Chapter 3.2 - Market Efficiency

I. Consumer Surplus, Producer Surplus, and Efficiency

Economists measure efficiency by the ability of markets to provide outcomes that are the most efficient to all other ways of organizing the exchange of goods—also called socially optimal.

Economists talk about gains from trade in the abstract, but any time a consumer makes a purchase from a producer, a trade has been made and both parties expect to gain. These gains are the concepts of consumer and producer surplus.

Total Surplus = Consumer Surplus + Producer Surplus

A. The Gains From Trade

Consumer surplus: The difference between actual market price and

consumers’ willingness to pay, summed over the quantity bought.

Producer surplus: The difference between actual market price and

producers’ willingness to sell, summed over the quantity sold

B. The Efficiency of Markets

Summary: An efficient market performs four important functions:

1. It allocates consumption of the good to the potential buyers who most value it, as indicated by the fact that they have the highest willingness to pay.

2. It allocates sales to the potential sellers who most value the right to sell the good, as indicated by the fact that they have the lowest cost.

3. It ensures that every consumer who makes a purchase values the good more than every seller who makes a sale, so that all transactions are mutually beneficial.

4. It ensures that every potential buyer who doesn’t make a purchase values the good less than every potential seller who doesn’t make a

sale, so that no mutually beneficial transactions are missed.

1. The Reallocation of Consumption Among Consumers

2. The Reallocation of Sales Among Sellers

3. Changes in the Quantity Traded

C. Equity and Efficiency

Are there goods and services that are priced “unfairly” high? What

should you do about it?

Often equity and efficiency are at the root of the debate surrounding

taxes.

Most nations have a system of taxation that serves to redistribute some

income from the wealthy to the poor. This may not be efficient, but these

nations have decided that it is fair.

Economists classify three types of taxes according to how they vary with

the income of individuals.

A tax that rises more than in proportion to income, so that high-

income taxpayers pay a larger percentage of their income than low-

income taxpayers, is a progressive tax. Ex. Income, Real estate tax.

A tax that rises less than in proportion to income, so that high-income taxpayers pay a smaller percentage of their income than low-income taxpayers, is a regressive tax. Ex. sales taxes and property taxes.

A taxes that rises in proportion to income, so that all taxpayers pay

the same percentage of their income, is a proportional tax. Ex. Sales grocery and social security tax.

Regressive vs. Proportional vs. Progressive Taxes Examples

Shoppers pay a 6% sales tax on their groceries whether they earn

$30,000 or $130,000 annually, so those with lesser incomes end up

paying a greater portion of total income than those who earn more. If someone makes $20,000 a year and pays $1,000 in sales taxes consumer goods, 5% of his annual income goes to sales tax. But if he earns $100,000 a year and pays the same $1,000 in sales taxes, this represents only 1% of his income.

One tax that is used in many countries is the excise tax. This is a tax levied on each unit of a good that is sold. In the U.S. excise taxes are

imposed upon the sale of goods such as gasoline, tobacco, alcohol and,

in many cities, hotel rooms.

