AP Microeconomics Unit 3

1/50

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

51 Terms

Marginal Product (MP)

The additional output produced when 1 additional unit of a resource is employed (the quantity of all other resources employed remaining constant);

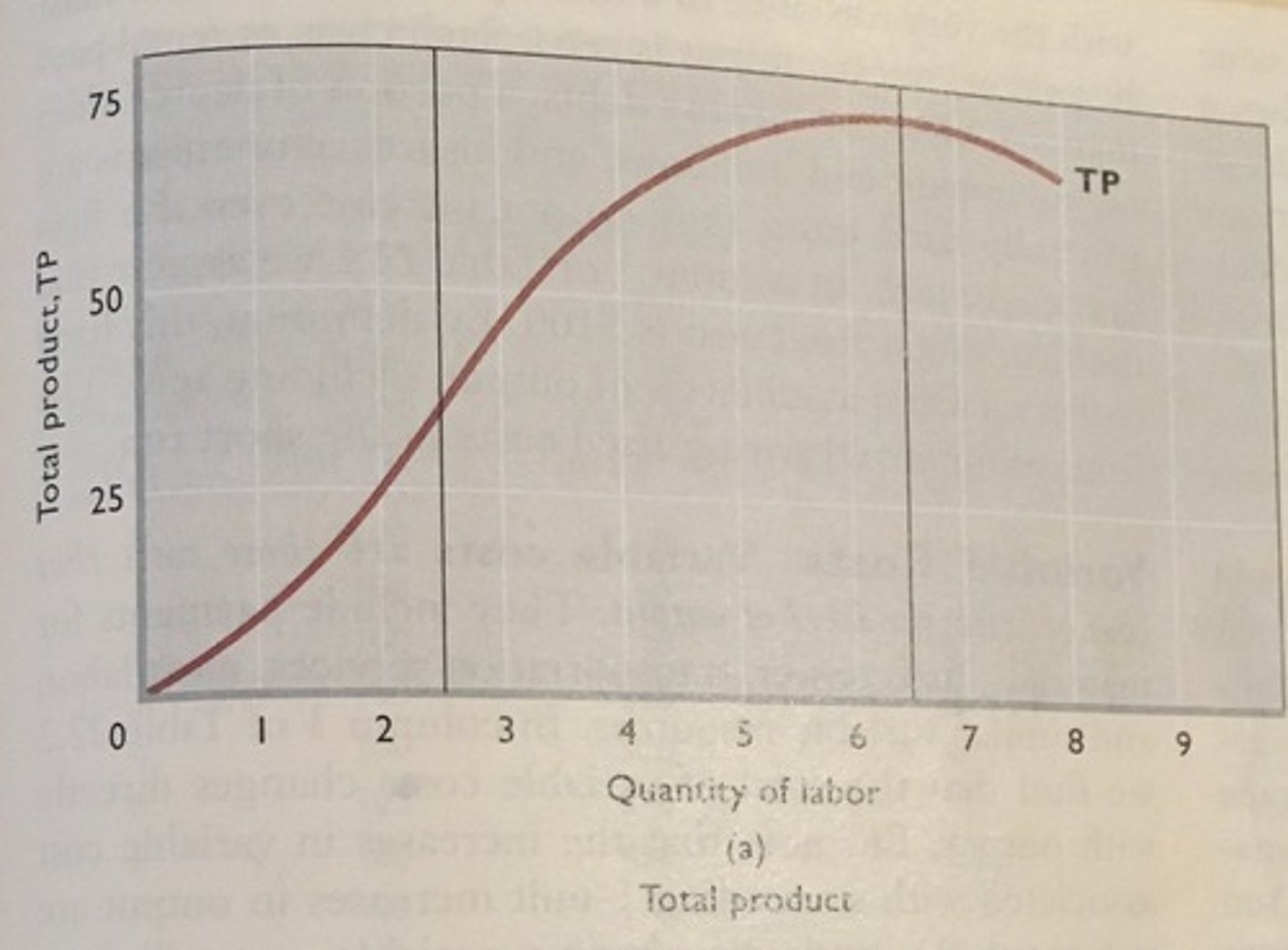

Total product (TP) or total output (Q)

total number of units of output produced by the firm per period of time

Average Product (AP)

output per unit of input

diminishing marginal product

MPP diminishes as the firm uses additional units of labor

marginal cost in output increases and the marginal product of labor decreases as each additional unit of input is added

bottom of MC curve

total product curve

shows how the quantity of output depends on the quantity of the variable input, for a given quantity of the fixed input

