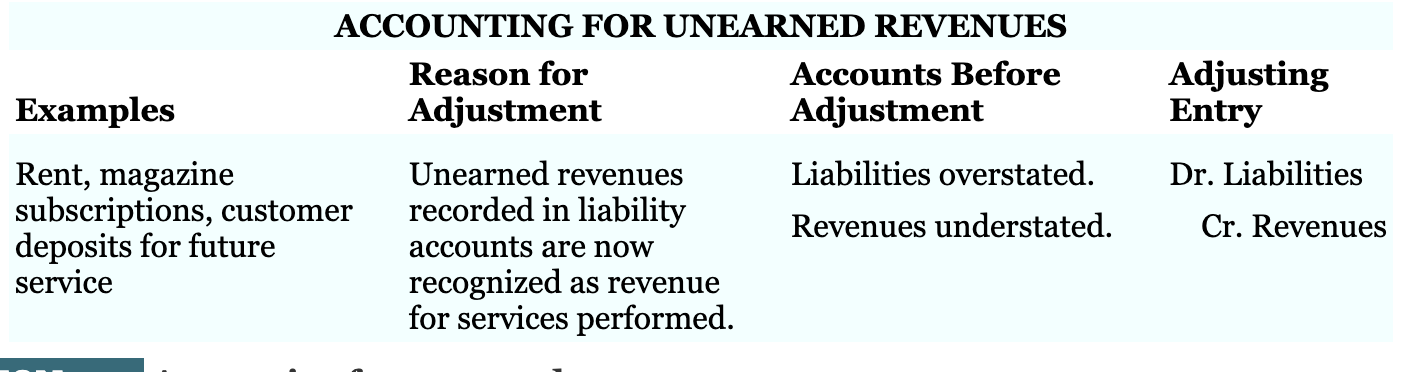

Unearned Revenues- Companies record cash received before services are performed by increasing (crediting) a liability account. he company has a performance obligation to transfer a service to one of its customers.

Notes:

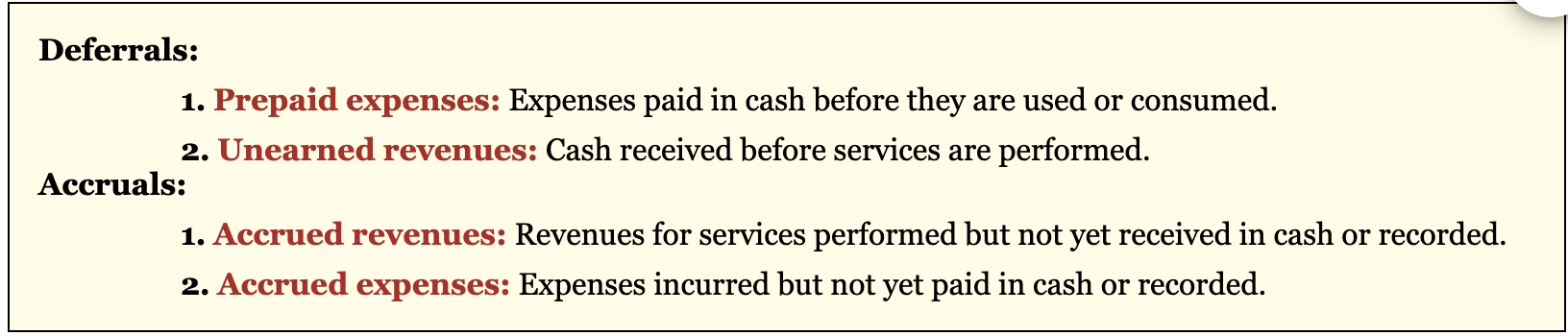

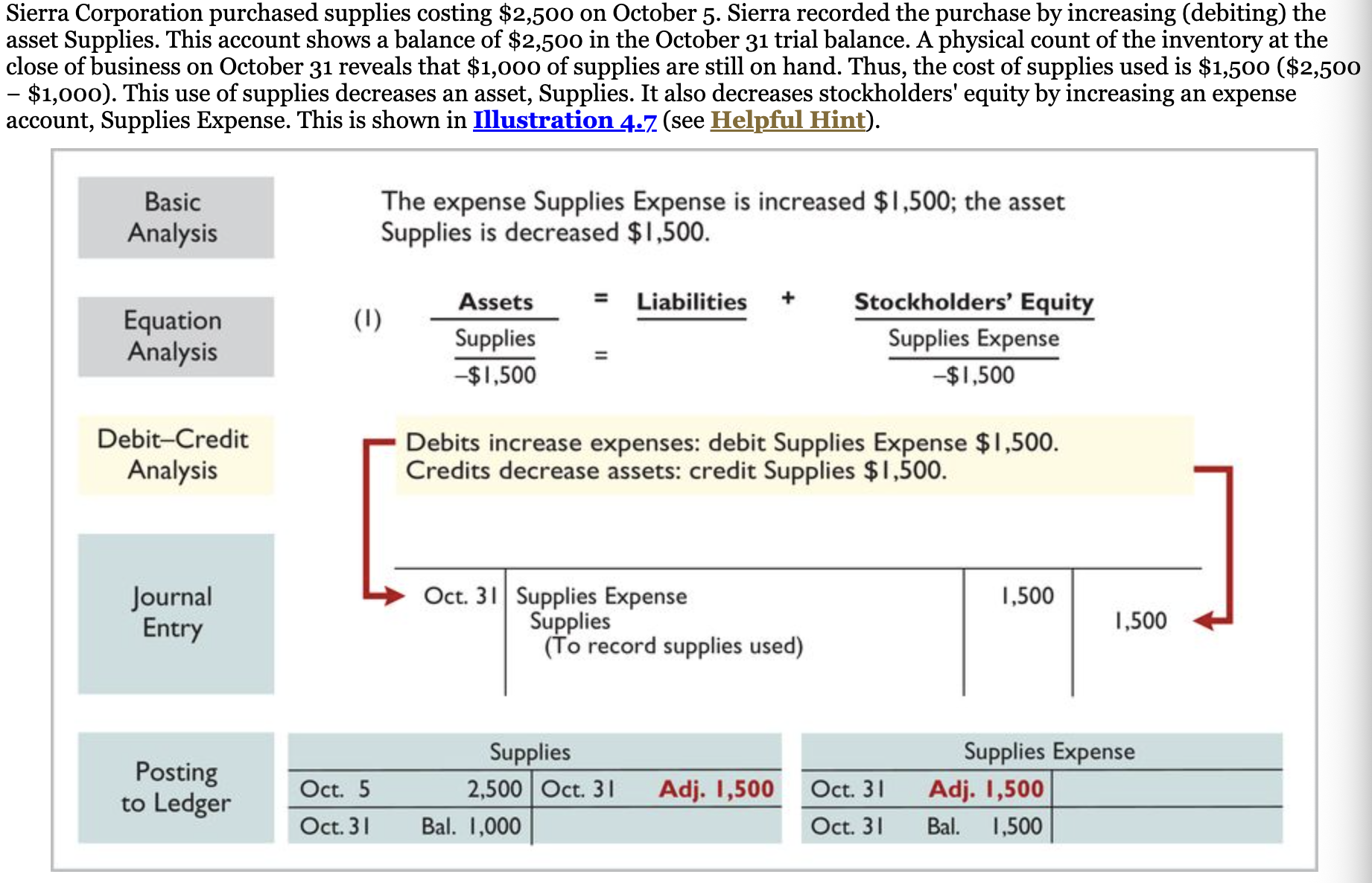

To defer is to postpone or delay. Deferrals are costs or rev. that are recognized at a date later than the point when cash was originally exchanged. Comps. make AE for deferred expenses to record the portion that was incurred during the period. Comp also make AE for deferred rev. to record services performed during the period. Two types of deferrals are prepaid expenses and unearned rev.

Prepaid Expenses:

Comp. record payments of expenses that will benefit more than one accounting period as assets. These expenses paid in cash before they are used or consumed. When expenses are prepaid, an asset account is increased (debited) to show the service or benefit that the company will receive in the future.

Things they are used for:

Insurance

Supplies

Advertising

Rent

Buildings

Equipment

Prepaid expenses are costs that expire either with the passage of time (rent and insurance) or through use (supplies). They make AE to record the expenses applicable to the current accounting period and to show the remaining amounts in the assets accounts.

An AE for prepaid expenses results in an increase (debit) to an expense account and a decrease (a credit) to an asset account.

Supplies is an expense recorded at the end of the accounting period. The difference between the unadjusted balance in the supplies (asset) account and the actual cost of supplies on hand represents the supplies used (an expense) for that period.

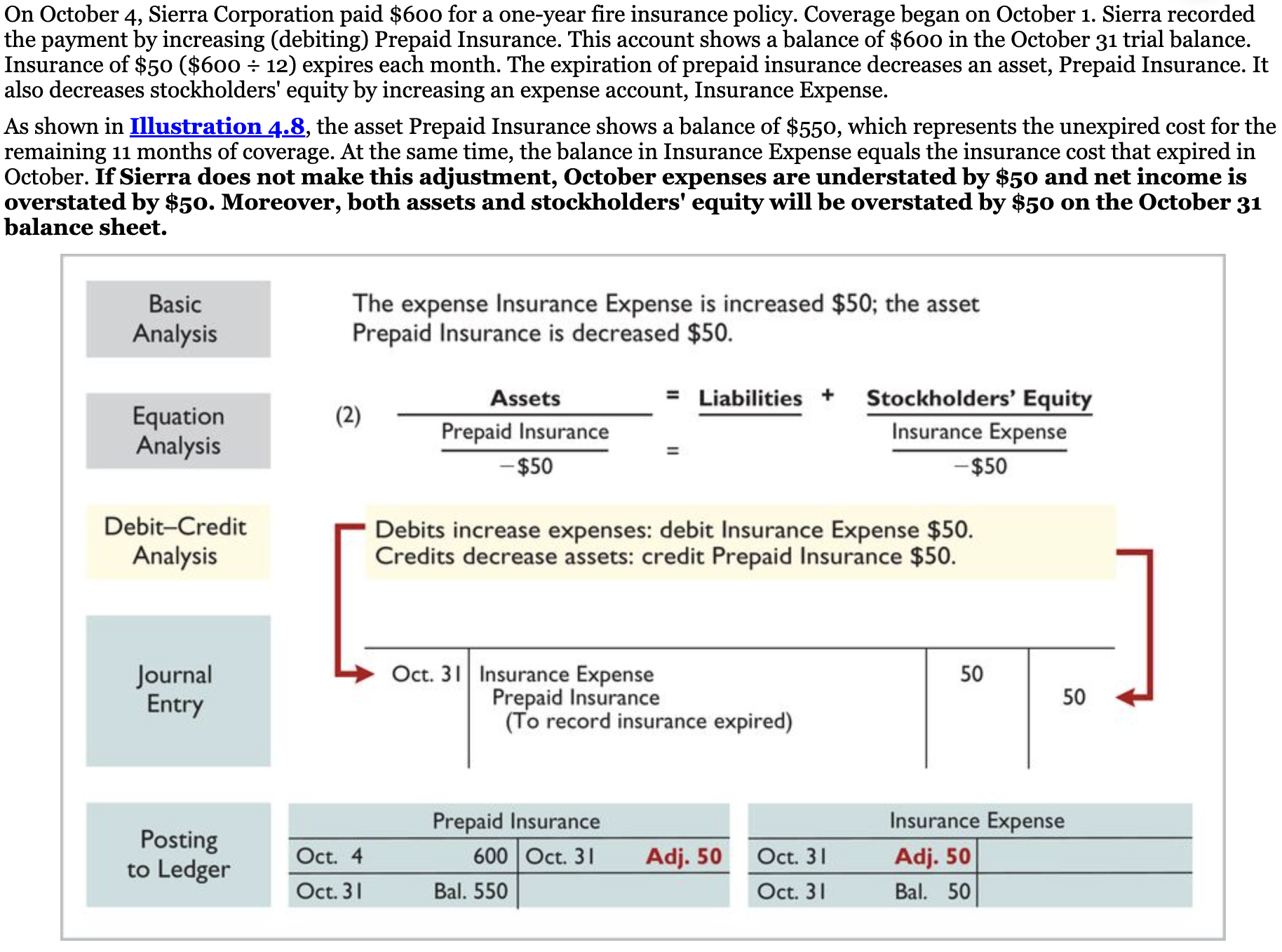

Insurance must be paid in advance. The cost of insurance paid in advance is recorded as an increase (debit) in the asset account prepaid insurance. At the fin. statement date, comp. increase (debit) Insurance Expense and decrease (credit) prepaid insurance for the cost of insurance that has expired during the period.

