Module 6 - Bond Valuation: Prices and Yields

1/16

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

Calculating value of a coupon bond

Summing the present values of all of the bond's promised/future cash flows.

If we know a bond's YTM, we can calculate its value, and if we know its value (market price), we can calculate its YTM.

On calculator use:

N (number of years),

PMT (annual coupon payment),

I/Y (annual discount rate or YTM),

FV (par value/face value of bond received at maturity) buttons to solve for value.

Calculating price of annual coupon bond with N years to maturity :

Calculating price for semiannual coupon bond with N years to maturity:

Yield to maturity

Market discount rate appropriate for discounting a bond's cash flows

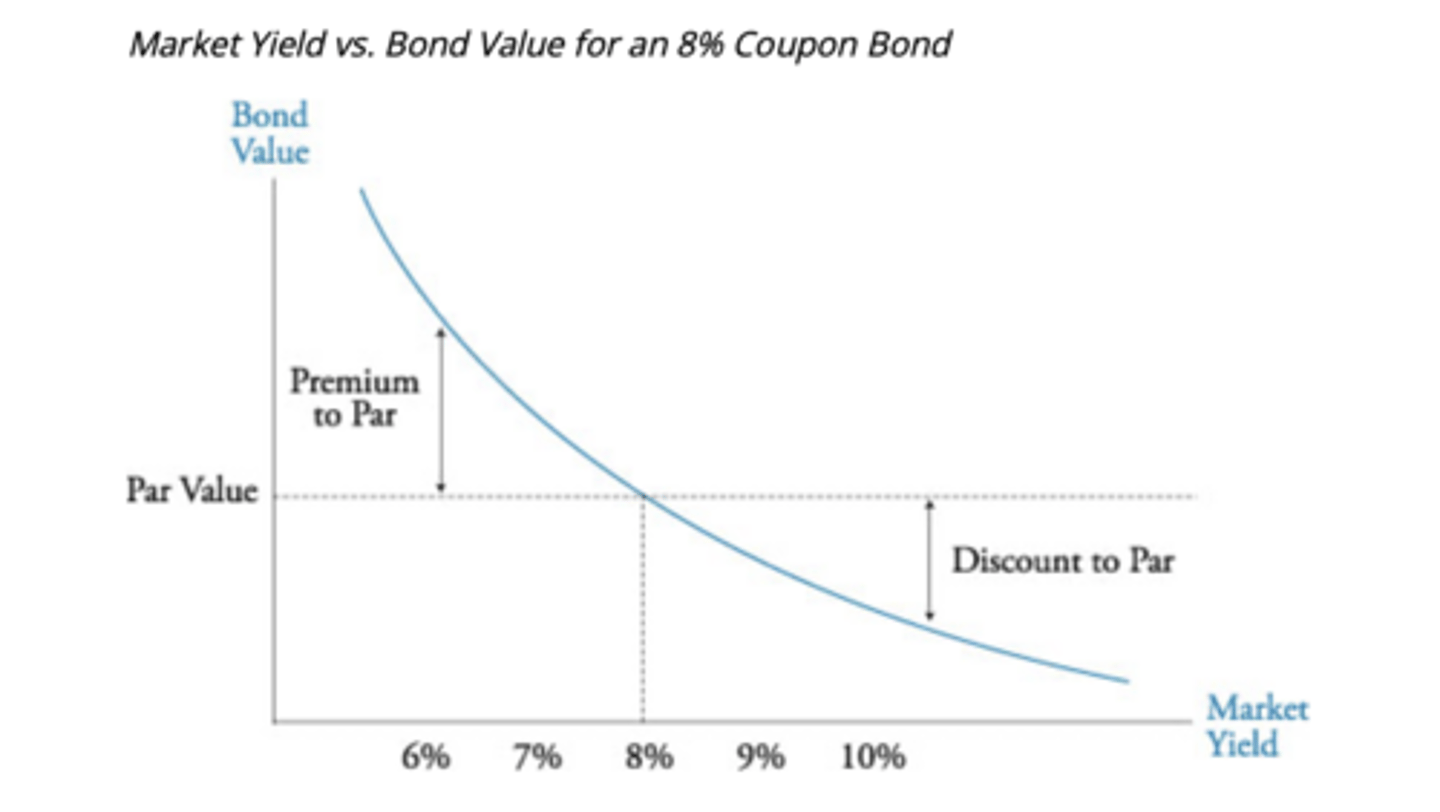

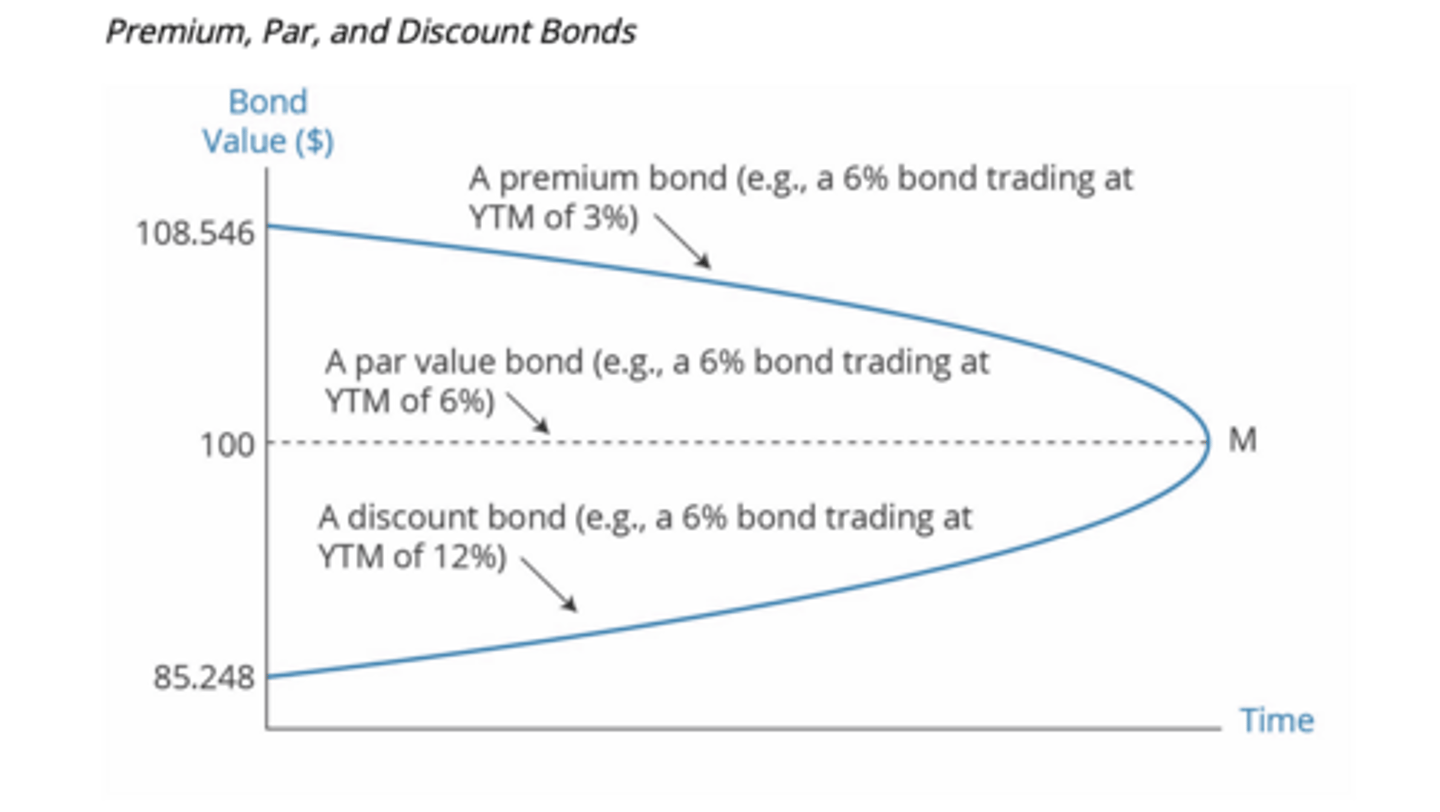

Premium

In the case of bonds, premium refers to the amount

by which a bond is priced above its face (par) value. In the

case of an option, the amount paid for the option contract.

When bond yields decrease, the present value of a bond's payments, its market value, increases. Here, we also see that a bond with a coupon greater than its yield will be trading above par.

Discount

When bond yields increase, the present value of a bond's payments, its market value, decreases. Here, we also see that a bond with a coupon less than its yield will be trading below par.

Calculating value of semi annual coupon bond

For semiannual pay bonds, must DIVIDE YTM by 2 (NOT DOING (1 + YTM)1/2 – 1).

YTM is not an effective annual rate, unless it's an annual-pay bond.

YTM is an effective rate for the coupon period, times the number of coupon periods in a year.

For a semiannual-pay bond, YTM is an effective semiannual rate times 2 periods.

For a quarterly-pay bond, YTM is an effective quarterly rate times 4 periods.

For a monthly-pay bond, YTM is an effective monthly rate times 12 periods.