Per-unit cost curve

shows the change in per unit cost from one input extra, ceteris paribus

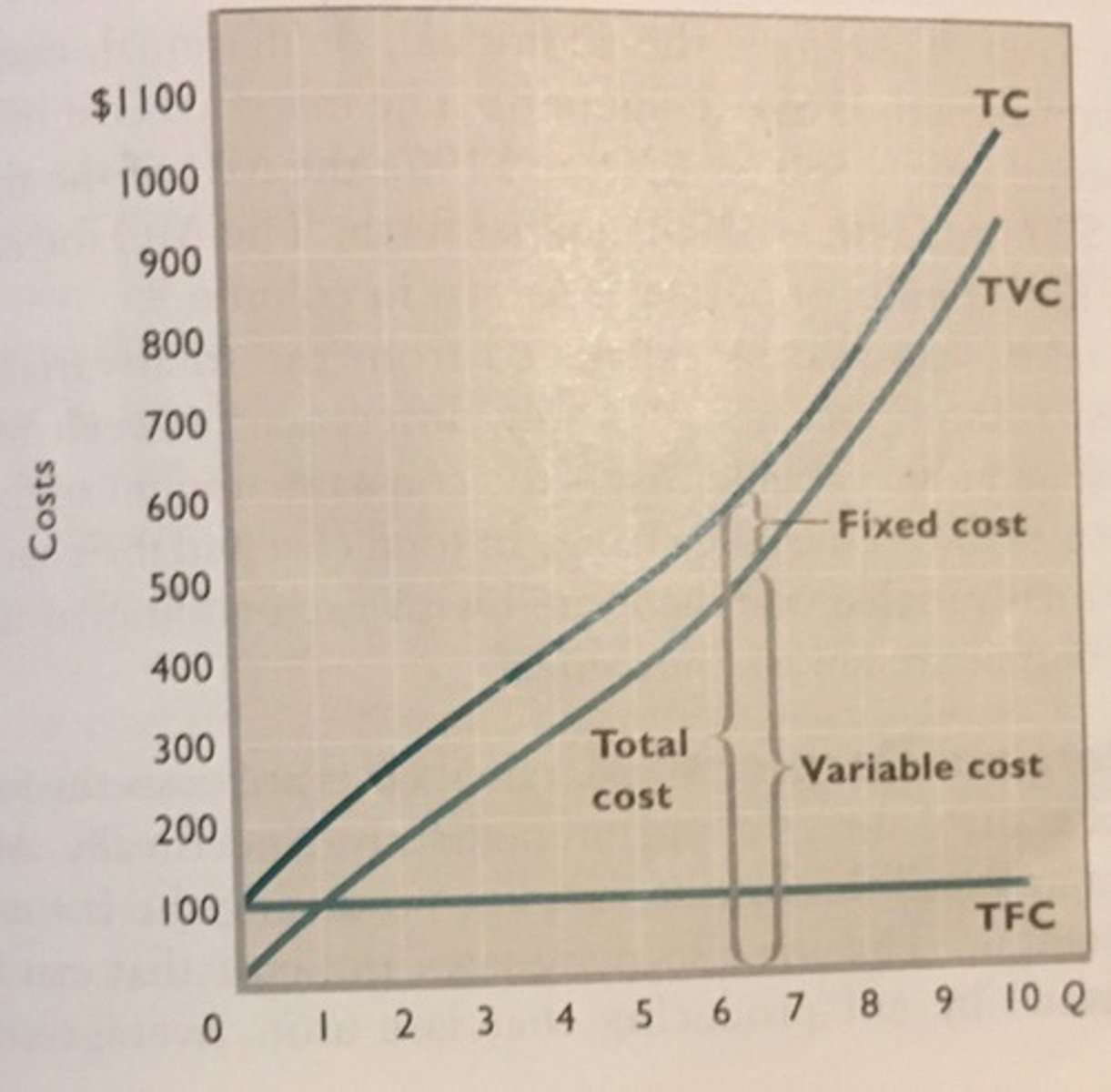

Total Cost (TC)

shows the change in total cost from one input extra, ceteris paribus

Fixed costs

costs that do not vary with the quantity of output produced

Average fixed costs (AFC)

fixed cost per unit produced

AFC = TFC/Q

AFC = ATC - AVC

Variable costs

costs that vary with the quantity of output produced

Average variable costs (AVC)

variable cost per unit produced

AVC = TVC/Q

AVC = ATC - AFC

AVC = wage/APP

Total cost (TC)

sum of fixed costs and variable costs

TC = TVC + TFC

Average total cost (ATC)

total cost per unit produced

ATC = TC/Q

ATC = AVC + AFC

Marginal cost (MC)

cost of producing an additional unit of a good (variable cost)