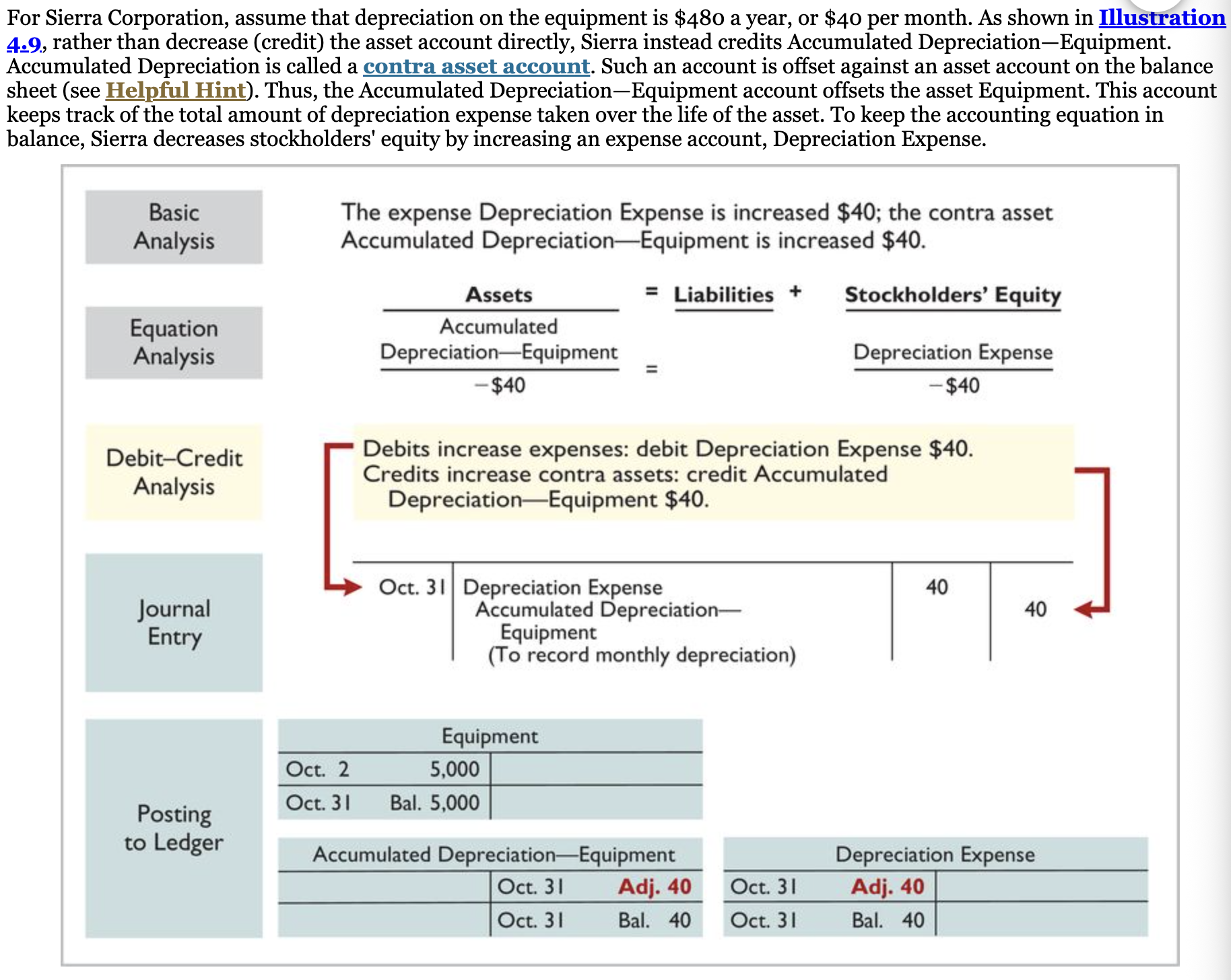

Depreciation is the process of allocating the cost of an asset to expense over its useful life. To follow the expense recognition principle, comp. allocate a portion of this cost as an expense during each period of the asset’s useful life. Is needed to recognize the cost that has been used (an expense) during the period and to report the unused cost (an asset) at the end of the period. Does not attempt to report the actual change in the value of the asset.

All contra accounts have increase, decreases, and normal balances opposite to the account to which they relate. Equipment is one. It is offset against Equipment on the balance sheet. The normal balance of a contra asset account is a credit. It discloses both the original cost of the equipment and total cost that has expired to date.

Book value means carrying value. Without this adjusting entry, total assets, total stockholders’ equity, and net income are overstated by 40 and depreciation expense is understated by 40.

Unearned Revenues:

Comp. has a performance obligation to transfer a service to one of its customers. Comp. record cash received before services are performed by increasing (crediting) a liability account.

May result in unearned rev.:

Rent

Magazine

Subscriptions

Customer deposits

When comp. receives payment for services to be performed in a future account period, it increases (credits) an unearned rev. account. It is a liability account to recognize an obligation that exists. The AE for unearned rev. results in a decrease (a debit) to a liability account and an increase (a credit) to a rev. account.

Learning Objective 3

Accrued revenues

Accrued expenses

Summary of basic relationships

Vocab:

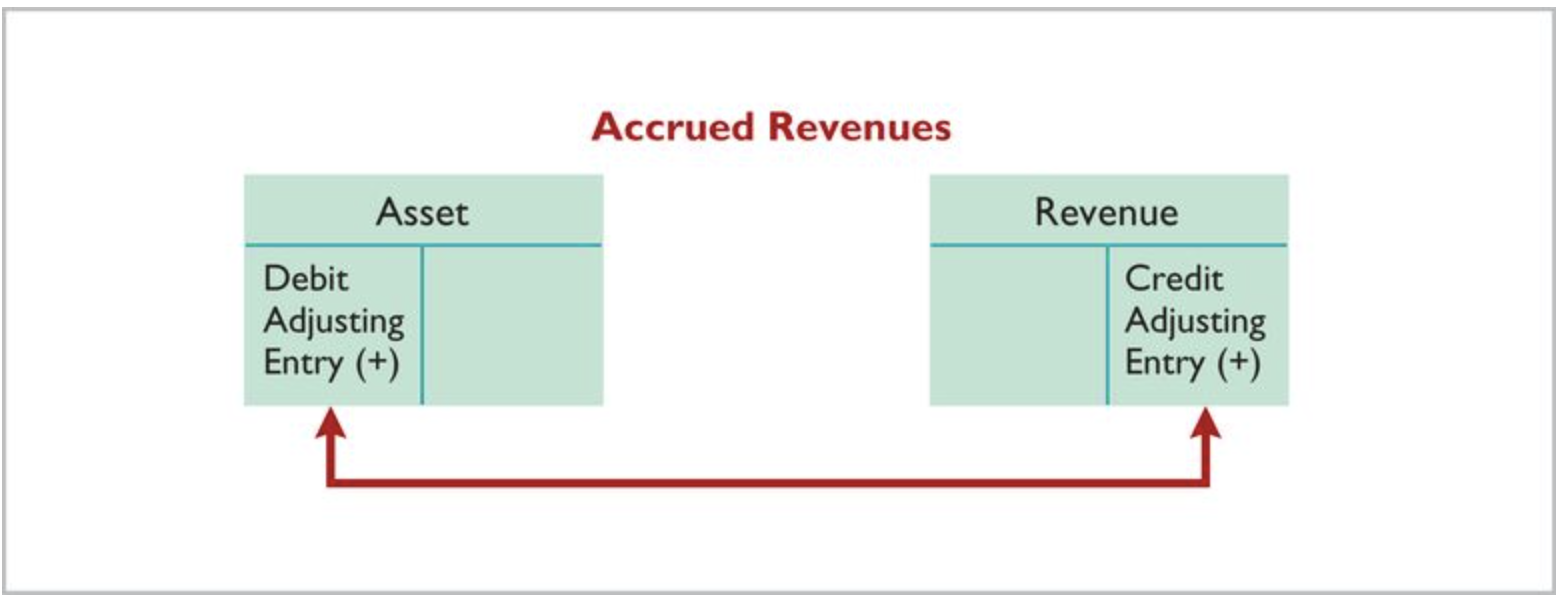

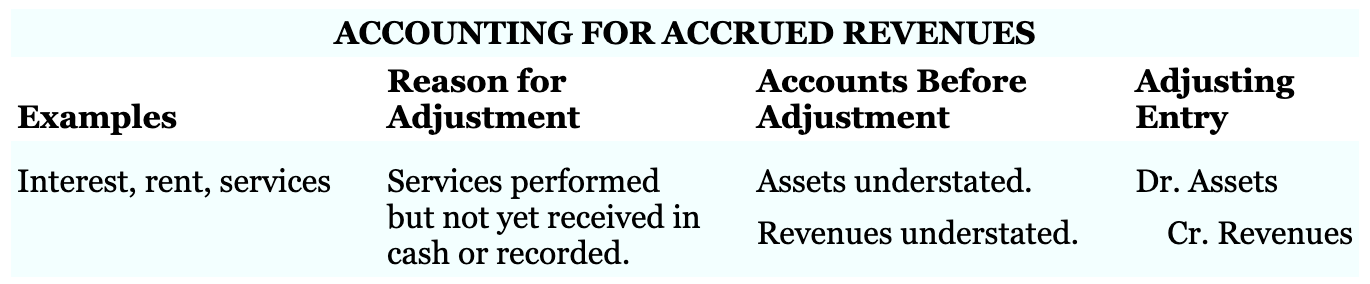

Accruals- Prior to an accrual adjustment, the revenue account (and the related asset account) or the expense account (and the related liability account) are understated. Thus, the adjusting entry for accruals will increase both a balance sheet and an income statement account

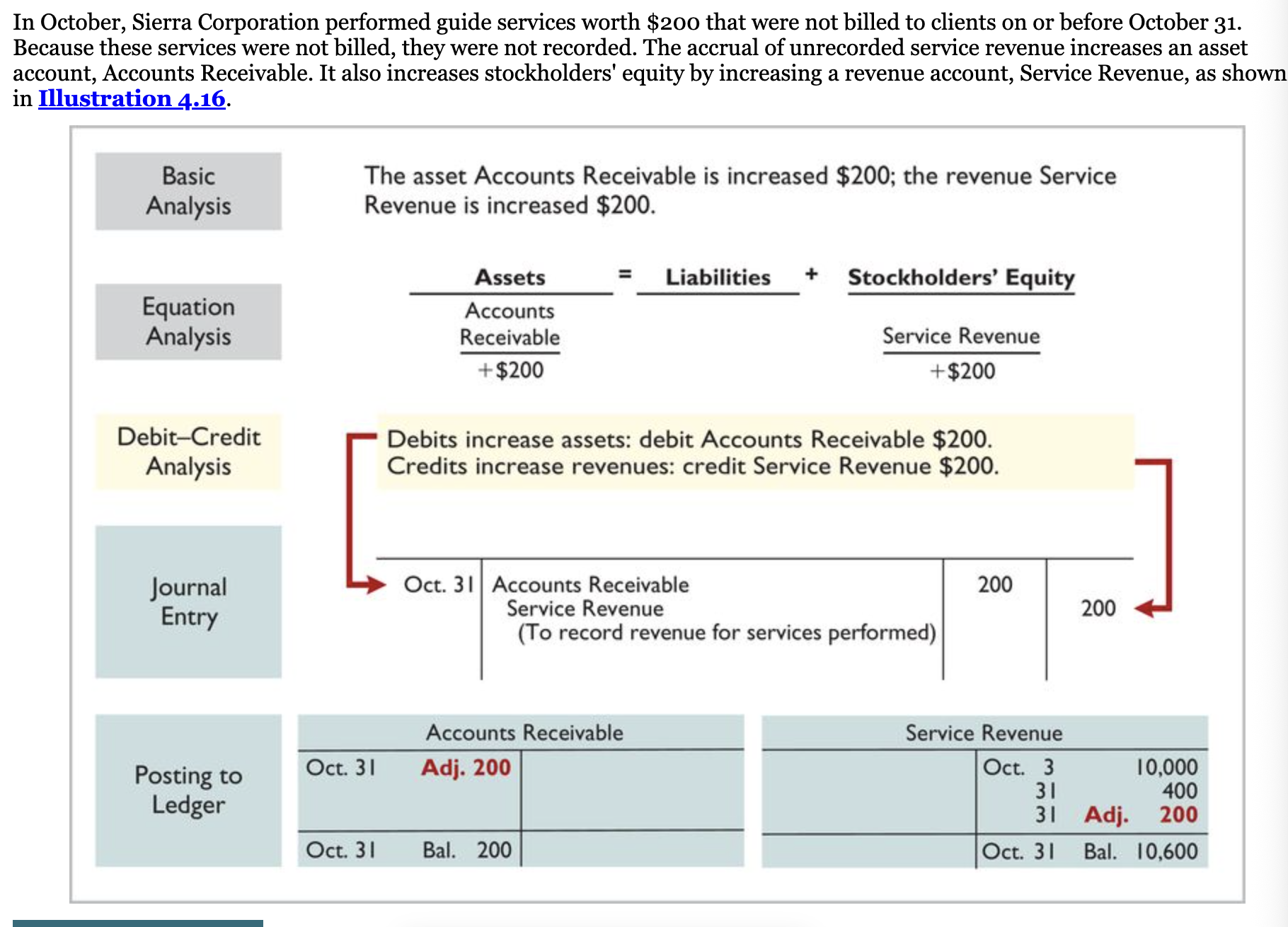

Accrued Revenues- Revenues for services performed but not yet recorded at the statement date. These are unrecorded because the earning of interest does not involve daily transactions. May result from services that have been performed but not yet billed or collected, as in the case of commissions and fees. These may be unrecorded because only a portion of the total service has been performed and the clients won't be billed until the service has been completed

