CSC Exam 2

1/408

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

409 Terms

Fundamental analysis

method of evaluating capital market conditions in an attempt to measure the intrinsic or fundamental value of society

To compare intrinsic value against security’s price to determine if security is over or undervalued

Market theories

Efficient market hypothesis

Random walk theory

Rational expectations theory

Efficient market hypothesis

stock’s price reflects all available information and its true value

Assumes that profit-seeking investors react quickly to the release of information

Three variations:

Weak form: all past market information is fully reflected in price, tech analysis has little or no value

Semi-strong form: all publicly available information is fully reflected in price, both fundamental and tech analysis have little or no value

Strong form: all information is fully reflected in price, all investors have equal information

Random walk theory

past price changes contain no useful information as developments have already been reflected in the current stock price

Assumes that new information regarding a stock is disseminated randomly over time

Rational expectations theory

past mistakes can be avoided by using available information to anticipate change

Assumes that people are rational and have access to all available information

Capital market inefficiencies

New information is not available to everyone at the same time

Investors do not react in the same way

Not everyone can make accurate forecasts

Investors may act irrationally

Macroeconomic factors affecting investor expectations

Fiscal policy

Monetary policy

Inflation

Fiscal policy impact

Taxation: higher taxes = less disposable income and spending, reduction of dividends or expansion

Government spending: increase in spending = stimulates economy in short run

Government debt: higher levels of debt can restrict both fiscal and monetary policy options

Monetary policy impact

Bank attempts to preserve value of dollar by keeping inflation low, stable, and predictable

Changes in monetary policy affect both interest rates and corporate profits

Tilting of the yield curve

when short term yields rise and long term yields fall from monetary policy

Decline in long term rates reduces competition between equities and bonds

Inflation impact

creates a widespread uncertainty and undermines confidence in the future

Causes: higher interest rates, lower corporate profits, lower earnings, higher inventory and labour costs, lower share prices

Industry classification

Product or service

Life cycle

Competitive forces

Reaction to the economic cycle

Classifying industries: product or service

Global Industry Classification Standard (GICS): comprehensive industry and sector classification system by S&P and Morgan Stanley

163 sub-industries

Classifying industries: life cycle

Emerging growth

Growth

Maturity

Decline

Emerging growth

brand new industries in the early stages of growth, software development

Unprofitable at first, not directly accessible to equity investors

Growth

sales and earnings are consistently expanding at a faster rate

Common shares are called growth stocks, high price-to-earnings ratios and low dividend yields

Above average rate of earnings, lower costs of production, high competition, rising demand and profits

Maturity

slower, more stable growth in sales and earnings that closely match overall rate of economic growth

High price competition, falling profit margins, steady during difficult economic conditions

Decline

declining demand due to tech changes, inability to compete on price, changes in consumer taste

Large cash flow, low profits

Classifying industries: competitive forces

Threat of new entry: ease of entry for new competitors

Depends on amount of capital required, opportunities to achieve economies of scale (cost dec as production inc), regulations etc

Competitive rivalry: degree of competition

Depends on number of competitors, strength, industry growth, uniqueness of product

Threat of substitutes

Bargaining power of buyers: pressure to lower prices, depends on buyers' sensitivity to price

Bargaining power of suppliers: pressure to pay for more resources

Classifying industries: reaction to the economic cycle

Cyclical

Defensive

Speculative

Cyclical industries

particularly sensitive to swings in economic conditions

Most are large international exporters of commodities such as lumber, metals, or oil -> sensitive to changes

Defensive industries

stable earnings, continuous dividend payments, stable during recessions

Blue chip: shares of top investment quality companies, dominant market position, strong financing and management

Canadian banks: though bank stock prices are relatively sensitive to changes in interest rates

Utility companies: generate consistent earnings over cycles

Speculative industries

risk and uncertainty are unusually high due to a lack of definitive information

Emerging companies

Technical analysis

method of determining future price direction of security based on past price movements

Look at trend in stock’s price instead of fundamental attributes

Assumptions of technical analysis

All influences on market action are automatically accounted for or discounted in price activity