MC = ∆TC/MPP

MC = wage/MPP

Marginal revenue (MR)

additional income from selling one more unit of a good

MR = price of good per unit

Economic profit

price is above the minimum of the ATC curve

total revenue - (implicit costs + explicit costs)

Economic loss

price below the minimum of the ATC curve

Normal profit

price on the minimum of the ATC curve

What are the characteristics of perfect competition

many firms with no entry barriers

firms maximize profits and are price takers

identical products (perfect substitutes)

no long run profit and have perfect information

no control over price or advertisements

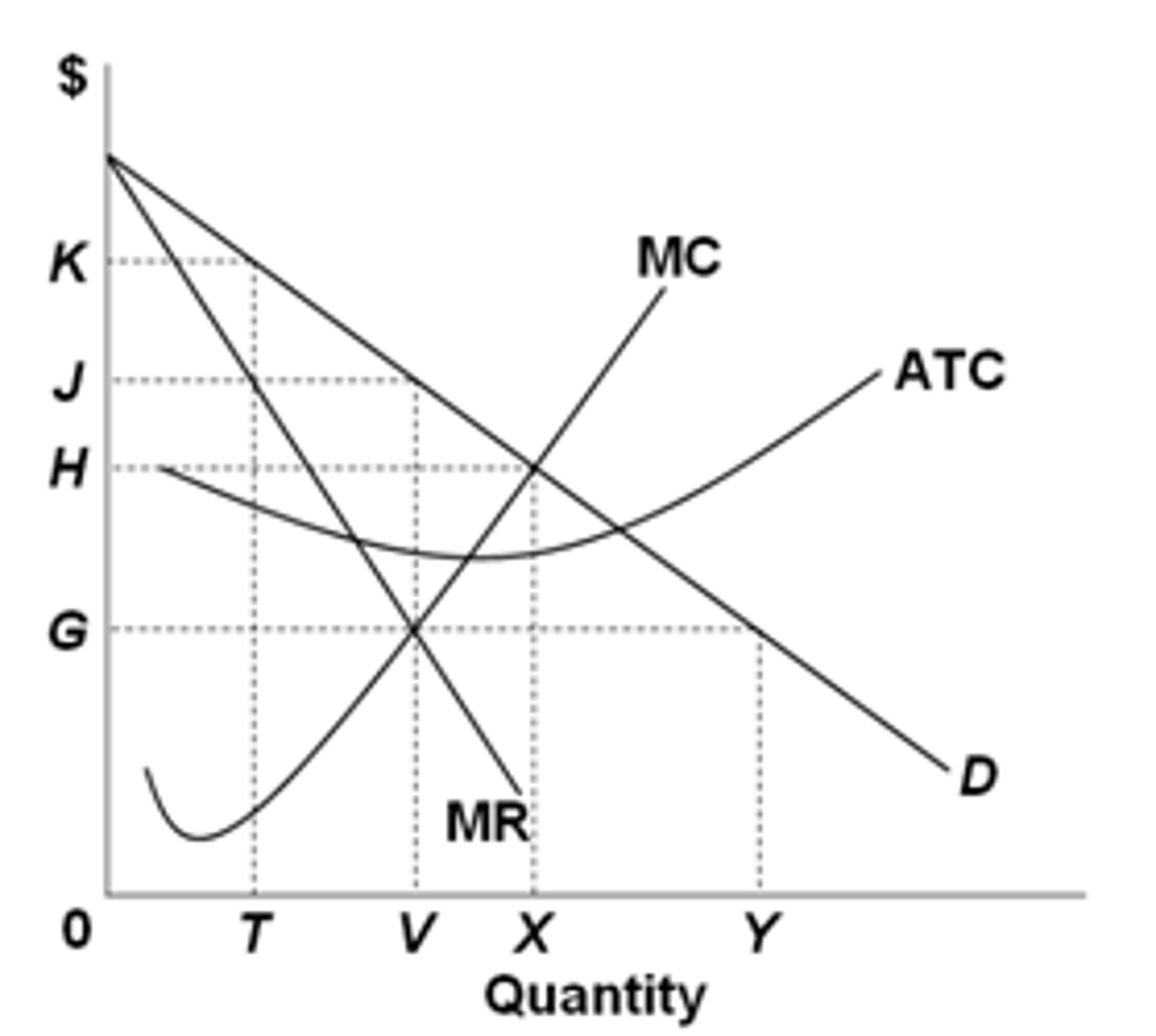

What are the characteristics of a pure competition graph

demand is perfectly elastic labeled MR = D = AR = P

supply is MC above AVC

ATC touches the MC at its lowest point and is always above AVC and AFC

AVC touches the MC at its lowest point and approaches (but never touches) the ATC