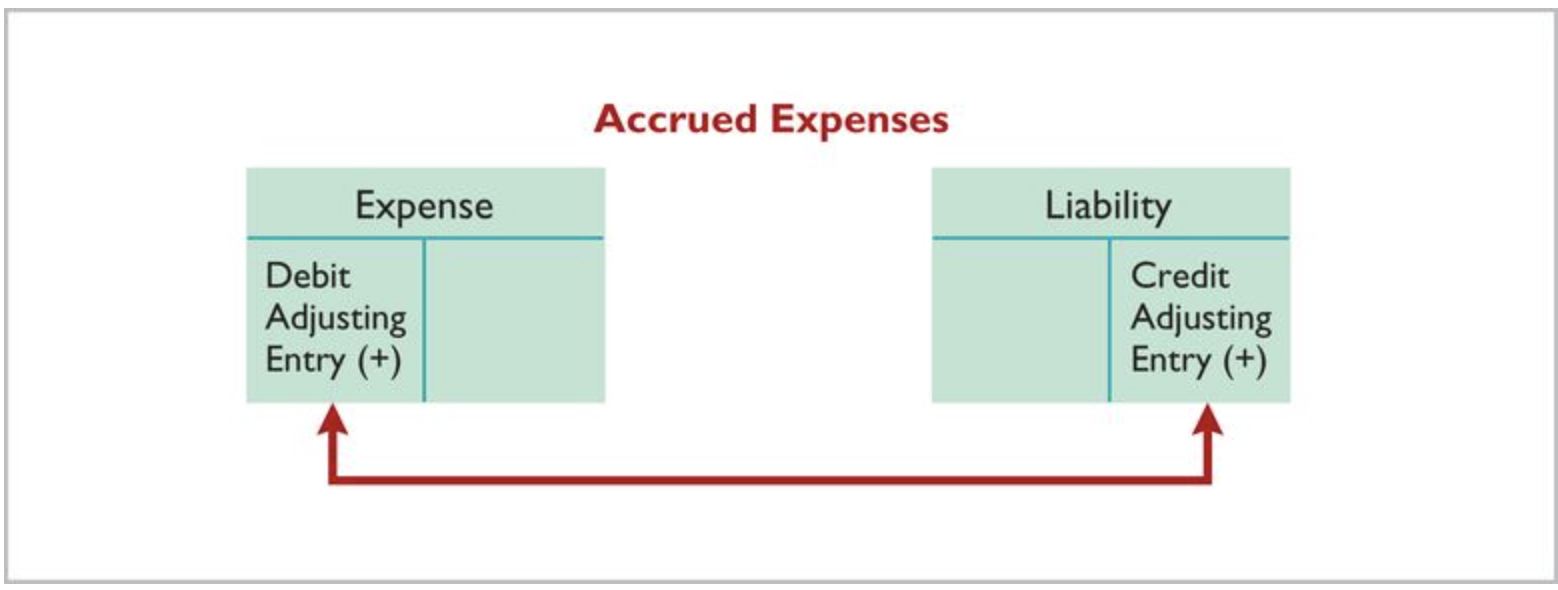

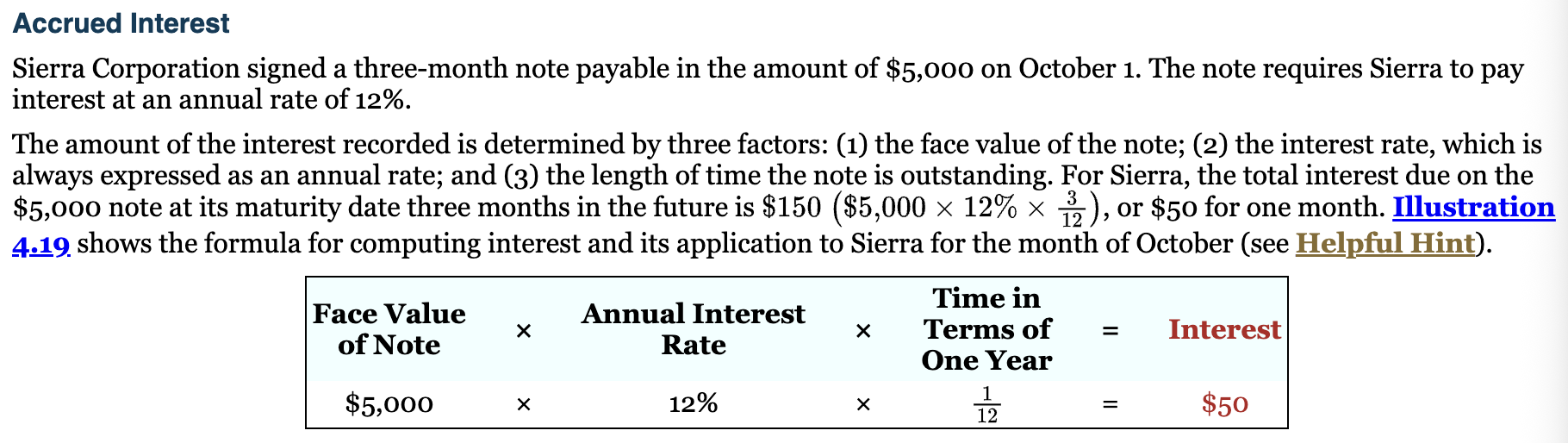

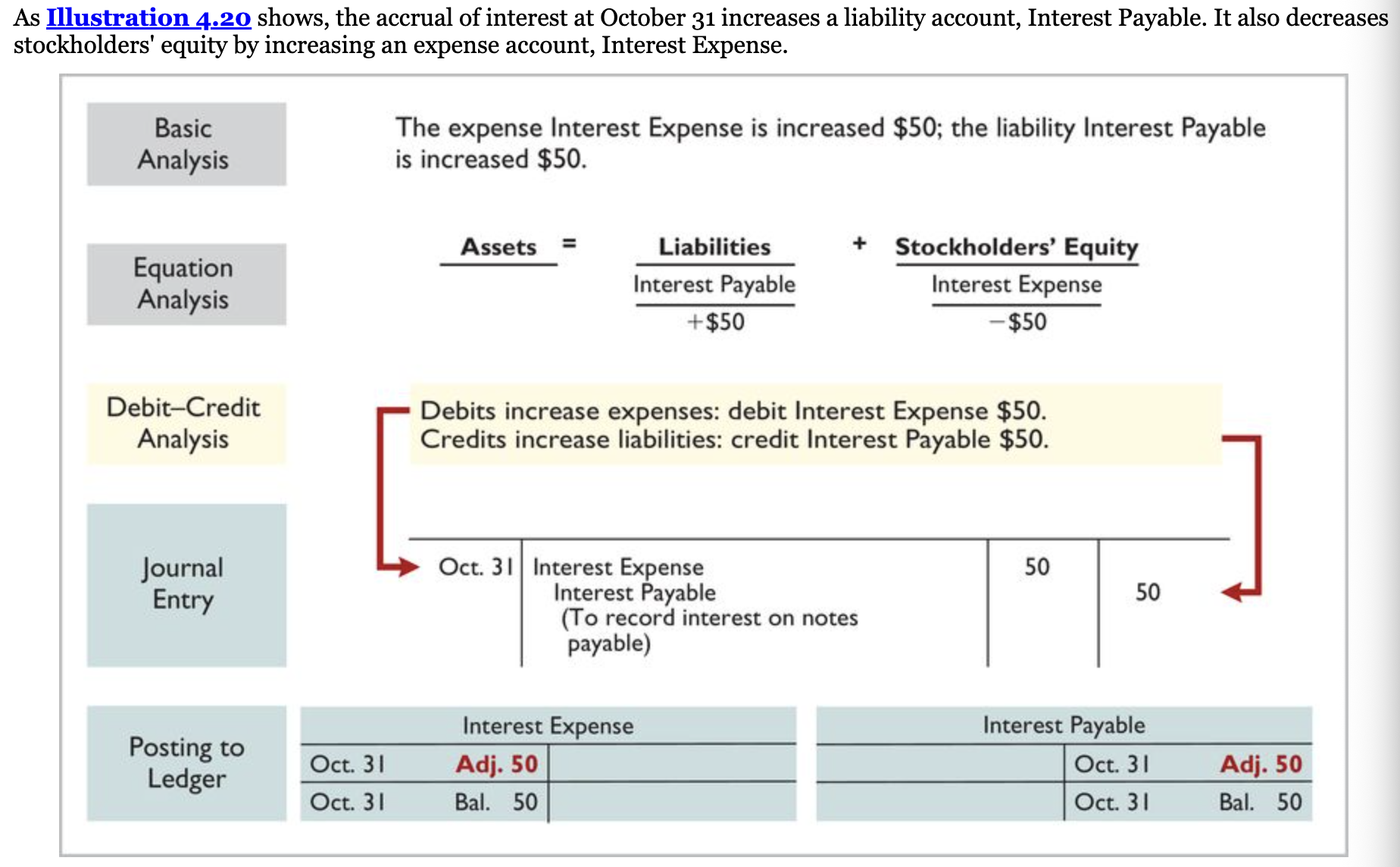

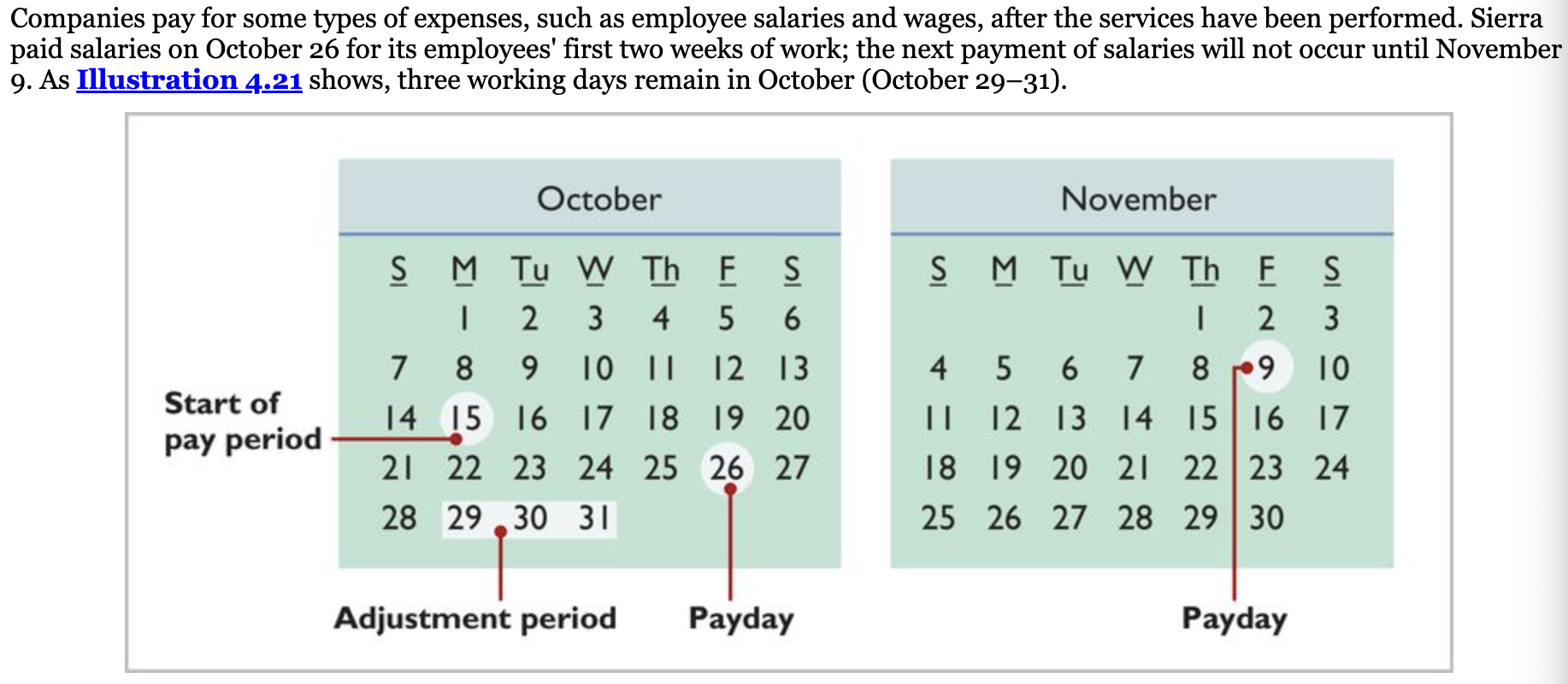

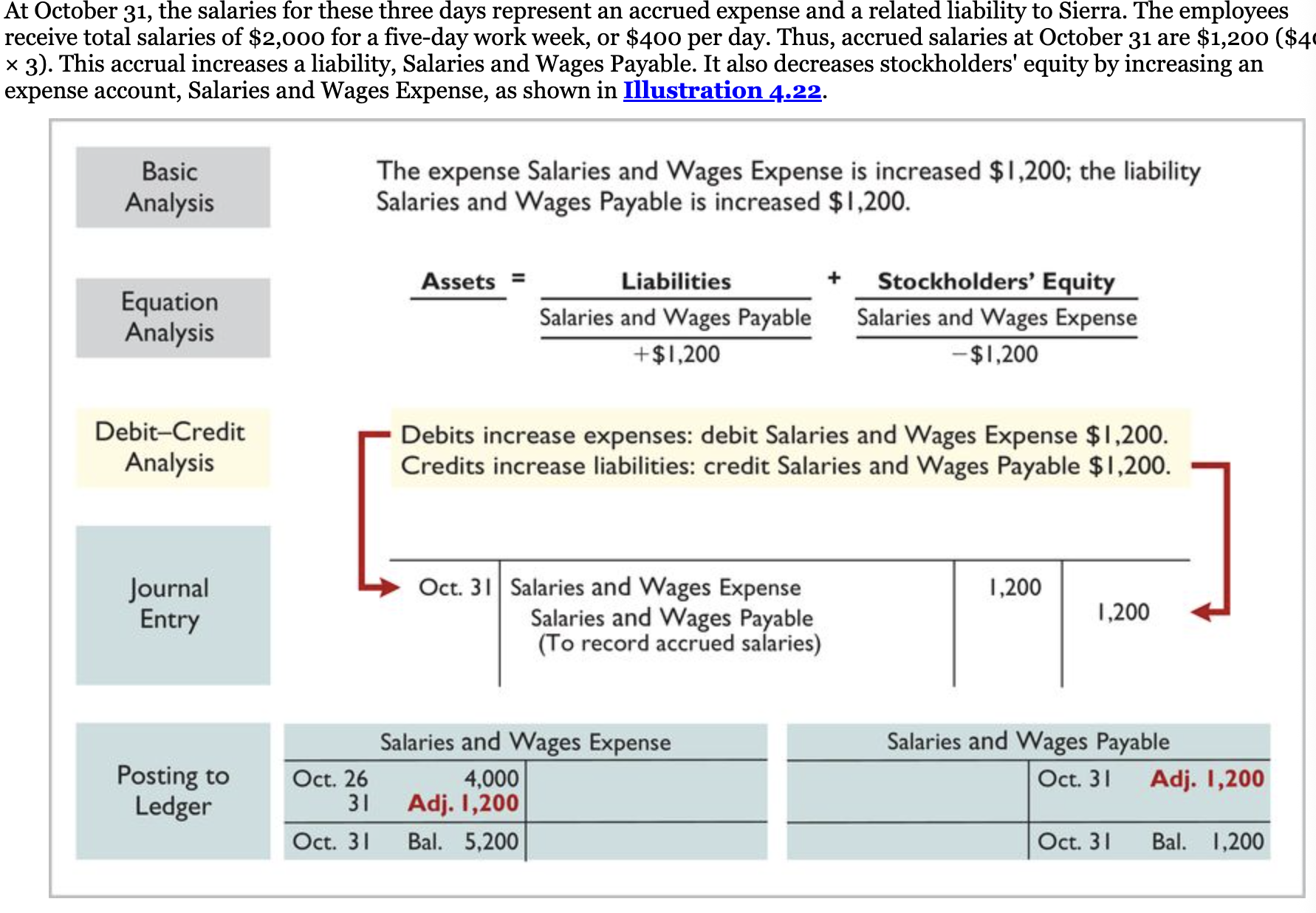

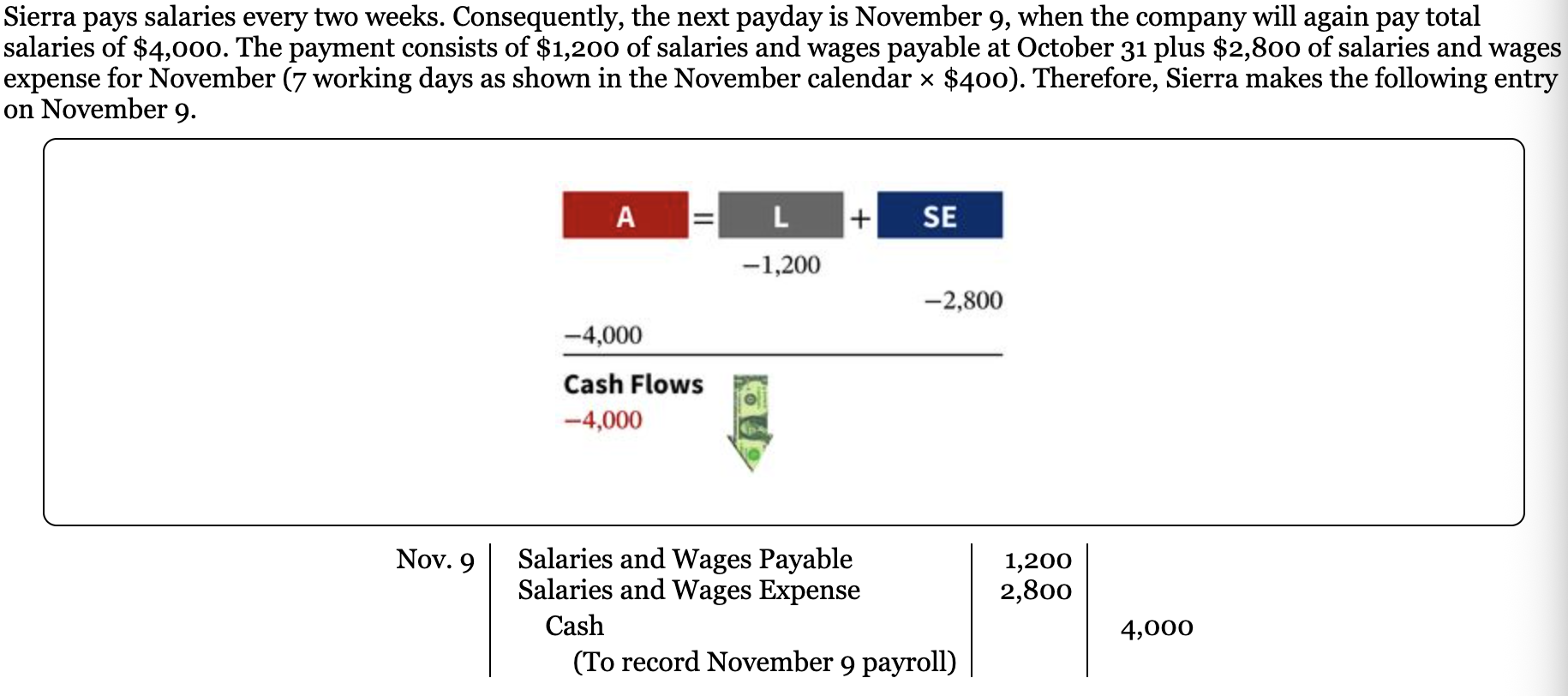

Accrued expenses- Expenses incurred but not yet paid or recorded at the statement date. Interest, taxes, utilities, and salaries are common examples of accrued expenses.

Notes:

Accrued Revenues:

An AE records the receivable that exists at the balance sheet date and the revenue for the services performed during the period. Both assets and revenues are understated. An AE for accrued rev. results in an increase (debit) to an asset and an increase (credit) to a rev. account. For accruals, there may be no prior entry, and the accounts requiring adjustment may both have zero balances prior to adjustment.

Without the AE, assets and stockholders’ equity on. the balance sheet and rev. and net income on the income statement are understated.

Accrued Expense:

Comp. make adjustments to record the obligations that exist at the balance sheet date and to recognize the expense that apply to the current accounting period. An AE for accrued expenses results in an increase (debit) to an expense account and an increase (credit) to a liability account.

In computing interest, we express the time period as a fraction of a year.

Comp. use the interest payable account, instead of crediting Notes payable, to disclose the two different types of obligations- interest and principal- in the accounts and statements.

Summary of the basic relationships:

Learning Objective 4

Preparing the adjusted trial balance

Preparing financial statements

Quality of earnings

Closing the books

Summary of the accounting cycle

