Audit things I keep forgetting

1/69

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

70 Terms

When do you stratify a sample

large homogenous groups

population has vairable amounts

results in smaller sample sizes

Mean per unit estimation equation

confirmation value/sample units X # of units

Ratio Estimation

audit sample $/BV sample $ X total BV $

Difference Estimation

(BV$-Sample Confirm $)/sample size X population units

What should you ask the predecessor auditor about?

What does the precessor auditor allow you to look at:

o Should ask about:

§ Management integrity

§ Disagreements

§ Reasons for change in auditor

§ Any fraud, noncompliance, and internal control matters related communications

§ Nature of entity’s relationships and transactions with related parties and any unusual transactions

What does the precessor auditor allow you to look at:

the predecessor auditor will allow a review of audit documentation related to planning, risk assessment, audit procedures, audit results, and matters of continuing audit significance.

what should the succesor auditor do if the predessor audiotr’s report isn’t included

When the successor auditor does not present the predecessor auditors’ report, the success should only express an opinion on the CY FS and indicate in an other matter(nonissuer) or explanatory paragraph(issuer), including:

- predecessor should be reference but not named unless involved in merger with successor

- Type of opinion expressed and if it was modified and reasoning

- Nature of any emphasis of matter, other matter, or explanatory paragraph included in the predecessor’s audit report

- Date of predecessor’s audit report

managemnet letter cs management representation letter

management letter: auditor writes to discusses weakness in IC

management representation letter: from managment to auditor saying everything is there

What is the difference of the following days:

Audit Report Date

Report Release Date

Documentation completion date

Audit report date: there is sufficent apporporiate evidence

Report release date: client can use the report(it is often delivered)

document completion date: The date after which existing audit documentation must not be deleted and any additions shold be documented

Issuers: 14 days

nonissuers: 60days

What are different types of audit evidence

corboratting(BoD meetings, inquiry)

accounting records(invoices)

electronic

Can we do an AR confirmation on a receivable? When would we do that?

Yes

if in py there were a lot of discrpencies that were not misstatemnts in PY it may be more effective to just confirm individual invoices

When can internal auditors be used?

in procedues:

assessing RMM

understanding the ntitiy

susbtatintive

IC

OFC cannot be used on areas with high risk or lack of compentance or indepndence

can analytical procedures be used to say controls are operating effectively

no

Do you mention a specalist in an audit report?

when there is an modified opinion given you have to add an explanatory paragrpah

If management doesn’t provide a representaion what does the auditor do

withdraw or disclaim

top down audit approach

FS levle risks

entity level controls

AB and transaction assertations

What audit procueders test deisgn effectivness? what about operating

Design:

inquiry

observatin

inspection

operating

inquiry

observation

inspection

referformance

recalculation

never confirms

Who uses emphasis of matter paragraphs? When are they required?

Nonissuers

remember this should be disclosed somewhere in the FS

Required

a material justified change in accounting principle

subsequently discovered facts that lead to a change in audit opion(colud be emphasis or other)

prepared using special purpose framework(other than GAAP and regulatory basis fs intended for general purpose use)

Not required but can be used:

uncertainty w unusual litigation or regulatory outcome

castrophe that signifncatly effects finacnial position

significant related party transactions

unusally important signficnat evens

going concern alleviation

Who uses other matter paragraphs? When are they required?

non issuers

Special Racoons Steal Pizza Constantly

When is it required?

To restrict the use of the auditor’s report when special purpose fs are prepared in accordance with contractual or regulatory basis of accounting

Anytime there is a restriction on the use of the auditor’s report

Subsequently discovered facts lead to a change in audit opinion(could be emphasis of matter or other matter paragraph

FS of prior period were audited by a predecessor auditor and the predecessor’s audit report is not reissued

Current period FS are audit and presented in comparative form that were not audited, reviewed or compiled

May be required?

To describe why the auditor can’t withdraw from an engagement although there are major issues(scope limitations, misstatements, etc)

-Law or generally accepted practices require the auditor to provide further explanations

Auditor has been engaged to report on more than 1 set of fs that have been prepared with different frameworks

How should an auditor address other informaiton in a report

a seperate section titled other information

what does an agreed upon procedures report include?

a statement that the subject matter is the responsibility of the responsible party

a statement that the sufficiency of the procedures is solely the responsibility of the specified parties

a descirption of the procedures peformed(or refrence thereto) and the related findings

A statement that the practitioner was not engaged to, and did not conduct, an examination or review, the objective of which would be an opinion or conclusion, respectively, on teh subject matter

a statement that the practitioner does not express an opinion or conclusion

What are auditor’s examining in prospective FS?