AFC is perpetually decreasing

MC is shaped like a swoosh

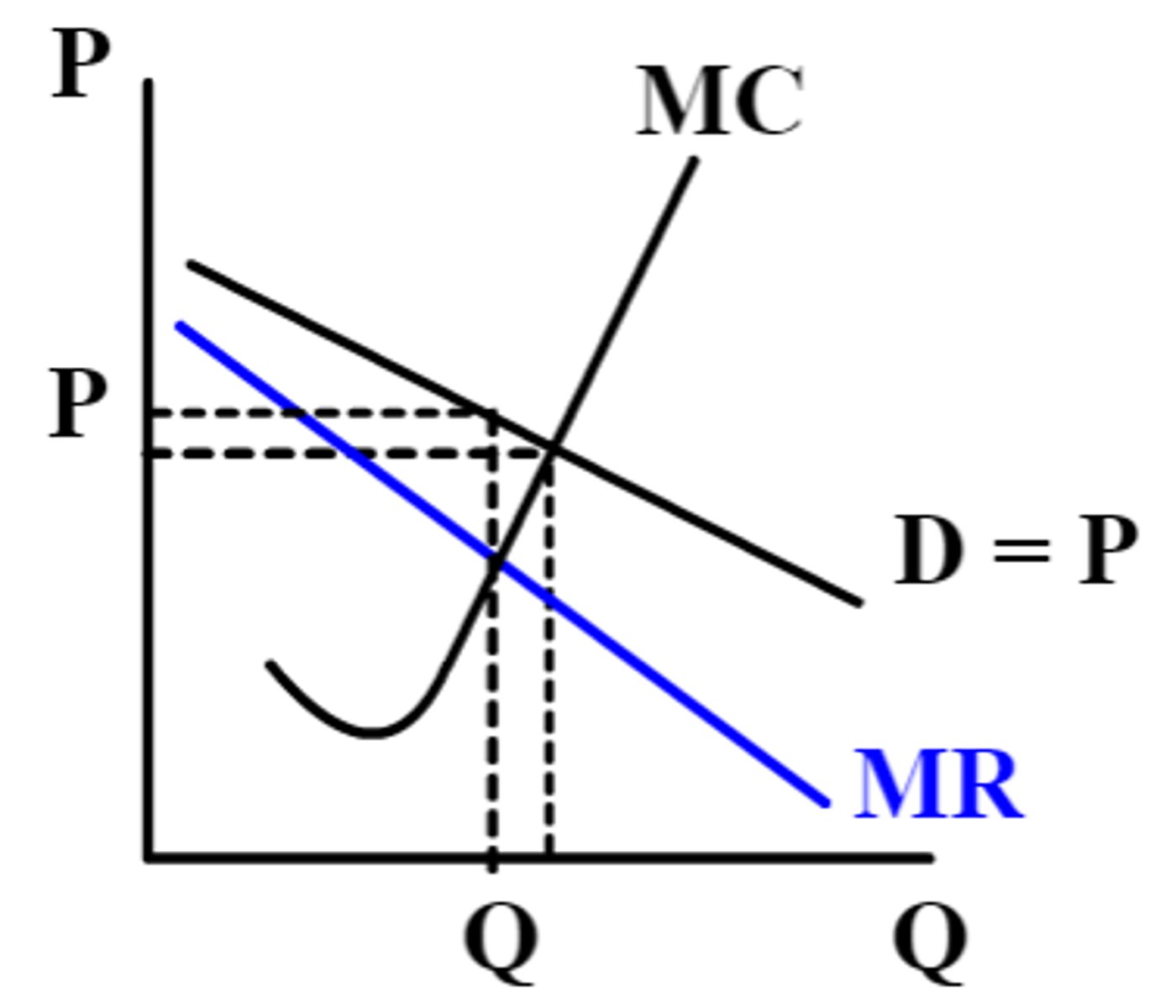

Optimal output (profit maximization)

wherever marginal revenue (MR) = marginal cost (MC)