Vocab:

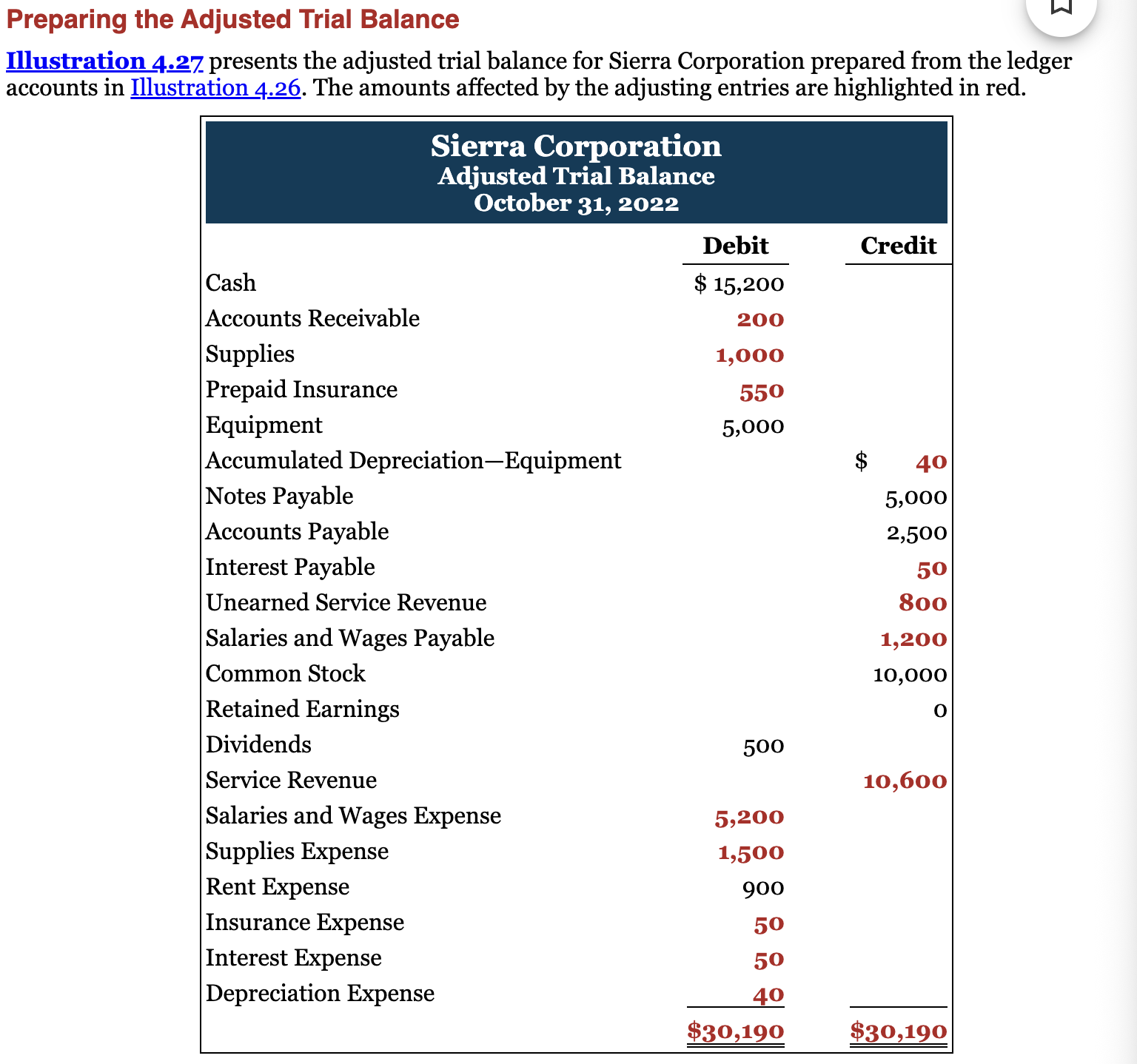

Adjusted Trial Balance- After a company has journalized and posted all adjusting entries, it prepares another trial balance from the ledger accounts.

Earning management- is the planned timing of revenues, expenses, gains, and losses to smooth out bumps in net income. The quality of earnings is greatly affected when a company manages earnings up or down to meet some targeted earnings number.

Quality of earnings- provides full and transparent information that will not confuse or mislead financial statement users.

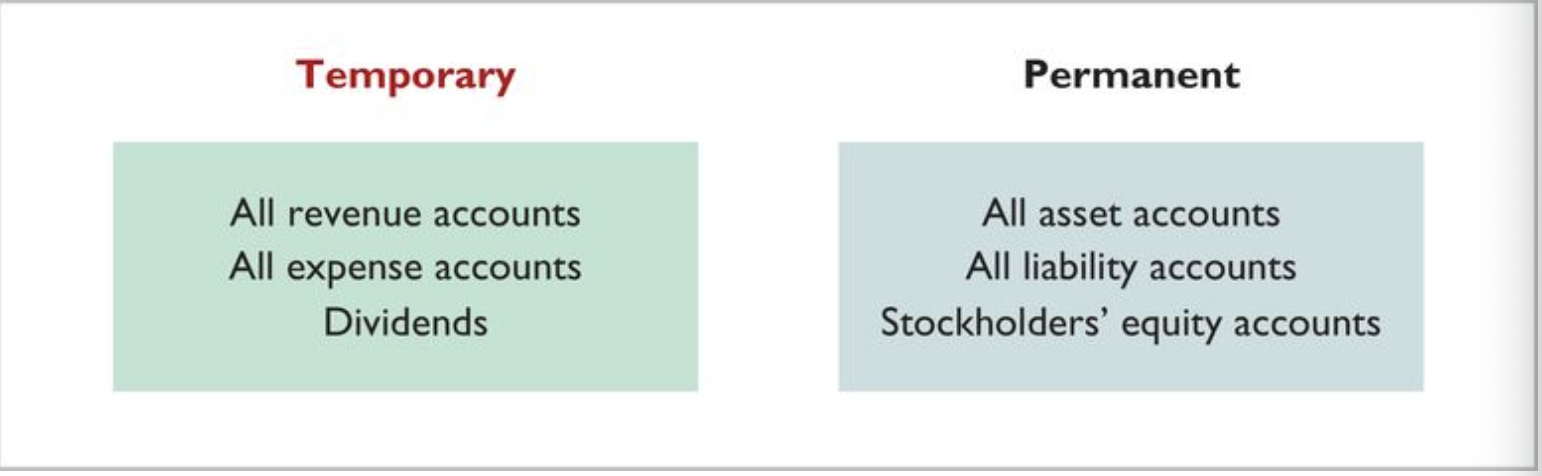

Temporary accounts- Because revenues, expenses, and dividends relate only to a given accounting period,

Permanent accounts- their balances are carried forward into future accounting periods

Closing entries- transfer net income (or net loss) and dividends to Retained Earnings, so the balance in Retained Earnings agrees with the retained earnings statement

Income summary- companies close the revenue and expense accounts to another temporary account

Post-closing trial balance- After a company journalizes and posts all closing entries, it prepares another trial balance

Notes:

Adjusted Trial Balance:

After a comp. has journalized and posted all adjusting entries, it prepares another trial balance from the ledger accounts.

It shows the balances of all accounts, including those adjusted, at the end of the accounting period.

The purpose of an adjusted trial balance is to prove the equality of the total debit balances and total credit balances in the ledger after all adjustments.

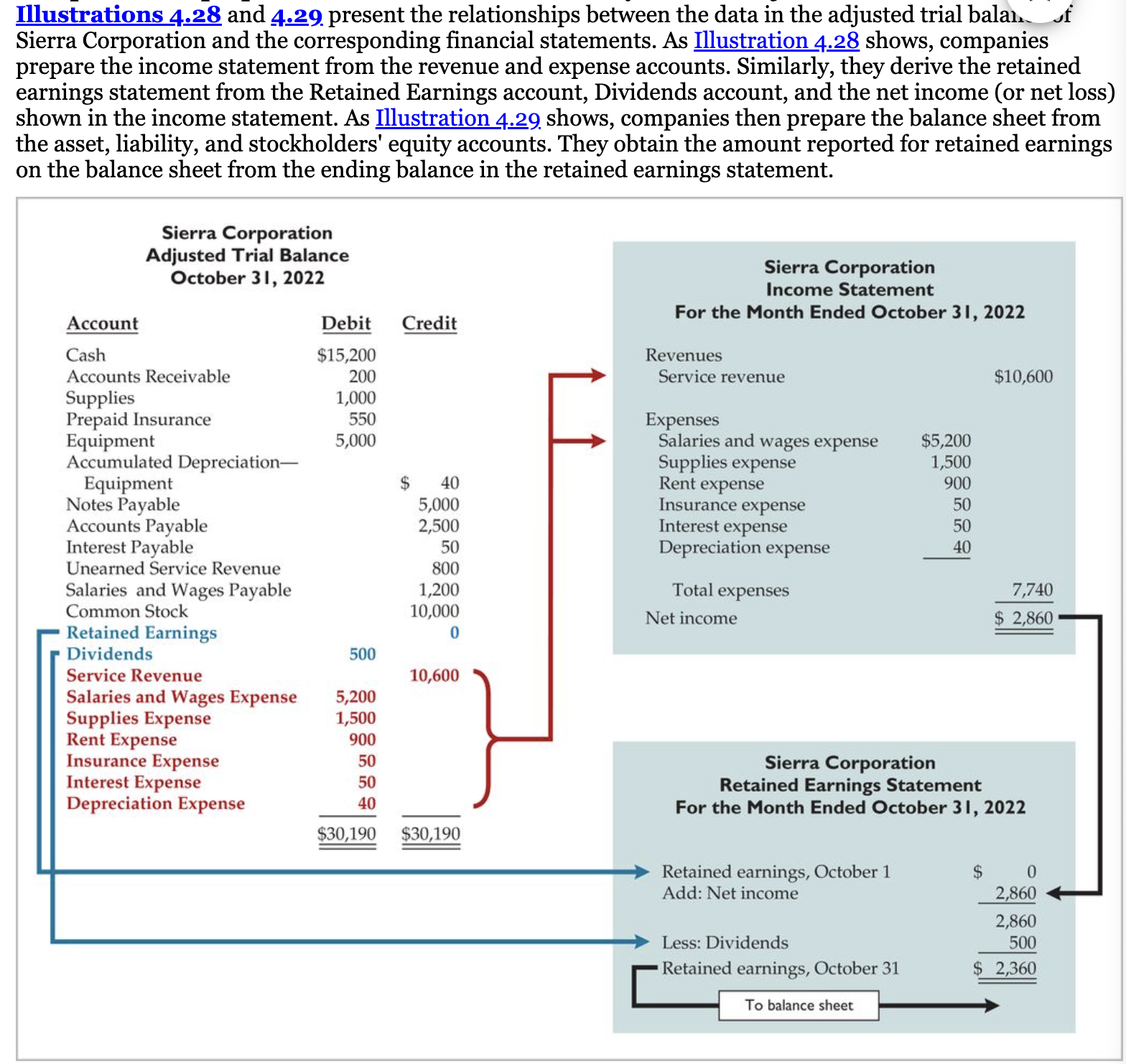

The adjusted trial balance is the primary basis for the preparation of fin. statements.