Prices move in trends which persist for long periods of time

The future repeats the past

Technical vs fundamental analysis

Tech: effects of supply and demand which are reflected in price and volume

Fundamental: causes of price movements

Chart analysis

analysis of graphic representations of relevant market data

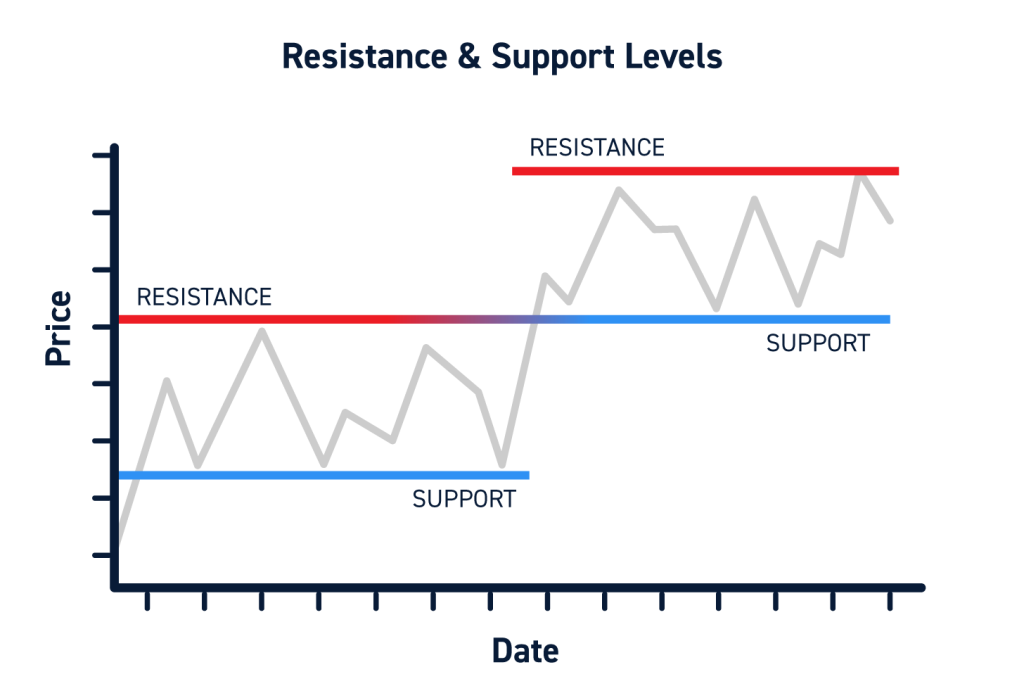

Identify support and resistance levels

Reflect market participation patterns

Support level

bottom price of trading range where investors are willing to buy, demand exceeds supply and prices rise

Resistance level

top price of range where investors are willing to sell, supply exceeds demand and prices fall

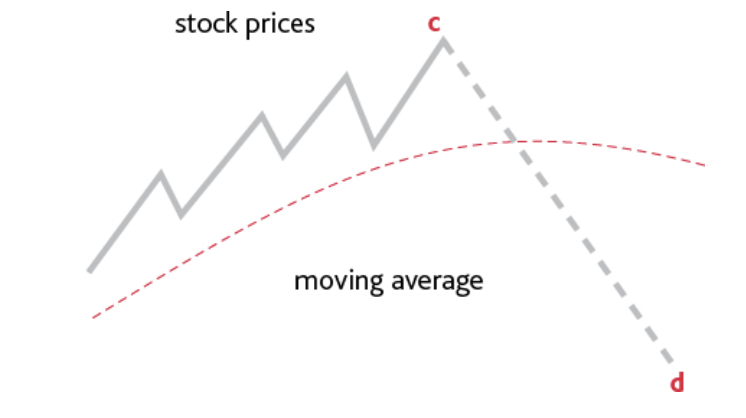

Reversal pattern

formation that precedes a decline in stock prices

Head and shoulders formation: can occur at a market top or market bottom

Top = bearish, bottom = bullish

Continuation pattern: current trend will continue

Symmetrical triangle: pause in market

Quantitative analysis

relies on statistics and computer technology

Moving average: device for smoothing out fluctuating values in an individual stock or aggregate market, shows long term trends

Calculated by adding closing prices over a period and dividing total by number of days in the period

Buy and sell signals

Buy signal

price breaks through moving average from below and line starts to rise = declining trend has reversed

Sell signal

price breaks through moving average from above and line starts to fall = upward trend has reversed

Sentiment indicators

measure investor expectations or the mood of the market

Contrarian investors use to move oppositely to other investors

Should only be used as evidence to support other technical indicators

Cycle analysis

helps forecast when the market will start moving in a particular direction and when it will reach peak or trough