Total revenue maximization

wherever marginal revenue (MR) = 0

Short run average total cost (SRATC)

period of time during which at least one of a firm's inputs is fixed

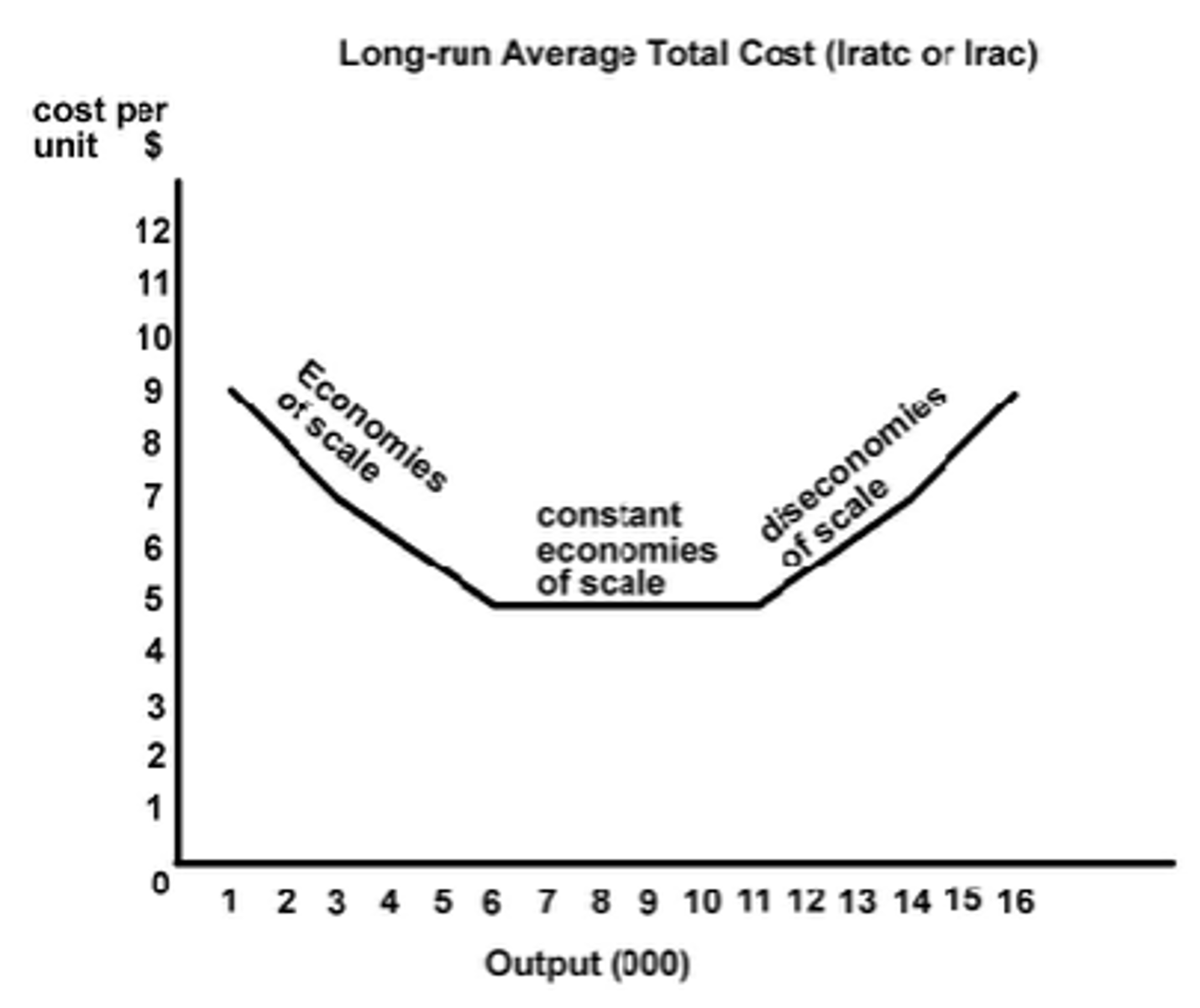

Long run average total cost (LRATC or planning curve)

period of time in which a firm has paid off all of its fixed costs

consists of many increasing then decreasing SRATC curves of various plant sizes available to a firm

price = minimum ATC

Productive efficiency

producing a good in the least costly way (minimal use of resources)

P = minimum ATC

Allocative efficiency

distribution of resources towards the production of products most wanted by society