Preparing Fin. Statements:

Comp. can prepare fin. statements directly from an adjusted trial balance.

Quality of Earnings:

Earnings management is the planned timing of revenues, expenses, gains, and losses to smooth out bumps in net income.

The quality of earnings is greatly affected when a company manages earnings up or down to meet some targeted earnings number.

A comp. has a high quality of earnings provides full and transparent info. that will not confuse or mislead fin. statement users.

A comp. with questionable quality of earnings may mislead investors and creditors. As a result, investors and creditors lose confidence lose confidence in fin. reporting, and it becomes difficult for our cap. markets to work efficiently.

Comps manage earnings in a variety of ways: one-time items to prop up earnings numbers, inflate revenue numbers in the short-run to the detriment of the long-run, and using improper adjusting entries which uses adjusted entries to increase net income by reclassifying liabilities as rev. and reclassifying expenses as assets.

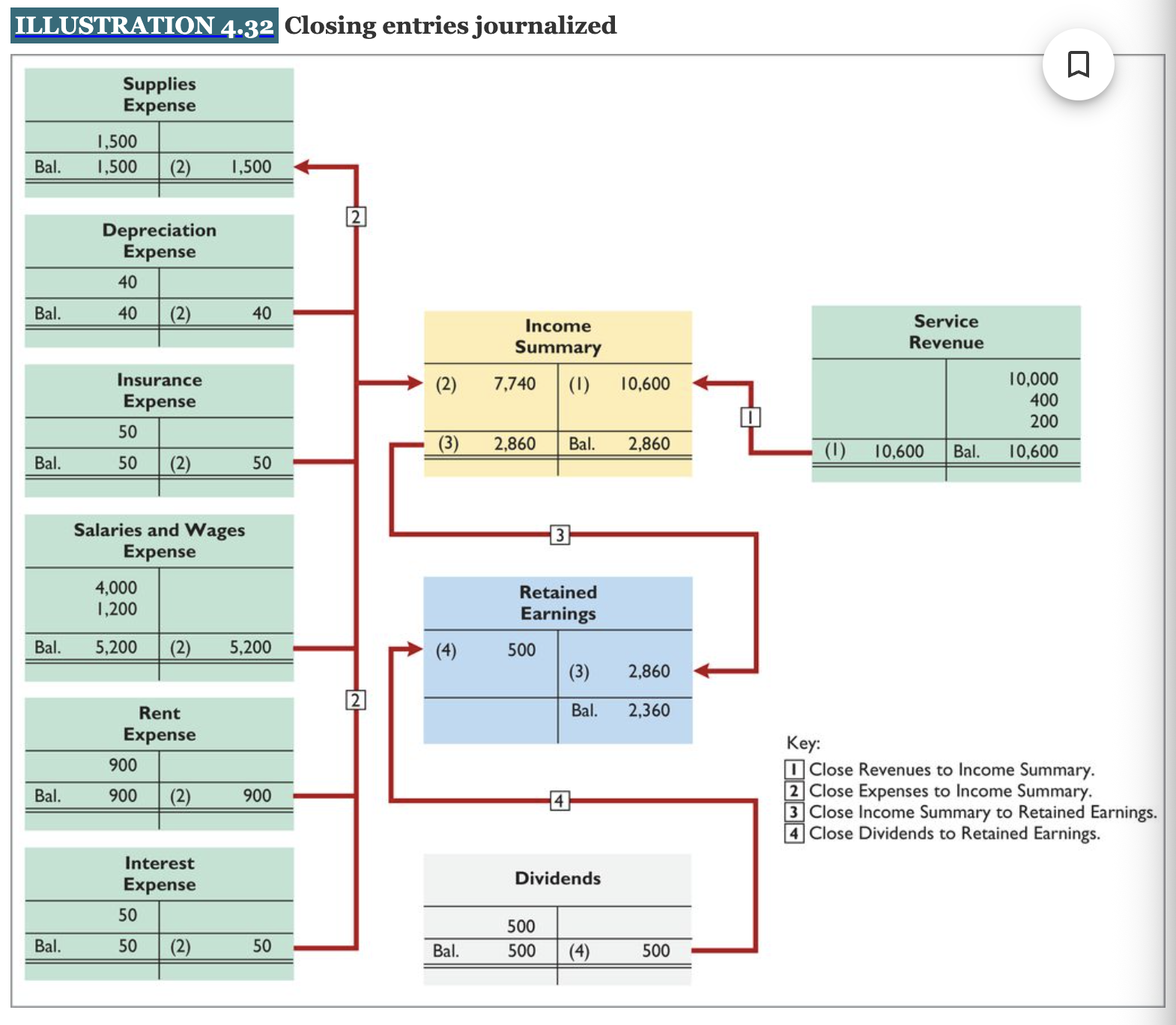

Closing the Books:

Temp accounts (nominal) uses rev., expenses, and dividends relate only to a given accounting period.

In contrast, all balance sheet accounts are considered permanent accounts (real) because their balances are carried forward into future accounting periods.

Preparing Closing Entries:

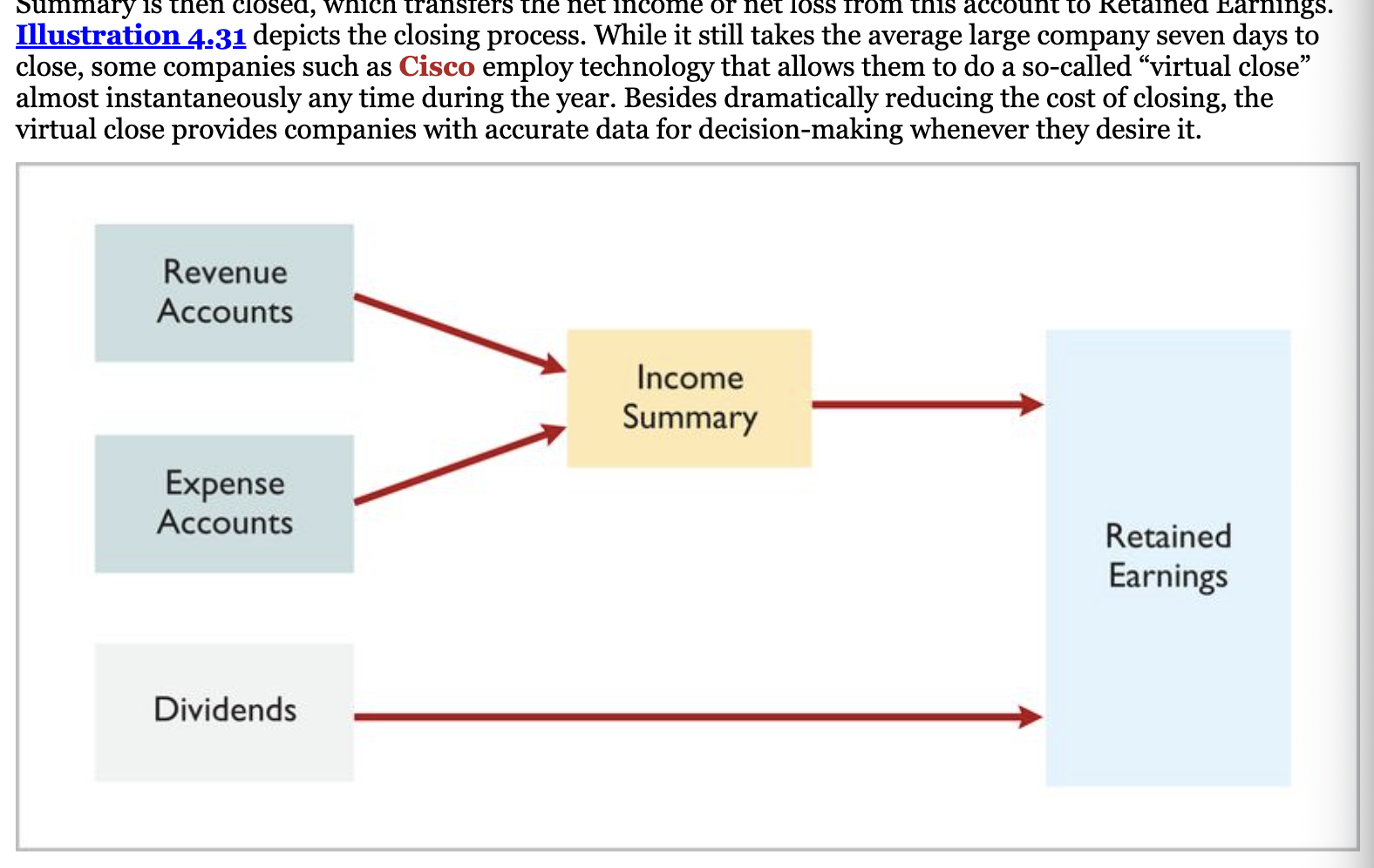

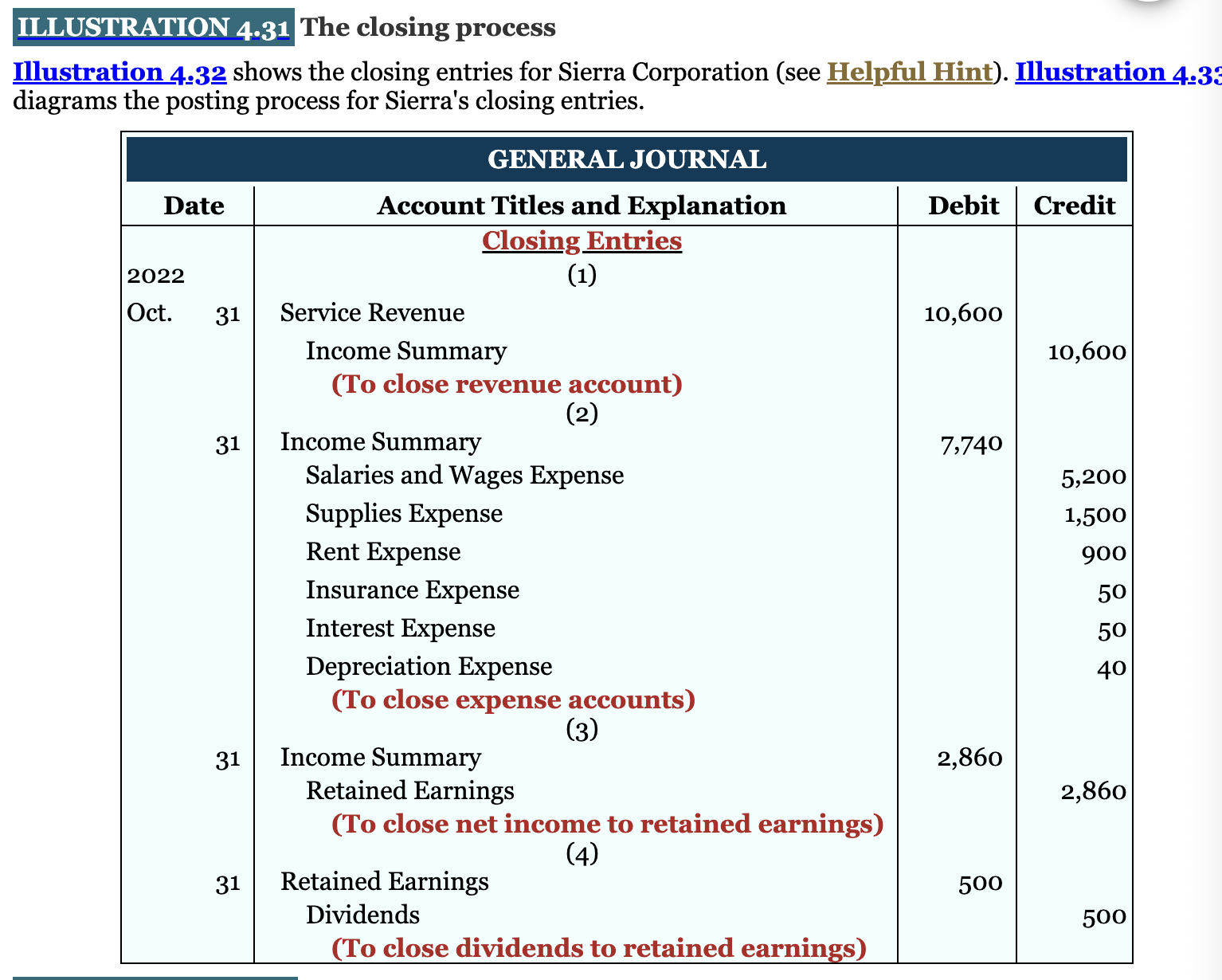

At the end of the accounting period, comp. transfer the temp. account balances to the permanent stockholders’ equity account -retained earnings- through the preparation of closing entries.

Closing entries transfer net income and dividends to retained earnings, so the balance in retained earnings agrees with the retained earnings statement.