Based on assumption that cyclical forces drive price movements

Lengths:

Trading: 4 weeks

Primary: 9-26 weeks

Seasonal: 1 year

Long term: >2 years

Company analysis

process of examining company specific factors that can influence investment decisions

Statement of comprehensive income analysis

see if management is making good use of the company's resources

Revenue: increasing revenue as important indicator of investment quality

Operating costs: use gross profit margin ratio to determine changes in ability to pay operating costs

Dividend record: shows how much it generally pays out in the form of dividends to shareholders

High dividend payout rate: stable earnings, declining earnings (indicate future cut), depleting resources

Low payout rate: growing earnings, earnings reinvested back into company's operations

Statement of financial position analysis

Capital structure: distribution of debt and equity that comprise the company’s finances

Effect of leverage: earnings are leveraged if the capital structure contains debt or preferred shares, accelerates any cyclical rise or fall in earnings

Small increase in revenue can produce a magnified increase in earnings per common share (EPS)

Financial ratios

financial calculations based on statements, provides clues about company’s financial health

Trend ratios

identify trends by selecting a base period, treating it as 100, then dividing it into comparable ratios for subsequent periods

May be misleading when base period is not truly representative, impossible to apply if base period is negative

Liquidity ratios

used to judge company's ability to meet short-term commitments

Working capital ratio

Quick ratio/acid test

Working capital ratio

shows the relationship between current assets and current liabilities

Current assets/current liabilities

Quick ratio

subtracts inventories from current assets, more stringent and conservative

(Current assets - inventories)/current liabilities

Risk analysis ratios

how well the company can deal with its debt obligations

Asset coverage ratio

Debt to equity ratio

Cash flow to total debt outstanding ratio

Interest coverage ratio

Asset coverage ratio

a company's ability to cover its debt obligations with its assets after all non-debt liabilities have been satisfied

Tangible assets - (current liabilities - short term debt)/total debt outstanding

Debt to equity ratio

shows relationship between company's borrowings and capital invested by shareholders

Total debt outstanding/equity

Cash flow to total debt outstanding ratio

gauges a company's ability to repay borrowed funds

Cash flow from operating activities/total debt outstanding

Cash flow: measure of a company's ability to generate funds internally

Cash flow = profits + non-cash deductions - all additions not received in cash + change in net working capital

Interest coverage ratio

ability of a company to pay interest charges on its debt based on profit available to pay interest, indicates margin of safety for interest coverage

Considered the most important quantitative test of risk for a debt security

Indicates only the likelihood that a company will be able to meet interest obligations

Profit before interest charges and taxes/interest charges

Operating performance ratios

how well management is making use of company’s resources, include profitability and efficiency measures

Gross profit margin ratio

Net profit margin ratio

Return on common equity ratio

Inventory turnover ratio

Gross profit margin ratio

indication of the efficiency of management in turning over the company's goods at a profit

(Revenue - cost of sales)/revenue

For calculating internal trend lines and for making comparisons with other companies

Net profit margin ratio

how efficient the company is managed after taking expenses and taxes into account

(Profit - share of profit of associates)/revenue

Return on common equity ratio

dollar amount of earnings that were produced for each dollar invested by company's shareholders

Profit/total equity

Inventory turnover ratio

measures the number of times that a company's inventory is turned over in a year

Cost of sales/inventory

High turnover ratio is good as the company requires a smaller investment in inventory

Low ratio: inventory contains a large portion of unsaleable goods, company has overbought inventory, value is overstated

Value ratios

shows investor what company’s shares are worth or return

Dividend payout ratio

Earnings per common share (EPS) ratio

Dividend yield

Equity value/book value per common share

Price to earnings ratio

Dividend discount model (DDM)

Dividend payout ratio

percentage of company's profit that is paid out to shareholders in the form of dividends

Common share dividends/profit x100

Generally unstable as they are tied directly to earnings of company which change year to year

Earnings per common share (EPS) ratio

earnings available to each common share

Profit/weighted average number of common shares outstanding

When estimating dividend possibilities consider:

Amount and stability of profit, company's working capital, policies etc

Dividend yield

annual dividend rate expressed as a percentage of the current market price of the stock

Indicated annual dividend per share/current market price x100

Equity value/book value per common share

net asset coverage for each common share if all assets were sold and all liabilities were paid