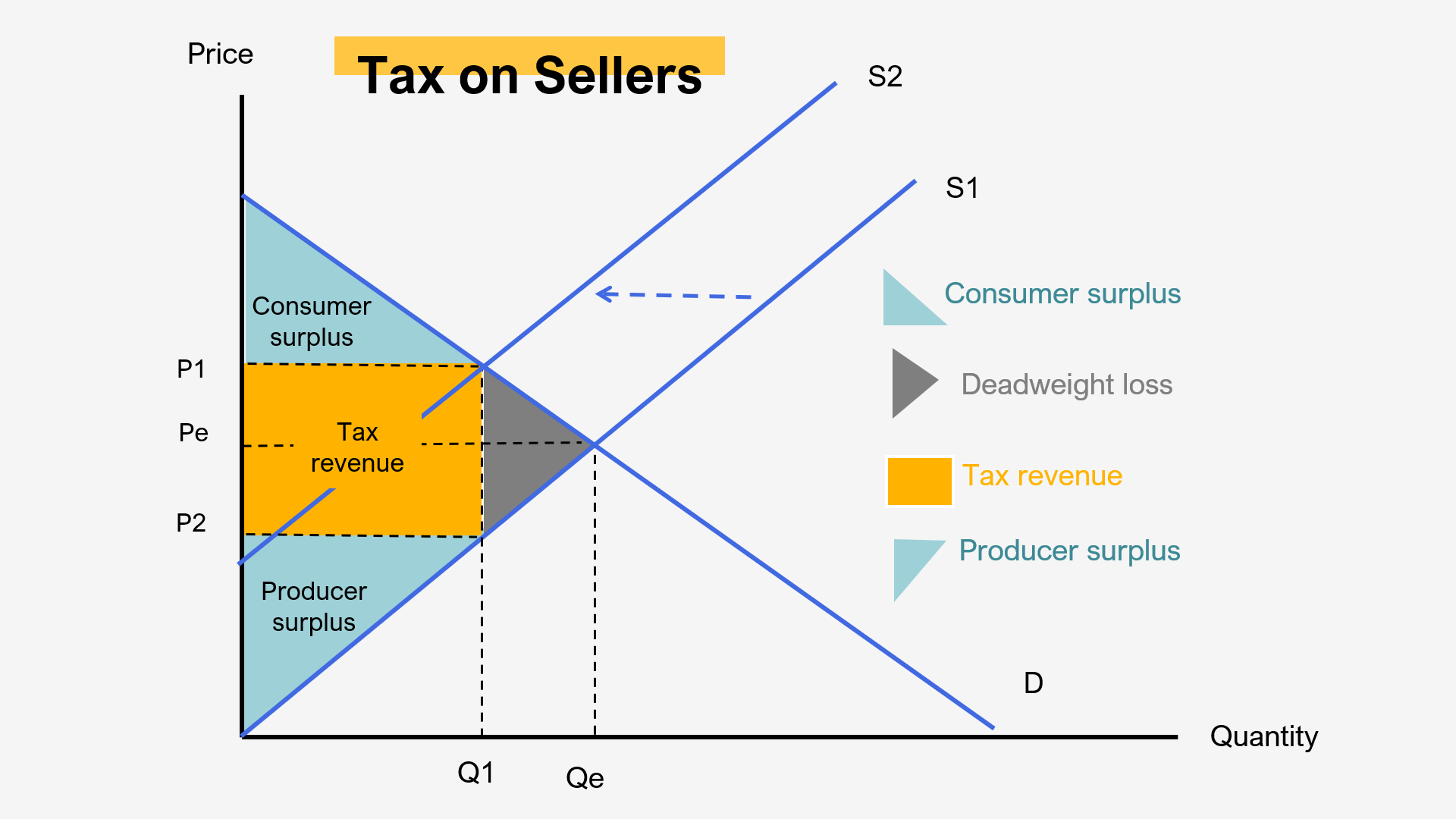

II. The Effects of Taxes and Total Surplus

A. The Effect of an Excise Tax on Quantities and Prices

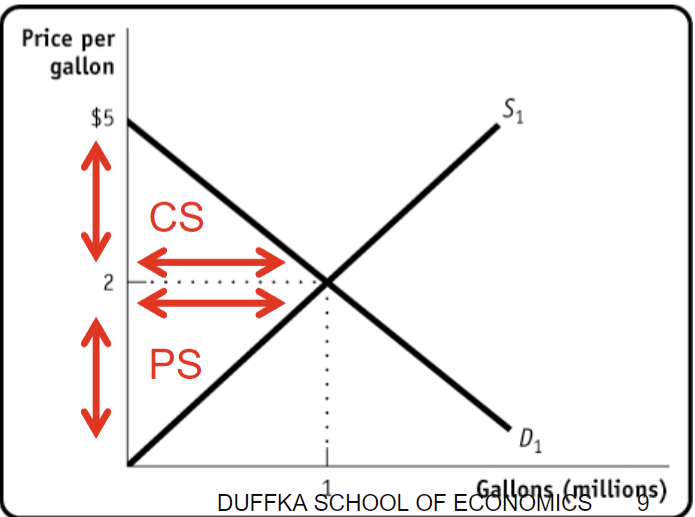

Suppose the market for gasoline in Smog City is free of any taxes.

The equilibrium price is $2 per gallon, and 1 million gallons are sold

every day.

Compute the total surplus as the combined area of two triangles seen in

the graph

Consumer surplus = ½*($3)(1million) = $1.5 million

Producer surplus = ½*($2)(1 million) = $1 million

Total surplus = $2.5 million\

A. The Effect of an Excise Tax on Quantities and Prices

B. Price Elasticities and Tax Incidence

1. When an Excise Tax is Paid Mainly by Consumers

2. When an Excise Tax is Paid Mainly by Producers

III. The Benefits and Costs of Taxation

A. The Revenue from an Excise Tax

B. The Costs of Taxation