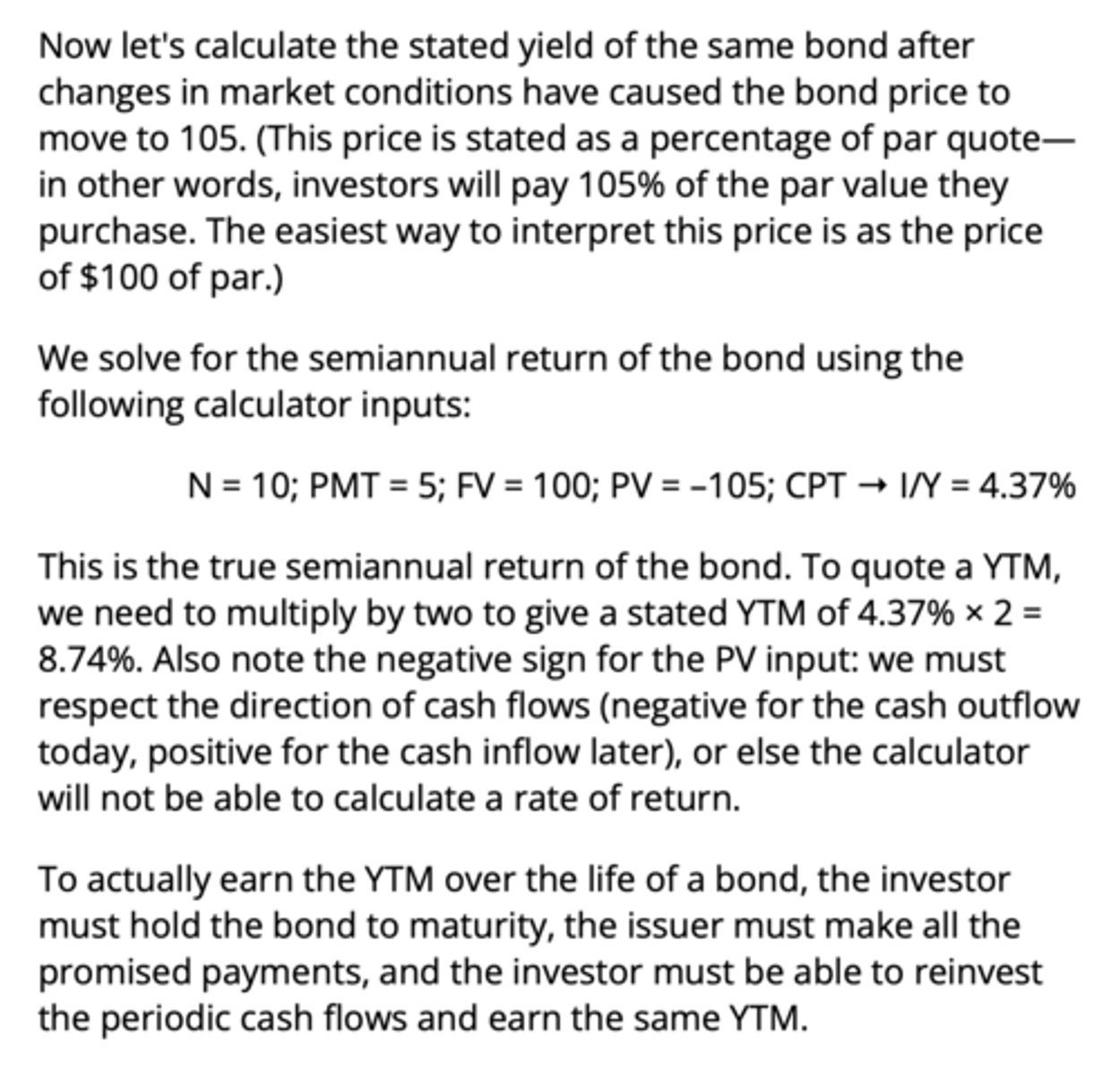

Calculating Yield to Maturity

Accrued Interest

For most actual bond trades, the settlement date, which is when cash is exchanged for the bond, will fall between coupon payment dates.

Bond pricing has to account for the fact that the next coupon will be paid to the buyer, but a portion of it is owed to the seller.

Calculation = coupon payment x days from last coupon to settlement divided by days in coupon period.

Crucial to note: day count methods (x2 options depending on type of bond).

Actual/actual convention (day count method)

Uses actual number of days between coupon payments and actual number of days between last coupon date and settlement date.

Most common used for Government bonds.

30/360 convention (day count method)

Assumes each month has 30 days and a year has 360 days.

Most common used for Corporate bonds.

Price quote of a bond - Flat Price/Clean Price

Quoted WITHOUT accrued interest.

Holding yield constant, incl accred interest would make bond's price appear to increase on each day of a coupon period and drop suddenly on coupon payment date.

Price quote of a bond - Full Price/ Invoice Price / Dirty Price

Theoretically the sum of its flat price and accrued interest. BUT cannot calculate it this way.

To calculate:

1. Calculate value of bond on last coupon date.

2. Compound this value at YTM per period, over the number of days since last coupon payment.

Things to note regarding relationship between price and specific bond features (x4)

1. There is an inverse relationship between yield and price.

2. Price of a bond with lower coupon rate is MORE SENSITIVE to change in yield than the price of bond with a higher coupon rate.

3. Price of a bond with longer maturity is MORE SENSITIVE to change in yield than price of a bond with shorter maturity.

4. % decrease in value when YTM increases by given amount is SMALLER than increase in value when YTM decreases by same amount. Price-yield relationship is convex.