Equity/number of common shares outstanding

Price to earnings ratio

links market price of common share to EPS, help determine a reasonable value for a common stock

Current market price of common shares/earnings per share

Most widely used because it combines all other ratios into one figure, allows comparison of different company shares

P/E ratios increase in a rising stock market or with rising earnings, when investor confidence is high

Want to be low (undervalued)

Inversely related to inflation

Dividend discount model (DDM)

how companies with stable growth are priced, related stock's current price to present value of all expected future dividends

Assumes an indefinite stream of dividend payments

current dividend(1+g)/r-g = expected dividend/r-g

Investment quality assessment

Preferred dividend coverage ratio: margin of safety for preferred dividends, amount of money a firm has to pay dividends to preferred shareholders

Higher ratio = company has little difficulty in paying preferred dividends, calculated the last 5 years

Equity/book value per preferred share: minimum value is at least two times the dollar value of assets that each preferred share would be entitled to at liquidation

Dividend payments: continuous?

Credit assessment: rating?

Portfolio approach

creating a diversified portfolio that allows investors to reduce risk without decreasing expected returns

Diversification

strategy that combines a variety of investments in a portfolio with aims to reduce investor’s risk of any single security

More diversified = closer to mirroring the market

Capital gain

selling a security for more than its purchase price

Cash flow

any income derived from a security in the form of interest payments or dividends

Expected return

expected cash flow + expected capital gain divided by beginning value

Rate of return/yield

returns expressed as a percentage

Return % = (cash flow + (ending value - beginning value)/beginning value x100

Portfolio rate of return = (equity portion x return) + (fixed income portion x return)

Percentage of return is also called annual rate of return

Holding period return

transactional rate of return that takes into account all cash flows and changes in value over time, can be greater or less than a year

Ex ante

expected returns, use to determine where funds should be invested

Can expect t-bill rate plus a certain performance percentage related to risk

Ex post

actual historical returns

Risk

likelihood that the actual return will be different from actual return

Risk/return scale: t-bills, bonds, debentures, preferred shares, common shares

T-bills have zero risk

Types of risk

Inflation

Business

Political

Liquidity

Interest rate

Foreign investment

Default

Systematic

Non-systematic/specific

Inflation rate risk

risk that inflation will reduce future purchasing power and real return

Business risk

risk that a company's earnings will be reduced as a result of business operations (labour strike, new products, competition)

Political risk

risk of unfavourable changes in government policies, general instability associated with investing in a particular country

Liquidity risk

risk that an investor will not be able to trade a security quick enough because opportunities are limited

Interest rate risk

risk that changing interest rates will adversely affect an investment, rising rates = falling value

Foreign investment risk

risk of loss resulting from an unfavourable change in exchange rates/drop off of liquidity/large bid-ask spreads

Default risk

risk that a company will be unable to make timely interest payments or repay principal amount upon maturity

Systematic risk

risk associated with investing in each capital market, cannot be diversified away

Non-systematic/specific risk

risk that the price of a specific security or group of securities will change in price to a certain degree or different direction from market

Can be reduced through diversification -> eliminated by buying a portfolio of shares that consist of all stocks in index

Standard deviation

percentage gives investor an indication of the risk associated with a security or portfolio

Commonly applied to portfolios and individual securities

Past performance is used to determine a range of possible future outcomes (more volatile price = larger range)

Greater deviation = greater risk

Beta

links the risk of securities to the market as a whole

Measures the degree to which securities tend to move up or down with the market

Greater beta = greater risk

Calculating rate of return in a portfolio

calculate return generated by each security and calculate the weighted average return on all securities

*equation

Combining securities in a portfolio

Correlation

Portfolio beta

Portfolio alpha

Correlation

statistical measure of how the returns on two securities move together over time, how a change to the value of one can predict the change in value of another

Perfect negative correlation: when one falls and other rises, allows for a positive return with little risk (only systematic), maximum gain from diversification

Portfolio beta

measures fluctuation in returns driven by changes in the stock market

Equity that moves up or down to the same degree as the stock market has a beta of 1, moves up more >1, moves down more <1

Most portfolio betas indicate a positive correlation between equities and the stock market

Industries with volatile earnings (cyclical) tend to have higher betas and defensive industries tend to have lower betas

Portfolio alpha

excess return due to skill of the advisor of manager in picking securities that outperform