Zero balance in each temp. account in updating retained earnings to its correct ending balance. As a result, these accounts are ready to accumulate data about rev., expenses, and dividends that occur in the next accounting period. Permanent accounts are not closed.

When comp. prepare closing entries, they could close each income statement account directly to retained earnings. However, they do income summary because they close the rev. and expense accounts to another temp. account. (income summary).

The balance in Income summary is the net income or loss for the accounting period.

Income summary is then closed, which transfer the net income or net loss from this account to Retained Earnings.

Preparing a post-closing trial balance:

After comp. journalizes and posts all closing entries, it prepares another trial balance, called a post-closing trail balance from the ledger.

It list of all permanent accounts and their balances after closing entries are journalized and posted.

The purpose of this trial balance is to prove the equality of the total debit balance and total credit balances of the permanent account balances that the comp. carries forward into the next accounting period.

Since all temp. accounts will have zero balances, the post-closing trial balance will contain only permanent-balance sheet-accounts.

Ch 5 Merchandising Operations and the Multiple-Step Income Statement

Learning Objective 1

Vocab:

Notes:

Learning Objective 2

Vocab:

Notes:

Learning Objective 3

Vocab:

Notes:

Learning Objective 4

Vocab:

Notes:

Learning Objective 5

Vocab:

Notes:

Learning Objective 6

Vocab:

Notes:

Learning Objective 7

Vocab:

Notes:

Learning Objective 8

Vocab:

Notes:

Chapter 6 Reporting and Analyzing Inventory

Learning Objective 1

Classifying inventory

Determine inventory quantities

Vocab:

Finished good inventory- Manufactured items that are completed and ready for sale

Work in process- Portion of manufactured inventory that has been placed into the production process but it not yet complete.

Raw materials- Basic goods that will be used in production but have not yet been placed into production.

Just-in-time (JIT) Inventory- Companies manufacture or purchase goods only when needed.

Goods in transit- On board a truck, train, ship or plane

FOB (free on board) shipping point- Ownership of the goods passes to the buyer when the public carrier accepts the goods from the seller.

FOB destination- Ownership of the goods remains with the seller until the goods reach the buyer.

Consigned goods-Hold the goods of other parties and try to sell the good for them for a fee, but without taking ownership of the goods.

Notes:

Classifying Inventory:

Two characteristics: 1. they are owned by the comp. 2. they are in a form ready for sale to customers in the ordinary course of business.

Merchandise inventory is describing the many different items that make up the total inventory.

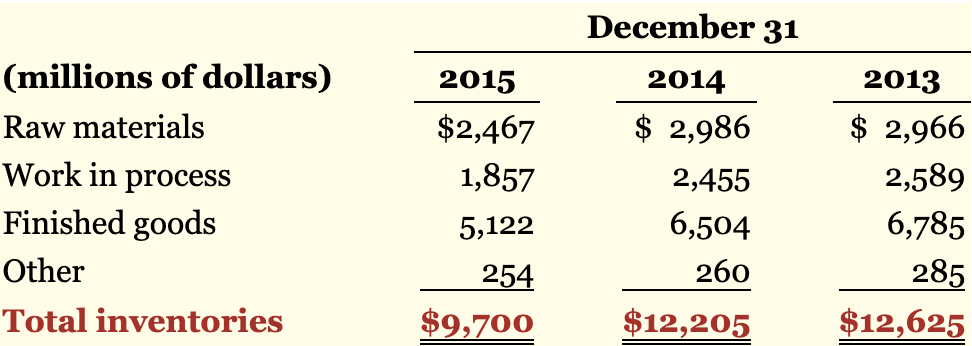

Manufacturing company, some inventory may not yet be ready for sale. It can be classified into 3 things: Finished goods inventory, work in process, and raw materials.

All classified under current assets.

Examples: Low levels of raw materials and high levels of finished goods suggest that management’s believes it has enough inventory on hand and production will be slowing down.

Vice Versa. High Levels of Raw materials and low levels of finished goods signals that management is planning to step up production.

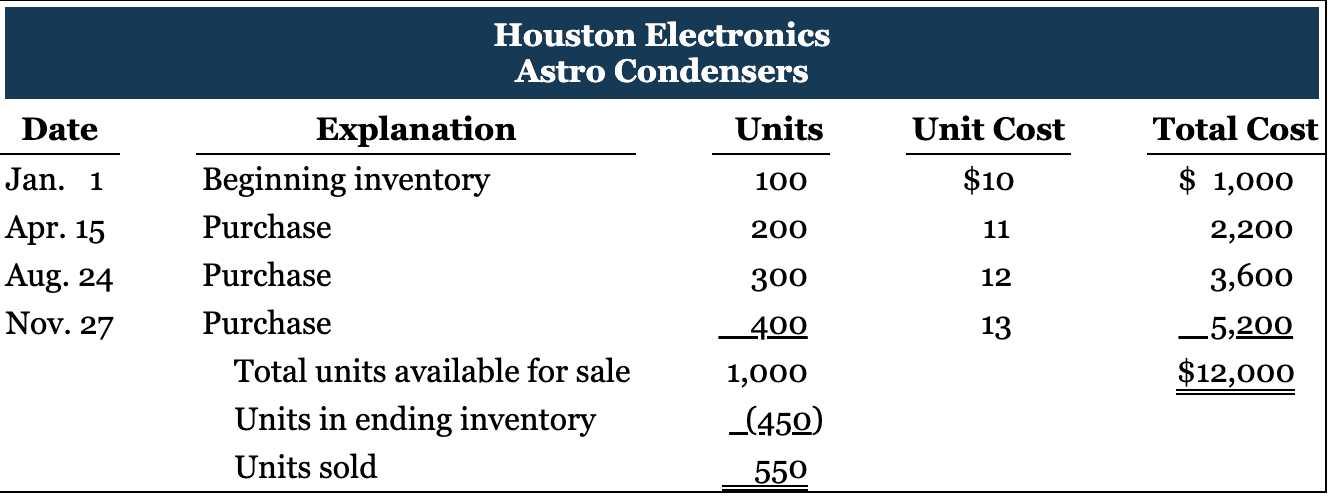

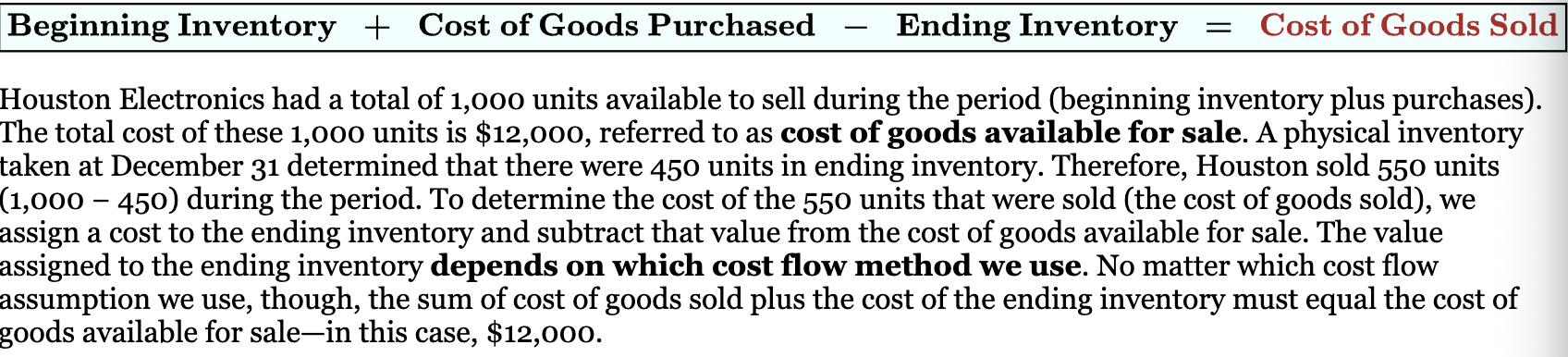

Determining Inventory Quantities:

If using a perpetual system. comps. take a physical inventory because

To check the accuracy of their perpetual inventory records

To determine the amount of inventory lost due to wasted raw materials, shoplifting, or employee theft.

Periodic inventory system take a physical inventory for two different purposes:

Determine the inventory on hand at the balance sheet date

to determine the cost of goods sold for the period

It involves in two steps: taking physical inventory of goods on hand and determining the ownership of goods.

Comps. take physical inventory at the end of the accounting period. It involves counting, weighing or measuring each kind on hand.

Learning Objective 2

Specific identification

Cost flow assumptions

FInancial statements and tax effects

Using inventory cost flow methods consistently

Vocab:

Specific identification method- An actual physical flow costing method in which particular items sold and items still in inventory are costed to arrive at cost of goods sold and ending inventory.

First-in, First-out (FIFO) method- An inventory costing methods that assumes that the earliest goods purchased are the first to be sold

Last-in, first-out (LIFO) method- An inventory costing method that assumes that the latest goods purchased are the first to be sold.

Average-cost method- allocates the cost of goods available for sales on the basis of the weighted-average unit cost.

Weight-average unit cost- COG for Sale divided by Total Unit Available for Sale.

Consistency concept- Comps. use the same accounting principles and methods from year to year.

Notes:

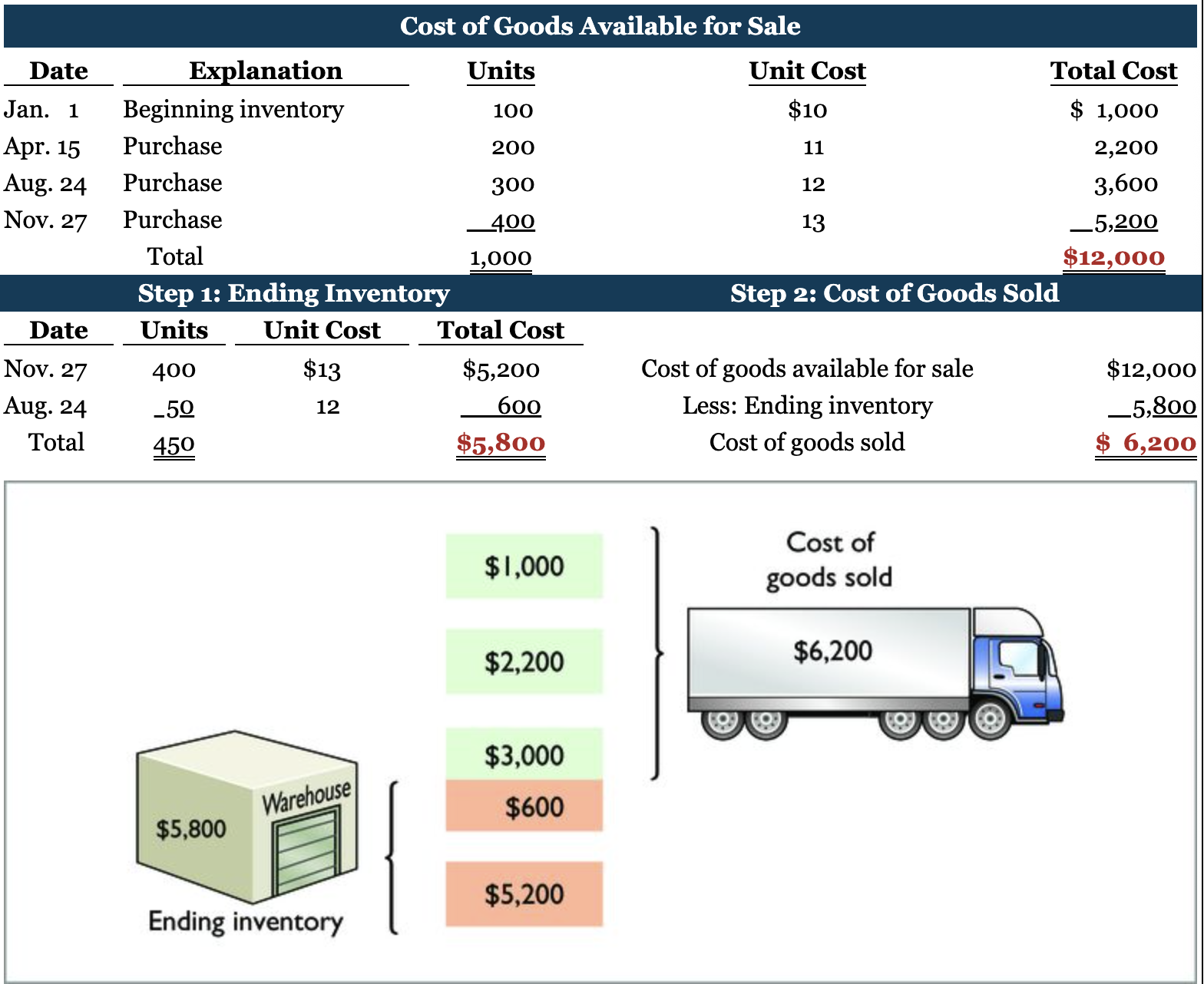

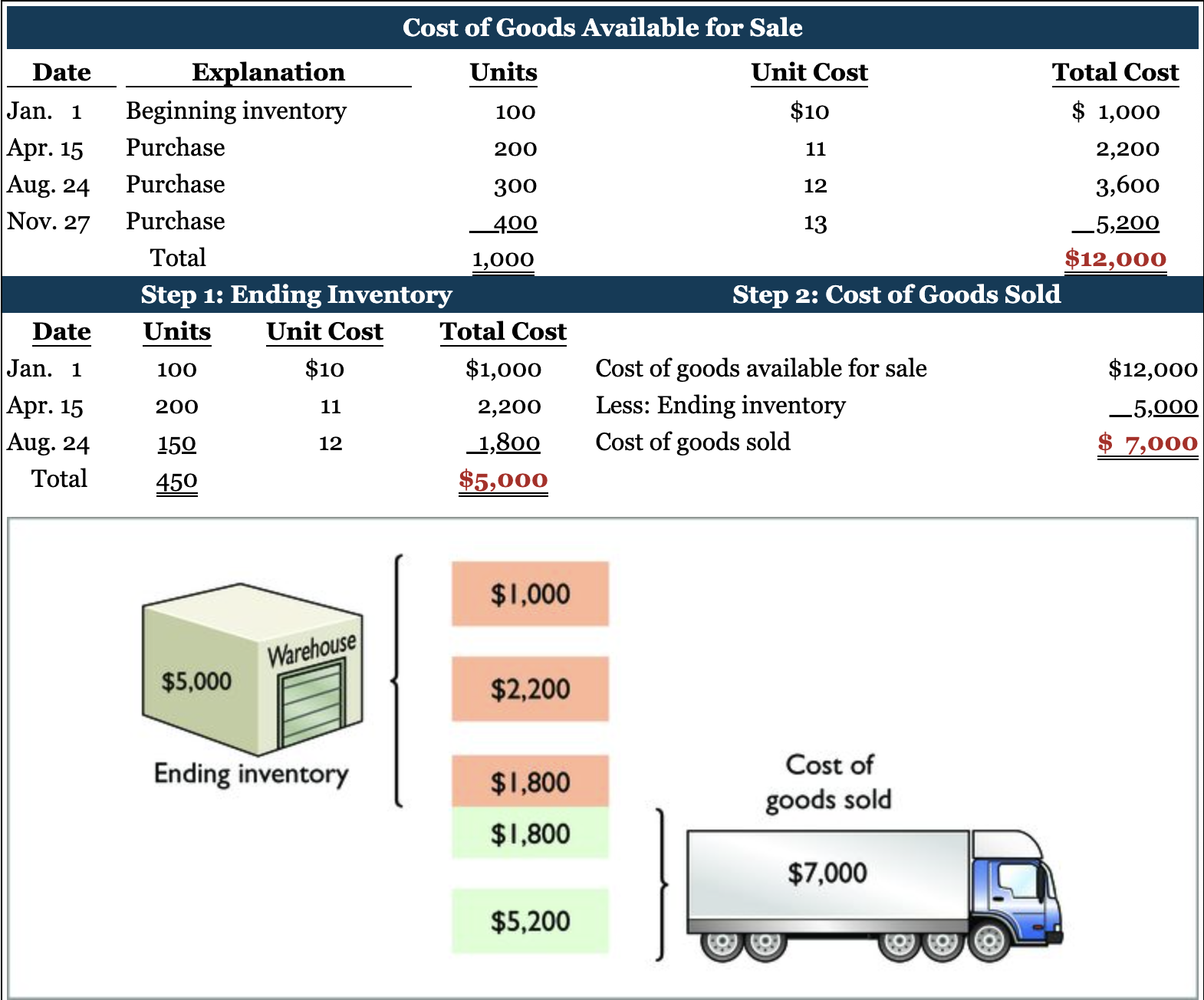

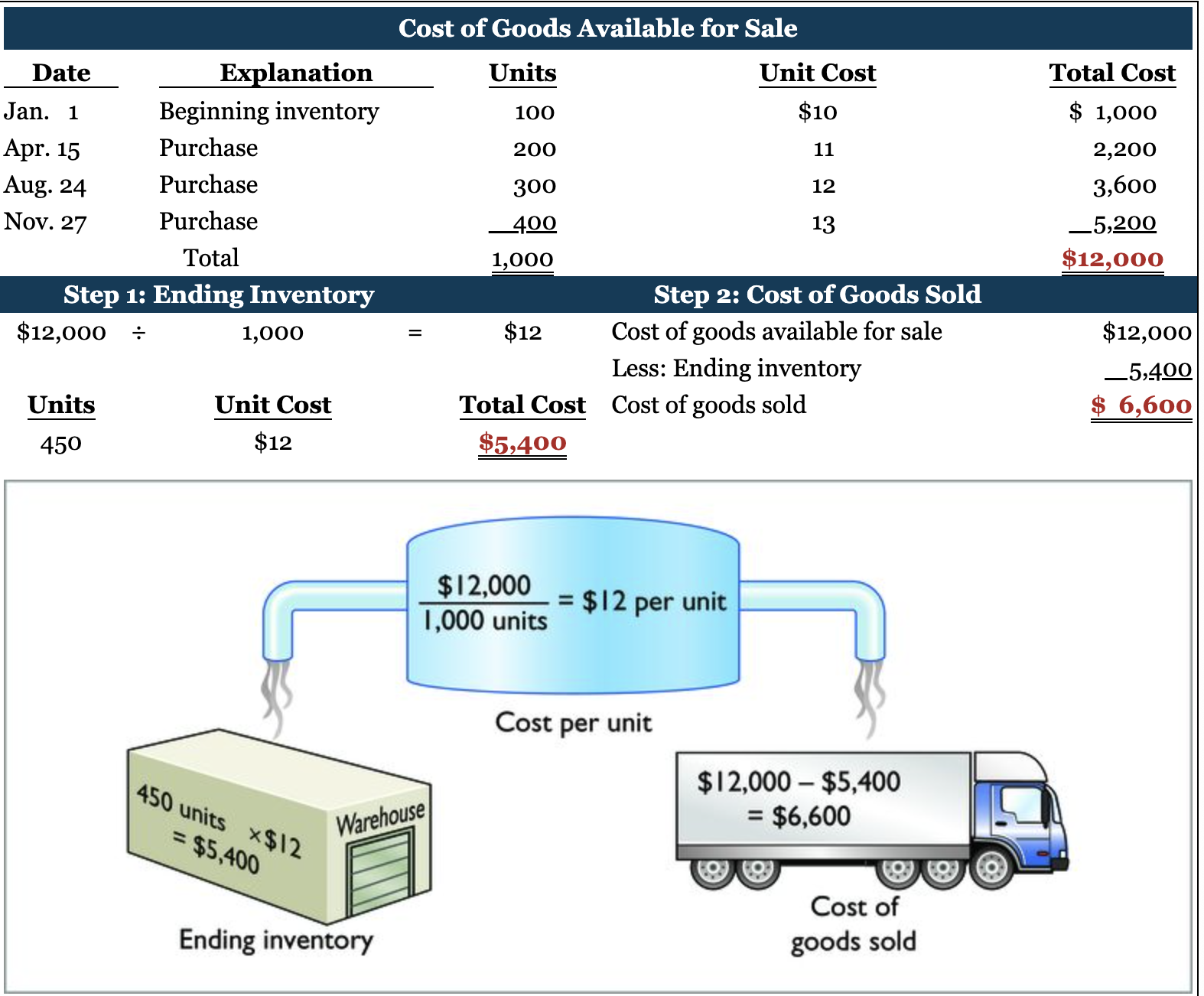

Inventory is accounted for at cost. Cost includes all expenditures necessary to acquire goods and place them in a condition ready for sale. After a comp. has determined the quantity of units of inventory, it applies unit costs to the quantities to compute the total cost of the inventory and the cost of goods sold.

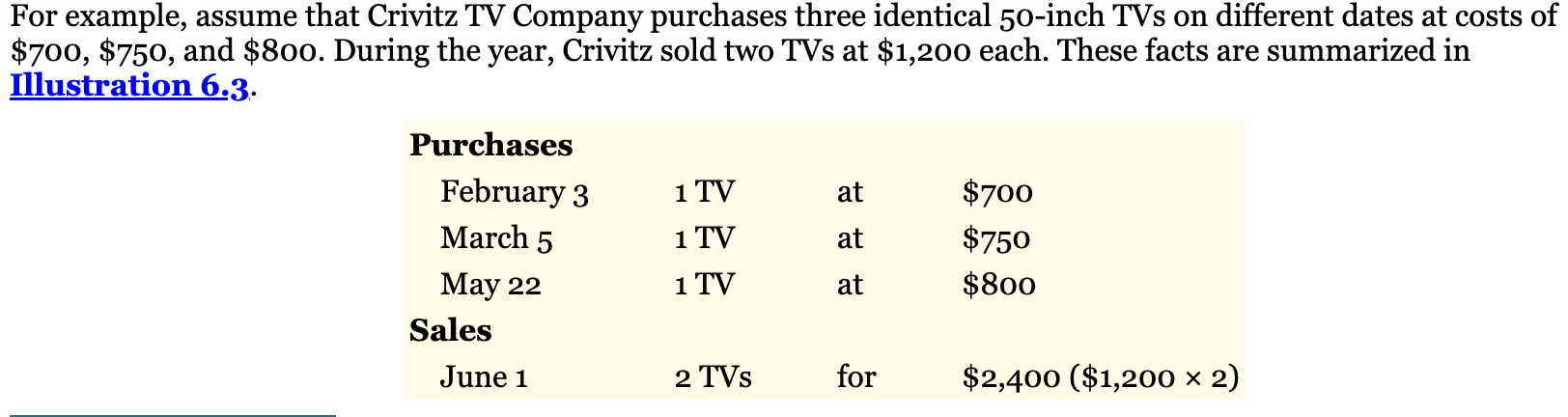

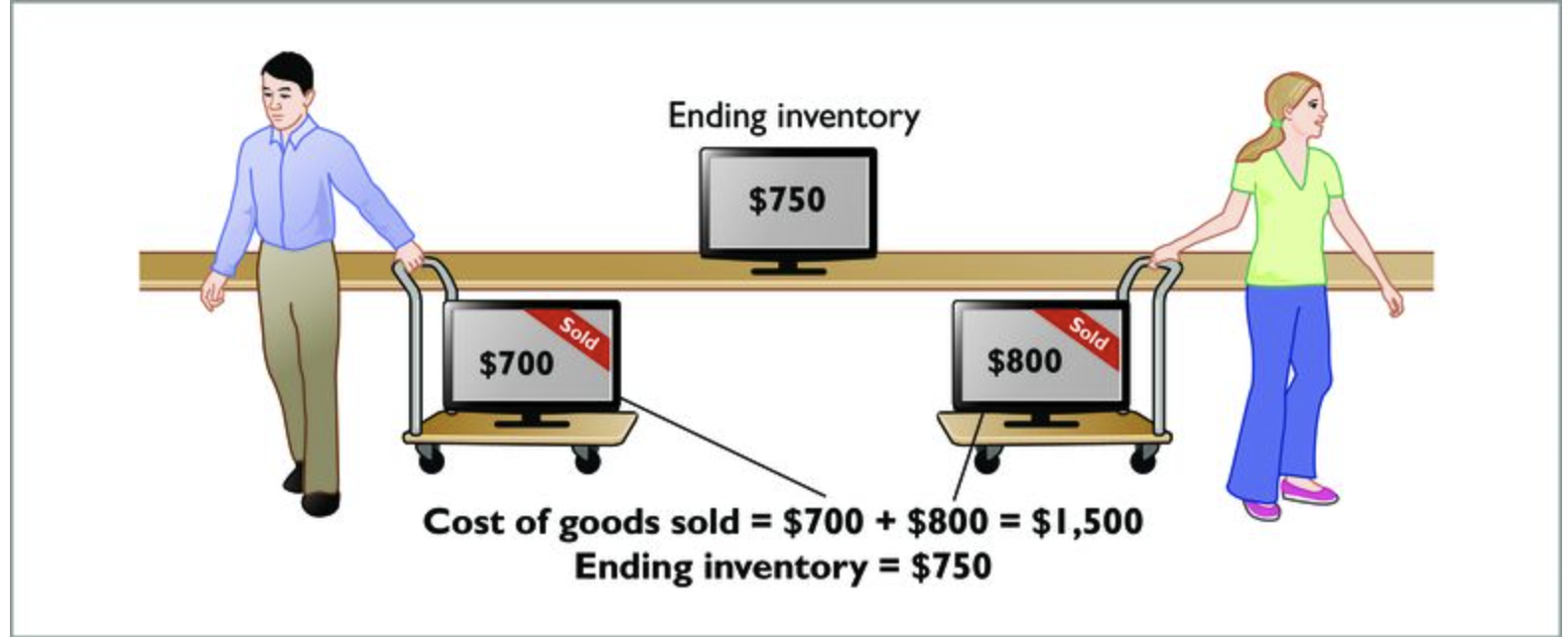

Differ on which of the 3 TV were sold. Ex: $1,450 ($700 + $750), or $1,500 ($700+$800).

If sold the TVs it purchased on Feb 3 and May 22, then its COGS is $1,500 ($700+$800), and its ending inventory is $750.

Specific Identification:

Requires comps. keep records of the og cost of each individuals inventory item.

Cost Flow Assumptions:

Assume flow of costs that may be unrelated to the physical flow of goods.

FIFO

LIFO

Average Cost

Mostly use periodic system to cost their inventory and related COGS.

Use perpetual system to assumed cost (standard cost) to record COGS at the time of sale.

At end of period, they calculate COGS using periodic system again.

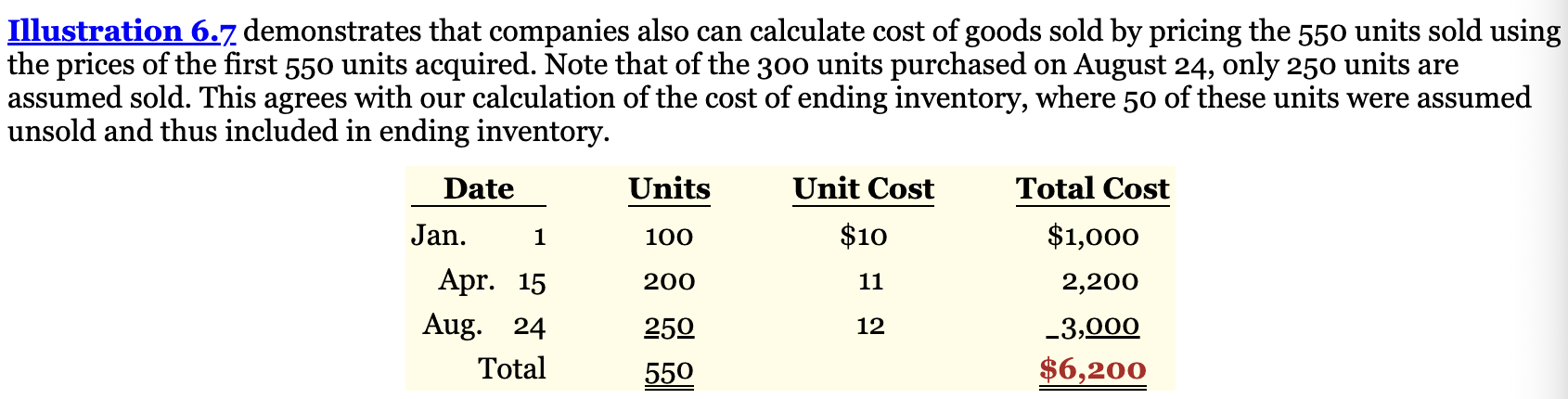

FIFO:

Earliest goods purchased are the first to be sold.

