Lecture 12 BSM Model

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

15 Terms

BSM model

prices options before maturity

increase in stock price

increase in call value

increase in strike price

decrease in call value

increase in volatility

increase in call value

increase in maturity

increase in call value

increase in risk free rate

increase in call value

increase in dividend

decrease in call value

price of put

price of call

must adjust formula for dividends so that S=So-De^-rt and use new S in d1 and d2

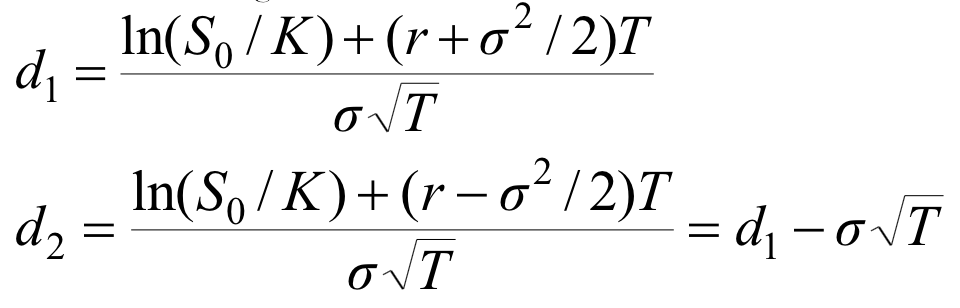

d1 and d2 formula

moneyness

S/K, if greater than 1 then intrinsic value for calls is positive

implied volatility of stock unobservable factor

volatility smile measures volatility with respect to stock price

volatility is minimum ATM

DITM options have high volatility, so banks may sell anyway because could be OTM by maturity

implied σ > actual σ

seller wins, overcompensated for actual amount of risk they took on

pros

foundation for greeks and delta hedging, used as market benchmark

cons

violates constant volatility, cannot price American options, lognormal distribution underprices tail events