Active investment strategy

goal is to outperform a benchmark portfolio on a risk-adjusted basis, compare performance of a portfolio to an appropriate benchmark

Bottom up analysis: focus on individual stocks

Top down analysis: study of broad macroeconomic factors, then industry-specific factors, then company specific factors to assess value of stock

Passive investment strategy

tend to replicate the performance of a specific market index

Indexing: buying and holding a portfolio that matches the composition

Buy and hold: securities markets are efficient, manager believes it is not possible to identify stocks as under or overpriced

Equity manager styles

Growth

Value

Sector rotation

Growth manager style

focus on current and future earnings (specifically EPS) of individual companies, will pay more if growth potential warrants higher price

Lower dividend yield, securities are turned over more often

Risks:

If EPS falters, can cause large percentage price declines

High portfolio volatility

Highly vulnerable

Characteristics:

High price to earnings

High price to book value

High price to cash flow

Based on expectations -> focus on long term investments, avoid paying too much, greater potential for capital appreciation

Value manager style

focus on stocks that are perceived to be trading for less than their value, bottom-up stock pickers with a research-intensive approach

More successful in inefficient markets, price may be low for a good reason in efficient markets

Risks:

Lower annualized standard deviation

Lower historical beta

Low stock price

Characteristics:

Low price to earnings

Low price to book value ratio

Low price to cash flow ratio

High dividend yield

Produces total returns similar to growth but with a higher current dividend yield and less portfolio volatility, performs best in down markets

Requires patience: long term investment horizons, ignore short term fluctuations

Sector rotation manager style

focus on analysing prospects for the overall economy, invest in sectors expected to outperform

Identify the current phase of the economic cycle, direction, and various sectors affected

Buy large cap stocks to maximize liquidity

Risks:

High volatility caused by industry concentration

Investors may significantly underperform the market benchmark, high turnover

Individual company stocks get overlooked -> picked stocks may not be representative of entire sector

Concerned with trying to outperform the market averages (S&P index)

Most basic industry rotation strategy involves shifting between cyclical and defensive industries

When stock prices fall: cyclical stocks fall faster, defensive fall slow and help the investor to preserve capital

Fixed income manager styles

Term to maturity:

Short term: t-bills and <5 year bonds, less volatile to interest rates

Medium term: 5-10 years, mortgage funds

Long term: >10 years

Credit quality: lower quality = higher yield

High yield bonds: non-investment grade/junk bonds, face greater credit risk, mature in less than 3 years

Lower rated bonds have less liquidity than government issues

Interest rate anticipators:

Anticipate a decrease in rates = extend average term on bond investments

Form of duration switching: anticipate falling interest rates = sell lower duration bonds and replace with higher duration for higher capital gains

Works best when yield curve is normal (wide gap between short and long term rates)

Portfolio management

analyzing client’s personal and financial information to determine an asset mix that best suits them (cash, fixed income securities, equities)

Selection of securities based on their interaction with each other and contribution to the portfolio

Portfolio management process

Objectives and constraints

Investment policy statement

Asset mix

Select the securities

Monitor client, market, and economy

Evaluate portfolio performance

Rebalance

Investment objectives

Safety of principal: assurance that client's initial capital will remain intact

Short term bonds and t-bills have a very high degree of security

Income: regular series of cash flows received from debt and equity securities

Maximize rate of income return = give up safety when purchasing corporate bonds or preferred shares

Growth of capital: profit generated when securities are sold for more than cost to buy

(Secondary):

Liquidity: nearly always buyers, important for investors who need money on short notice (sell within one business day)

Tax minimization: tax treatment of returns influences the choice of investments

Securities and their investment objectives

Short term bonds: best safety, very steady income, very limited growth

Long term bonds: next best safety, very steady income, variable growth

Preferred shares: good safety, steady income, variable growth

Common shares: least safety, variable income, most growth

Types of equities

Conservative: low risk, high capitalization, predictable earnings, high yield, high dividends, lower price to earnings ratio, low volatility

Growth: medium risk, average capitalization, potential for above average growth in earnings, aggressive management, lower dividends, higher price to earnings ratio, higher volatility

Venture: high risk, low capitalization, limited earnings, no dividends, low significance of price to earnings ratio, short operating history, high volatility

Speculative: max risk, short term, max volatility, no earnings, no dividends, no significance of price to earnings ratio