Management’s assumptions

the presentation of the FS(per AICPA guidelines)

who determines the sufficiency of procedures relating to an agreed upon procedures audit?

we make a judgement during acceptance

but ultimately the responsibly of the client

What statements should be made in an accountant’s compilation and examination of projected FS

There are limitations on the project’s usefulness, including:

1) that there will usually be differences between projected and actual results, and

(2) that the accountant has no responsibility to update the report for events occurring after the date of the report.

What type of assurance do you give in an complaince engagemnt

Negative assurance = compliance report issued with financial statement audit (limited assurance, no opinion).

Positive assurance (opinion) = separate compliance examination engagement (reasonable assurance).

objective of a compliance governemtnal audit

An objective of a compliance audit of a governmental entity is to form an opinion on whether that government complied with applicable compliance requirements in all material respects, and then to report at the level specified by the governmental audit requirement.

What is a cognizant agency in govenmnetal accounting

overseees the audit of the agency(siminlar to a audit committee)

typically the federal awarding agency that provides the most amount of direct funding to a nonfederal entity.

Conditions for agreed upon procedures in an prospecttive audit

all otherwise stated agreed-upon procedures

summary of significant assumptions

state results may not be acheived and there is no obligation to update thsi

whether the statemetns follow assumptions and AICPA

what is included in an audit report of an issuer with materail weaknesses

B. | A statement that management failed to report two material weaknesses identified by the auditor with a description of the omitted weaknesses. | |

C. | A statement that material weaknesses have been identified. | |

D. | The definition of a material weakness. |

what does it mean to take a top down risk based approach?

Evaluation of overall risks at the financial statement level. |

Consideration of controls at the entity level. |

Evaluation of accounts, disclosures, and assertions for which there is a reasonable possibility of material misstatement. |

how does a lack of a written asseration effect attestation arangements

Guidelines if written assertion isn’t given | ||

| If responsible party = engaging party | If responsible party ≠ engaging party |

Assertion-based examination | 1. Withdraw 2. Disclaim | Restrict |

Review | 1. Withdraw 2. Restrict | Restrict |

Agreed upon procedures | 1. Modify the report | Restrict |

compare examination, reviews and agreed upon procedures on teh following categories

Independence Required? |

Written assertion required? |

Type of report |

Level of assurance |

Amount of Evidence |

Documentation (working papers) required? |

Issue | Examination | Review | Agreed-Upon Procedures | |

Assertion-based | Direct | |||

Independence Required? | Yes | Yes | Yes | Yes |

Written assertion required? | Yes*

| No | Yes* | No |

Type of report | Opinion | Opinion | Whether a material modification is needed | Findings of procedures |

Level of assurance | High | High | Limited(negative) | Findings of specific procedures |

Amount of Evidence | Sufficient and appropriate to support opinion | Sufficient and appropriate to support opinion | Sufficient and appropriate to support conclusion | Findings of specific procedures |

Documentation (working papers) required? | Yes | Yes | Yes | Yes |

compare types of complaince reports on the following situations

Assurance |

Requirements |

Noncompliance |

Standards |

Other Notes |

| Auditor may be asked to report on compliance with contractual agreement requirements in connection w a FS audit | Attestation engagement regarding an entity’s compliance with requirements of specific laws and regulations or on IC over compliance | May report on compliance and IC over compliance as part of a single audit when auditing a recipient of federal financial assistance | |

Agreed Upon Procedures | Examination | |||

Assurance | Negative | No Assurance | Reasonable Assurance | Reasonable assurance for each major program, no assurance for nonmajor |

Requirements | Must have done the FS audit and expressed a qualified of unmodified opinion