The costs of the earliest good purchased are the first to be recognized in determining cost of goods sold.

Are RECOGNIZED FIRST NOT SOLD FIRST.

First goods purchased were the first goods sold, ending inventory is based on the prices of the most recent units purchased.

COmps. obtain the cost of the ending inventory by taking the unit cost of the most recent purchase and working backward until all units of inventory have been costed.

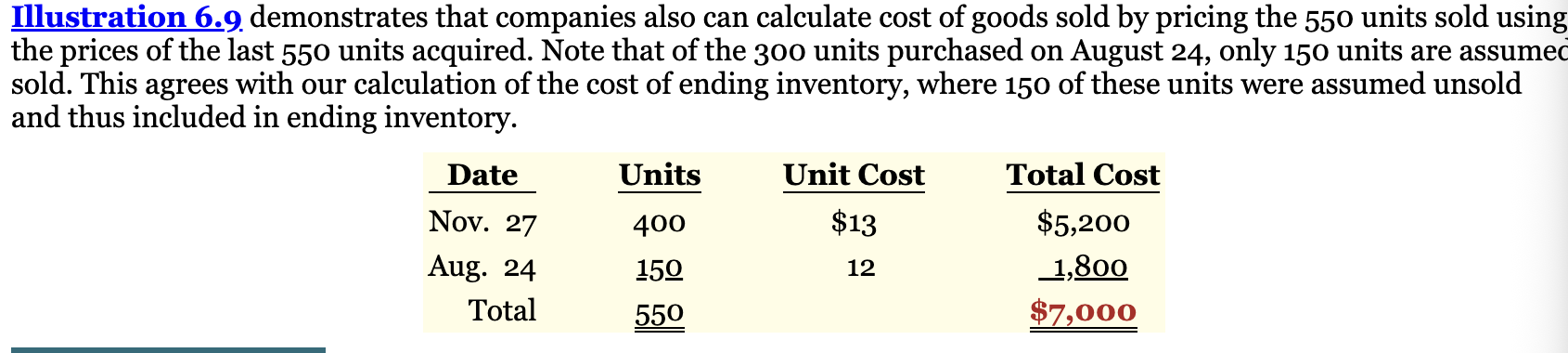

LIFO:

Latest goods purchased are the first to be sold.

Coincides with the actual flow of inventory

Costs of the latest goods purchased are the first to be recognized in determining COGS.

Assumed first goods sold were those that were most recently purchased, ending inventory is based on the prices of the oldest units purchased.

Comps. obtain the cost of the ending inventory by taking the unit cost of their earliest goods available for sale and working forward until all units of inventory have been costed.

All goods purchased during the period are assumed to be available for the first sale, regardless of the date of purchase.

Average Cost:

Allocates COG available for sale on the basis of the weighted-average unit cost.

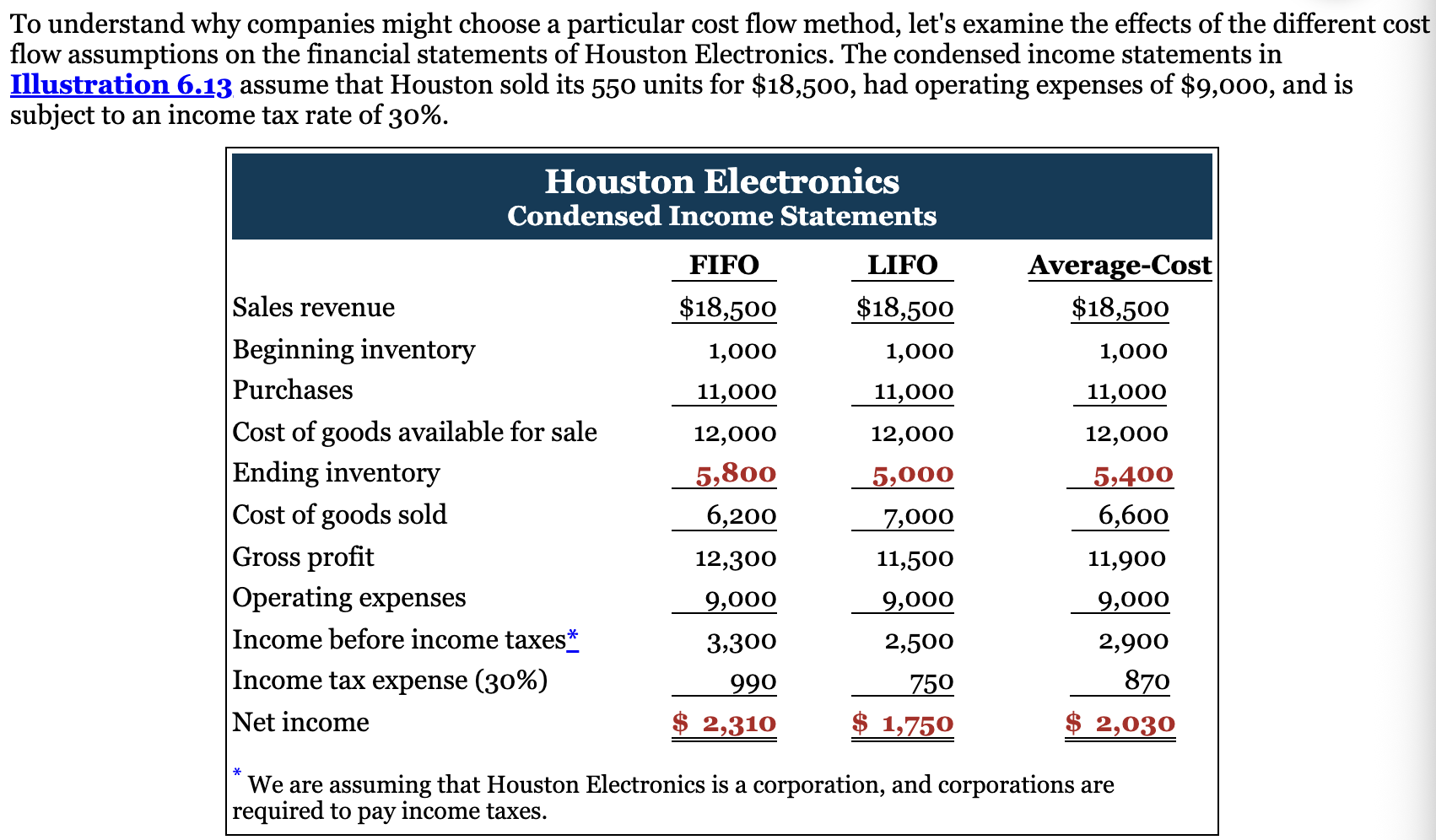

Income Statements Effects:

This difference is due to the unit costs that the company allocated to COGS and to ending inventory.

Each dollar of difference in ending inventory results in a corresponding dollar difference in income before income taxes.

1. In a period of inflation, FIFO produces a higher net income because lower unit costs of the first units purchased are matched against revenue.

2. In a period of inflation, LIFO produces a lower net income because higher unit costs of the last goods purchased are matched against revenue.

3. If prices are falling, the results from the use of FIFO and LIFO are reversed. FIFO will report the lowest net income and LIFO the highest.

4. Regardless of whether prices are rising or falling, average-cost produces net income between FIFO and LIFO.

Balance Sheet:

FIFO method advantage is in a period of inflation, the costs allocated to ending inventory will approximate their current cost.

LIFO method disadvantage is in a period of inflation, the costs allocated to ending inventory may be understated in terms of current cost.

Tax effects:

LIFO results in the lowest incomes taxes because of lower net income during times of rising prices.

Learning Objective 3

Presentation

Lower-of-cost-or-net realizable value

Analysis

Adjustments for LIFO reserve

Vocab:

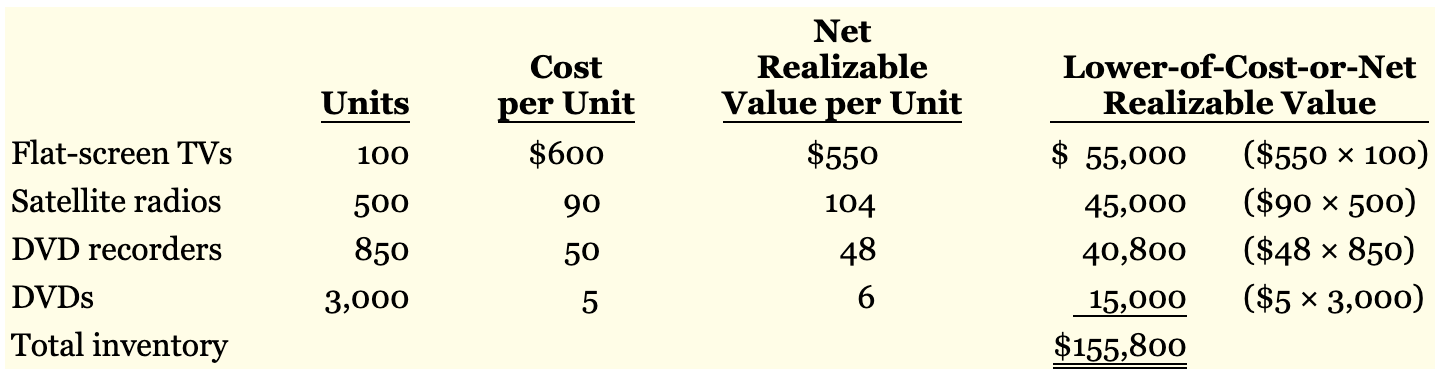

Lower-of-cost-or-net realizable value (LCNRV)- Valuing the inventory at the period in which the price declines occurs.

Net realizable value- Net amount that a comp. expects to realize (receive) from the sale of inventory. Estimated selling price in the normal course of business, less estimated costs to complete and sell.

LIFO reserve- Required to report the difference between inventory reported using LIFO and inventory using FIFO.

Notes:

Presentation:

The major inventory classifications

Basis of accounting (cost, or lower-of-cost-or-net realizable value)

The cost method (FIFO, LIFO, or average-cost)

Lower-of Cost-or-Net Realizable Value

When the value of inventory is lower than its cost, comp. must “write down” the inventory to its net realizable value.

Done by valuing the inventory at the LCNRV in the period in which the price decline occurs.

The best choice among accounting alt. is the method that is least likely to overstate assets and net income.

Net realizable value is the estimated selling price in the normal course of business, less estimated costs to complete and sell.

Comps. apply LCNRV to the items in inventory after they have used one of the inventory costing methods to determine cost.

Comp. that use LIFO method or the retail inventory method are not required to use LCNRV for inventory valuation.

Analysis:

Having too much inventory can lead to hand costs the comp.l money in storage costs, interest cost (funds tied up inventory), and costs associated with the obsolescence of tech. goods (computer chips) or shifts in fashion (clothes)

Having too little inventory on hand results in lost sales

Analyze customer habits, buying patterns, and sales tends. They strive to optimize inventory levels to maximize sales while minimizing inventory holding costs.

Using inventory turnover calculating as cost of goods sold divided by average inventory. It indicates the liquidity of inventory by measuring the number of times the average inventory “turns over” (is sold) during the year. Inventory turnover can be divided into 365 days to compute days in inventory, which indicates the average number of days inventory is held

High inventory turnover (low days) indicates the comp. has minimal funds tied up in inventory-that it has a minimal amount of inventory on hand at any one time.

Too high of inventory turnover may indicate that the comp. is losing sales opp. because of inventory shortages.

LIFO Reserve:

The fin. statement differences from using LIFO normally increase the longer a comp. uses LIFO.

Requires to report the difference between inventory reported using LIFO and inventory using FIFO.

Reporting the lIFO reserve enables analysts to make adjustments to compare companies that use different cost flow methods.

Notes from Meeting with Dawn Hill (04/14/26)

Practice multiple choice in the textbooks, try to reread questions and the way they are worded.

Try to pace and get up with timing

COGS problem is a matter of format, I added to much that was supposed to be in the income statement.

I can drop the test score, she can give me additional points but should be drop it

Chapter 7: Fraud, Internal Control, and Cash

Learning Objective 1:

Fraud

The Sarbanes-Oxley Act

Internal control

Principles of internal control activities

Data analytics and internal control

Vocab:

Fraud- A dishonest act by employee that results in personal benefit to the employee at a cost to the employer.

Fraud triangle- Contribute to fraudulent activity are opportunity, financial pressure, and rationalization

Internal Control- A process designed to provide reasonable assurance regarding the achievement of comp. objectives related to operations, reporting, and compliance.

Internal auditors- comp. employees who continuously evaluate the effectiveness of the comp. internal control systems.

Bonding- Involves obtaining insurance protection against theft by employees. it contributes to the safeguarding of cash.

Notes:

Notes:

Chapter 8: Reporting and Analyzing Receivables

Learning Objective 1:

Types of receivables

Recognizing accounts receivable

Vocab:

Receivables- Amounts due from individuals and companies. Claims that are expected to be collected in cash.

Accounts receivable- amounts customers owe on account They result from the sale of goods and services.

Notes receivable- written promise for amounts to be received. The notes requires the collection of interest and extends for time periods of 60-90 days or longer.

trade receivable- Notes and accounts receivable that result from sales transactions

other receivables- nontrade receivables such as interest receivable, loans to company officers, advances to employees, and income taxes refundable. These do not generally result from the operations of the business.

Notes:

Recognizing Accounts Receivable:

A service org. records a receivable when it performs a service on account.

Ex: When a merchandiser sells goods, it increases (debits) Accounts Receivable and increases (credits) Sales Revenue.

Learning Objective 2:

Valuing accounts receivable

Disposing of accounts receivable

Vocab:

Bad Debt Expense- Companies record credit losses. Losses are normal and necessary risk of doing business on a credit basis.

Direct write-off method- Comp. determines a particular account to be uncollectible, it charges the loss to Bad Debt Expense.

Allowance method- Accounting for bad debts involves estimating uncollectible accounts at the end of each period. Provides better matching of expenses with revenues on the income statement.

Cash (net) realizable value-

Aging the accounts receivable-

Factor-