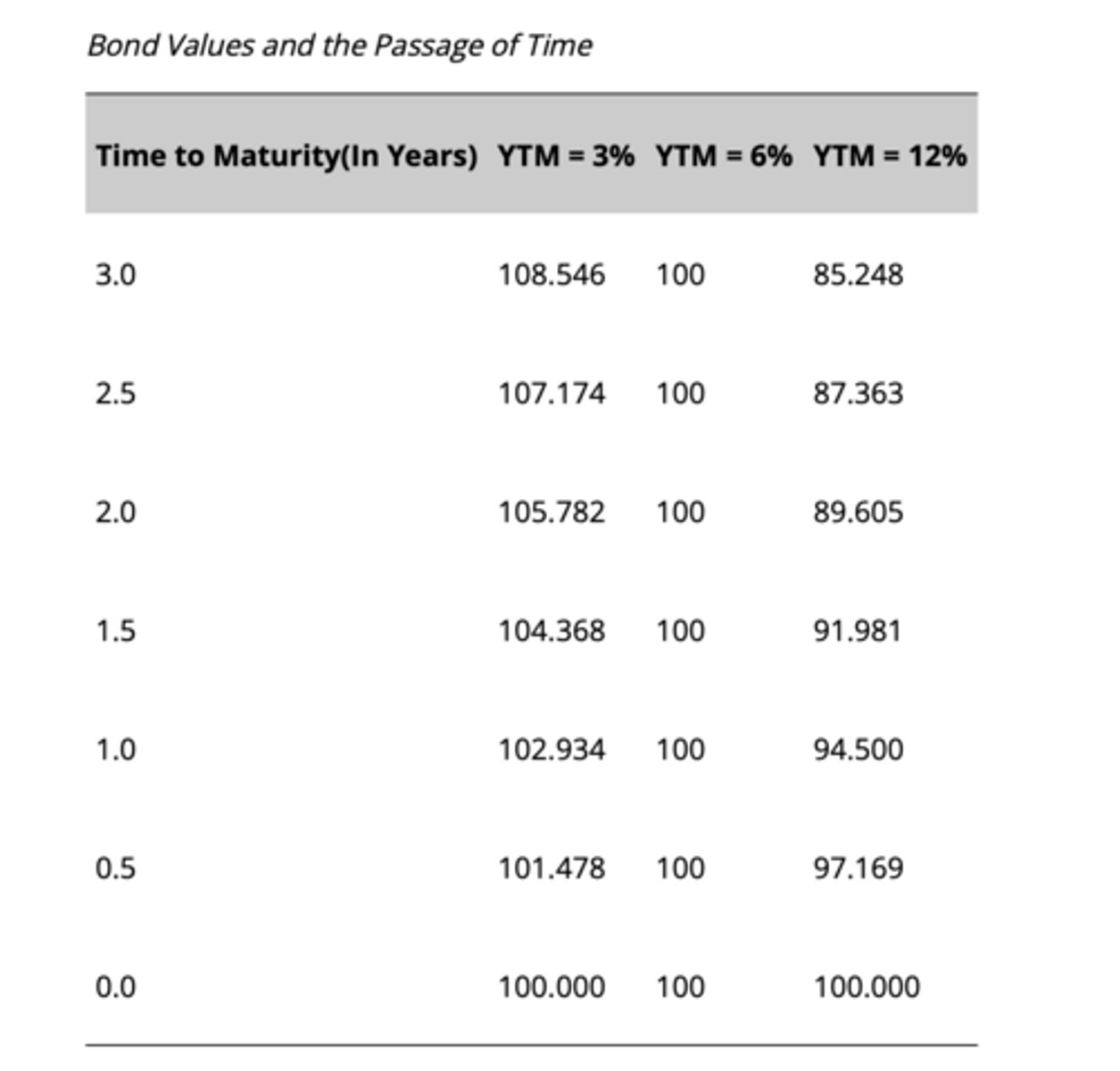

Relationship Between Price and Maturity

Before maturity, bond can be selling at significant discount OR premium to PAR.

BUT regardless of required yield, price WILL get closer to PAR as maturity approaches (pull to PAR).

Constant yield price trajectory

Pull to PAR.

Shows how bond's price would change as time passes if its YTM remained constant.