Must have a direct and material effect on income statement

| - Responsible party must accept responsibility for the entity’s compliance with the requirements - The responsible party evaluates the entity’s compliance with specified requirements or the entity’s internal over compliance | - Responsible party accepts responsibly for the entity’s compliance with specified requirements and the effectiveness of the entity’s IC over compliance - The responsible party evaluates the entity’s compliance with specified requirements - Sufficient evidential matter exists or could be developed to support management’s evaluation |

|

Noncompliance | Should describe If adverse or disclaimer of opinion was expressed on FS you can only issue a report on noncompliance if there are identified instances of noncompliance | Just report on procedures don’t say noncompliance |

| Give a qualified or adverse opinion for each major program Immaterial instances should be reported but not specifically identified |

Standards | Auditing Standards(SAS) | SSAE | GAGAS, GAAS and 2 CFR 200(maybe) | |

Other Notes |

| Could be an engagement to assess compliance with specified requirements or IC over compliance or both | Auditor expresses and opinion on FS and considers compliance | |

Who created the following standards

SAS

SARRS

SAEE

AS

SAS: AICPA - accounting standards board

SARRS: AICPA- Accounting and Review Services Committee

SEAA- AICPA Accounting standards board

AS- PCAOB

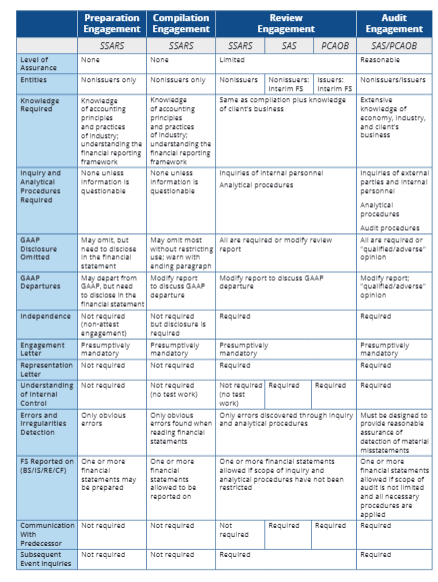

Answer the following for hte different SSARRS engagments

Is assurance provided? |

Is an engagement letter required? |

Is a report required? |

May the FS be released to users other than management |

May the FS omit disclosures(notes)? |

Issue | Preparation | Compilation | Review |

Is assurance provided? | No | No | Limited |

Is an engagement letter required? | Yes | Yes | Yes |

Is a report required? | No | No | Yes |

May the FS be released to users other than management | No | yes | yes |

May the FS omit disclosures(notes)? | Yes | Yes | No |

when unaudited FS are shown with audited ones how should they be referred too

SEC:

not referred to in auditors reprot

but marked unaudited

NONSEC

empahsis paragraph

how does a review report included in a regraition statement look?

If a report on a review of interim financial information is presented in a registration statement, the prospectus should include a statement that the report is not a "report" or "part" of the registration statement. The accountant should also read the other portions of the registration statement to ensure that his or her name is not used in a way that indicates greater responsibility than he or she intends.

Summarize the following engagements on teh following categories

Engagements

prepartion

compilation

Review(normal,interim-issuer&nonissuer)

audit

Categories

Standards

level of assurance

entities

knowledge required

inqury and anlytical procdures required?

GAAP discolsure ommitted

GAAp departures

inpendence

Engamgent letter

Rep Letter

Understanding of IC

error and irregusarlities detection

FS reporting on (BS/IS/RE/CF)

Communication wiht predessor

Subsequent event inqury

According to the AICPA code of professional conduct, what is a covered member?

an individual on the attest engagement team

an individual in a position to influence the attest engagement

a partner who provides more than 10hrs of non-attest services to the attest client within any fiscal year

a partner in the office in which the lead engagement partner primarily practices in connection with the attest engagement

the firm including, the firm’s employee benefit plans

an entity for which operating, financial or accounting policies can be control by any of the individuals or entities described above

Regulation S-X provides three conditions that must b emet for issuers to reiceve on-audit services without impairing indepndence. What are theese?