P = MC

Shutdown point

point where price is less than minimum AVC and the firm must shut down to minimize its losses

firm should continue to produce as long as it's price is above the AVC

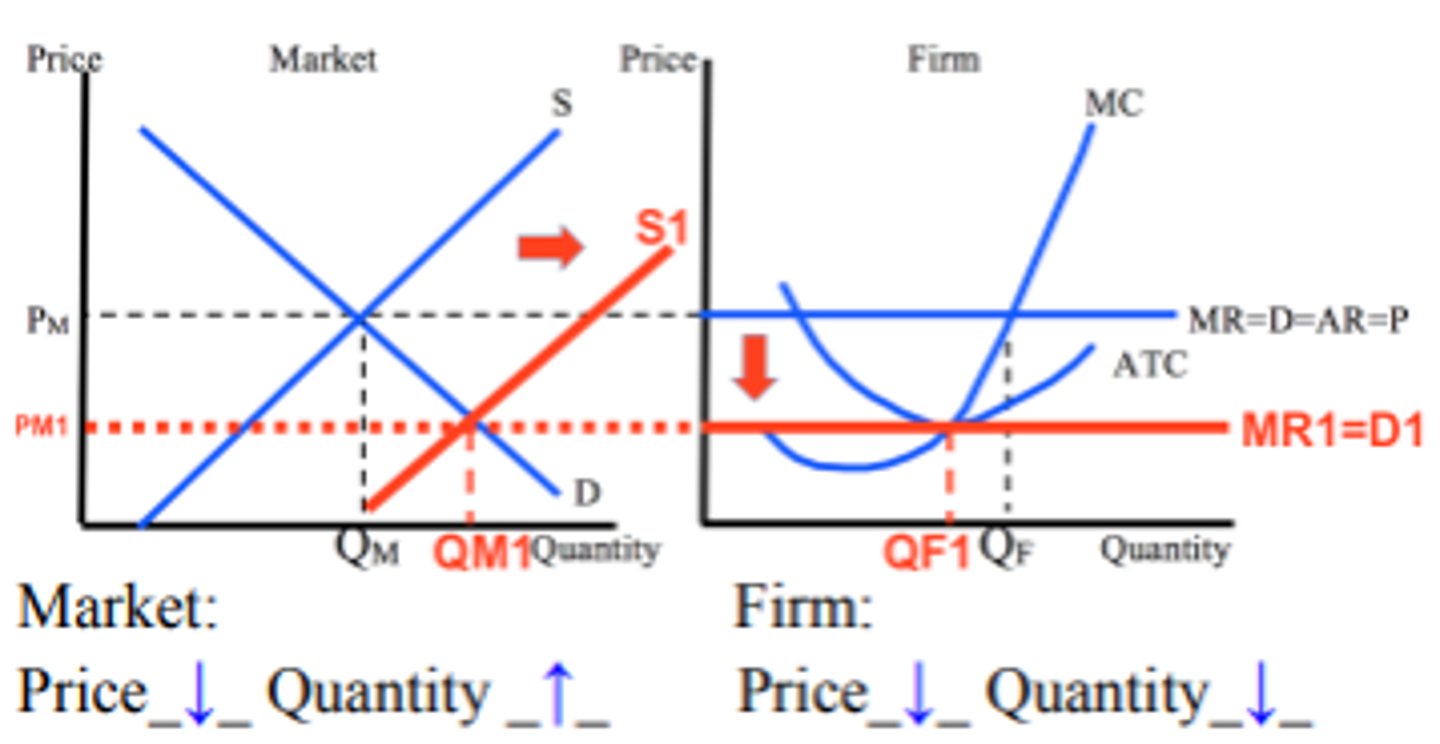

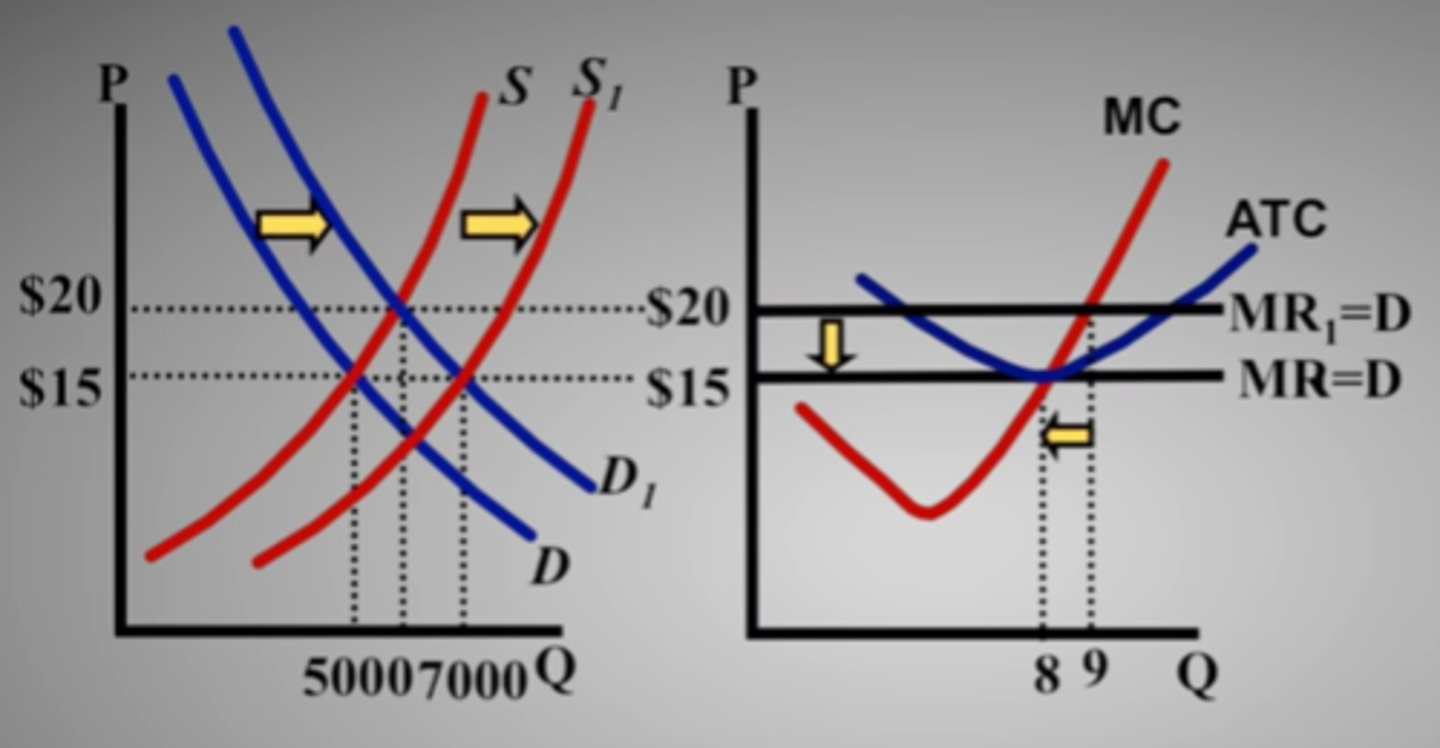

Increase in demand in the short run (perfect competition)

market price and market quantity increases

firm price and firm quantity increases

profit occurs

Increase in supply in the short run (perfect competition)

market price decreases and market quantity increases

firm price and firm quantity decreases

encourages entry into the market

Decrease in demand in the short run (perfect competition)

