Financial insolvency

1/8

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

9 Terms

What is insolvency

When a company or person can’t pay back their debts as they fall due

What is financial distress

The stages before and including insolvency

Types of insolvency and explain

Cash flow/flow based insolvency

when a firm doesn’t have enough cash to meet its contractually obligated commitments

essentially cash rich, house poor

common in young firms or firms waiting on AR

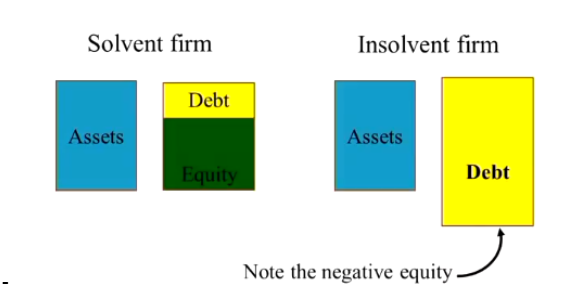

Balance sheet insolvency

when the value of a firms assets is less than the value of debt.

essentially cash poor and house poor

Equity no longer exists since equityholders are residual claimants so they get wiped out the second debt=assets

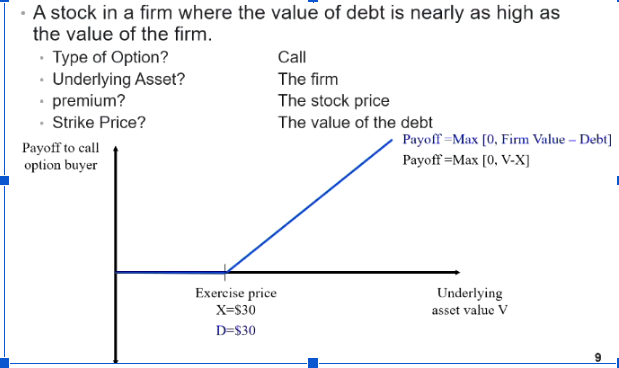

How is equity similar to a call option

Type of option: call option

underlying asset: the value of the firm

strike price: value of debt

premium: equity value/stock price

hence shares in a firm with financial distress are still considered valuable because volatility increases the chance of it being in the money

Distortions arising from financial distress

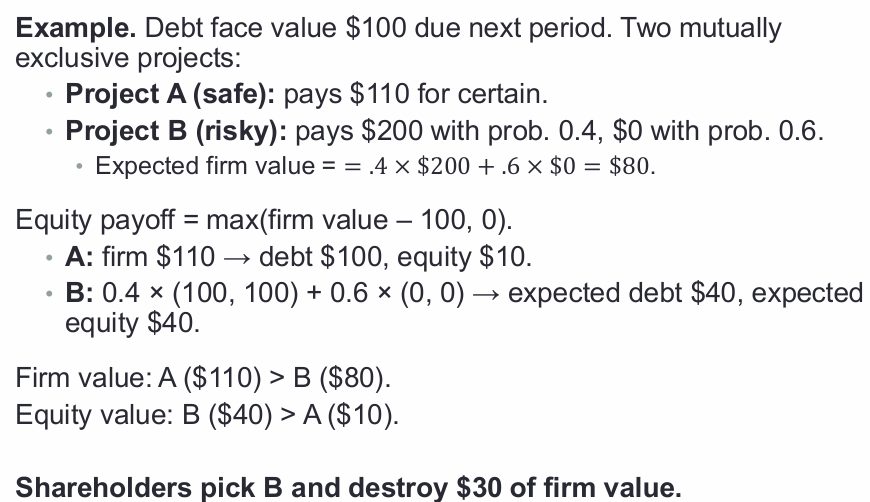

asset substitution

tendancy for managers to pursue excessive risk-taking investments because the upside to shareholders is unlimited but their downside is limited

hence in the example, even though the more certain option increases firm value, equityholders still prefer the risky one since it increases their expected return.

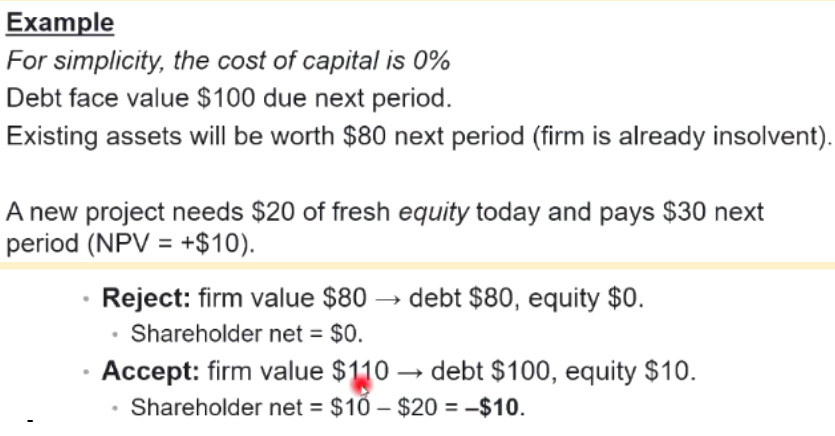

Debt overhang/underinvestment

incentive for managers to underinvest in good projects because most of the benefit goes to creditors/lenders.

Options when firm is in financial distress

liquidation(if the firm is worth more dead to debtholders) or reorganisation(if the firm is worth more alive to debtholders)

Reogranisation

keep the firm operating just restructure the claims

ie. such as issuing new securities to replace old ones, or selling assets to raise cash, engiotating with creditors to reduce debt or issuing new equity in a new company

if things are too bad, the firm goes into voluntary administration

this is when independent registered liquidator who takes control of the company and they decide if company should be saved or liquidated

this gives time for third parties or management to see if they can save the company

Voluntary administrator proposes a DOCA which is a binding agreement between the company and creditors regarding how the company will be handled and how much creditors will be paid

If creditors approve DOCA, company is saved, if not it gets liquidated

Liquidation

assets are sold for salvage and the proceeds go to paying creditors in order of priority

Liquidation costs:

Paying lawyers, pay liquidator fees

Secured creditors: paying creditors with secured assets (where the debt is guaranteed by some asset, ie. if you borrowed money for a company car, if you didn’t pay them back they would just take the car)

Employee entitlements: super, wages

Unsecured creditors: suppliers, customers (in order of seniority)

Shareholders

Z-score critera:

is less than <1.81: high prob of insolvency

if more than >3, low prob of insolvency