A. | Non-audit services with revenues in aggregate of less than 5% of the total revenues paid by the issuer to the auditor during the fiscal year in which the non-audit services are provided. | |

B. | Non-audit services that were promptly brought to the attention of, and approved by, the audit committee prior to the completion of the audit. |

Services that the issuer did not recognize as non-audit services at the time of the engagement. |

between reviews, audits, and exmanations which require considerations of fraud risk:

which require considerations of fraud risk:

audits and examination

according to the AICPA how can independence be impaired by financial interests

(material or immaterial) direct or (material) indirect finacnial interest

Direct:

stock ownership even in a blind trust

financial interest through a partnership if the member is a general partner

financial interest in a trust when the member is a trustee

in direct:

member owns shares in a mutal fund that invests in a cleint

member owns direct fincail interest in company A and company A invests in the client

Also impaired

member or immediate family member has a loan from teh cleint

given more than a token gift

close realtive has finacail interest or influnce over the client

not impaired

fully colleratlized car loan

cash advance or credit card not exceeding 10,000

bank account, fully insured by teh govenment

passbook loan

According to the AICPA when is indpendence impaired by employment

cannot be on an engagemnt if you were employed by the cleint during the tiem perod of the engagment

close realitve in key posistion

leave the frim to join teh client in a key possition(1 year wait period)

discuission of employement

According to the PCAOB, how could financial relationships threaten independence

again: an direct or materail indirect relationships by covered members or family

includes:n

direct investments(even if through an intermediary)

benecifical ownership of more than 5% of an audit’s clients equity securties

services as an excuter or voting trustee of an esate that holds the clients securites

Also:

loans from a cleint unless in teh normal course of business with standard rates or before they were a covered person

savings and checking amounts that exceed teh FDIC

broker dealor accounts if there are things other than cash or securites that eceed FDIC

futures commissions merchant accounts

consumer loaons in excess of 10,000

finacnial interest in an invesmtnet company complex that includes client

exceptions

securites thorguh an unsolicted gift or inehratiance disposed of within 30 days(ASPA)

if they got rid of it before the earlir of the engagment letter and commnecment of audit dates

covered family member has interset du eto employment retirement plan but again disposes of it in 30 days

when can an auditor expose a client’s name?

An ethics ruling related to the Confidential Client Information Rule states that it is permissible for a member to disclose the name of a client without the client's consent unless the disclosure of the client's name results in the release of confidential information.

Who created COSO

AAA, AICPA, FEI, IIA, IMA

3 objectives of COSO

reliability of financial reporting

effectiveness and efficiency of operations

compliance with appliable laws and regulations

Organizational structure in COSO

entity level

division

operating unit

function

Components/principles of COSO

these are necessary to achieve objectives

Control Environment

Risk Assessment

Information and communication

monitoring activities

existing control activities

What is associated with the control environment aspect of COSO

commitment to ethics and integrity

Board independence and oversight

Organizational structure(reporting lines)

commitment to competence

accountability

Principles within risk assessment of COSO

specific objectives

identify and analyze risk

consider potential for fraud

identify and assess changes

Principles within information and communication of COSO

obtain and use information

internally communicate info

communication with external parties

Principles within monitoring activities of COSO

ongoing and separate evaluations

communication defciencies

Principles within excisting control activities of COSO

select and develop control activities

select and develop technology controls

deployment of polices and procedures

Remember this isn’t a principle but there are 4 types of controls:

SOD - ACR

Physical controls

information processing controls

General controls: overall information process environment

Application controls: processing of individual applications and help ensure teh occurrence(validy), competences and accuracy

performance reviews

who are the following people within teh investment cycle”

registrar

transfer agent

trustee

investment advisory services

- Register: maintains the official shareholder ledger and number of shares issued and outstanding

- Transfer agent: manages ownership records and share counts

To find the number of shares issued and outstanding, you’d check with the registrar because they maintain the official master record of total shares and shareholders.

To find who owns which shares (like for related party investigations), you’d ask the transfer agent, since they handle the detailed ownership records and process transfers.

- Trustee: holds bonds and ensures rules are being followed

- Investment advisory services: this is like Moody and they keep track of dividends

What is the special cycle and what is special about it

In the revenue there is a presumption of fraud, thsi requires that auditors to do analytical procedures in both teh planning and review stages

Name 3 things often not done in a review engagmeent

1 | Tests of the accounting records. |

2 | Tests of management's assertions regarding continued existence. |

3 | Inquiries of the entity's attorney concerning contingent liabilities. |

What justifies a departure from GAAP

New legislation

The evolution of a new form of business transaction (for example, cryptocurrencies or blockchain)

when an auditor does an audit of an nonissuer what do they need to do?

must have a written asseration

must have done the FS id inconncetion with finacnal reporting

otheriwse its fine

Due to 50 percent store growth year after year, monitoring controls at a national retail chain has come under tremendous pressure. According to COSO, which of the following responses would be appropriate under the circumstances to help restore effective monitoring?