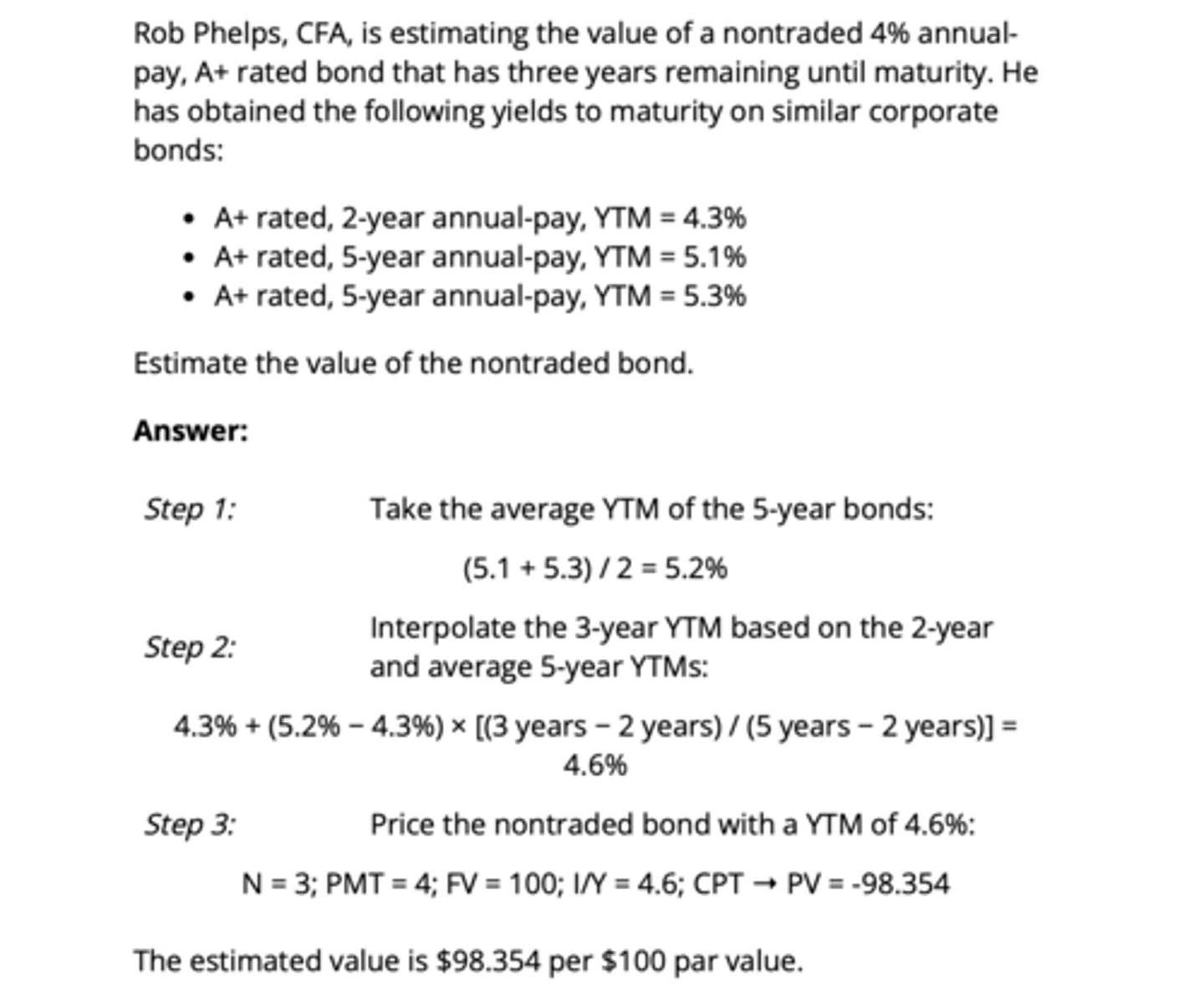

Matrix pricing

Method of estimating required YTM of bonds not currently traded or infrequently traded.

Use YTMs of traded bonds that have credit quality v close to that of non-traded/infrequently traded bonds and that are similar in maturity and coupon to estimate price.

If these traded bonds have different maturities than the bond being valued, linear interpolation is used to estimate the subject bond's yield.