market price and market quantity decreases

firm price decreases and firm quantity decreases

loss occurs

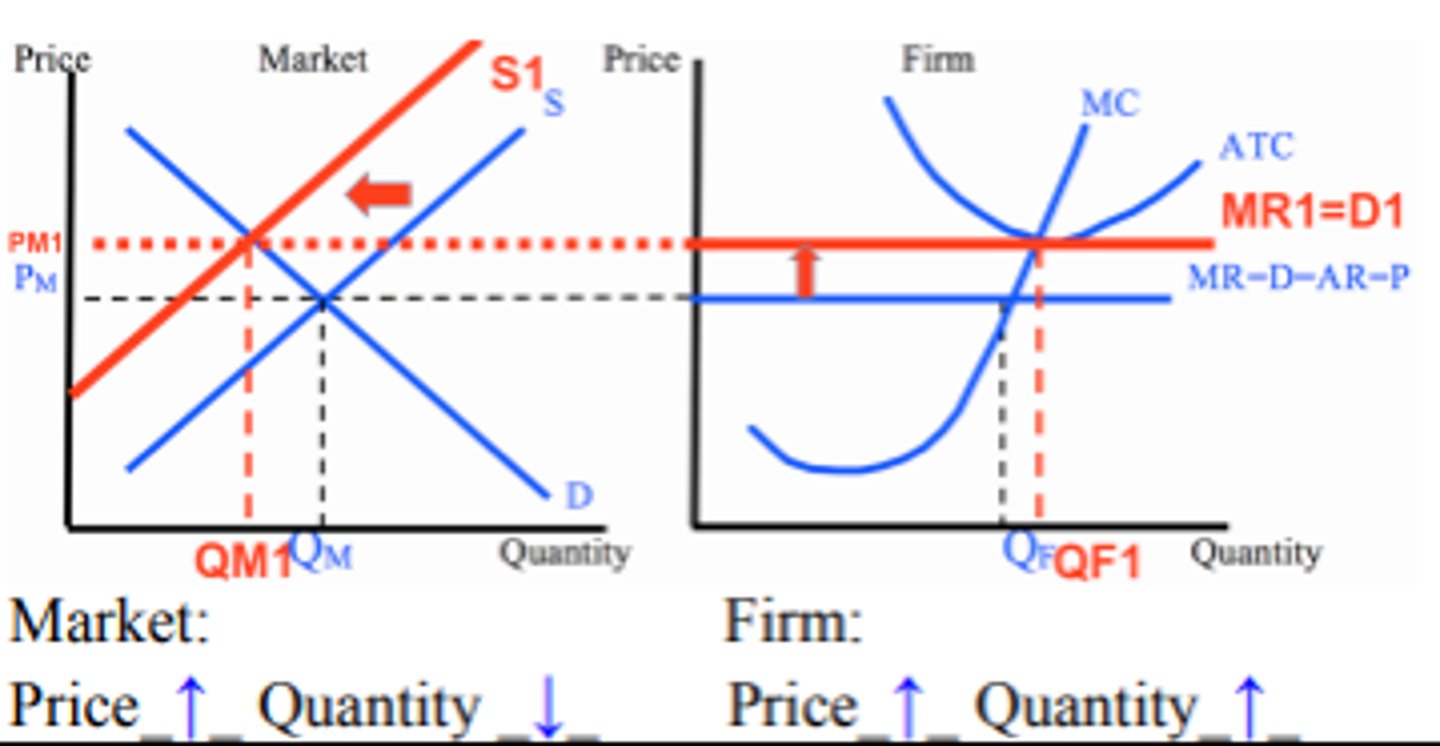

Decrease in supply in the short run (perfect competition)

market price increases and market quantity decreases

firm price and firm quantity increases

encourages exiting out of the market

When will only the ATC shift upwards

fixed costs increase once

price and quantity remain the same

When will only the ATC shift downwards

fixed costs decrease once

price and quantity remain the same

What are the characteristics of a pure monopoly

single firm that is a price searcher

firm has no substitutes

market entry is blocked (no competition)

legality dependent on government approval

earns a profit in the long run by maximizing total profit and selling where price is elastic

causes income inequality

What are the characteristics of a pure monopoly graph

MR slopes downwards from left to right at a faster rate

ATC below MR = MC

profit-maximizing price is the point on the demand curve of the profit-maximizing quantity at MR = MC

D = P ≠ MR

D = P is the demand curve and slopes downwards from left to right

no supply curve exists

creates deadweight loss, has no productive or allocative efficiency in the long run, and an unfair market price

demand is elastic where MR > 0, inelastic where MR < 0, and unitary elastic where MR = 0

When can price discrimination be possible

monopoly power

market segregation

no resale possible

Economies of scale

factors that cause a producer's average cost per unit to fall as output rises and can alter the quantity of all inputs

LRATC decreasing

Constant economies of scale

all inputs can be increased equally to maintain the lowest cost per unit

LRATC constant

Diseconomies of scale

average cost per unit increases in the long run due to size

LRATC increasing

Accounting profit

total revenue - explicit costs

Explicit cost

cost that involves spending money for production

Implicit cost

opportunity cost when a firm uses owner-supplied resources

What are the characteristics of monopolistic competition

many firms that are price searchers

no entry barriers

products are similar but not identical

constant advertising (fixed cost that increases demand and becomes more inelastic)

normal long run profit

market demand curve different (lowering prices does not instantly mean more market share for a firm)

has no productive or allocative efficiency in the long run

What are the characteristics of an oligopoly

few firms that are price searchers

difficult entry barriers

products are similar but not identical

firms are interdependent (decisions dependent on each firm's actions)

firms make their own price

What are the barriers of entry for a monopoly

patents and copyrights

legal restrictions

control of key resources

high startup costs

Changing cost industry in the long run (perfect competition)

quantity remains the same in the firm and quantity increases in the market after prices stabilize

When will firms enter a market,

economic profit is greater than zero

When will firms exit a market

economic profit is less than zero

Decreasing cost industry

industry that faces lower per-unit production costs as industry output decreases in the long run

long run industry supply curve slopes downward

Constant cost industry

industry that faces no change in per-unit production costs as industry output stays the same in the long run

long run industry supply curve horizontal

increasing cost industry

an industry in which expansion through the entry of new firms raises the prices firms in the industry must pay for resources and therefore increases their production costs