When the size of an organization grows substantially, it becomes more difficult to effectively monitor from only the top level. An effective strategy to ensure that monitoring is done across the organization is to shift monitoring responsibility to all of the store and district managers—essentially transferring the responsibility to the local rather than the central level.

What is used in explanatory, emphasis of matter, and other matter paragraphs

Emphasis of matter:

material justified change in accounting principle

change in audit opinion

Special-purpose framework

Other matter

change in audit opinion

FS of prior period were audited by a predecessor auditor and the predecessor’s audit report is not reissued

comparative FS when PY wasn’t audited

Restrict of use of report

report on compliance in audtior’s report

Explanatory

material justified change in accounting principle

change in audit opinion

Special-purpose framework

FS of prior period were audited by a predecessor auditor and the predecessor’s audit report is not reissued

comparative FS when PY wasn’t audited

Restrict of use of report

report on compliance in audtior’s report

Otherinfomraitno

supplmentary information

RSI

DoL independce standards

Direct Financial interest

Material indirect financial interest

Former employee of the client participates on teh engagement team when teh client covers any period of the individual’s employment with the client

Disallowed services:

bookeeping

management services

service as broker, dealer, investment advisor, or IB

leading, lagging, and coincident economic factors

§ Average duration of unemployment

§ GDP(gross domestic product)

§ Interest rate spreads(10-years treasury bond versus federal funds rate)

§ Consumer price index for services(CPI)

§ Manufacturing and trade sales

§ Average weekly unemployment insurance claims

§ Producer price index(PPI)

§ Industrial production

§ Bond yield curve increase

o Leading: predict future:

§ Average weekly unemployment insurance claims

§ Bond yield curve increase

§ Interest rate spreads(10-years treasury bond versus federal funds rate)

§ Producer price index(PPI)

o Coincident: happening at the same time

§ Industrial production

§ Manufacturing and trade sales

§ GDP(gross domestic product)

o Lagging indicators: after the fact

§ Average duration of unemployment

§ Consumer price index for services(CPI)

What is communication with the predecessor auditor before the audit

inquiry is required with client permission

inquire before accepting engagement about:

fruad

noncomplaince

manamnget integrity

disagreements

change in auditior

communication w/ management, audit committee and those charged with governance about IC

RP and significant unusual transactions

how does the reissuance or lack of reissuance effect the audit report

Yes reissued:

predecessor auditor should”

read and compare PY to CY

obtain a rep letter from management and CY adutior

date:

if revised: dual date

if unrevised: OG date

No, not reissued:

Use another matter or explanatory paragraph

Do not name predecessor auditor

state opinion and reasoning if unmodified

nature of any emphasis of matter, other matter, or explanatory paragraph

date of the old report

Discuss AP confirmations, when are they used, on what accoutns, should they be posistve, negative or both

they are only used when external evidence cannot be secured

the are used on small or empty account

they should be blank or positive

What does substance over form mean in relation to testing IC

"Substance over form" concerns relate to controls that appear on the surface to exist but in reality are not operating effectively. When obtaining an understanding of a client's system of internal control, an auditor should concentrate on the substance of controls rather than the form because even when appropriate procedures are established, management may not enforce compliance.

what should be included in a going concern paragraph. what if substantial doubt has been alleviated? what if disclsoures are inadequate?

Nonissuers: get their own section, Issuers: explanatory

include the words “substantial doubt” and “going concern”

Alleviation:

nonissuer: optional emphasis of matter paragraph

if there was a going concern doubt in a previos period, but it has been alleivated you should not repeat the paragrpah this period

inadequate:

could give a qualified or adverse opinion

when do auditors talk to regulatory or enfromcement agencies

Regulatory or enforcement authorities (e.g., SEC):

When required by law or regulation (e.g., SEC for auditor changes or material fraud).

In response to court orders or subpoenas.

For entities receiving government financial assistance, to the funding agency.

must report change in auditors to SEC

and OFC successor aduitors

Does teh auditor document the sepcific page number of SAS they are following in thier documentation

NO

In which situations should disagreements with management and significant audit adjustments be communicated to those charged with governance?

Disagreements with Management | Significant Audit Adjustments | ||

|---|---|---|---|

A. | Communicate even if the issue has been | Communicate regardless of whether |